Investors’ Outlook: Of carrots and sticks

The financial markets look back on a year full of uncertainties so far. Trade tariffs, inflation and labor market data, as well as the ongoing conflict between U.S. President Donald Trump and Fed Chairman Jerome Powell, dominate the picture. Nevertheless, stock markets are trading near record highs. Quo vadis, global economy and capital markets?

More spurs than brakes?

New tariffs, mixed macroeconomic data, personnel changes at major US institutions, and ongoing geopolitical tensions have unsettled investors over the summer. Even so, equity markets climbed. Based on current market conditions, we believe economic growth is poised to improve, supported by favorable monetary conditions and the prospect of global fiscal stimulus.

Earlier rate cuts are still filtering through the economy,and there’s a possibility the Fed will resume easing as early as September. On the fiscal side, Germany has

already announced measures, and China may act later this year. And while tariffs may push some prices higher, the effect should be modest and temporary, with weaker consumption offsetting inflationary pressure.

US politics also shape the outlook. Since Liberation Day, we believe President Donald Trump has leaned more toward a pro-growth stance, which may gain traction as midterm elections approach and approval ratings decline.

The Fed’s rate decisions will hinge on labor market conditions, which are difficult to read. Trump’s restrictive immigration measures have sharply reduced the number of foreign-born workers. From March to July, 1.7 million dropped off payrolls data, according to the National Foundation for American Policy. Immigrants have driven more than half of US labor force growth over the past three decades. What’s more, since the launch of ChatGPT and similar tools, IT job postings have declined while unemployment among recent college graduates has risen. It’s possible AI may be displacing roles that were once filled by early career professionals. We believe the Fed is likely to steer interest rates back to neutral territory, a level that neither stimulates nor hinders economic growth.

When political pressure meets monetary policy

One could accuse US Federal Reserve Chair Jerome Powell of many things, misjudging inflation in 2021, not raising interest rates quickly enough in 2021 – 2022, or not lowering them fast enough in 2025, but being thin-skinned is not one of them. Due to his reluctance to cut interest rates, Powell has been branded a “stubborn moron” and an “average mentally person” with a “low IQ for what he does” by US President Donald Trump. Considering Trump’s repeated attempts to influence the Fed’s rate-setting body by either threatening to fire or outright firing Fed governors, it may be time for a closer look at central bank (in)dependence.

In one way or another, central banks have always been established, at least in part, to serve political interests. The world’s oldest, the Swedish Riksbank (1668), was

created to lend funds to the government and serve as a clearinghouse for commerce. Other European nations soon followed, using central banks to carry out government policy. The Bank of England (BoE), for instance, was founded in 1694 primarily to finance England’s war against France.

In the early 20th century, a new wave of central banks emerged with a focus on crisis prevention and financial stability. Among these “second-generation” central

banks was the US Federal Reserve (Fed). Before its creation, the US experienced frequent market panics, bank runs, and failures. The Panic of 1907 was particularly severe, with the New York Stock Exchange losing nearly 50 percent of its value from the previous year’s peak. With no central bank to intervene, wealthy individuals like J.P. Morgan and John D. Rockefeller stepped in to stabilize the financial system. The reliance on private bankers to rescue the national financial system spurred President Woodrow Wilson to sign the Federal Reserve Act in 1913. Just one year later, the newly created Fed already faced its first major test.

During World War I (1914 – 1918), it played a significant role in stabilizing the economy and supporting the war effort. So-called Liberty Bonds were sold to the public to fund military expenses, while rising government spending and heightened demand for goods put upward pressure on prices. The Fed sought to manage these pressures by influencing interest rates and credit conditions, although its tools were still limited at the time.

World War I marked a significant turning point in monetary policy. Many countries, including the UK, Germany, and France, abandoned the gold standard to print more paper money and finance higher spending. The resulting inflation served as a stark reminder of the risks when governments instruct central banks to print money at will. In the postwar years, the concept of central bank independence began to gain ground, emphasizing the need for monetary authorities to set interest rates and policy without short-term political interference. Despite growing awareness of the importance of central bank independence, the economic collapse of the 1930s and the demands of World War II saw governments exert greater control over central banks once again, whether to address unemployment and deflation during the Great Depression or to finance wartime government spending. After the establishment of the Bretton Woods system in 1944, central banks assumed a central role in maintaining fixed exchange rates. As they had to defend currency pegs, their independence remained limited.

In the decades that followed, political pressure on central banks intensified, particularly in the US (see the chart). In 1951, President Harry Truman attempted to compel the Fed to maintain a cap on Treasury yields, thereby effectively financing US involvement in the Korean War. By 1965, things even turned physical: President Lyndon B. Johnson—who was pouring money into both his “Great Society” programs and the Vietnam War—summoned then-Fed Chair William McChesney Martin to his Texas ranch.

There, Johnson reportedly shoved Martin against a wall and yelled, “Boys are dying in Vietnam, and Bill Martin doesn’t care.” Johnson’s successor, Richard

Nixon, preferred a more public (and sarcastic) approach. At the 1970 swearing-in ceremony of Arthur Burns, Nixon quipped, “I respect his independence. However, I hope that independently he will conclude that my views are the ones that should be followed.” Determined to get the Fed to cooperate ahead of the 1972 election, Nixon held several meetings to push Burns to cut rates. Burns ultimately yielded, lowering interest rates despite the inflationary risks.

