Listing of Volvo Cars puts focus on significant value gaps

The IPO of Volvo Cars was a success despite a debate about excessive Chinese ownership (Geely Holdings controlled 93 percent of the votes, but that now is reduced to 82%, in line with the total number of shares) during the subscription period. The share price rose by 23% on Friday, October 29, to a market capitalization of SEK 194 billion.

In this weekly trading note from Carlsquare, we elaborate on the following topics, indices, and stocks:

- Listing of Volvo Cars put focus on significant value gaps

- Is the Polestar stake a hidden diamond in Volvo Cars or a value trap?

- Valuations of automakers

- Investors don't care about the EV/sold cars-multiple

- Technology best performing S&P500-sector in the Q3 reporting season

- Apple bounced after selling pressure on report

- S&P 500 on yet another all-time-high, but time for a break?

- Nasdaq is again ahead of S&P 500

- Time for OMXS30 to close the spread?

- Will DAX approach the previous top?

- EUR/USD fell on inflation figures

- Oil finally under some pressure

Listing of Volvo Cars puts focus on significant value gaps

The IPO of Volvo Cars was a success despite a debate about excessive Chinese ownership (Geely Holdings controlled 93 percent of the votes, but that now is reduced to 82%, in line with the total number of shares) during the subscription period. The share price rose by 23% on Friday, October 29, to a market capitalization of SEK 194 billion.

It is worth noting that Volvo Cars owns 50 percent of the electric car manufacturer Polestar. On September 27 this year, Polestar announced that it intends to merge with the SPAC (Special purpose acquisition company) Gores Guggenheim (GGPI) for listing on NASDAQ in the US. GGPI is supported by businessman Alec Gores and the investment bank Guggenheim Partners. In addition to Volvo Cars, Polestar has Chinese Geely Holding and Leonardo DiCaprio as dominant shareholders.

The merger is expected to occur in the first half of 2022 and gives Polestar a valuation of around $20 billion, about SEK 170 billion. Of which 50 percent of the ownership will remain in the hands of Volvo Cars. It is worth noting that Volvo Cars' market cap is around SEK 190 billion.

Is the Polestar stake a hidden diamond in Volvo Cars or a value trap?

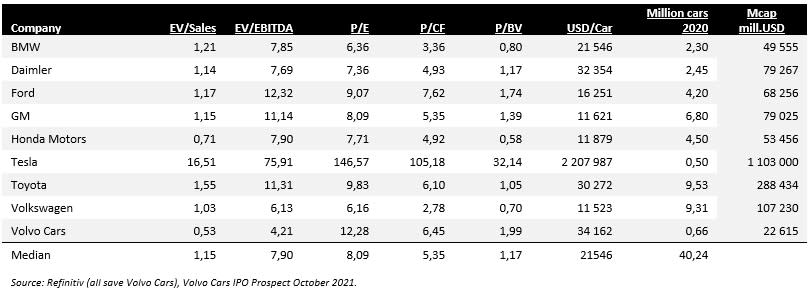

Polestar sold just over 9,800 cars in 2020. That compares to Tesla, which sold around 500,000 in the same period. The forecast is that Polestar's car sales should be almost ten-fold by 2025. A growth, if realized, would even make Tesla scratch its head. Polestar could deliver about 30,000 cars in 2021, a 200 percent growth over the previous year. The $20 billion valuations divided by 30,000 cars yield a valuation per car sold that exceeds the median of our peer group (see table below), which is about $21,000 per car. Polestar is seemingly one of the fastest-growing electric car manufacturers on the market right now and should benefit Volvo Car as the dominant owner. Should the company reach sales above 105,000 cars in 2025, this represents a CAGR of just over 60 percent between 2020 and 2025. It is a company that deserves a high valuation.

