Elements of the future: the race to catch up begins

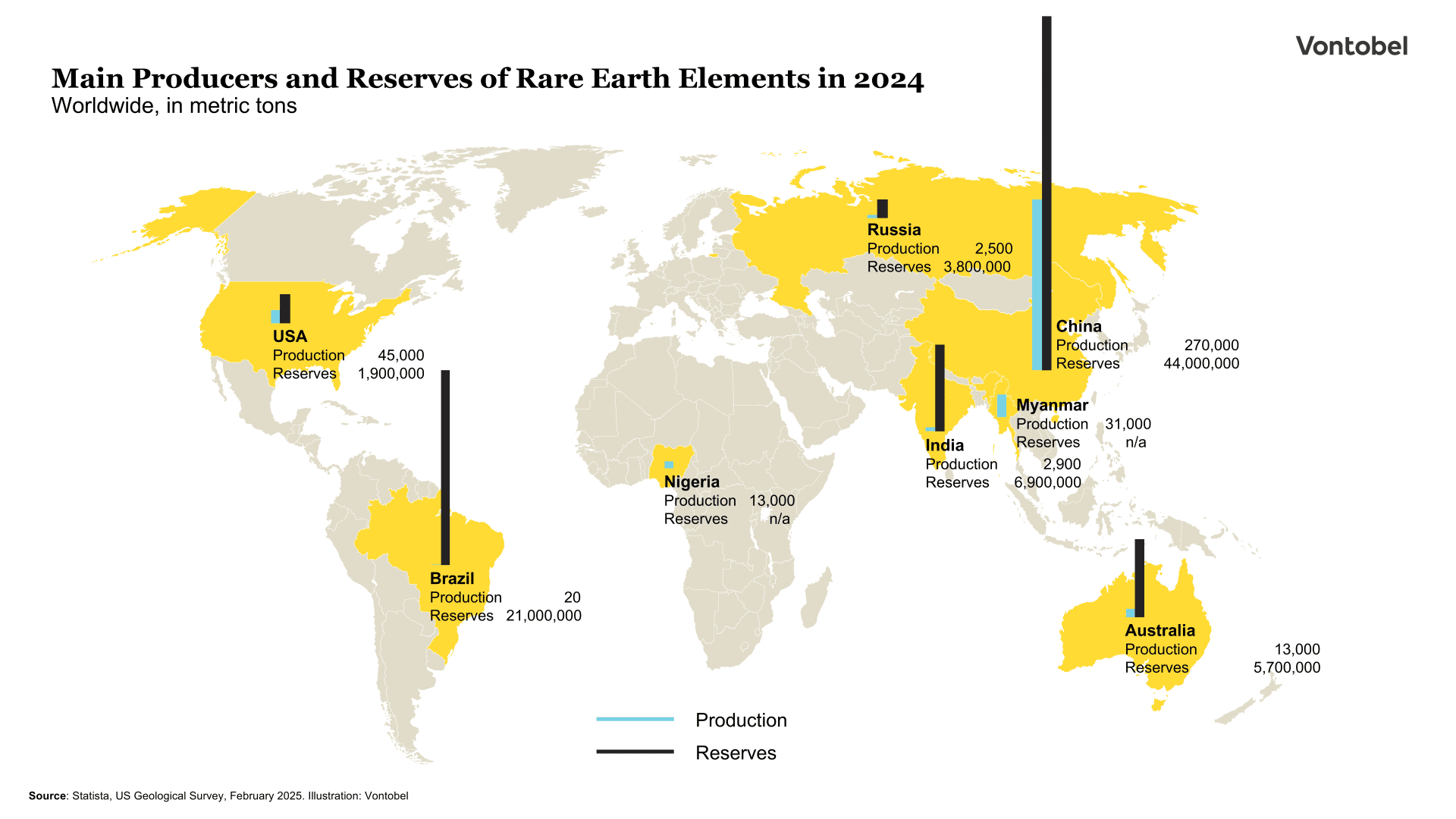

Rare earths have moved into the geopolitical and economic spotlight in recent years. China recognized the signs of the times early on and invested in domestic capacities years ago. The result is sobering for the rest of the world: around 60 percent of global rare earth production and 90 percent of refining takes place in China. This situation is forcing western countries to reduce their dependency and build up alternative capacities.

Indispensable for high-tech and the energy transition

Whether smartphones, electromobility or renewable energies - rare earths are an indispensable component of modern industry. Contrary to their name, the 17 elements classified as rare earths are relatively common in the earth's crust, but are usually only found in low concentrations or mixed with other minerals. Their extraction is therefore complex, expensive and often associated with environmental pollution.

Rare earths are most frequently used for the production of permanent magnets, which are used in electric car motors, wind turbines and even in defense technologies. Permanent magnets such as neodymium-iron-boron (NdFeB) magnets have the property that they generate a permanent magnetic field without the need for an external energy source (such as electricity). So-called heavy rare earths such as dysprosium or terbium are in high demand, as they make magnets more heat-resistant and more powerful. These properties are particularly important for electric vehicles and defense systems (Guardian, 06.06.2025).

After mining, often from clay deposits in southern China or from carbonate-rich rock in Australia and the USA, comes the crucial and technically most challenging step: separating the individual elements. This is the real bottleneck in the global value chain. Chemical separation is usually carried out using complex solvent processes that require large quantities of acids and are harmful to the environment (Harvard International Review, 12.08.2021). Only after refining are the elements processed into metal alloys and then shaped into high-performance magnets, for example.

China flexes its muscles

Rare earths and their availability have been increasingly used as geopolitical leverage in recent years. China has repeatedly demonstrated to the rest of the world how strong its influence on global supply chains is. in 2010, for example, China temporarily cut supplies to Japan following a political dispute, to which Japan responded with a comprehensive strategy to reduce its dependence on Chinese rare earths. This included investing in recycling, promoting technologies that enabled the use of substitutes and diversifying supply chains, for example through closer cooperation with Australia, which reduced Japan's dependence on China.

In 2023, China enforced an export ban on separation technologies and since April this year, seven strategic rare earths have been under export control (samarium, gadolinium, terbium, dysprosium, lutetium, scandium and yttrium). This decision was introduced by Beijing as a countermeasure to the US punitive tariffs as part of "Liberation Day". As a result, the licensing requirement for exports has been delayed by months in some cases, which has brought production in some Western companies to a standstill.

The handling of state production quotas for Chinese raw materials companies is also new. Unlike in previous years, the quotas for 2025 were not communicated publicly, but were sent to companies confidentially (Reuters, 20.07.2025). The quota model has been in place since 2006 and sets annual maximum quantities for mining and processing. It was originally used to combat illegal mining and to protect the environment, but is now increasingly being used as a strategic component.

Supply chains under pressure

Although the US and China were somewhat more willing to compromise in the aftermath of the tariff storm in April, the distortions that have arisen in the meantime are only slowly closing. Western companies, for example, often only receive orders for end products such as magnets with a delay or in small quantities (The Wall Street Journal, 26.06.2025).

The consequences for the industry were quickly felt: Ford, for example, had to shut down a production line in Chicago in May, Suzuki stopped production of the Swift in Japan and European suppliers reported bottlenecks in electric motors (FuW, 20.06.2025).

China denies that the export restrictions are being used specifically against certain countries and emphasizes that they are only intended to regulate military goods. However, the reality shows just how politicized the raw materials market is: with a 90 percent market share in magnet production, China has leverage that can severely affect supply chains for electromobility, wind power and defence systems.

Hopes for new producers

Recent developments have triggered a veritable race in the USA, Europe and Australia to become less dependent on Chinese suppliers. In the United States, the focus is on the raw materials company MP Materials. The operator of the Mountain Pass mine in California, the largest rare earth deposit in the western hemisphere, is enjoying increasing strategic government support. The United States Department of Defense recently secured a 15 percent stake and guaranteed the company a minimum price for its production (The Wall Street Journal, 10.07.2025). In addition to mining, MP Materials will also increase magnet production at its new plant in Fort Worth, Texas, to 10,000 tons per year. This quantity would cover a large proportion of US demand. A deal worth USD 500 million with the technology company Apple, which wants to source magnets made from recycled material in future, underlines the importance of this project (The Wall Street Journal, 15.07.2025). Other US companies such as USA Rare Earth and Energy Fuels are also benefiting from government funding and are expanding their processing capacities.