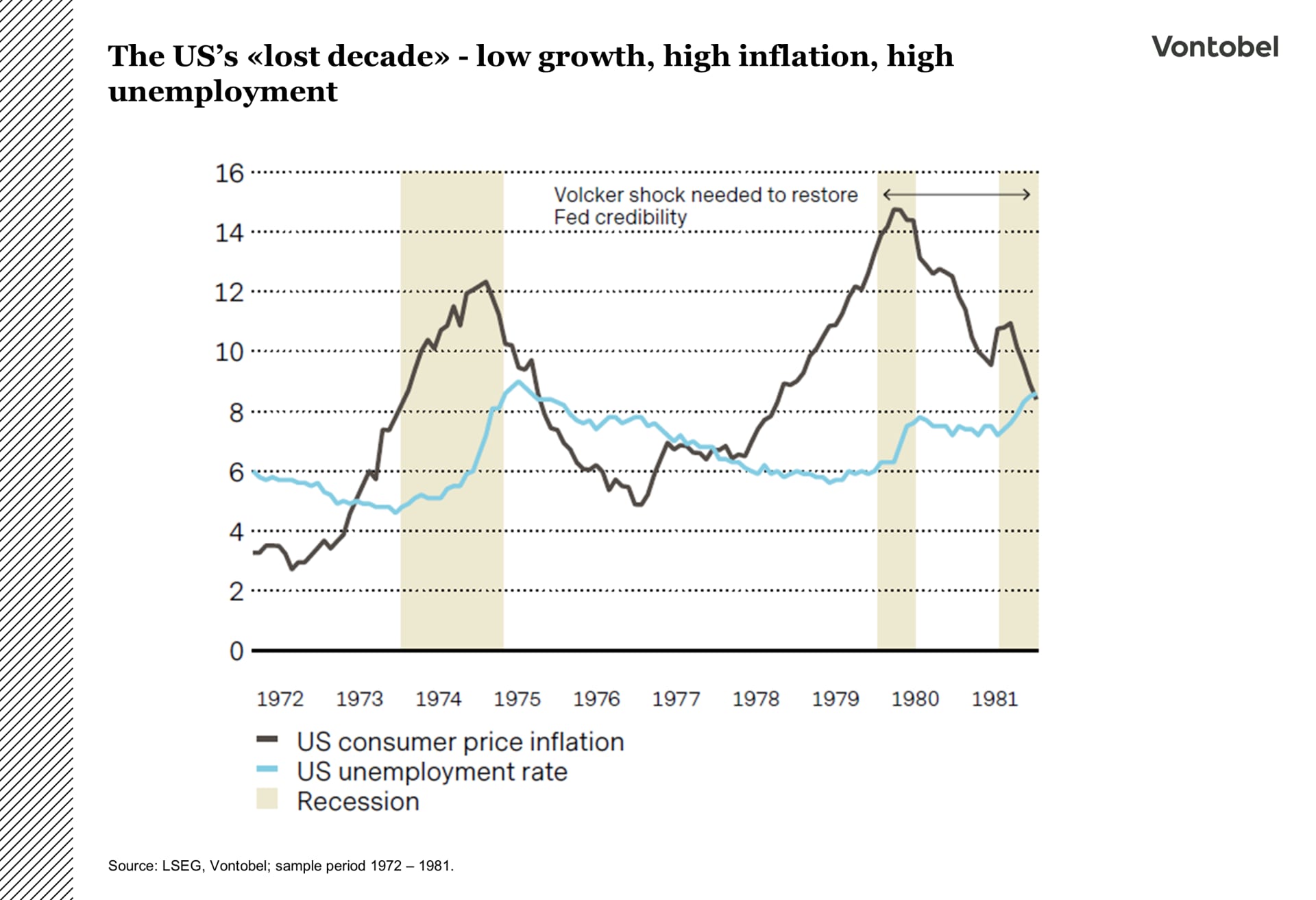

The 1972 intervention resulted in what many consider one of the most painful chapters in US economic history: a brief pre-election boom followed by a decade of stagflation, i.e., a combination of stagnant economic growth, high unemployment, and high inflation, which defies traditional macroeconomic theory (such as the belief that inflation and unemployment have an inverse relationship). It took the so-called Volcker Shock (1979 – 1982) to restore the Fed’s credibility (see the chart). Appointed as chair in 1979, Paul Volcker aggressively raised the federal funds rate from roughly 10 percent to 20 percent, triggering double-dip recessions.

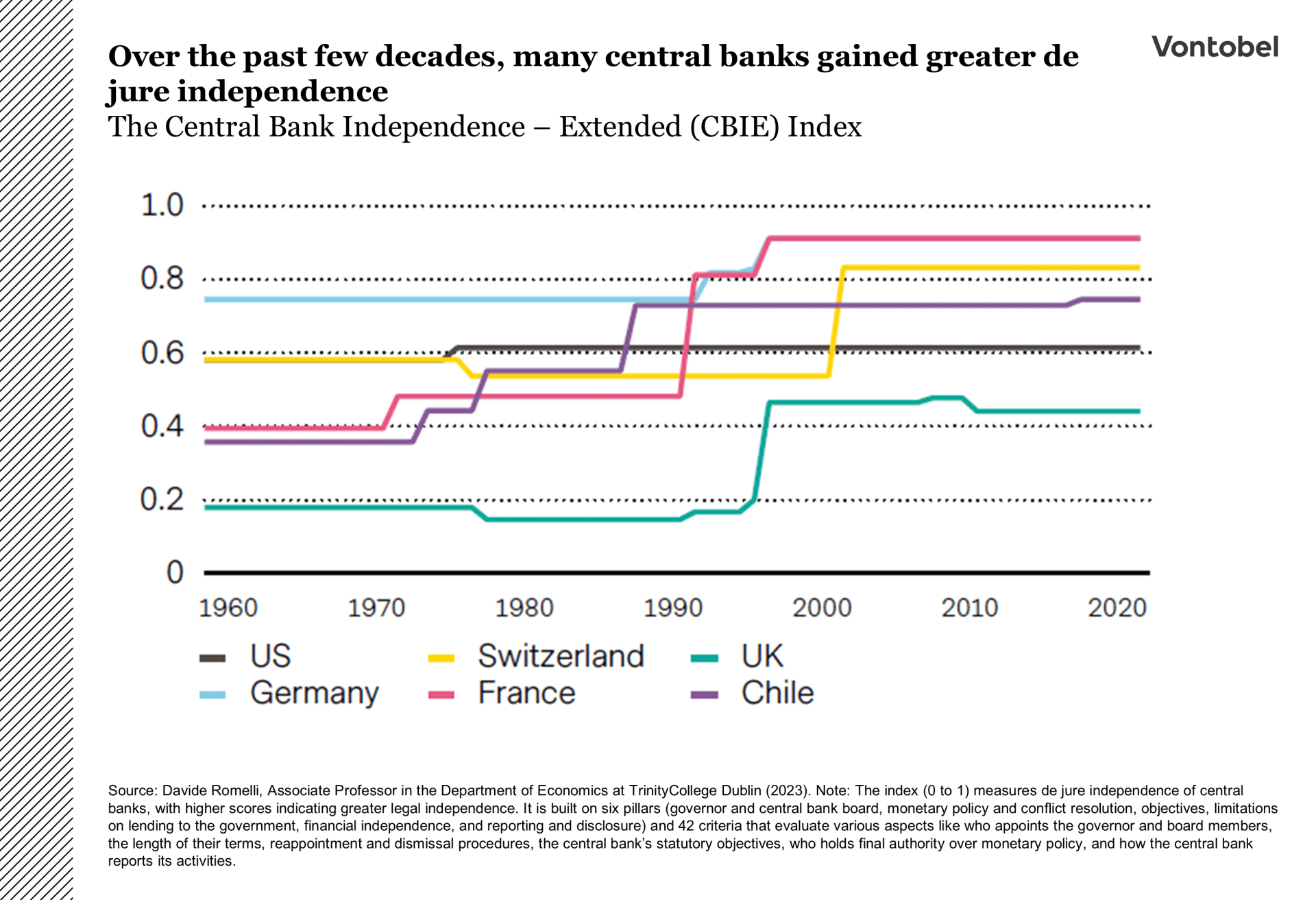

In doing so, Volcker resisted political pressure from both Democratic President Jimmy Carter, who had appointed him, and Republican President Ronald Reagan, who inherited the recession. From the 1990s to early 2000s, central banks entered

what is widely regarded as the “golden age” of independence, as many institutions achieved greater de jure independence (see the chart).

Several factors contributed to this trend.

First, numerous countries enacted statutory reforms or treaty provisions that explicitly defined central bank independence. For example, the Maastricht Treaty

of 1992 enshrined the ECB’s independence in EU law. Similarly, the Bank of England (BoE) gained operational independence to set interest rates in 1997, and the Swiss National Bank (SNB) was granted independence in 2000 with the adoption of a new National Bank Act. Before 2000, the SNB already enjoyed a degree of operational independence, but without explicit legal guarantees.

Second, mandates became clearer and more narrowly defined. The adoption of so-called “inflation targeting” as a key policy framework was arguably one of the most significant developments of the era, as it enabled central banks to prioritize managing inflation, thereby limiting the scope for political interference.

Third, the tenure of many central bank governors and board members was

often lengthened, and made non-renewable, to insulate them from political pressure. For instance, members of the ECB’s Executive Board, including the president and vice president, serve a single, non-renewable eight-year term. Finally, central banks also began emphasizing greater transparency

and accountability to strengthen public trust. They started publishing meeting minutes, releasing economic forecasts, and holding regular press conferences.

This shift marked a clear break from longstanding traditions, such as the “never explain, never excuse” ethos or the tendency to “mumble with great incoherence.”

These positive changes were not limited to developed markets. In fact, emerging-market economies like Chile serve as powerful reminders of how past crises can

drive meaningful progress. In the early 1970s, Chile was plagued by weak economic growth, elevated fiscal deficits, and triple-digit inflation, while real interest rates were in negative (i.e., accommodative) territory. The military

government’s push for rapid deregulation and liberalization, combined with an overvalued exchange rate, led to a deep economic and banking crisis in the early 1980s.

The Central Bank of Chile was granted independence in 1989 and started to pursue an inflation-targeting regime in the early 1990s. Today, it is considered one of the most independent and stable central banks in the region. Mexico provides another example of improved central bank independence. Following a period of economic instability in the late 1980s, marked by high inflation and debt crises,

the country reformed its central bank in 1994, granting the Bank of Mexico constitutional autonomy and a clear mandate to prioritize price stability. Similarly, the South African Reserve Bank (SARB) strengthened its independence

after decades of grappling with challenges, particularly during the apartheid era. Since 2000, the SARB has focused on inflation targeting, enhancing its credibility and effectiveness in monetary policy.

Better than it used to be, but increasingly at risk again

That said, one cannot help but notice that the role of many central banks has shifted once again. Crises such as the Global Financial Crisis (2007 – 2009), the Euro Area Crisis (2009 – 2010), and the Covid-19 Crisis (2020) forced many central banks to take on broader roles: they were not only expected to act as “lenders of last resort” to stabilize financial institutions (e.g., through bailouts) but also to deploy unconventional monetary tools (e.g., quantitative easing) to support the post-crisis recovery.

These expanded roles arguably blurred the lines between

monetary and fiscal policy, as governments grew increasingly reliant on central banks to finance deficits and stabilize markets. This dynamic is also evident in several of Trump’s recent statements. For example, in June, he remarked, “If they (the Fed) were doing their job properly, our country would be saving trillions of dollars in interest cost (…) we should be paying 1 percent interest, or better!”

This blurring of roles is not unique to the US. In 2020, ECB President Christine Lagarde faced criticism after unveiling emergency stimulus measures to protect the financial system. The controversy was less about the measures themselves than about her refusal to echo the “whatever it takes” approach championed by her predecessor, Mario Draghi, in 2012 to save the euro. What happened?

