Weak Dollar as a tailwind for Emerging Markets?

Emerging Markets are economies that are in transition to a developed industrialized nation. Typical examples are China, India or Brazil as well as various Southeast Asian countries. Depending on the context, however, countries of the former Warsaw Pact or individual states in Africa and the Middle East are also counted as Emerging Markets. Despite some similarities, this is a heterogeneous group with differences in important areas. However, these countries have one thing in common: they can offer interesting opportunities for various investment strategies.

World trade is being reshaped

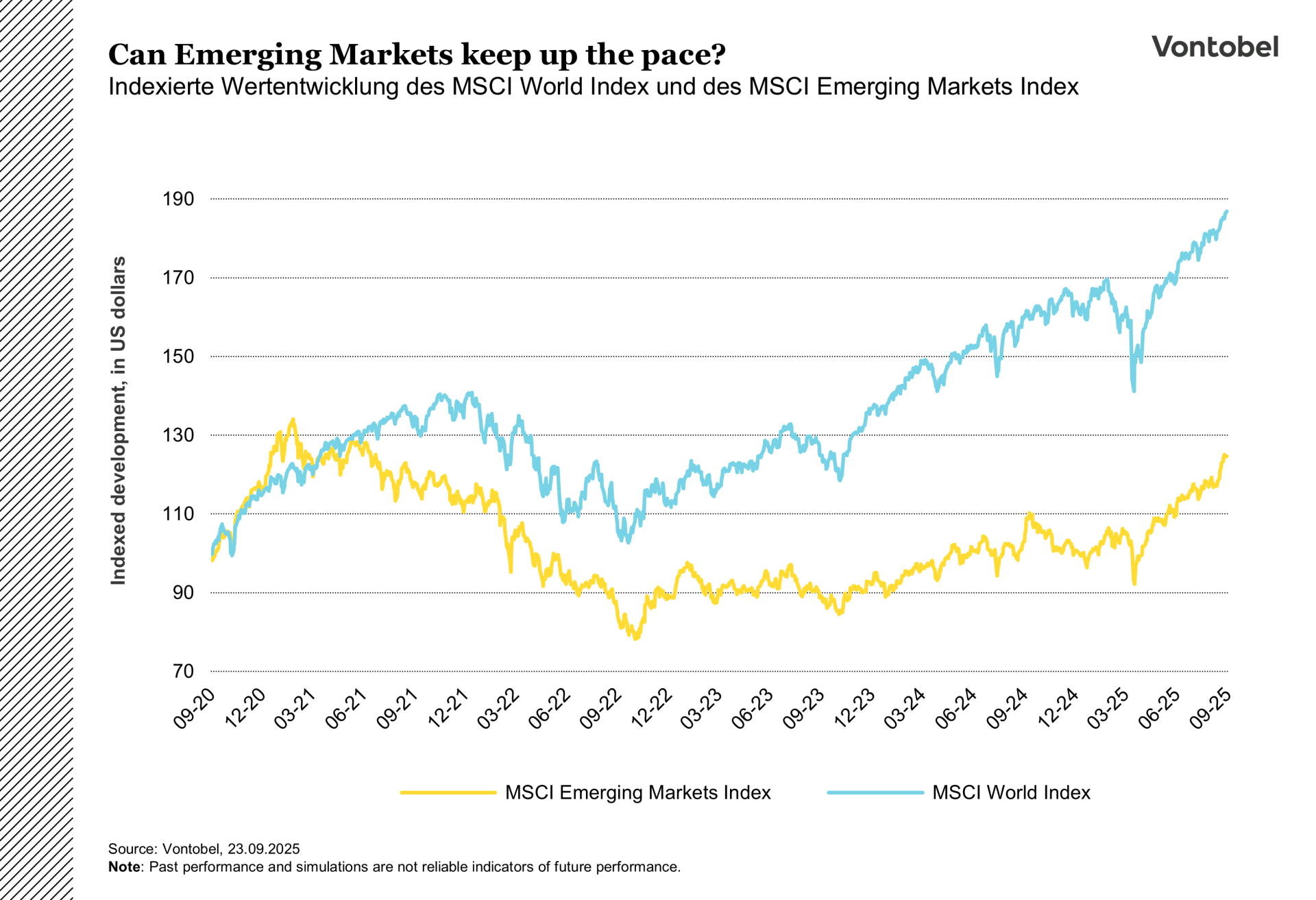

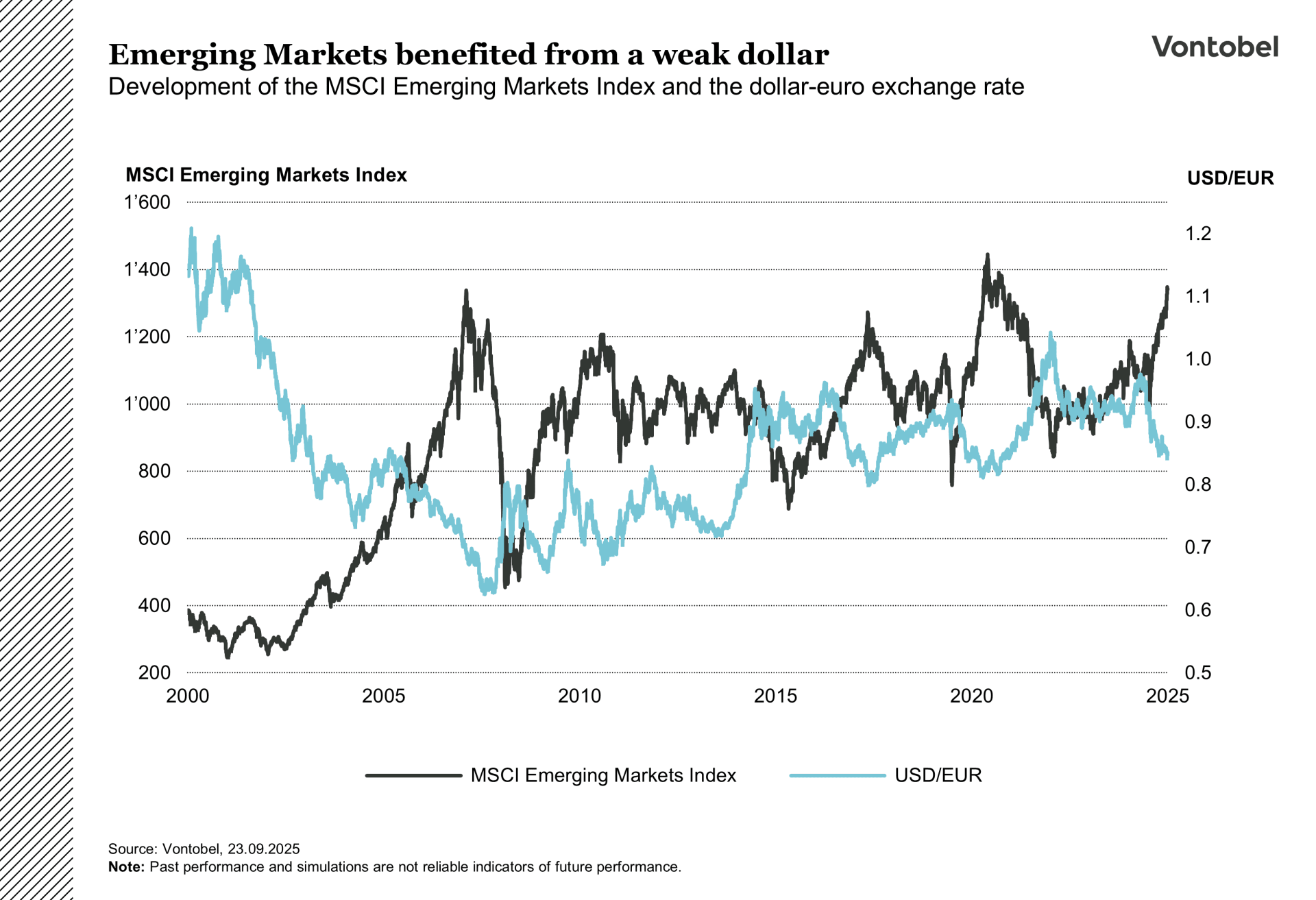

Although US President Donald Trump has imposed particularly high punitive tariffs on many Emerging Markets, the stock markets of Emerging Markets have reacted surprisingly resiliently - the MSCI Emerging Markets Index is up by around 24 percent since the beginning of the year. One of the reasons for this can be found in the world of foreign exchange markets: The trade-weighted US dollar index has fallen significantly in value since the beginning of the year. For many Emerging Markets, whose companies often borrow in US dollars, this development reduces the debt and interest burden. Historical experience shows a certain correlation: weak phases of the US dollar often go hand in hand with bull markets in Emerging Markets.

In addition to this, it seems that less is eaten hot than is cooked. Numerous tariff exemptions, for example for strategic semiconductor supply chains in Taiwan and South Korea, show that more pragmatic solutions are often implemented behind the headlines, which could gradually create a somewhat more positive mood among some market participants.

Emerging Markets with a comeback?

Over the past 15 years, Emerging Markets have never really been able to build on the great bull market of the early 2000s. Since the onset of the Coronavirus pandemic in 2020, disappointing economic developments in China, the long-standing driving force behind global economic growth, have also contributed to a gloomy mood. The ongoing real estate crisis, the trade war with the USA and weakening domestic consumer demand caused concern in China.

This year could see a turnaround in some respects: The US dollar has weakened noticeably since the beginning of the year while the markets expect further interest rate cuts by the Federal Reserve and thus further falls in US real interest rates.

While the US markets might be losing momentum due to new tariffs and a cooling economy, Emerging Markets could gain relative strength. The growth gap between industrialized and Emerging Markets could therefore widen further in favour of the latter. In addition, some indicators increasingly suggest that equity markets in industrialized countries are currently very proudly valued. Many Emerging Market equity markets are considered to be moderately valued compared to industrialized countries, which can be attributed not least to many years of capital outflows. Rising foreign investment, higher corporate profits and a certain degree of political stabilization in parts of Asia and Latin America could provide a fresh tailwind.

At the same time, the differences in the world of emerging markets remain large. While Taiwan and South Korea, with their strong focus on technology, also appear to be highly valued, countries such as Brazil and Mexico are attracting investors with low entry prices and fiscal leeway. India is also benefiting from a young population, ongoing reforms and robust consumption, although trade barriers with the USA could act as a brake.

Risks still exist

The tariffs imposed by Washington could have a noticeable impact on individual markets, even if exemptions and new supply chains cushion the impact somewhat. The situation in China remains tense: The real estate crisis continues, domestic demand is weakening and, despite government support measures, it remains unclear whether these can have a sustainable, long-term effect. The picture on the capital markets is also mixed. Technology-driven stock markets in particular, such as Taiwan and South Korea, now appear highly valued, which increases the risk of corrections. In addition, the tailwind effect of a weak US dollar could quickly dry up if the Fed acts less expansively than expected or yields in the US rise again. Last but not least, political uncertainty factors, from election cycles to regulatory intervention, remain a constant companion. The development of commodity prices could also become a burden for export-dependent Emerging Markets.

Solactive Optimized Emerging Markets Index

The Open End Tracker Certificate in USD on the Solactive Optimized Emerging Markets Index from Vontobel offers investors the opportunity to invest in leading companies from Emerging Markets with one single investment. This certificate has no predetermined expiry date and is therefore also suitable for long-term investment strategies.

The Solactive Optimized Emerging Markets Index tracks the performance of a portfolio of 50 large and medium-sized companies from Emerging Markets. It uses an optimization methodology that aims to minimize the tracking error (the tracking error measures the deviation of the performance of a portfolio or index from that of a reference benchmark) compared to a broad benchmark index, while ensuring balanced regional and sectoral diversification. The index is developed, calculated and published by Solactive AG. The index components are rebalanced quarterly in February, May, August and November to adjust the weightings to current market conditions. Dividends and other distributions are reinvested net in the index.