Will we have a white Christmas?

It was a historically tight presidential race in Brazil, ending with the win of Luiz Inácio Lula da Silva, better known as Lula. The left-wing politician and former metal worker clinched the vote at the last minute, edging out Bolsonaro with 51 % of the vote. This coincides with sugar production supply possibly not meeting demand, as ethanol production wins favour. The win of Lula opens a potential shift in market sentiment for sugar prices by removing a price cap on biofuels.

In the middle of the summer, then-incumbent Bolsonaro passed laws capping the price of fuel, trying to stem the rapid increase in prices since the start of 2022. With high inflation and rising fuel prices, the price cuts forced the state-owned company Petrobras to reduce their output prices to levels nearing 2020. That was a move that probably helped sate the increasingly displeased population. Inconsequential of the political aspect of the price cuts, they put a blanket over E25 and E100 prices, meaning, in turn, that more canes could be crushed and sold as white sugar.

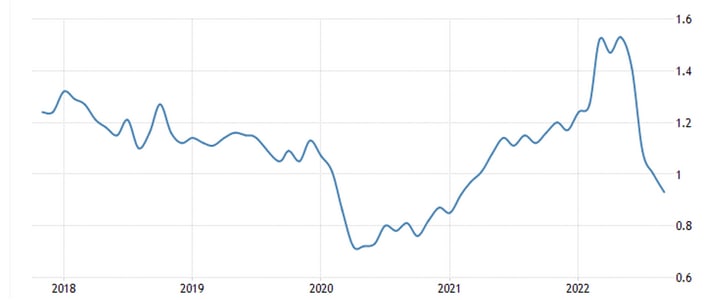

Gasoline prices (USD/Litre), a monthly five-year chart, Sep-22 reference

Lula has previously promised to decouple fuel prices from the broader economic system; more precisely, he has stressed that domestic fuel prices must not depend on an international benchmark. Since the original removal of the gasoline price gap in 2016, following a five-year stint with regulated prices, ethanol prices have covaried closely with domestic gasoline prices. This was the case until 2022, however, when prices diverged, and ethanol dropped heavily after the previously mentioned price cuts. With expectations of the current price cap being removed at the beginning of next year, this should make the pendulum swing the other way, raising prices on biofuels such as ethanol. This is further supported by sugar approaching the back half of the season with, despite a 59 % increase in harvest yield during the first half of October, production being weaker this harvest season.

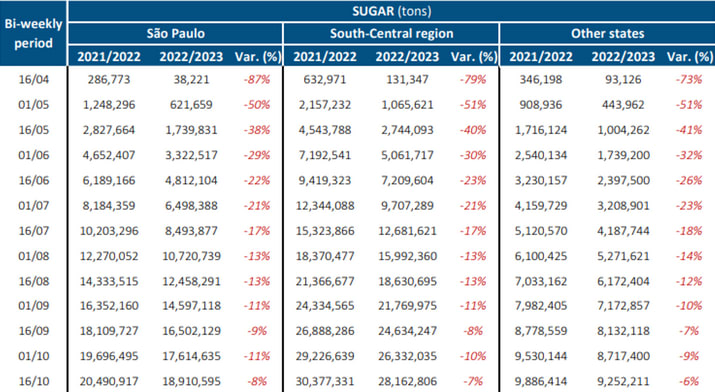

Bi-weekly accumulated sugar production (tons)

Sugar has been slumping in price during the year but might be in for a rebound. More precisely, if gasoline prices increase the demand for alternative fuels such as ethanol should increase. As this demand increases more sugar canes go to ethanol production rather than white sugar production. Assuming demand remains constant, supply should slip relative demand, and prices might rally for Christmas.

White Sugar Future Mar23 (USD/tonne), daily one-year price chart

Relaterte produkter

White Sugar Future Mar23 (USD/tonne), a daily six-month price chart

White Sugar Futures(USD), five years

Risiko

Ekstern forfatter:

Denne informasjonen er utelukkende på gjesteforfatterens ansvar og representerer ikke nødvendigvis oppfatningen til Bank Vontobel Europe AG eller noe annet selskap i Vontobel Group. Den videre utviklingen av indeksen eller et selskap samt aksjekursen avhenger av en lang rekke selskaps-, gruppe- og sektorspesifikke samt økonomiske faktorer. Hver investor må ta hensyn til risikoen for kurstap i investeringsbeslutningen. Vær oppmerksom på at investering i disse produktene ikke vil generere løpende inntekter.

Produktene er ikke kapitalbeskyttet, i verste fall er et totalt tap av investert kapital mulig. Ved insolvens av utstederen og garantisten, bærer investoren risikoen for totaltap av sin investering. I alle fall bør investorer merke seg at tidligere resultater og/eller analytikeres meninger ikke er en tilstrekkelig indikator på fremtidig ytelse. Ytelsen til de underliggende elementene avhenger av en rekke økonomiske, entreprenørielle og politiske faktorer som bør tas i betraktning i dannelsen av en markedsforventning.

Disclaimer:

Denne informasjonen er verken et investeringsråd eller en investerings- eller investeringsstrategianbefaling, men en annonse. Den fullstendige informasjonen om handelsproduktene (verdipapirene) nevnt her, spesielt strukturen og risikoene knyttet til en investering, er beskrevet i basisprospektet, sammen med eventuelle tillegg, samt de endelige vilkårene. Grunnprospektet og de endelige vilkårene utgjør de eneste bindende salgsdokumentene for verdipapirene og er tilgjengelige under produktlenkene. Det anbefales at potensielle investorer leser disse dokumentene før de tar noen investeringsbeslutning. Dokumentene og nøkkelinformasjonsdokumentet er publisert på nettsiden til utstederen, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Tyskland, på prospectus.vontobel.com og er gratis tilgjengelig fra utstederen. Godkjenningen av prospektet skal ikke forstås som en godkjenning av verdipapirene. Verdipapirene er produkter som ikke er enkle og kan være vanskelige å forstå. Denne informasjonen inkluderer eller er relatert til tall for tidligere resultater. Tidligere resultater er ikke en pålitelig indikator på fremtidig ytelse.