Investors' Outlook: Strait forward

After weeks of escalating rhetoric between the US and Iran, a preliminary peace agreement could be imminent, according to media reports, adding to signs of improvement. Tanker traffic had slowly picked up again, but remains well below pre-war levels.

Narrow passage

After weeks of escalating rhetoric between the US and Iran, a preliminary peace deal may be close, according to news reports, adding to signs of improvement. Tanker traffic had been slowly picking up, although it has remained significantly below pre-war levels.

Ahead of the most recent developments, the Multi Asset Boutique had updated its scenario probabilities for the Middle East conflict. It assigned a 40 percent likelihood to both de-escalation and stalemate, and 10 percent each to escalation and a breakdown into chaos. While de-escalation and stalemate differ in their timelines and implications for oil prices, neither scenario is likely to trigger an economic downturn, in their view. Under de-escalation, growth is likely to resume, even if at a slower pace than was expected before the war. In a stalemate, growth may stall but remain stable enough to avoid tipping into contraction.

Macroeconomic data for March showed inflation was creeping up in the US and the Eurozone, and even in Switzerland, where it edged up to 0.3 percent. Central banks have hence adopted a cautious wait-and-see approach, conscious of the risks associated with tighten-ing policy too early in an uncertain environment. The

War has interrupted the earlier disinflation trend, but another wave of inflation is unlikely, mainly because today’s situation differs from past episodes in that policy rates are higher, excess savings have diminished, and labor markets are softer. As such, market fears of further rate hikes may be overdone.

Markets closely mirrored the influx of headlines, and commodities experienced some of the most dramatic swings in April, especially as Brent crude oil erased some of the “war premium” that had pushed prices toward USD 120 per barrel.

Taiwan: Tail risk number one

In his 2026 New Year’s address from the Great Hall of the People, Chinese President Xi Jinping declared: “We Chinese on both sides of the Taiwan Strait share a bond of blood and kinship. The reunification of our motherland, a trend of the times, is unstoppable!”

While Xi’s words may have resonated with nationalist sentiment at home, they raised concern abroad. In an inter-view with the New York Times just days later, US President Donald Trump said Xi considers Taiwan, a democratically governed island of roughly 23 million people, to be a part of China. He added that any action regarding Taiwan would be up to Xi, but that he had expressed to Xi that he would be “very unhappy” if Xi chose to invade.

The unease was echoed by Japan’s Prime Minister Sanae Takaichi, who said that a crisis in Taiwan could see Japan and the US act together to rescue their citizens. She added that if US forces were attacked during such a joint operation, Japan couldn’t flee without doing anything, as doing so would risk the collapse of the Japan-US alliance.

Everybody talks about Taiwan, but why does it matter?

So, why is this small island so critical on the global stage? Beyond China’s “One China Principle,” which frames Tai-wan as a matter of sovereignty and unity, the island holds significant economic and geopolitical importance.

At the core of Taiwan’s economic significance is its position as the undisputed leader in the race for technological supremacy. Taiwan Semiconductor Manufacturing Company (TSMC) produces over 60 percent of the world’s semiconductors and more than 90 percent of the most advanced chips. These tiny silicon components power everything from AI and smartphones to advanced defense systems. Without TSMC, the global tech economy would likely come to a standstill.

But Taiwan’s economic importance extends beyond silicon. The Taiwan Strait, which separates the island from mainland China, is a vital artery for global commerce. In 2022, goods worth an estimated USD 2.45 trillion (over one-fifth of global maritime trade) passed through these waters. Of the BRICS5 countries, China is the most reliant on the Taiwan Strait, with over 32 percent of its imports and approximately 15 percent of its exports passing through this critical waterway, according to the Center for Strategic & International Studies (CSIS). The United Arab Emirates follows, with 20 percent of its imports and nearly 25 percent of its exports depending on the strait. Other EM powerhouses, such as India, Iran, and South Africa, also maintain significant trade flows through the strait. The Group of Seven (G7) countries generally have lower expo-sure, with most of their trade flows falling in the low to mid-single digits. Japan stands out as an exception, with over 32 percent of its imports and 25 percent of its exports passing through the strait.

