Don’t fight the Fed

Quick and steep increases in interest rates sends prices of financial assets down.

I have previously written an article about the effects of increasing interest rate. The article was based on classical financial theory and described how a rise in interest rates feeds directly into the pricing models for all assets that are valued as the "present value of future cash flows". After all, most people are familiar with how interest and compound interest can cause an amount you put in the bank to grow from year to year. A higher interest rate gives a higher effect. For the pricing of shares, this effect works the opposite way. An increase in the interest rates used to discount the future cash flows will reduce their present value. The further into the future these incomes are assumed to be, the stronger the impact of an increase in the discount rate. That high-growth companies in technology have been hardest hit by the current rise in interest rates is therefore completely logical.

This effect does not only apply to shares, but also affects bonds and commercial property. What makes shares different from these two other asset classes, however, is that in addition to the pure interest rate effect on the pricing of the future cash flows, you can also have the second-round effect that higher interest rates lead to a more unfavorable business environment, which in turn means that the assumed future cash flows will most likely be smaller. After all, it is the companies' profits that are discounted in the net present value models. Profit is revenue minus costs. Most companies have loans in addition to equity, and higher interest on the loans will, all else being equal, directly contribute to reducing profits. If worse times also lead to lower sales, income will also be lower.

I have seen several analyzes from

economists in brokerage houses who point out that the fall in the stock markets

so far roughly corresponds to a mathematical adjustment to the effect of a rise

in interest rates. Going forward one can expect that higher interest costs and

lower calculated income will find their way into the analysts' spreadsheets. It

is difficult to imagine that this will not lead to downgrading of earnings

estimates and thus lower target prices.

In addition to these two effects, interest

rates have now risen to such an extent that one can also have a significant

so-called substitution effect for investors. While the interest rate was close

to zero, many people talked about the fact that there was no alternative to

shares if you wanted a return. TINA – There Is No Alternative. When it is now

possible to get a rather nice interest rates on American government bonds, TINA

is history.

How high can interest rates go, and when will the quick pace of increases stop?

The only correct answer to this is "nobody knows". If you want to make a qualified guess, you can, however, rely on two good sources. One is to listen to the central banks themselves. After all, they are the ones who set the interest rate. The signals from there are that interest rates will continue to rise at the upcoming central bank rate meetings, then reach a peak and start to come down again approximately in 2023-2024. Now it must be said that all central banks have been notoriously bad at hitting their own estimates for future interest rates. In the short term, however, the picture is reasonably clear: Interest rates are still on the rise, and we haven't seen the peak yet.

The other source I rely on is technical analysis. Simply looking at price behavior and studying charts to look at similar situations. The chart below shows the current interest rate on 5-year US government bonds going back to 1962. Since the chart displays such a long period of time, monthly prices are shown. In the bottom row of the chart you can see the technical momentum indicator RSI (Relative Strength Index). This can tell something about the speed/length of the current trend movement. Traditionally, values above 70 are considered "overbought" and values below 30 as oversold. The 14-month RSI on the US 5-year is now at 79.35. This is very high, but as we see there are several times in history where this level has been reached and also exceeded.

There is basically nothing in the chart

that yet indicates a peaking, flattening or reversal of the current interest

rate movement. The 5-year is now close to 4% On the chart, we see that the

level around 5% marked several interest rate bottoms until the turn of the

millennium, and after that it has been the level for some peaks. Is it

inconceivable that we will go there again? No, it is not. In any case, the

direction in interest rates still seems to be upwards. They have also come up

so quickly that the effects have not yet had a chance to spread in the real

economy. It is reasonable to assume that it will continue beyond autumn and

winter, and that is also the central bank's intention. Don't fight the Fed

(Federal Reserve) was a well-known mantra in the bull market that went on while

the Fed was running its quantitative easing. It is safe to say that it still

applies, but this time with the opposite sign in the market.

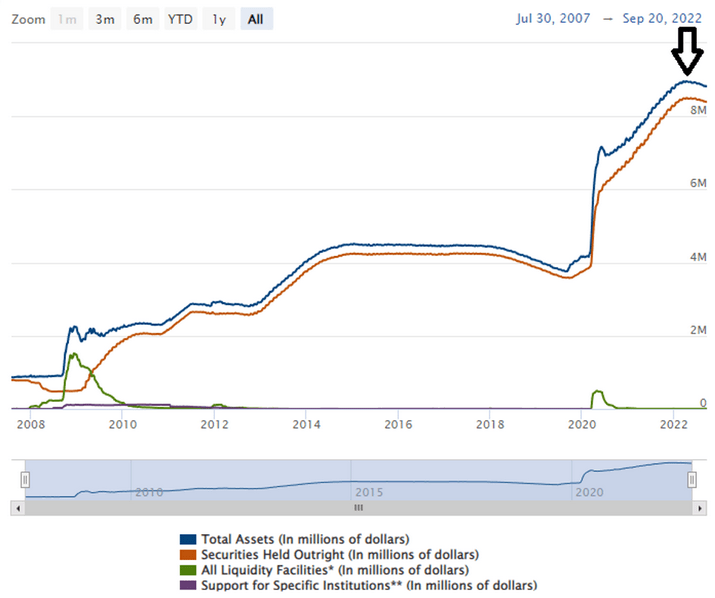

It must also be remembered that the key

interest rate is only one of the tools at the Fed's disposal. They are also in

the process of reversing the enormous quantitative easing that inflated the

central bank's balance sheet and provided significant stimulus to the market.

On the Fed's own website, you can see that this reversal has only just started,

and the chart below is borrowed from there. In fact, the speed of the reversals

doubled this month, and the plan is to keep the speed at this level for some

time to come. The arrow indicates where the turn started.

Knock-Out Warrants

Disclaimer: After many years in the brokerage industry I started my own business in 2021. I published the book "Paleo Trading: How to trade like a Hunter-Gatherer” and launched a hedge fund that trades according to the principles described in the book. Vontobel asked if I would write posts for their blog, similar to what traders and managers do in other countries. I must emphasize that nothing written on this blog is to be regarded as personal advice or a concrete call to take positions. Everyone must be responsible for their own decisions and familiarize themselves with the products they use.

Risks

Legal notice:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance.