Don't listen to what they say

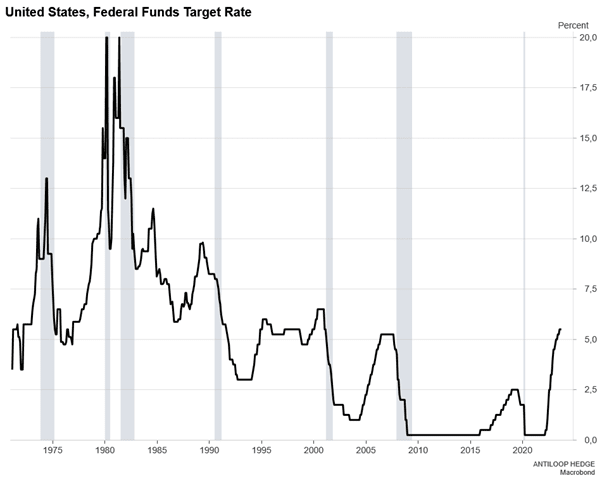

Another increase after the break. That's what the Federal Reserve says when asked about where interest rates will go next, followed by "higher interest rates for an extended period" and "soft landing for the economy" while the market prices in 2 percent inflation for the next 30 years.

For those who pay attention, it all sounds like an echo. QE wouldn't last forever either, and the economy would also soften in 2008 and interest rates should always go up after that pause that comes when too-rapid austerity after a long period of stimulus begins to take effect.

Now, in and of itself, history is not a guarantee of the future, but it can still be interesting to study. Let's start with the statement about further rate hikes after the break. Never before in US history has a pause been followed by another hike without us seeing lower rates first. Moreover, sharply rising interest rates have always been followed by a recession. So I would rather place my bet that what we will see in the future is probably a repetition of history rather than a new paradigm.

Inflation then?

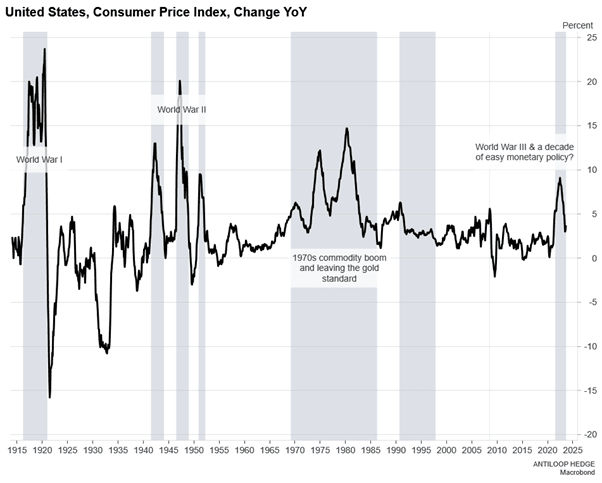

Despite the fact that inflation both in the US and in many other places has come down to lower levels, it is not a sign that the problem has been solved for the coming years. If we look at history there too, we can state that not during a single occasion when inflation has exceeded 5 percent have we only seen a peak.

In the same way that inflation is not created overnight, we can expect inflation to disappear just as quickly. High inflation is not fought in one or two years, it often leads to a secular trend that lasts for a decade or more.

How can you protect your capital and your portfolio?

Whether you believe in a coming period that is more like the decade we just left behind, with low interest rates and lots of stimulus, or, if you believe, like me, that inflation will make another entrance after the Fed is forced to cut interest rates as a result of a slightly harder landing than expected, there are alternatives.

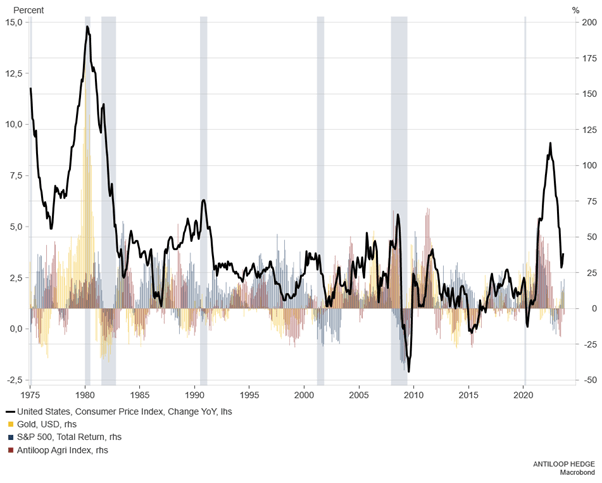

(Yes, here too it can be useful to study history). The graph below shows the US inflation rate YoY from the year 1975 along with how the asset classes gold, agricultural commodities and stocks have performed both during periods of high and low inflation. One of the clearest trends is, of course, that stocks underperform during recessions and after periods of high inflation, and that gold and agricultural commodities tend to outperform during the same period. However, this does not mean that an investor should invest in just one of these assets, but spread his risks over several over time.

The key here is correlation . High risk-adjusted returns over time, under different types of market paradigms, are created by diversifying one's portfolio in low-correlation asset classes. Gold and agricultural commodities are good options, but there is much more to choose from for those who are curious and want to find their own perfect allocation strategy.

Risks

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.