The interconnected nature of global trade means that focusing solely on import and export shares fails to capture the full picture. Beyond risks to global semiconductor supply chains, disruptions in the Taiwan Strait could have profound impacts on global commodity markets. For example, countries such as Oman, Saudi Arabia, Iraq, Kuwait, Qatar, and Yemen depend on the strait to trans-port over 30 percent of their oil exports to Asian markets.

Similarly, the Democratic Republic of the Congo shipped nearly USD 13 billion worth of copper, cobalt, and other metals through the strait in 2022 (62 percent of its total global exports), with most destined for China. Eritrea sends more than 70 percent of its zinc ore and nearly all its copper ore to China, while Gabon and Angola export around 40 percent of their oil to China, much of it traveling through the Taiwan Strait to northern Chinese ports. Any instability in this critical waterway would likely reverberate across regions and severely disrupt trade flows and global markets.

Why are there growing concerns?

China’s ambitions regarding Taiwan are not new. The government has long maintained that the island is a break-away province that must eventually be reunified with the mainland. However, the rapid modernization of the People’s Liberation Army (PLA) since 2015, including advancements in missile systems, aircraft carriers, and amphibious assault capabilities, along with increased PLA military activity around Taiwan, such as record-breaking air and naval incursions into Taiwan’s Air Defense Identification Zone has revived concerns.

Large-scale military exercises, such as those simulating blockades or amphibious assaults, have further raised alarm about Beijing’s preparedness and willingness to use force.

Then there’s also the so-called “Peak China” theory, which argues that China’s rapid economic and geopolitical rise has peaked due to declining demographics, slowing productivity, and high debt burdens, and that the nation is now facing long-term structural decline or stag-nation rather than continuous growth.6 This could, theoretically, increase the likelihood of a more hawkish foreign policy over time.7 Indeed, Beijing has adopted a firm stance that extends far beyond the Taiwan Strait, evident in events such as the 2020 border skirmishes with India, the full integration of Hong Kong’s legal system, and educational reforms in Inner Mongolia.

What also attracts attention is China’s increasing financial estrangement from the West. Beijing’s decision to reduce its US Treasury holdings to a 16-year low while significantly increasing its gold reserves has drawn comparisons to Russia’s actions in the lead-up to its invasion of Ukraine.

Simultaneously, the social fabric in Taipei is changing. According to Chengchi University’s Election Study Center, some 62 percent of residents identified as Taiwanese in 2025, while fewer than 3 percent identified as Chinese. For context, in 1992, 25.5 percent identified as Chinese, compared to just 17.6 percent as Taiwanese. The risk for China is that the longer it delays action, the wider this ideological gap is likely to grow.

What speaks against an invasion today

Despite the heightened rhetoric, the likelihood of an immediate Chinese invasion of Taiwan remains

low. First and foremost, the “Peak China” theory remains a subject of intense debate rather than an established fact. It is true that the era of rapid double-digit growth is over, the population is shrinking, debt levels are elevated, and the external environment has grown more challenging. But Beijing is actively pivoting toward high-tech manufacturing and renewable energy. Sectors like electric vehicles (EVs), batteries, and solar power are expanding rapidly and are helping to offset some of the economic drag from the property sector downturn. Moreover, breakthroughs in AI and other advanced technologies in 2024 and 2025 show that China retains a strong capacity for innovation and remains globally competitive, often defying skeptics.

Second, the Chinese Communist Party has a well-documented history of “muddling through” crises through pragmatic policy adjustments. The launch of the 15th Five-Year Plan in 2026 is aimed at consolidating these gains rather than risking a hard landing.