In Australia, Lynas Rare Earths in particular is pushing into the gap left by the dwindling supply from China. The company has built a plant in Kalgoorlie that is the first outside of China to separate heavy rare earths such as dysprosium and terbium (Deptartment Of Industry Science and Resources, 08.11.2024). Projects such as the one sponsored by the Australian government to develop the Iluka Resources refinery in Eneabba are intended to create additional refinery capacity.

Europe follows suit

The topic is also gaining momentum in Europe. The EU has set ambitious targets with the Critical Raw Materials Act: By 2030, at least 40 percent of Europe's demand for critical raw materials is to be processed in the EU, while the proportion from individual third countries is to be limited to a maximum of 65 percent. A high level of investment and coordinated cooperation between private companies and the state sector will be required to implement this plan. One of Europe's most important players is the Belgian company Solvay. It operates one of the few processing plants on European soil on the west coast of France. The plant, which has been in operation since 1948, originally produced materials for the automotive industry, such as car batteries, catalytic converters and electronics, but is now gradually focusing its production on the manufacture of permanent magnets. Another, more recent project by the Canadian company Neo Performance Materials in Narva (Estonia) is to become the first processing plant specifically geared towards the production of permanent magnets with the support of EU funding.

At the same time, potential locations for mines are being sought in Sweden (Kiruna) and Greenland, for example, but political and environmental hurdles have so far delayed mining, which means that Europe does not yet have any active rare earth mines (FuW, 01.08.2023; BBC, 06.08.2025).

