Investor AB: The Balance Sheet That Proved Its Point

Investor AB needs little introduction. The Wallenberg family's holding company has been a cornerstone of the Swedish industry since 1916, and anyone who follows European markets knows the name. What makes this particular quarterly report worth reading closely is the timing. Early 2026 was a turbulent time, marked by geopolitical tensions, tariff fears, and a broader market that showed little sign of improvement. That is exactly the kind of environment where a company like Investor is supposed to earn its keep. This quarter, it did just that.

The Headline Number Is Better Than It Looks

The most important takeaway is simple: Investor delivered a 7 percent total return to shareholders in the first quarter while the Swedish stock market index fell by 1 percent. That is an 8-percentage point gap in just three months. Adjusted NAV, the estimated value of all holdings minus debt, rose 3 percent to SEK 367 per share. The B share closed at SEK 381.70 on April 20, meaning investors were paying roughly a 4 percent premium to the latest reported NAV. That NAV is about three weeks old, so the actual figure could have shifted depending on how the underlying holdings have moved since March 31. Either way, the market is giving Investor credit for what it owns, and then some.

Related Products

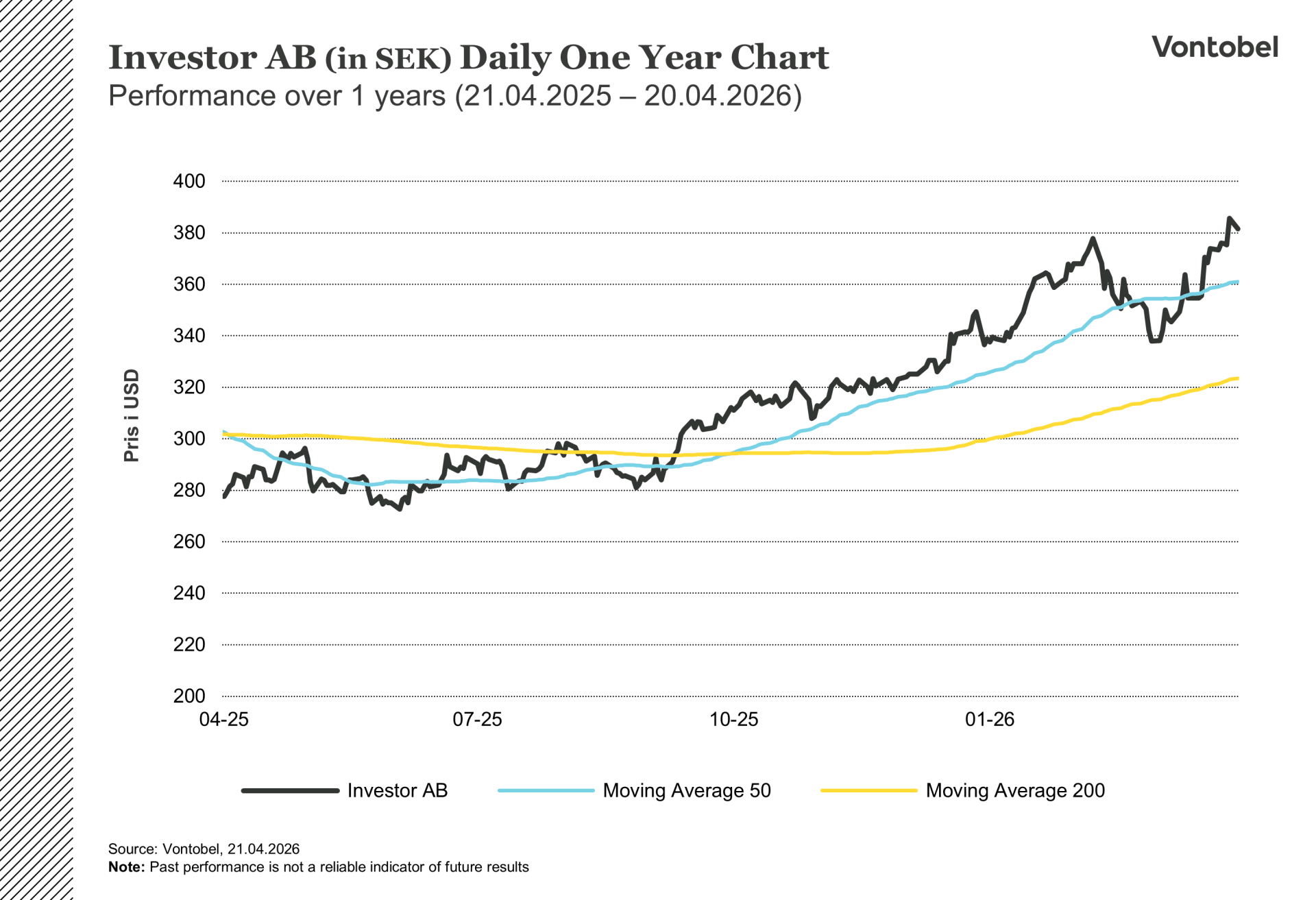

Investor AB (in SEK) Daily 1-year chart

Investor AB (in SEK) Daily 5-year chart

Walking Through What Actually Drove the Numbers

The listed portfolio, including ABB, Saab, AstraZeneca, and others, delivered a 5 percent total return in the quarter. Saab led the way, up nearly 14 percent, supported by continued defense spending momentum across Europe. ABB contributed 10 percent. These are significant positions, and they have a meaningful impact. Patricia Industries, the private investment arm, added 4 percent, partly due to the strengthening of the US dollar during the quarter, which flattered the translation of dollar-denominated earnings back into kronor. Organic sales growth across the private companies came in at 3 percent in constant currency, which was solid if unspectacular.

Then there is EQT, the global private equity manager in which Investor is a founding shareholder. That segment was weaker, with a 13 percent negative value change reducing NAV by SEK 13.8 billion, almost entirely driven by EQT AB's share price falling 22 percent in the quarter. On the positive side, gross cash increased to SEK 37.4 billion, while leverage, measured as net debt as a share of total assets, fell to just 1.2 percent. The balance sheet remains in excellent shape.

The EQT Wound Is Painful but Not Dangerous

At first glance, the EQT segment looks like a significant problem, and a SEK 14.4 billion decline in a single quarter is hard to ignore. On closer inspection, however, the picture is less negative. Investor used the weakness to add SEK 1.4 billion of EQT AB shares at lower prices, while the underlying fund investments actually edged higher. The bigger issue is the size of the EQT position itself. At current values, it accounts for around 8 percent of Investor’s total assets, which means a prolonged fall in EQT AB’s share price would keep weighing on reported NAV even if the rest of the portfolio performs well. That is the risk most analyst commentary still seems to underappreciate.

The Market Context Makes Outperformance More Meaningful

Most large European holding companies struggled in Q1 2026 as tariff fears affected industrial and healthcare stocks. Investor's diversification across listed equities, private businesses, and alternative assets acted as a genuine cushion. Companies such as Mölnlycke, the wound-care business, and Nova Biomedical, the diagnostics company, generate steady cash flows that are largely unaffected by short-term market fluctuations. Currency remains the sharpest macro variable to watch. The stronger dollar was a tailwind in Q1, but the reverse is equally true, and management acknowledged this.

Two Things Worth Watching From Here

The Mölnlycke CEO transition is an underappreciated risk heading into the next quarter. Mölnlycke is Investor’s largest private asset, with an estimated value of SEK 82.3 billion, and it is currently being run by an interim executive while a permanent replacement is being sought. At that scale, leadership uncertainty can slow strategic decision-making at precisely the moment when tariff pressure and rising Chinese competition require the opposite.

The second thing to watch is whether Nova Biomedical’s EBITA margin, which increased from 26 percent to 32.3 percent year over year, can be sustained. That improvement is the clearest sign so far that Investor’s largest recent acquisition is starting to deliver. Two more quarters at a similar level would materially change the discussion around Patricia Industries. Until then, Q1 was strong, but the most important questions remain open.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.