Is Nvidia a value play?

Nvidia surprised the market when the company last week reported revenues for the first quarter of its broken fiscal year 2024.

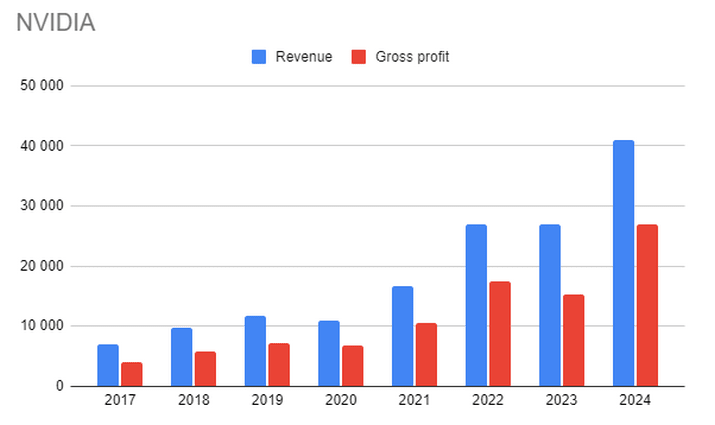

Sales fell only 13% to $7.19 billion from $8.29 billion in Q1 last year. That was clearly better than in the previous quarter, when Nvidia's revenues fell 21% year-on-year, or the quarter before that when the decline was 16.5%. In that perspective, a decline of only 13% was a step forward.

In the second quarter of last year, things looked a little better. Sales increased by 3% compared to the same period the year before. This is the quarter Nvidia will be measured against next. And this is where the real surprise happened. Despite all the reports and analysis about the high demand for Nvidia's AI chips from Amazon, Microsoft, Meta and others, no one was prepared for the fact that Nvidia would suddenly sell 11 billion in a single quarter. This is 50% more than expected, and a yearly growth of 64%. Nvidia has really managed to take full advantage of the LLM hype. The question is where the ceiling for the demand for Nvidia's superior chips is. In practice, only Nvidia's products can power Chat GPT, Midjourney, Bart and other popular AI services. I think Q3 and Q4 revenue could be a bit higher than the recent Q2 guidance, but not much more than that. Production and prices are already close to max thanks to the hype.

Nvidia did not provide guidance on earnings, but given the profit margin in the just-reported first quarter, earnings in the next quarter could possibly be as large as the whole of last year, around USD 1.75 per share. If this new level is maintained for the rest of the year, we are talking about about $6 per share in earnings for the current year. With a growth rate of 40% per year after that, profits will double every two years, to USD 12 in just under three years and USD 24 in just under five years. Then the valuation at the current price of USD 380 is down to 16 times earnings, i.e. like an average listed company in an average year. So you lose five years in time, but you get a fantastic company in the bargain. NOTE! This would be an unusual and unexpectedly positive development for Nvidia. The growth rate has normally only been around 25% per year. The series looks like this: 41%, 21%, -7%, 53%, 61%, 0%, [52% this year?]. This is actually not very impressive, or at least nothing that guarantees as much as 40% annual growth over several years. Semiconductor companies never have unbroken series of such high growth, probably not even the future Nvidia.

Moreover, the years before the above series, i.e. 2014-2017, were clearly worse, with annual growth rates of a low -3.5%, +13%, +7%, and +38%. The average for 2017-2024 is 30%. This is measured from the year with 38% growth, i.e. selected to give the highest possible average, to the current year - assuming an optimistic +52% for the whole year. To assume more than 30% is to really hope for a new era for Nvidia. But yes, one can argue for a profit growth of 40 percent per year, driven by rising prices and margins, in addition to the volume growth the company manages to squeeze out of the factories. If nothing else, the market is likely to price in those kinds of numbers, now that the quarters are showing annual growth rates of over 60%. By the way, I have entered 90% for the last two quarters of the year to get to the annual profit of USD 6.28, and then 40% per year to reach USD 24 in 2027 (the year Nvidia calls 2028).

So is Nvidia a value play? Yes, it is, if you keep what you promise in Q2 and then maintain that level and a little more in the second half of the year (which then becomes a 90% growth rate for H2), and finally grow at a historically high 40% per year for four more years with maintained record margins from the Chatbot year 2023. Then you get Nvidia at the same price as an average stock market, which is to be considered really deep value for such a company. On the negative side, you get the risk of production disruptions at TSMC in Taiwan. You also get the risk that the most intense AI hype fades, which means a more normal growth rate of 25% rather than 40%, and then it takes 6 years instead of 4 to reach the same annual profit. Then there are (as always) a number of macro threats. Perhaps there will be problems related to the US debt ceiling. Maybe there will be no interest rate cuts by the Fed. Maybe an unexpectedly deep global recession strikes.

You can go back and forth like this endlessly. In practice, the buyers and sellers of Nvidia have agreed that at USD 380/share the opportunities and risks are balanced. To put my foot down, I want to emphasize that I think the stock is too expensive today, that the macro risks are greater than the potential for Nvidia to grow by 90% in the second half of the year and then by 40% per year for 4 years. What I mean is that I think that if you pay 380 USD per share, you will get a poor average annual return over the next five years. But on the other hand, I think the market in the near future will love the next three quarterly reports and that it will ignite a fantasy of more than 40% growth, and not least of a sustained high level even beyond the calendar year 2027. Then suddenly 380 USD / share and thus a P / E figure of 218 for the last reported annual profit looks like a real value play! In theory, it is only 16 times 2027 earnings.

In today's euphoria, I understand that it is easy to ignore the fact that it is five years away. The price may therefore just as well go to 500 (P/E 2027 of 21) or 600 (P/E 2027 of 25) this year. If Nvidia achieves about USD 11 billion in revenue per quarter for the rest of the year, it will probably hurt to be short the stock from USD 380.

Nvidia stands out in this reporting period, but a similar argument can be made for several other companies in The 500+ Billion Dollar Club. They attract all the attention, capital, fund flows and customers when the rest of the market is sluggish. Alphabet, Tesla, Microsoft, Meta, LVMH have similar investment calculations behind them. Maybe it's time for Amazon's stock to take off in earnest?

The winners take it all in this stock market phase, but I am still afraid that this, the narrow market, means that we are close to the top this time.

Risks

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.