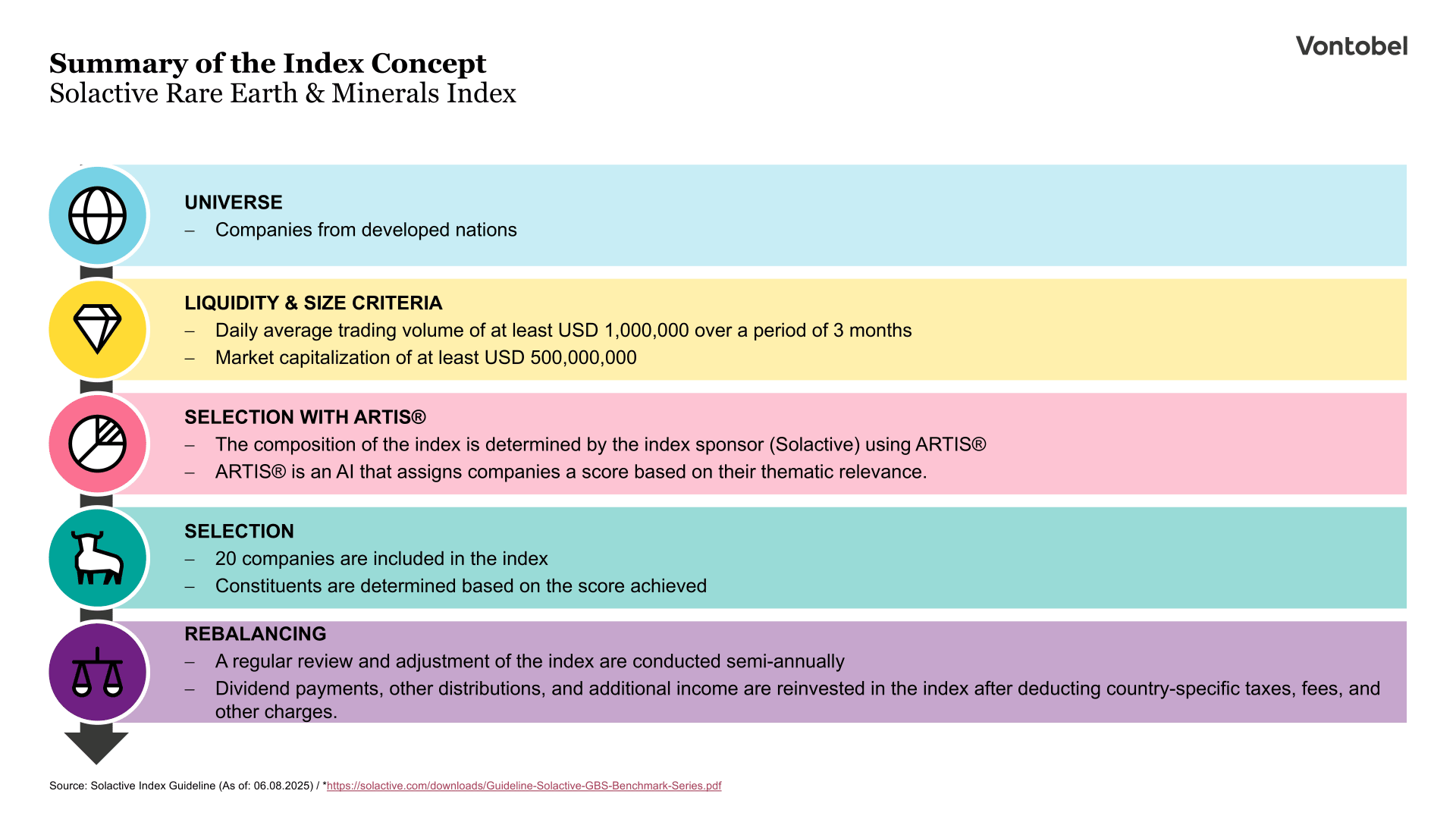

The measures show that the political will is there and initial steps are being taken, but the road to a truly independent supply chain is a long one. Heavy rare earths remain a bottleneck, and Western companies are struggling with high production costs, complex chemistry and a shortage of skilled labor. Nevertheless, the course has been set: Thanks to targeted cooperation between the state and private sectors, a competitive rare earth industry is set to emerge in the West that can take on the dominant Chinese competition. For investors who would like to participate in the development of this industry, it could be worth taking a look at the Open-End Tracker Certificate on the Solactive Rare Earth & Minerals Index from Vontobel.

Solactive Rare Earth & Minerals Index

The Open-End Tracker Certificates in CHF or USD on the Solactive Rare Earth & Minerals Index from Vontobel enable investors to build up a diversified holding in the rare earths and critical minerals sector with just a single investment. As the products have no fixed expiry date at the time of launch, they can also be used for longer-term exposure to the sector.

The Solactive Rare Earth & Minerals Index tracks the share price performance of companies active in the exploration, extraction, processing and refining of rare earths and critical minerals. These materials are essential for numerous high-tech applications, including electric vehicles, renewable energy technologies and defense systems. The index is calculated and published by Solactive as administrator. Rebalancings take place semi-annually in March and September, whereby the weighting of the companies included is adjusted accordingly. Dividends and other distributions are reinvested net in the index. The tracker certificates make Solactive's specialized index investable for investors.

Open-End Tracker Certificates on the Solactive Rare Earth & Minerals Index

License notice and disclaimer

Solactive AG ("Solactive") is the licensor of the Solactive Rare Earth & Minerals Index (the "Index"). The financial instruments based on the Index are in no way sponsored, endorsed, promoted or sold by Solactive and Solactive makes no representation, warranty or guarantee, express or implied, as to: (a) the advisability of investing in the Financial Instruments; (b) the quality, accuracy and/or completeness of the Index; and/or (c) the results that may be obtained or will be obtained by any person or entity from the use of the Index. Solactive does not guarantee the accuracy and/or completeness of the Index and shall not be liable for any errors or omissions in relation to the Index. Without prejudice to Solactive's obligations to its licensees, Solactive reserves the right to change the methods of calculation or publication in relation to the Index and Solactive shall not be liable for any incorrect calculation or any incorrect, delayed or interrupted publication in relation to the Index. Solactive shall not be liable for any loss or damage of any kind, including, without limitation, any loss of profit or business interruption or any special, incidental, indirect or other consequential damages suffered or incurred as a result of the use of (or inability to use) the Index.