Lagarde stated, “We are not here to close spreads (…) there are other tools for that and other actors to deal with those issues”, referring to the borrowing spread differences between heavily indebted countries like Italy and less indebted ones like Germany. Her implicit attempt to shift responsibility back to governments led to a sharp sell-off in Italian assets. Three years later, the BoE (legally independent since 1997) found itself embroiled in a highprofile dispute with the UK government. What happened? Just days before Chancellor Kwasi Kwarteng’s “mini budget,” which included GBP 45 billion in unfunded tax cuts, the BoE sold GBP 40 billion worth of gilts.

At a time when inflation was running above 10 percent, the prospect of unfunded tax cuts triggered a bond market sell-off, made worse by pension funds facing collateral calls on leveraged gilt investments. Prime Minister Liz Truss demanded

an investigation into the BoE’s actions and even called for the dismissal of Governor Andrew Bailey. Ironically, Truss herself ultimately resigned amid the ensuing turmoil. Even the SNB, often regarded as one of the most independent

central banks in the world, has come under increasing political pressure. Swiss cantons, which receive a share of the SNB’s profits, have pushed for higher distributions, potentially prioritizing short-term financial gains over longterm

monetary stability. Additionally, climate activists and political groups have urged the SNB to align its investment policies with environmental goals, adding a new

layer of challenge to its independence.

Türkiye offers one of the clearest examples of how political interference can undermine a central bank and destabilize an economy. While the Central Bank of the Republic of Türkiye (CBRT) is formally independent, its governor can be appointed or dismissed at the president’s discretion. President Recep Tayyip Erdoğan, known for his unorthodox belief that cutting interest rates reduces inflation, has dismissed five CBRT governors since 2019, including one just two days after a rate hike. This has led to double-digit inflation, capital flight, and widespread dollarization of the economy.

Fast forward to today’s threats to the Fed chair

Trump’s repeated threats to fire Powell, coupled with his history of dismissing other government officials, have heightened concerns that he might eventually attempt to remove Powell. Financial markets have reacted nervously whenever such threats dominated headlines. For instance, in mid-July, Bloomberg—citing an unidentified White House official—reported that Trump was likely to fire Powell soon. Following the news, US bond yields rose (bond yields move inversely to prices), the US dollar weakened, and US equities came under pressure (see the

chart ). As it stands, Trump cannot dismiss Powell solely because he disagrees with his monetary policy views. The Supreme Court case Humphrey’s Executor v. United States (1935) established that officials of independent agencies cannot be removed by the president “without cause,” with “cause” typically interpreted as malfeasance or gross misconduct. While the Supreme Court has recently upheld Trump’s authority to dismiss certain US officials, it also emphasized that the relationship between the president and the Fed is distinct from that with other

independent agencies. This suggests that Powell may, in fact, be legally protected. Consequently, consensus assigns only a very low probability to Powell being fired in 2025.

Meanwhile, Trump and his allies have begun searching for a “cause”. In mid-July, Office of Management and Budget (OMB) Director Russell Vought sent a letter to Powell, criticizing cost overruns tied to the renovation of the Fed’s historic headquarters—even though the OMB has no oversight of the Fed, which funds its operations independently of the congressional appropriations process. Shortly afterward, Federal Housing Finance Agency Director Bill Pulte expressed confidence that Congress would investigate Powell over what he described as “deceptive” statements made during a June Senate hearing. Even Treasury Secretary Scott Bessent—widely regarded as a voice of reason—called for an investigation into the Fed’s operations and effectiveness. “What we need to do

is examine the entire Federal Reserve institution and whether they have been successful,” Bessent said in July 23. He went on to accuse the Fed of “fearmongering over tariffs” despite “great inflation numbers” and voiced frustration with “all these PhDs over there” who, he claimed, are unable to “break out of a certain mindset.” If prediction markets are any indication, Trump will also face difficulties charging Powell “for cause”. By mid-August, the probability of Powell being federally charged in 2025 was just 10 percent.

The most market-friendly outcome, in our view, would be for Trump to allow Powell to serve out his term as chair, which expires in May, and then appoint someone more aligned with his preferences. Even in that scenario, however,

Trump may still have to contend with Powell as a voting member of the Federal Open Market Committee (FOMC). This is because Powell holds two distinct terms:

one as chair (until 2026) and another as an FOMC governor (until 2028). That said, Powell could choose to leave the Board voluntarily when his term as chair ends, following the precedent set by some of his predecessors.

Should investors worry about an “overly accommodative” Fed?

To answer this question, it’s worth stepping back to look at the FOMC’s structure. The committee has 12 members: seven members of the Board of Governors and five of the 12 regional Reserve Bank presidents. Governors are appointed by the US president and confirmed by the Senate for staggered 14-year terms, with one term expiring every two years on February 1 of an even-numbered year. The chair and vice chair serve separate renewable four-year terms, but must be sitting governors. Of the five Reserve Bank presidents, one seat is permanent (held

by the New York Fed president), while the other four rotate annually. In practice, this means that over a typical fouryear term, a US president can directly appoint or reappoint at most about two governors. For Trump, these are Jerome Powell’s chair seat (expiring in May 2026) and Adriana Kugler’s governor seat (expiring in January 2026). After Kugler unexpectedly stepped down in August, Trump appointed Stephen Miran, the current chairman of the Council of Economic Advisors, as her temporary replacement. According to Trump, Miran is not a successor-in-waiting for Powell but is expected to serve only the remainder of Kugler’s existing term. At the end of August, Trump once again sought to expand his influence over the FOMC by dismissing Fed Governor Lisa Cook on allegations

of mortgage fraud. Cook hired a lawyer who promised to “do whatever is necessary” to prevent this “illegal action.”

If market expectations are correct, there are three likely contenders for the Fed chair role. First is Kevin Warsh, a former FOMC governor (2006 – 2011) who was not only considered to be Fed chair during Trump’s first term but also for Treasury Secretary in his second. Some observers believe that Trump appointed Scott Bessent as Treasury Secretary to keep the door open for Warsh’s potential appointment as Fed chair. Second is Kevin Hassett, the current National Economic Council Director, who has joined in criticizing the Fed’s renovation project. Third is Christopher Waller, already a sitting FOMC member, who recently broke rank by publicly supporting a July interest-rate cut.

There is no denying that the Fed chair holds significant sway over the FOMC’s direction and agenda. Paired with more dovish governors, the chair could potentially push for a more accommodative monetary policy. However, several checks and balances are in place that we believe would prevent Trump from selecting overly dovish or outright “unorthodox” candidates. Chief among

them is the Senate confirmation process, which acts as a critical gatekeeper. During Trump’s first term, the Senate rejected his nomination of Judy Shelton for a governor position. Shelton, an economist known for her unorthodox monetary policy views, had advocated for tying the US dollar to gold and suggested that the Fed should be less independent. Notably, three Republican senators joined

Democrats in voting against her. We would expect the Senate to exercise even more vigilance when confirming a Fed chair.

Beyond these two seats, Trump has little influence over the remaining Reserve Bank presidents. These presidents are even further outside his control, as they are hired by the banks’ Boards of Directors (each Reserve Bank has its own board), which are independent of supervised entities. Only three Reserve Bank presidents have terms expiring during Trump’s term, and none before 2028. The rest serve terms extending into the 2030s, well beyond the end of Trump’s second term.

When might a new Fed chair be announced?

Since five-time Fed Chair Alan Greenspan stepped down, successors have typically been announced about 4.5 months before the end of the current chair’s term. For Powell, this points to an announcement in early 2026. The timing could matter for financial markets. If a successor is named earlier—say, in autumn 2025—markets

might begin pricing in expectations of lower borrowing costs even while Powell is still in office.

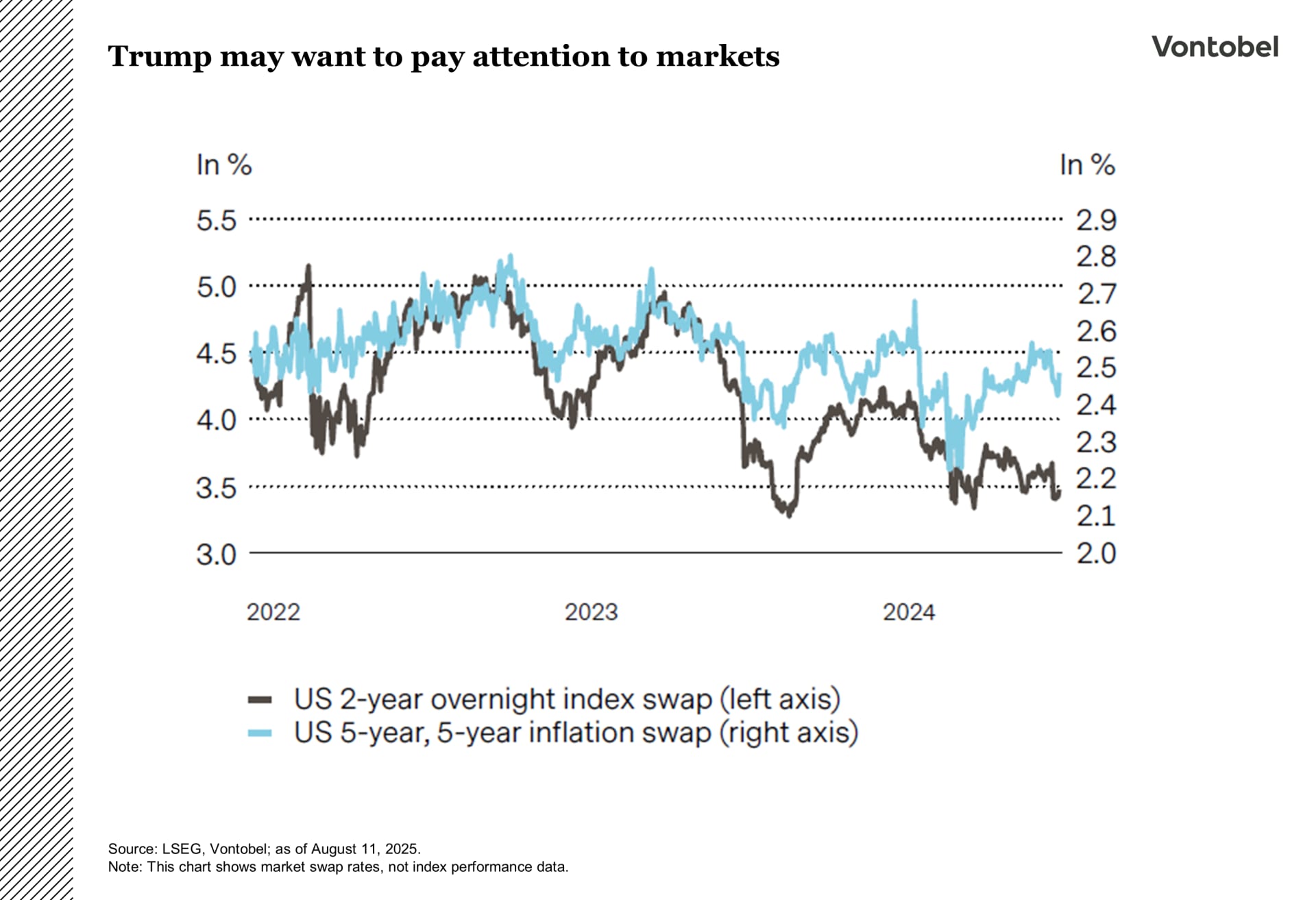

Trump may want to pay attention to markets

Ironically, the more Trump pressures the Fed and its chair, the less likely he is to achieve lower borrowing costs. Why? Many of his assertions, like claiming that “people aren’t able to buy a house because this guy (Powell) is a numbskull (…) he keeps the rates too high,” are at odds with economic realities. Fed interest-rate cuts, if they occur, do not automatically translate into lower mortgage rates. The standard 30-year fixed-rate mortgage is determined not by the Fed’s overnight rate but by longdated Treasury yields. The greater the perceived political

influence on US monetary policy, the more volatile inflation is likely to become—and the higher the compensation investors will demand for holding long-term investments in the US. That compensation typically comes in the form of higher bond yields. As we go to press, the market’s inflation expectations—as tracked by five-year, five-year forward swaps—are picking up. This suggests that markets already price in a certain risk (see the chart).

We believe Trump would be well-advised to pay close attention to market signals. If he does not, investors may consider reducing exposure to US assets and increasing allocations to alternatives such as gold. The yellow metal performed exceptionally well during the stagflation of the 1970s. Its outperformance only came to an end when Paul Volcker’s aggressive interest-rate hikes managed

to restore market confidence in the Fed’s independence

Focus on the Fed as markets press for cuts

The Fed kept rates on hold in July as inflation stays above target and hiring cools. Tariff uncertainty and debate over the neutral rate initially left policymakers cautious about signaling near-term rate cuts, though Chair

Jerome Powell opened the door to that possibility at the Jackson Hole symposium.

In July, Powell noted the case for easing was somewhat stronger than in June, and two officials voted for a cut, but policy remained modestly restrictive. The data has come in mixed: growth has slowed, unemployment ticked higher, yet inflation is still above target and new tariffs may add pressure. Markets hoped for hints of cuts, which they interpreted as all but guaranteed after Powell’s dovish

comments. The risk balance is murky, though. Tariffs’ inflation impact is unclear, and the neutral rate itself (the level for stable growth and inflation) is up for debate. Fed estimates range from 2.5 percent to 3.9 percent versus the 3 percent many investors assume. Cutting too soon, before inflation is back at target and the labor market weakens further, could backfire. The White House is pushing for steeper cuts. We believe the data doesn’t support an outsized cut. A September cut looks more plausible now given signs of a softer job market, but payrolls are still growing, so we see no cause for alarm.

History warns against political meddling. Research by macroeconomist Thomas Drechsel shows sustained political pressure, like in the early 1970s, can raise the

price level about 7 percent over a decade without lasting output gains. In today’s high-debt, fast-moving environment, costs could hit sooner. Markets still trust Powell to hold the line, and that trust rests on Fed independence. Futures show little change in the Fed’s expected path since June, but now price

in more easing after Powell’s final meeting in April 2026 (see the chart).

Tight spreads, thin cushions

Investment-grade credit is extremely tight, with spreads around 73 basis points over US Treasuries, the narrowest in nearly 30 years (see the chart). That reflects stronger balance sheets, Fed easing hopes, improved earnings, a low perceived recession risk, and robust demand that keep all-in yields appealing despite thin spreads. The catch is that valuations leave little margin if growth slows as tariffs at multidecade highs and some labor data softens. Credit markets are signaling calm while rates markets show more caution, which leaves little cushion if growth disappoints.

Climbing the wall of worry

Equities kept climbing the “wall of worry” over what usually is a quiet summer period, with most regional indexes hitting all-time highs in local currencies.

