Is platinum the new gold?

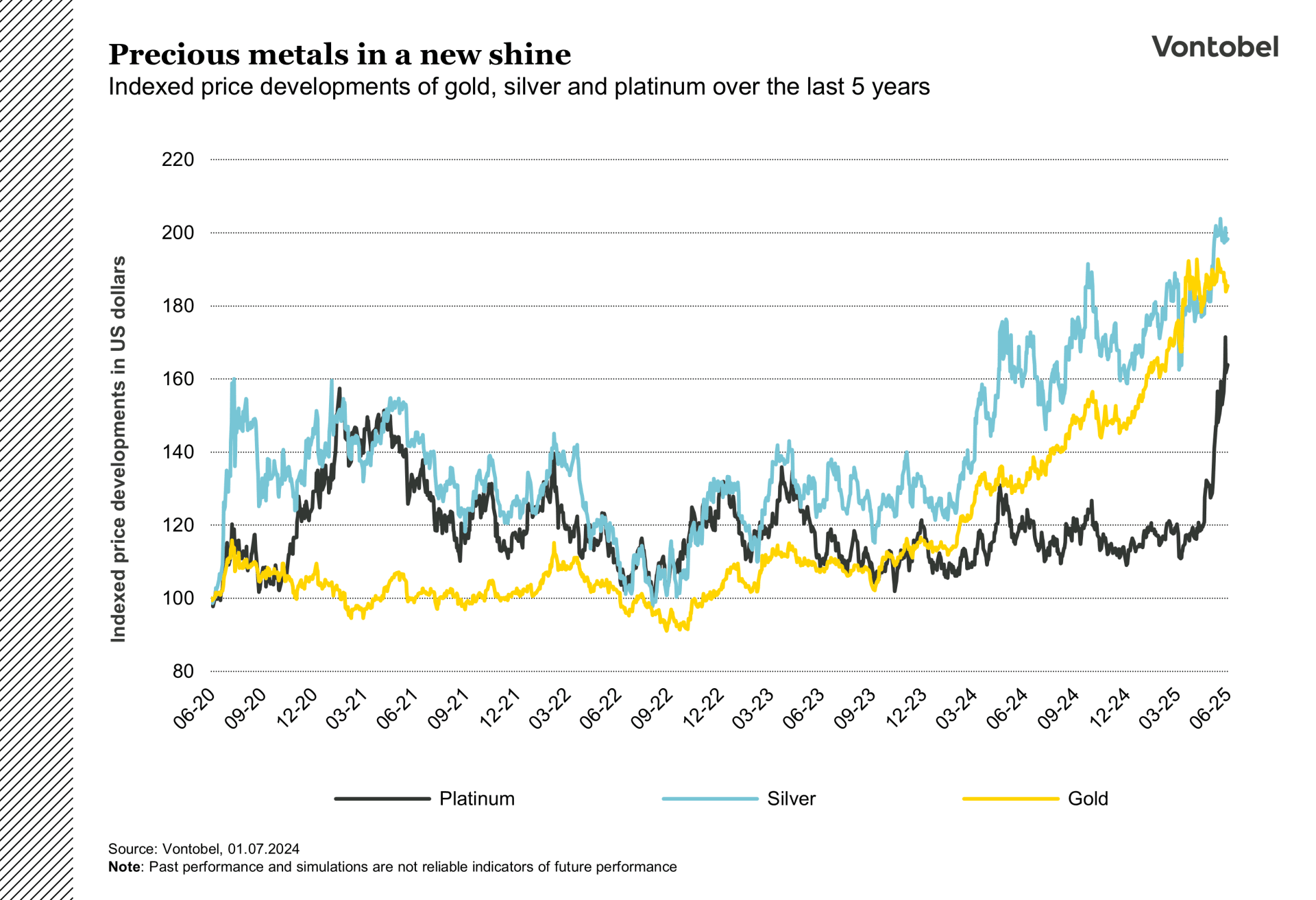

The rally in the price of gold has brought precious metal investments increasingly into focus. While the gold price appears to be consolidating at a record level, it could be worthwhile for investors to look for alternatives. Platinum could offer exciting investment opportunities. As one of the rarest elements in the earth's crust, the precious metal is widely used in industry, medicine and the luxury goods sector thanks to its properties.

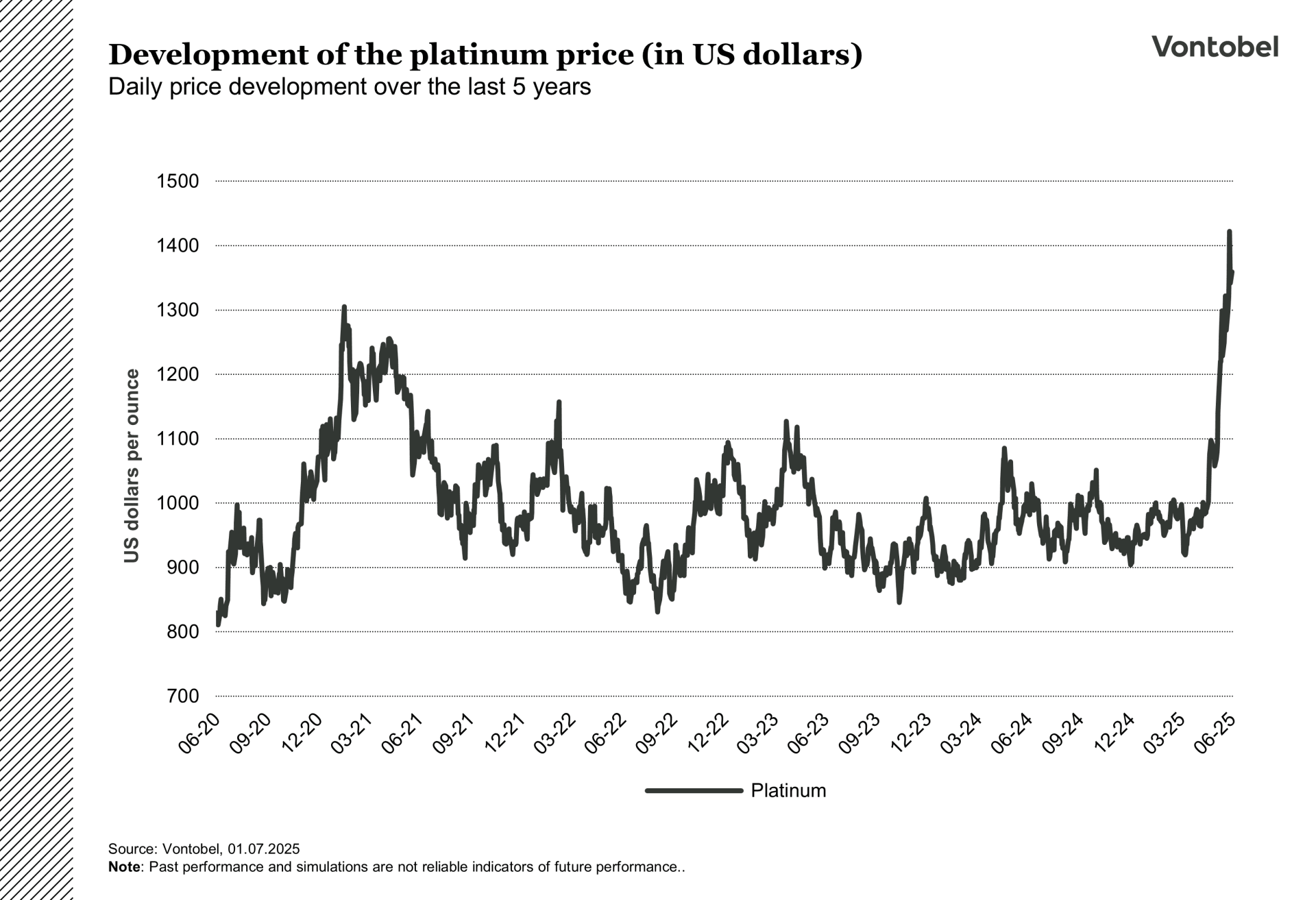

As in the previous year, the development of the gold price is in the spotlight of the investment world. Geopolitical events, the rising debt level in the US and sustained demand from central banks have led to the yellow precious metal trading at over USD 3,000 per ounce since April 2025. The price of silver also recently broke through a level that has not been reached for over 10 years. May 2025 also saw movement in the precious metal platinum after a prolonged sideways trend. The price of platinum has risen by over 35 percent since May 1, 2025. Could this rise mark the start of a long-lasting structural trend in platinum?

A versatile precious metal

Platinum is an extremely rare and corrosion-resistant metal which, together with palladium, rhodium, ruthenium, osmium and iridium, belongs to the group of platinum group metals (PGM). Its chemical properties and resistance make it a material with numerous areas of application. Platinum plays a key role in the automotive industry in particular due to its ability to catalyze: around 40 percent of global consumption is accounted for by catalytic converters, which convert pollutants in vehicle exhaust gases into less harmful substances. Stricter emission standards such as Euro 7 or China 7 could cause this proportion to rise further in the coming years.

Platinum is also used in the chemical industry, for example in the production of silicones, fertilizers and plastics. In medical technology, platinum impresses with its biocompatibility and is used in pacemakers, implants and cancer drugs, among other things. Last but not least, platinum is currently experiencing a renaissance as a jewelry metal: demand has recently risen noticeably, particularly in China, as many consumers and jewelry manufacturers increasingly see platinum as a more attractively priced alternative to gold.

Possible turnaround in the e-car boom?

Platinum has been in a prolonged bear market since the early 2010s, during which the platinum price has not seen any significant breakouts, with the exception of the period during the coronavirus crisis. The rather one-sided demand structure led the market (at least the industrial sector) to take a rather pessimistic view of the precious metal's prospects. The reasoning was that the breakthrough of electromobility would largely banish the combustion engine, and thus the use of catalytic converters, to the history books. However, current developments could now contribute to market participants increasingly questioning this rationale.

Disappointing sales figures for electric vehicles and political changes of direction, for example in Germany and the USA, are increasingly leading to the combustion engine being phased out. In recent months, the first vehicle manufacturers such as Volkswagen and Mercedes-Benz have decided to postpone or put on ice the phasing out of their combustion engine range.

While fully electric vehicles are lagging behind ambitious forecasts, plug-in hybrids are increasingly coming into focus not just as a temporary compromise solution, but as a key future mobility solution. These are vehicles that have both a combustion engine and an electric motor with a rechargeable battery.

Plug-in hybrid drive units require more platinum per vehicle than a conventional combustion engine, as the combustion engine installed in plug-in hybrids starts cold more often and the converters therefore have to be loaded with more platinum. If we conservatively calculate with an increase of just one gram more per car, the effect multiplies to 650,000 ounces of additional demand by 2030 with 20 million hybrids sold. According to the Statista platform, around 4.12 million plug-in hybrids were sold in 2024. Meanwhile, the consulting firm Alix Partners has increased its forecast for the global share of plug-in hybrids from 5 percent to 12 percent by 2030 (Reuters, 09.09.2024).

All that glitters is not gold

It is not only developments in the automotive industry that are putting the price of platinum in the fast lane. Gold has historically been valued as a "safe haven" in turbulent market phases, but its record price of over USD 3,300 per ounce is increasingly driving investors into cheaper alternatives such as silver or platinum. In China, now the most important jewelry market, jewellers imported 11.5 tons of platinum in April 2025, the most in a year (Bloomberg, 20.05.2025). This dynamic is now also noticeable on the futures market: The futures curve is in a rather rare "backwardation", in which futures prices trade below the spot price in the future. Put simply, this means that market participants are prepared to pay a higher price now in order to obtain the commodity immediately - a signal of physical scarcity (Bloomberg, 11.06.2025). Every piece of jewelry that is made from platinum instead of gold in the future draws additional metal from an already tight market. This means that platinum could increasingly move away from its status as a more industrially oriented precious metal to become a gold alternative in the world of luxury goods.

Can the supply side follow suit?

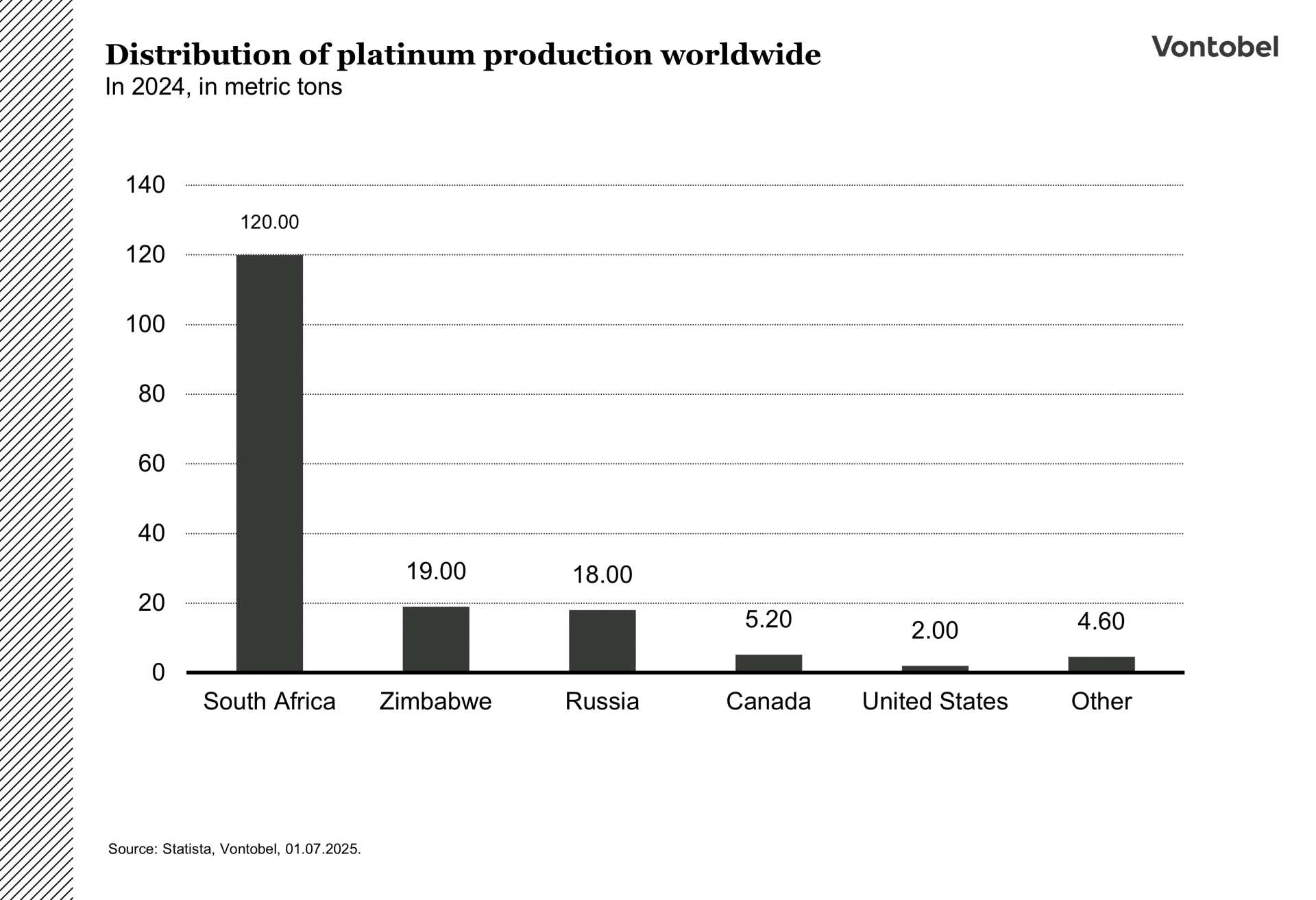

The platinum market is experiencing a structural supply deficit driven by several factors. Around 70 percent of global primary production comes from the Bushveld complex in South Africa. According to the WPIC (World Platinum Investment Council), the amount mined there fell by 10 percent year-on-year in the first quarter of 2025 alone, the lowest quarterly figure since the coronavirus lockdown in 2020. This was mainly due to unusually heavy rainfall, which severely disrupted refinery production. At the same time, global mine production fell by 13 percent in the same period, while the volume obtained from recycling processes increased only slightly by 2 percent. WPIC expects a slight recovery for the year as a whole, but output will remain below the pre-coronavirus level: according to WPIC, the forecast annual production is 6.99 million ounces, the lowest level in the last five years.

New projects such as Ivanhoe Mines' Platreef mine could provide relief in the medium term: The first production phase will start there from the end of 2025, initially with around 100,000 ounces of platinum group metals per year, with up to 500,000 ounces per year planned in the long term (Ivanhoe Mines, 08.05.2025). At the same time, numerous producers are increasingly investing in recycling infrastructure in order to increase the return flow of used catalysts. However, the availability of used material remains limited as many car owners are using their vehicles for longer and end-of-life vehicles are coming onto the market with a delay (S&P Global, 22.05.2024). According to WPIC, the recycling volume in 2024 was at a twelve-year low and could only recover gradually.

There are also geological and economic limitations to a rapid expansion of production. Many deep South African deposits are only accessible at high cost and are hardly scalable in the short term, even if prices rise. Supply could therefore remain tight in the short to medium term and market players could be prepared for structural deficits to continue to shape the price structure in the coming years.