Third, China’s current military constraints make an immediate invasion highly unlikely. Taiwan’s geography, combined with its robust defensive preparations, present formidable challenges for any amphibious assault. The roughly 100-mile-wide Taiwan Strait is known for choppy waters, with monsoons and unpredictable weather narrowing the window for a seaborne invasion to just a few months each year. Even then, transporting hundreds of thousands of troops across the strait under constant fire would be a logistical nightmare. Taiwan’s “Porcupine Defense” strategy further complicates the equation. Its military has focused on asymmetric warfare, emphasizing mobile missile systems, coastal defenses, and the ability to sabotage critical infrastructure such as ports to deny invaders a foothold. For instance, Taiwan’s “shallow water” defense ensures that if major ports are rendered inoperable, Chinese forces would struggle to offload tanks and heavy equipment, leaving them vulnerable to coastal artillery and missile strikes. Even if a beachhead were established, the challenges would only multiply. Taiwan’s mountainous terrain is ideal for guerrilla warfare, with defenders able to use natural cover to harass and delay advancing forces. The capital city, Taipei, is nestled in a natural “bowl,” offering a defensive advantage in urban combat. Together, these factors make Taiwan a difficult target and reinforce the effectiveness of its deterrence strategy.

Another deterrent is the potential for US military intervention. Since the Cold War, the US has adhered to a policy of “strategic ambiguity,”9 deliberately avoiding explicit com-mitment on whether it would defend Taiwan in the event of a Chinese attack. This creates calculated uncertainty for Beijing, which can’t reliably predict the nature or extent of a US response. Despite this ambiguity, there is a strong likelihood that the US would intervene

in some capacity if China were to invade Taiwan today. This is due in part to its dependence on Taiwanese semiconductors, with TSMC a key supplier to major US technology companies such as Apple, Nvidia, and AMD.

China also faces significant economic constraints that make an invasion a risky proposition. As the world’s larg-est exporter and a dominant manufacturing hub, its share of global manufacturing exports has grown from the low single digits in the early 1980s to around 20 percent in 2024.

Would Beijing risk jeopardizing this position through severe Western sanctions and wide-spread supply chain disruptions? Probably not. The Russia-Ukraine war has already demonstrated the steep economic and geopolitical costs of becoming a pariah state in a dollar-dominated global economy.

Energy dependence presents another vulnerability. While China is the world’s largest energy producer, it is also the largest consumer, and domestic output cannot meet its growing demand. The country relies heavily on imports, particularly for oil and liquefied natural gas, much of which passes through key maritime chokepoints, such as the Strait of Hormuz and the South China Sea.

An invasion of Taiwan would likely expose these routes to blockades or disruptions, severely impact-ing China’s energy imports. International sanctions could further restrict energy flows, with suppliers in the Middle East, Africa, or even Russia potentially facing pressure to limit exports.

Over the years, China has steadily increased its domestic energy production, invested heavily in renewables, and built up its strategic petroleum reserves (SPR) to mitigate short-term supply disruptions.

However, wars cannot be fought with renewable energy alone, and strategic stockpiles are finite. Replenishing SPR during a conflict would be challenging, especially if key shipping routes were to be blocked. A disruption in energy imports would likely result in energy shortages, driving up domestic prices and increasing costs for oil- and gas-dependent industries. This could exacerbate

preoccupied with other conflicts, or if NATO were to face internal divisions, China might perceive a window of opportunity. Another factor to consider is the US effort to reduce its dependence on foreign chips and reindustrialize domestic chip manufacturing. Data from the Semi-conductor Industry Association and Boston Consulting Group projects that US semiconductor fabrication capacity will jump from 11 percent in the 2012 – 2022 period

to around 81 percent in 2022 – 2032. In other words, as US dependence on Taiwan for chips declines, so may its incentive to intervene.

Domestically, the Chinese government could intensify nationalist rhetoric to rally public support for an invasion, particularly if internal pressures like economic stagnation or social unrest were to worsen. In such a scenario, Beijing may conclude that the risks of inaction outweigh the potential costs of military action.