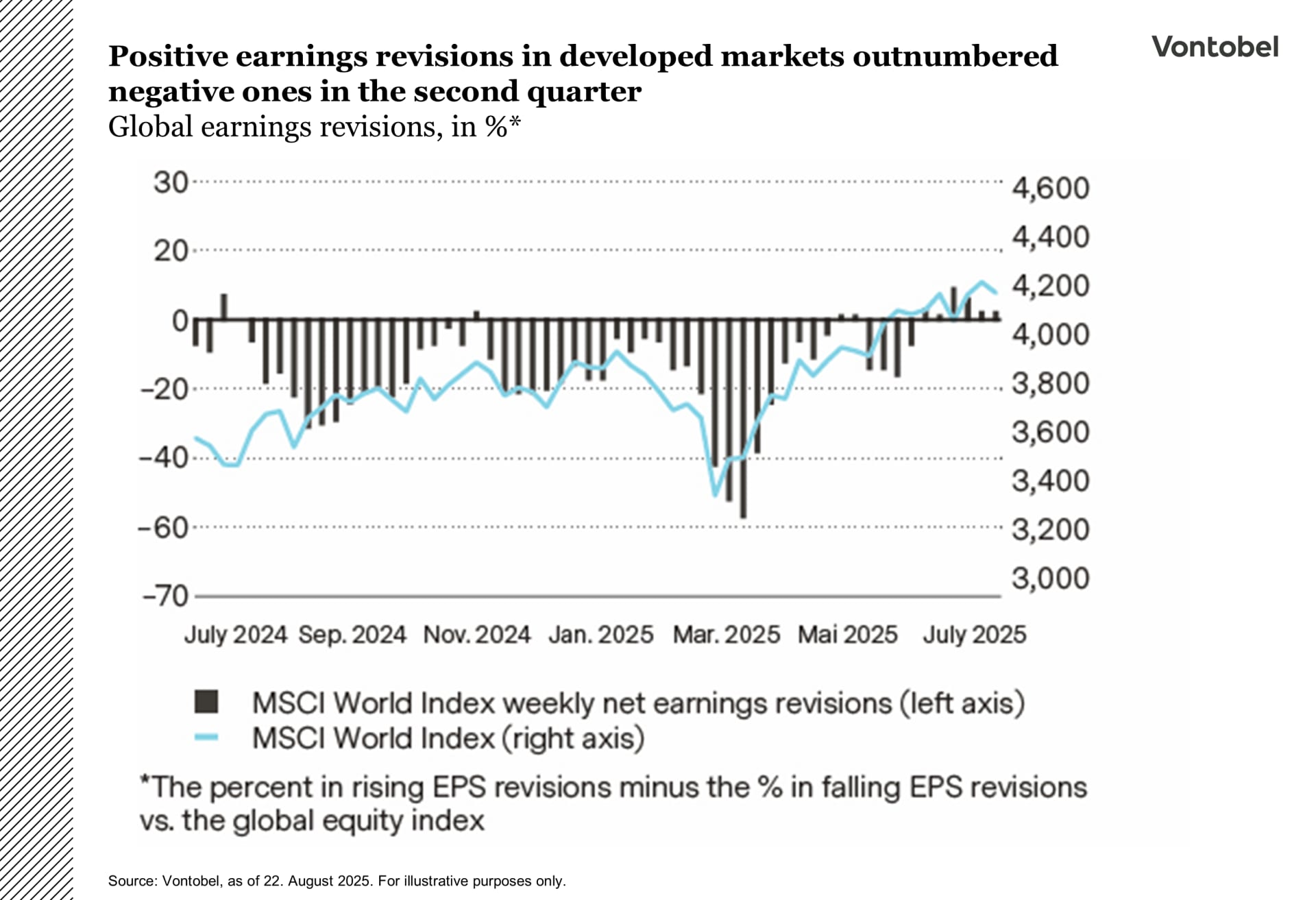

Bullish sentiment is based on a strong second-quarter earnings season, upbeat guidance, easing tariff uncertainty, expectations for September rate cuts, anticipated Fed leadership changes, and expected 2026 stimulus that could boost companies’ earnings per share (EPS) as in 2018 (see the chart). Earnings season delivered solid surprises with minimal tariff effects, marking an inflection

in momentum (see the chart) and suggesting prior revisions may have been too pessimistic. Going forward, earnings surprises are likely to play an important role in stock performance given stretched valuations.

Inflation remains the main driver of equities’ direction. Billions in tariffs are now hitting the US economy each month, but who really bears the cost? The spillover

to consumer prices is more nuanced than many assume. Tariffs don’t automatically flow fully through to consumers. Their impact depends on factors like a company’s competitive position, demand elasticity, distribution model, time lags, and value chain structure. We see this in US Producer Price Index (PPI29) data, where importers typically absorb the first hit through margin pressure, and

the historical correlation between PPI and the US Consumer Price Index (CPI30) has been weak, suggesting producer prices aren’t a reliable predictor of consumer

inflation. Companies also have tools to offset tariffs: prebuying inventory, temporarily absorbing margins, diversifying supply chains, reformulating products, redesigning value chains, and – only as a last resort – passing on costs selectively. Recent US “Big Box” retailer earnings confirm this.

So, will tariffs show up in CPI? Yes, and the third quarter could bring a step-up, but we believe the overall transmission is poised to be moderate, partial, and temporary, spread across sectors and diluted over time. Services, which account for 70 to 80 percent of CPI, remain largely insulated. Higher-risk areas are consumer goods such as electronics, toys, autos, and auto parts.

Tariffs may add volatility to CPI readings in coming quarters, potentially reigniting the tug-of-war between the Fed and the Trump administration, with Powell reluctant to cut rates. But unlike 2021 – 23, we see no structural damage

to value chains. We view market pullbacks as opportunities to add to equity exposure.