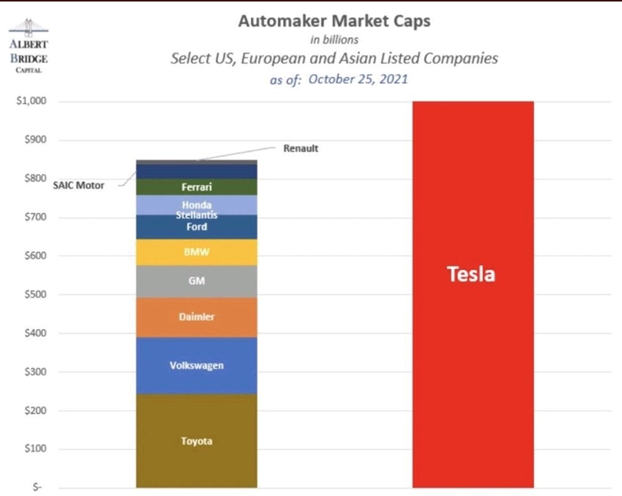

Valuations of automakers

The listing of Volvo Cars highlights the world's carmakers' valuation on the stock markets. The US electric car company Tesla, which is still considered an aspirational company, is currently valued higher than all significant and established listed car companies worldwide. These include Volkswagen, with a leading position in the European market, and Toyota, with its great historical exporting successes.

In the following table, we have compiled valuation multiples for nine major automotive companies, including Tesla (which stands out with significantly higher key ratios than the rest of the sector) and Volvo Cars. As can be seen, Volvo is valued low relative to the industry, despite its share price appreciation, in terms of sales and EBITDA. In contrast, Volvo Cars shares look more expensive relative to net income and equity. Volvo Cars are still subject to a majority shareholder discount mentioned earlier, although it now has decreased.

An essential aspect of Tesla and its valuation is the expectations of significantly higher profitability than its peers. Tesla reports an operating margin (EBIT) of 9.8 percent, in line with the median of 10 percent. However, the big difference is that Tesla's profitability is forecast to rise in the coming year and reach more than 13 percent already next year, about 40 percent higher than the sector median. In addition to the fact that Tesla sells more than just cars, it indicates that the company has a solid profitability per car sold, which justifies a higher multiple than other carmakers.

A total of 63.8 million cars were sold globally in 2020, of which the nine listed companies in the table above sold around 40.2 million vehicles combined. Furthermore, Tesla accounts for about 60 percent of the total market capitalization of the nine-car companies in the table. Dividing Tesla's market capitalization by the number of cars sold in 2020 (around 0.5 million) gives a market capitalization per car sold in 2020 of about USD 2.2 million (!) In fairness, Tesla has the highest growth in the sector, but still, it is remarkable. As can be seen, the median value (market capitalization per car sold by each company) is just over USD 21 thousand (i.e., about one percent of Tesla's "car value"). Volvo cars are in the premium segment, which is equivalent to a higher price per car.

Investors don't care about the EV/sold cars-multiple

Investors do not care about the number of sold cars as Tesla just joined the trillion-USD club together with Microsoft, Apple, Alphabet, and Amazon. The Tesla shares gapped up on a large order from Hertz and are approaching the 250 percent line from the local bottom in May 2021. The RSI is on scream sell levels, even though the RSI alone has little signal value.

Tesla daily share price chart, March 26 to October 29, 2021

Source: Refinitiv Eikon and Carlsquare

The weekly chart below visualizes last week's strong move even better.

Tesla weekly five-year share price chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Technology best performing S&P500-sector in the Q3 reporting season

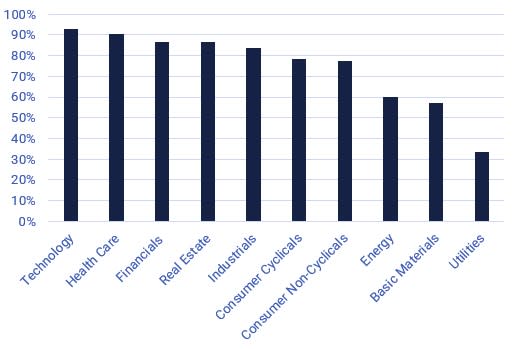

Last week, 163 of the S&P500 companies reported. We now have 280 companies, or 56% of the total, that have reported their Q3 results. The share of positive earnings surprises now stands at 82 percent, while 76 percent of revenues for the reporting companies were higher than forecast.

Technology has been the best performing sector in the S&P500 index with 93% of companies' results better than anticipated in Q3, followed by healthcare, with 91% positive earnings surprises. Notably, healthcare has not been a trendy sector lately. For the big US pharmaceutical companies, momentum could shift to more positive.