Lessons from past invasions: When should investors worry about an imminent invasion?

Identifying warning signs of an imminent invasion is inherently challenging, as aggressor nations often rely on deception and strategic ambiguity to mask their intentions.

Nevertheless, by analyzing historical precedents, the Multi Asset team has identified several indicators that could potentially signal an impending Chinese invasion of Taiwan. These can be grouped into five categories: financial, economic, logistical, military, and narrative.

From a financial perspective, signs of “sanctions-proofing” would be critical. This could include accelerated divestment from US Treasuries or record-high gold purchases by the People’s Bank of China. Both could be potential signals of preparing for economic isolation.

On the economic front, heightened stockpiling of strategic goods could serve as a red flag, including unusual surges in imports of crude oil, liquefied natural gas, and grains. Another indicator could be a noticeable redirection of industrial production capacity, such as a shift from manufacturing EVs toward defense-related machinery and equipment.

Logistical movements might also provide valuable clues. A sudden and significant rise in vessel activity around Taiwan or the anomalous relocation of blood supplies closer to potential conflict zones could raise alarms. While not definitive, such movements are considered among the more reliable near-real-time indicators of imminent military action, as red blood cells have a shelf life of up to 42 days, and platelets must be used within 5 to 7 days.

On the military side, unusual or conspicuous patterns in military exercises would warrant scrutiny. A surge in cyberattacks targeting Taiwan’s critical infrastructure in the lead-up to an invasion could serve as an additional warning signal.

Finally, shifts in the narrative propagated by Chinese state media or government officials could provide insight into Beijing’s intentions. A sudden escalation in nationalist rhetoric, increased emphasis on Taiwan as an inseparable part of China or attempts to justify military action under the guise of self-defense or reunification could indicate a shift toward imminent conflict.

Scenario analysis and investment implications

The Multi Asset team has identified three potential scenarios for the next five years and assigned probabilities to each.

Its baseline, “Status Quo” (it estimates an 80 percent probability), assumes China continues its grey-zone tactics, which include cyberattacks, occasional air defense incursions, and economic coercion, without escalating into full-scale kinetic conflict. The US maintains strategic ambiguity, while Taiwan continues to strengthen its “porcupine” defense. This scenario assumes a continuation

of current levels of policy uncertainty and economic conditions, supporting a risk-on investment environment, in which maintaining a structurally long exposure to EM assets is likely to yield positive returns.

Its second scenario, “The Hong Kong Model” (it estimates a 10 percent probability), envisions reunification without major conflict. A political shift within Taiwan or overwhelming economic pressure leads to a negotiated “one country, two systems” framework, with no direct US intervention. While this scenario could trigger short-term spikes in policy uncertainty, the broader economic context would likely remain stable with a risk-on environment intact. Investors might prefer Chinese assets in this case.

Its final scenario, “Invasion” (it estimates a 10 percent probability), involves a full-scale amphibious assault or blockade, likely triggering US and allied intervention or, at minimum, sweeping G7-wide sanctions comparable to or harsher than those imposed on Russia in 2022. Escalation into a broader war, potentially even World War III, cannot

be ruled out. This scenario would likely result in a prolonged period of heightened policy uncertainty, a global eco-nomic recession, sustained de-globalization, and a pronounced risk-off environment.

In such a scenario, historical patterns from World War I and World War II offer some guidance. Two factors, inflation risks and geographical proximity, played an important role in shaping asset performance. Wars have historically been highly inflationary. Wars caused massive supply disruptions due to destroyed infrastructure, labor shortages, and disrupted trade, while demand remained stable or even increased because of hoarding and wartime needs. As governments ramped up spending and printed money to stabilize economies and prevent unrest, inflation surged. During these periods, commodities emerged as the top-performing assets, driven by heightened demand for resources to support war efforts and rebuild infrastructure. In contrast, bonds performed the worst, as inflation eroded their real (inflation-adjusted) value. Equities landed in the middle, initially benefiting from government-driven demand, particularly in industries such as aircraft manufacturing and transportation. However, a significant portion of their profits was often reclaimed by the government, limiting their overall gains. Geography also matters. Countries far from the fighting experienced better returns, as they avoided physical destruction. Among those directly involved, victors out-performed losers, though both lagged behind non-battle-ground nations.

Applying these insights to the "Invasion" scenario, investors might be inclined to steer clear of EM stocks entirely, especially given that China and Taiwan account for

48.2 percent of the MSCI Emerging Markets Index (27.6 percent and 20.6 percent, respectively). However, avoiding these markets entirely could result in significant opportunity costs. Investors would instead likely consider taking a structural long position in commodities and gold, which have historically performed well during periods of geopolitical conflict and uncertainty.

Thinner air

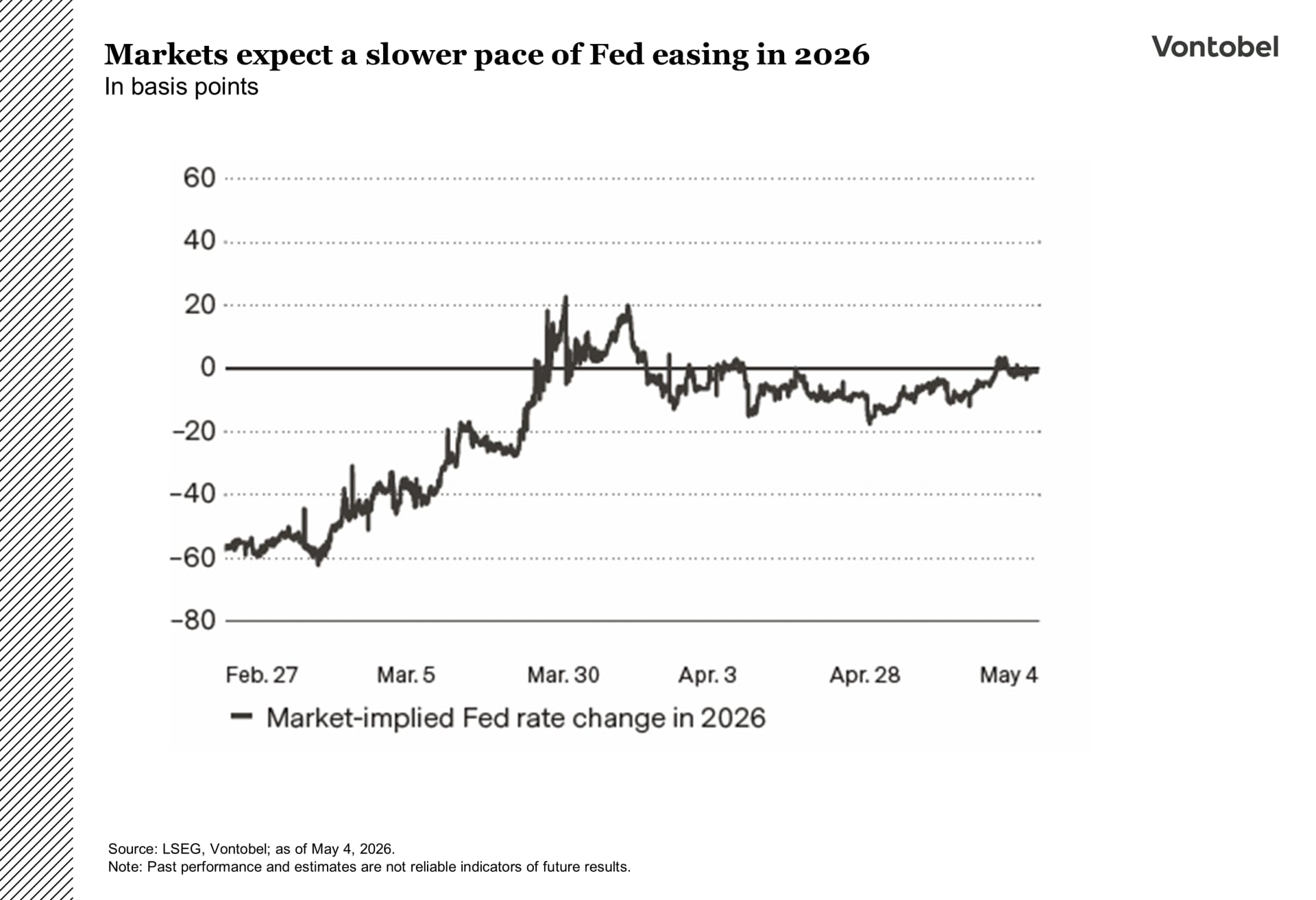

The macroeconomic backdrop is becoming more com-plex. Inflation is no longer following a steady downward path, the Fed has turned more cautious, and markets are adjusting to a higher-for-longer rate environment.

The Fed has moved into wait-and-see mode, and the bar for rate cuts has moved higher. Inflation expectations have picked up again amid higher energy prices and geo-political risks. Inflation swaps now point closer to 4 per-cent headline inflation, suggesting markets are looking through recent benign prints. The Federal Reserve Bank

of Cleveland nowcasts add to these concerns, with second-quarter inflation tracking well above levels consistent with the Fed’s target.

While the Fed’s policy remains on hold, the discussion has become more guarded, with some policymakers again entertaining the possibility of further tightening if inflation persists.

They’re grappling with not just with the question of when to resume rate cuts, but whether policy is restrictive enough in the first place.

For yields, this supports a higher-for-longer environment. Front-end rates remain under upward pressure as expectations for easing are pushed further out, while the long end is anchored by elevated supply and fiscal deficits. The result is a rates market that is range-bound but prone to bouts of volatility.

Credit markets are starting to reflect this more demanding environment (see chart 2) as higher rates, tighter financial conditions, and geopolitical tensions have weighed on sentiment and valuations.

While the Fed’s policy remains on hold, the discussion has become more guarded, with some policymakers again entertaining the possibility of further tightening if inflation persists.

They’re grappling with not just with the question of when to resume rate cuts, but whether policy is restrictive enough in the first place.

For yields, this supports a higher-for-longer environment. Front-end rates remain under upward pressure as expectations for easing are pushed further out, while the long end is anchored by elevated supply and fiscal deficits. The result is a rates market that is range-bound but prone to bouts of volatility.

Credit markets are starting to reflect this more demanding environment as higher rates, tighter financial conditions, and geopolitical tensions have weighed on sentiment and valuations.

The war in Iran has added a new layer of pressure. What was previously a supportive mix of solid growth and contained inflation is now being disrupted by higher energy prices, rising yields, and in-creased geopolitical uncertainty. This change can be observed in credit dynamics: higher funding costs, increased issuance, and more selective investor demand

are limiting further spread compression and introducing a gradual widening bias. And tighter refinancing conditions and a cloudier outlook are beginning to weigh on weaker issuers.

Then there’s private credit. Redemption requests exceeded USD 20 billion in the first quarter, with only a portion met so far, signaling rising investor caution, particularly around leveraged exposures. This doesn’t yet amount to systemic stress, though it probably does point to early pressure. With a war-driven energy shock and tighter financial conditions, private credit may act as a leading indicator for broader credit risk.

Snapping back

In April, investors witnessed one of the sharpest reversals in global equities in more than a decade.

After touching trough valuations in early March as the war in Iran and the closure of the Strait of Hormuz weighed on markets, the S&P 500® swung from a first-quarter decline of nearly 10 percent to fresh highs above 7000 points. That was a 14 percentage-point round trip in roughly three weeks. The NASDAQ-100 Index® posted 13 sessions of consecutive gains, its longest winning streak since 1992.

The catalyst was familiar: a Trump-brokered ceasefire and renewed momentum in diplomatic relations between the US and Iran, which triggered aggressive short-covering and a rapid compression in risk premia. The pattern echoed Liberation Day in 2025: panic selling into com-pressed multiples, followed by a reflexive snapback as soon as there was a sign that policymakers might deescalate.

Why has the Multi Asset Boutique remained constructive? First, the energy shock appears manageable. The global economy is less oil intensive than in prior cycles, with services and technology now dominating output and margins. Second, the inflation pass-through is likely to be contained, provided the Strait disruption doesn’t drag on. If normalization continues, the narrative around investors pricing in central banks possibly hiking instead of cutting rates could revert quickly, which would likely provide renewed support for risk assets. The yield on 10-year US Treasuries briefly spiked above 4.3 percent at the end of March. This threshold has often coincided with a rebound in equities.

Third, this shock is fundamentally different from 2022. Back then, global supply chains were already broadly disrupted and reeling from the pandemic, inflationary pressures were well entrenched (further amplified by the Russia–Ukraine conflict), and consumer demand remained strong on the back of substantial monetary stimulus. Today, consumer price inflation hasn’t gotten out of hand, labor markets have been relatively robust, and the Fed retains optionality.

Finally, earnings remain the main anchor.

Positive revisions on projected earnings

First-quarter results are off to a strong start, with most companies showing limited impact from the energy shock. Consensus still points to double-digit earnings-per-share (EPS) growth for the S&P 500®, and markets are already looking past potential second-quarter soft-ness toward a 2027 earnings trajectory that appears intact.

Safe haven under siege

For decades, the conventional investment playbook during geopolitical turmoil was simple: when the drums of war beat, investors tend to buy gold. But since the outbreak of the Iran war, the yellow metal has behaved less like a steady anchor and more like a high-beta technology stock.

While gold has partially recovered from the brutal sell-off in late March, it has yet to regain the levels observed prior to the conflict. The changing nature of gold’s DNA is most visible in the CBOE Gold Volatility Index (GVZ).

Gold volatility typically remains relatively muted compared to equities, but in 2026, GVZ readings have spiked. Gold’s traditional safe-haven appeal is being over-shadowed by the strength of the US dollar and investor concerns that central banks may struggle to look past the current inflation spike. Higher rates would be negative for a non-yielding asset like gold. As long as investors are wary of hawkish monetary policy, gold is unlikely to regain the “cheap money” tailwind it enjoyed in 2025.

On the central bank front, reports of proposed or actual gold sales have unsettled investors further. Poland is considering selling part of its reserves to fund increased defense spending, while Türkiye and Russia have already offloaded some of their holdings.

This has lifted short-end US yields and given the dollar additional support, even as growth shows signs of slowing. As long as uncertainty and oil prices stay high, the Fed has limited room to cut rates, which is poised to continue to support the dollar in the near term. But it’s mainly cyclical and tied to the current risk backdrop rather than a stronger underlying story. The US fiscal position remains weak, and Treasury supply is heavy while external balances have not improved. Those factors tend to matter more once markets move out of crisis mode, which is why the broader case for a softer dollar in the medium term still appears intact to us.

Another currency has also continued to benefit from classic safe-haven demand: the Swiss franc. But unlike the dollar, it is now running into a growing policy constraint, which could make further gains harder to sustain in the near term. In periods of stress, the franc has historically performed well, and this episode has been no different.

Switzerland’s persistent current account surplus, relatively disciplined fiscal policy, and low inflation give the cur-rency a solid medium-term anchor and leave it better sup-ported fundamentally than most of its peers. At the same time, that strength is becoming a challenge for the Swiss National Bank (SNB).

With the policy rate already at zero, further appreciation tightens financial conditions and risks pushing inflation even lower. The SNB has already signaled a greater willingness to counter excessive moves through intervention in foreign-ex-change (FX) markets, which means policy resistance is building. The franc is likely to remain supported as long as geopolitical risks stay elevated, but the pace of appreciation may slow if the SNB becomes more active.