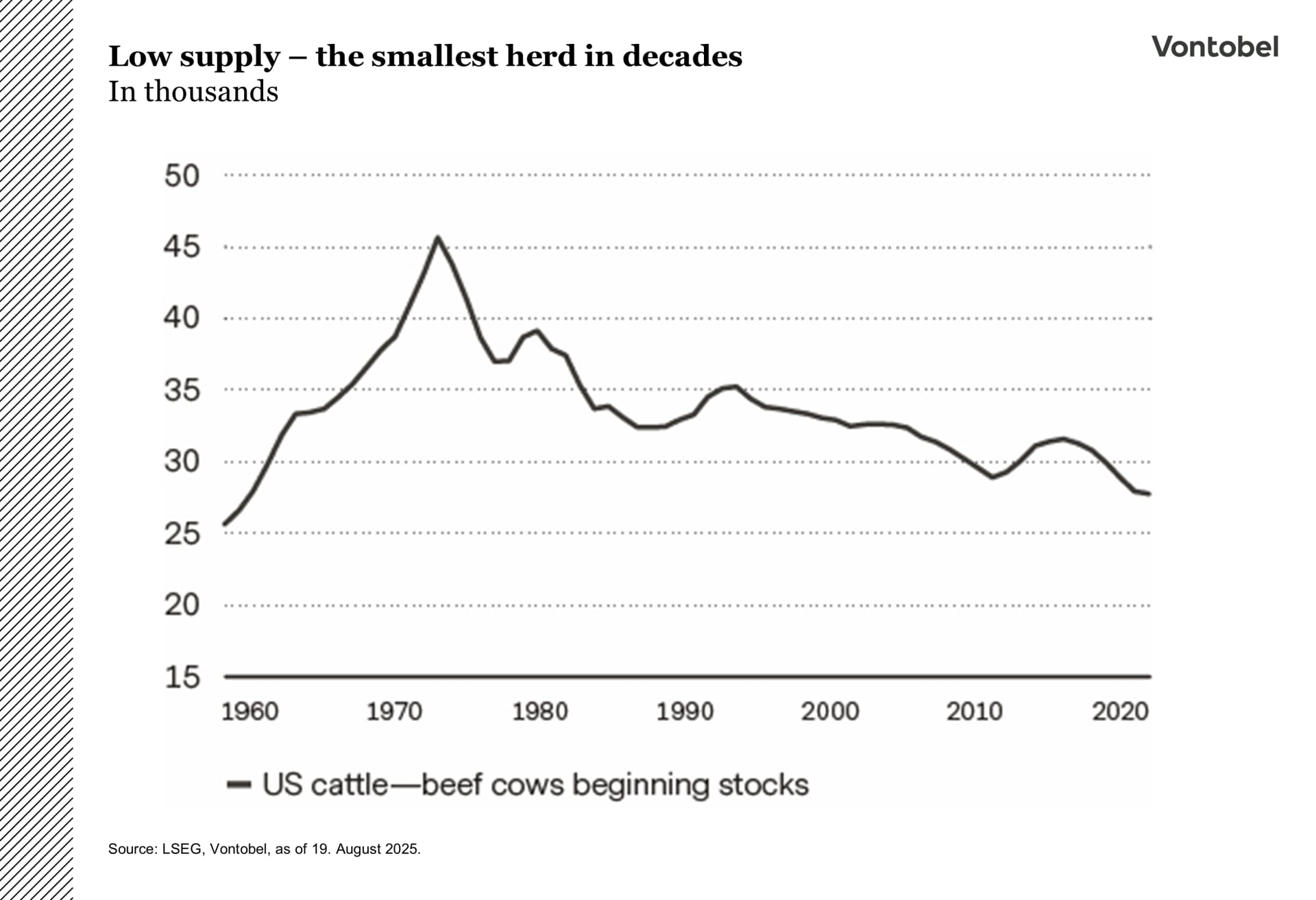

Meat-flation

US cattle prices have surged to historic highs in 2025 (see the chart), highlighting the “three Ds” that often push agricultural commodity prices higher: drought, disease, and demand.

The main force behind the price surge is the multiyear contraction of the US cattle herd. Rising production costs and severe drought across key states like Texas, Oklahoma, and Kansas, home to roughly one-third of the US beef cow inventory, have led ranchers to aggressively cull their herds. According to the US Department of Agriculture (USDA), the national herd is now at its lowest level since the early 1960s (see the chart). Supply issues have been compounded by the closure of the US-Mexico border to cattle imports due to the resurgence of the New World screwworm. The worm – actually a type of fly – lays its eggs in the wounds of warm-blooded animals, often leading to death as the larvae hatch and feed on living tissue. In the 1950s, the screwworm devastated cattle herds, leading to significant economic losses. Mexico, a key source of more than one million feeder cattle annually, has faced repeated outbreaks of the parasite, sharply reducing cattle exports to the US in 2025. For now, the border remains closed. The USDA will review the import suspension monthly, taking into account eradication

progress and the worm’s spread.

In addition, Immigration and Customs Enforcement raids on farms and meatpacking plants targeting individuals without proper work authorization further disrupted operations. On the demand side, consumer appetite for beef

has remained surprisingly strong. For financial markets, surging cattle prices are contributing to broader food inflation. While energy prices are falling, protein inflation, led by beef, is keeping grocery inflation stubbornly high.

What are the potential sources of relief? Favorable weather would be the most organic solution, as improved forage availability could incentivize ranchers to rebuild their herds. The expected record-high US corn harvest may also boost feed supplies and lower costs. Government programs (e.g., emergency assistance for drought-stricken areas) could also encourage restocking efforts. Lastly,

increased imports from other countries could help rebalance US supply. However, these measures won’t resolve the low inventory problem (and may not be politically desirable).

In the short term, the situation may worsen before it improves. Rebuilding cattle supply is typically a multi-year process. Additionally, when ranchers hold back heifers from slaughter to expand their herds, beef production temporarily slows. This reduction in supply will likely push prices even higher before they eventually come down.

Tariffs and US resilience cloud the euro’s short-term outlook

The euro’s cyclical outlook has been dented by tariffs and lingering US strength, but market trends indicate that the longer-term bullish case against the dollar holds, with the key risk being a stronger-than-expected US economy.

Last year’s dollar rally was fueled by strong US growth and repeated upgrades to gross domestic product (GDP). But momentum faded in 2025. The US Dollar Index fell about 11 percent in the first half of the year, marking the end of a structural bull run that began in 2010 and delivered a cumulative gain of around 40 percent by 2024. Back in 1985, the dollar’s slump came in the wake of the Plaza Accord, when major economies coordinated to weaken the US currency after a period of extreme strength. By August 21, the US dollar had clawed back part of this year’s losses, though the scale of the drawdown invites comparison with the 1985 reversal following the Plaza Accord (see the chart).

A 15 percent US levy on the EU, coupled with a firmer euro, leaves euro-area exporters more exposed. The bigger risk, in our view, isn’t further European weakness but a US rebound. Consensus for US growth has slipped to 1.5 percent from 2.3 percent for 2025 and to 1.7 percent from 2 percent for 2026. Euro-area projections have held near 1 percent (see the chart). With Europe’s weakness

already priced in, the swing factor is US data. Incoming releases now sit at the center of the EUR/USD outlook. Our longer-term stance is unchanged: structurally bullish on the euro, with stronger-than-expected US growth the main risk.

In Switzerland, tariffs may weigh on growth, but the Swiss franc’s outlook rests on its role as a defensive hedge, which keeps the long-term bullish case intact. Inflation inched higher in July, with headline CPI up 0.2 percent year on year and core up 0.8 percent, driven by transport, services, and some food prices, while the strong franc kept import costs low. July’s uptick aside, inflation is still at the low end of the SNB’s 0 – 2 percent range and is likely to hover near zero in the months ahead. Some pickup is expected only toward late 2025 as base effects fade and tariffs filter through. Current data is unlikely to sway the SNB’s stance, with officials focused on the franc, wary that further appreciation could quickly erase the modest rise in prices.

The surprise 39 percent US tariff on Swiss exports in August initially sparked a short-lived selloff in the franc. While such a levy may weigh on Switzerland’s growth outlook, they don’t drive the currency. The franc’s strength is rooted less in domestic fundamentals or rate differentials and more in its role as a structural hedge. With diversification back in focus and de-dollarization themes resurfacing, its defensive appeal is as strong as ever, in our view. These factors leave the longer-term case for a stronger franc intact.