S&P500 sectors ranked by share of Q3 2021 earnings better than expected

Source: Refinitiv Eikon

FANG technology stocks dominated the flood of reports on the New York Stock Exchange last week. In our study, we have included Netflix, which reported back on October 19 and Microsoft (which is not a FANG company). Three of the six technology companies surprised investors positively: Netflix, Alphabet (Google), and Microsoft with 24.6, 19.2, and 9.7 percent better earnings, respectively, than Analysts' forecasts. Apple and Facebook were almost in line, while Amazon was significantly worse (minus 31.4 percent) than analysts' earnings forecasts. We saw a positive share price reaction in all three earnings outperformed companies during the last week, plus 4.2 percent in Netflix, 7.6 percent in Alphabet (Google), and 7.2 percent in Microsoft.

Apple bounced after selling pressure on report

Apple reported in line with expectations but is waved a flag for supply chain issues, including lack of chips for its latest iPhone. The share also fell on Friday's opening but managed to recover most of the losses with some help from the general market sentiment. Momentum is positive and rising, as shown by MACD in the chart below.

Apple daily share price chart, March 26 to October 29, 2021

Source: Refinitiv Eikon and Carlsquare

In the weekly chart, Apple is trading above rising EMA9 and MA20. But given the report, we would be surprised if new highs emerged before the Q4 2021 report is released.

Apple weekly five-year share price chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

S&P 500 on yet another all-time-high, but time for a break?

S&P 500 index closed last week on a new all-time-high. RSI is on overbought levels.

S&P 500 daily chart, March 26 to October 29, 2021

Source: Refinitiv Eikon and Carlsquare

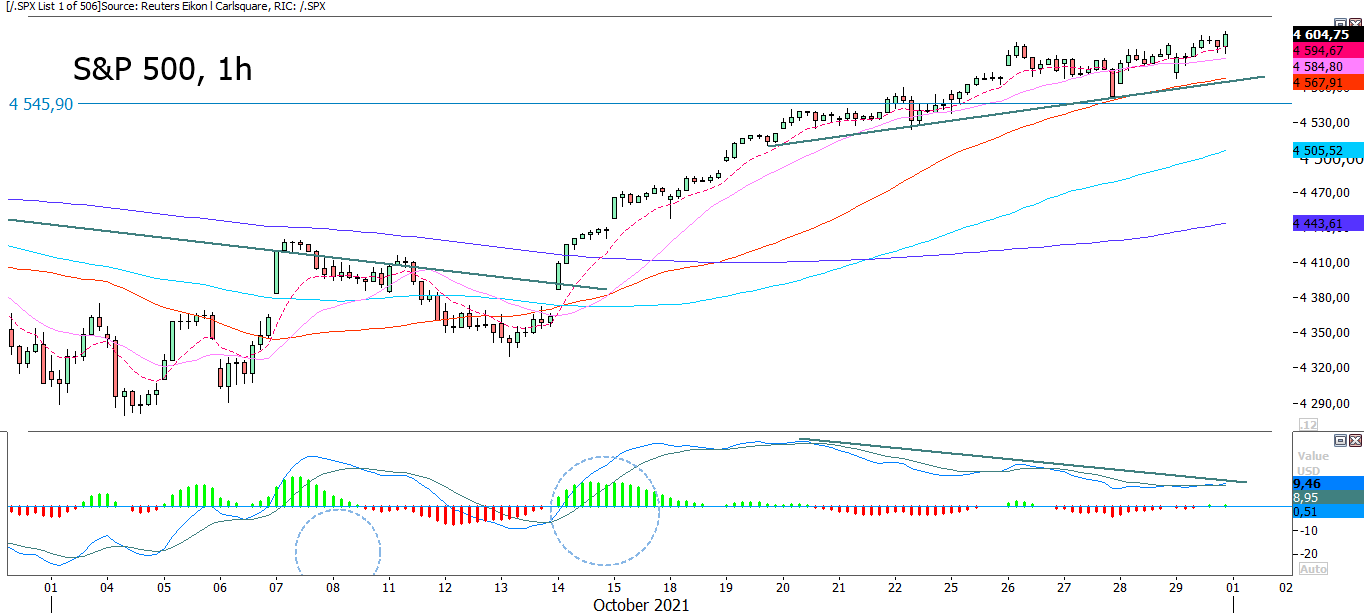

In the 1-hour chart below, one can see how the index is trading nicely and slightly upwards above rising EMA9 and MA20. Note, however, the negative divergence between the index and MACD. Let the trend be your friend but keep an eye on the rising trend line and MA50 in the hourly graph. In case of a break to the downside, the previous high around 4 545 could be next.

S&P 500 1h-chart, September 30 to October 29, 2021

Source: Refinitiv Eikon and Carlsquare

The weak sell-signal generated by MACD in the weekly chart remains as the last given signal:

S&P 500 weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Nasdaq is again ahead of S&P 500

As S&P 500 set a new all-time high last week, so did Nasdaq 100. All moving averages, as well as MACD, are pointing upwards. RSI is on overbought levels.

Nasdaq 100 daily chart, March 26 to October 29, 2021

Source: Refinitiv Eikon and Carlsquare

Nasdaq is again ahead of S&P 500, YTD, even though with little margin:

Source: Refinitiv Eikon and Carlsquare

Negative divergence in the weekly chart remains. A setback to gathering some energy may be in the cards.

Nasdaq 100 weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Time for OMXS30 to close the spread?

Last week was terrible for OMXS30, but as shown in the graph below, the index managed to hang on to MA20. With the optimistic glasses on, this is a signal of strength. Is long OMXS30 short S&P 500 an interesting spread?

OMXS30 daily chart, March 26 to October 29, 2021

Source: Refinitiv Eikon and Carlsquare

Below is the relative performance spread in orange. Note how the spread has come together from these levels in September 2020 and around the year-end 2020 and early 2021.

Source: Refinitiv Eikon and Carlsquare

In the weekly graph, the index closed below MA20 as well as EMA9. MACD is falling. That is speaking for caution in OMXS30. A clearer bounce of MA20 in the daily graph above would add some comfort.

OMXS30 weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Will DAX approach the previous top?

German DAX tested EMA9 and MA100 on Friday. As can be seen in the graph below, the two levels held. However, DAX is also lagging S&P 500 as the index has not yet managed to try previous tops. Long DAX short S&P 500 may, from a technical perspective, be a less risky trade.

DAX daily chart, March 26 to October 29, 2021

Source: Refinitiv Eikon and Carlsquare

From a technical point of view, DAX also looks more attractive viewing the weekly chart. As can be seen, the index managed to close last week above MA20 and EMA9. Nevertheless, MACD is falling.

DAX weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

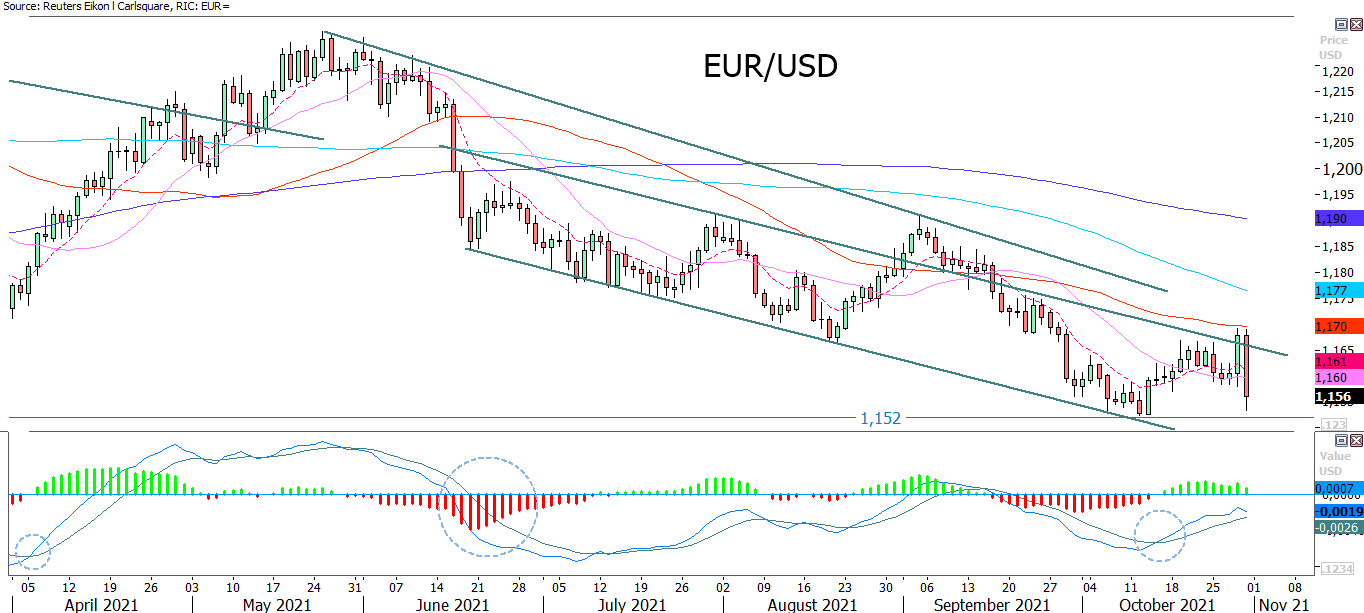

EUR/USD fell on inflation figures

The interest rates in the US rose on Friday, October 29, as the Federal Reserve's preferred inflation measure showed prices continuing to grow faster than its two percent target. That also put some pressure on the EUR/USD that fell to close below MA20. Will the 1.152-level be tested?

EUR/USD daily chart, March 26 to October 29, 2021

Source: Refinitiv Eikon and Carlsquare

In the weekly graph, one can see how MA200 once again is being tested. In case of a break, Fibonacci 50 around 1.145 could next.

EUR/USD weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

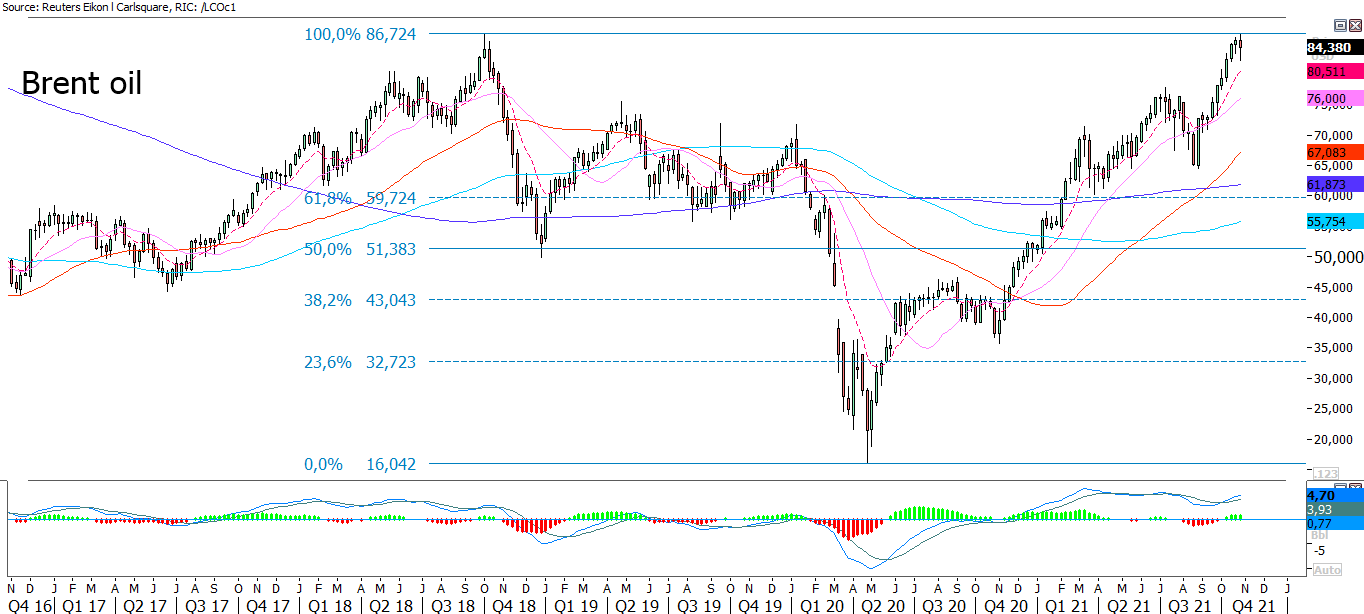

Oil finally under some pressure

Brent oil is finally under some pressure, and the strong USD is not helping out. The graph below shows that the Brent oil price has fallen below EMA9, now supported by MA20. Also, note how MACD has generated a weak sell signal. In case of a break, levels around 81.5 USD per barrel could be next.

Brent oil daily price chart, March 26 to October 29, 2021

Source: Refinitiv Eikon and Carlsquare

The weekly chart also shows how Brent is trading close to the previous top from Q4 2018.

Brent oil weekly five-year chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence of numbers in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Riskit

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance.