Gold is gold to have in the portfolio

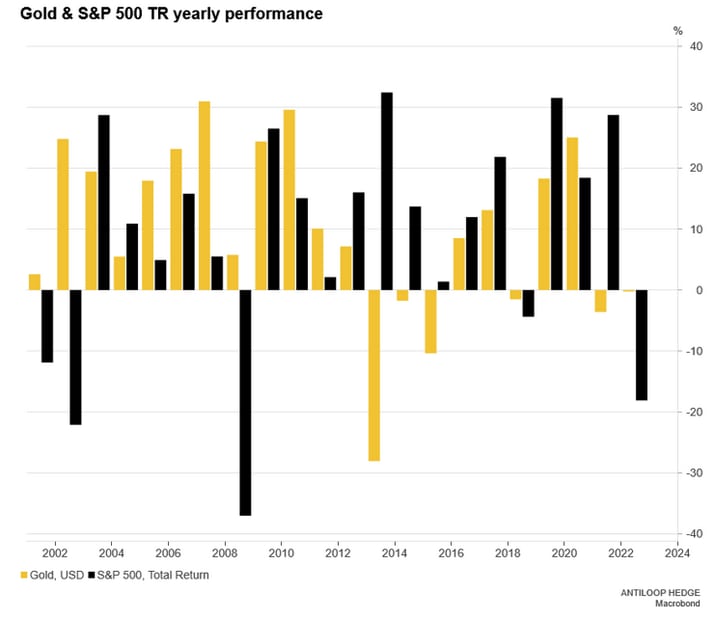

Since the year 2000, the gold price in USD has risen on average more than 9 percent annually, which can be compared with the S&P 500 TR, which on average during the same period returned 8.5 percent annually.

Both, Gold and S&P 500 also faced years with negative performance over the time. Despite gold's total development of 538 percent since the year 2000, many are now questioning gold's role as an inflation hedge because the gold price in USD has mainly moved sideways after the peak in August 2020 and whether gold even has an obvious role in a portfolio.

But the question is: does gold work as a good complement to stocks?

Depending on what you want to achieve with your portfolio in the long term, gold can function as an important component or not. Contrary to what many investors have learned since the financial crisis, an investor who has the goal of as high a risk-adjusted return as possible should add one or a few diversified assets with low correlation to his portfolio.

If the goal is to own as much productive assets as possible over time, an asset such as gold can act as a good hedge against declines in the stock market. by investing part of your capital in gold short- or long-term, you can then sell the asset that rises in relation to the other and thus have cash left to buy more shares.

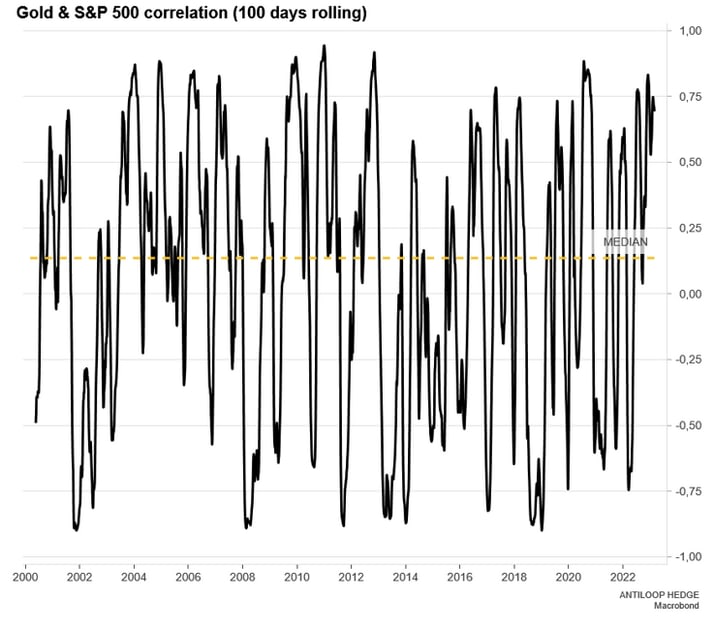

Gold and stocks rarely have bad years at the same time, which makes gold a good complement to stocks.

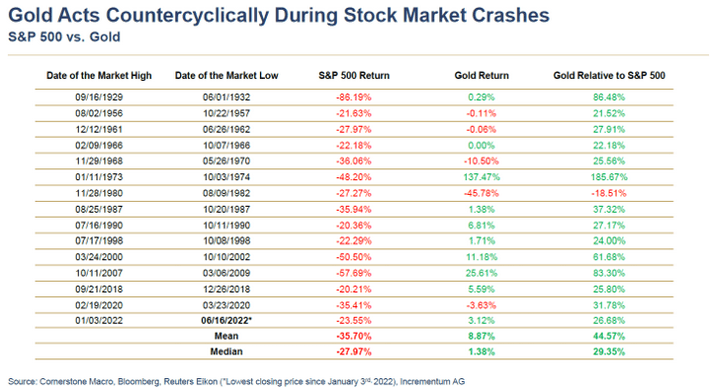

Historically, during larger and longer stock market downturns, gold has also, in both relative (with one exception) and absolute terms, functioned as a hedge against downturns. During the 1970s, for example, which was marked by high inflation for an entire decade, gold rose between January 11, 1973 and October 3, 1974 over 137 percent and relative to the S&P 500 over 185 percent. During the 2007-2009 financial crisis, gold in USD rose over 25 percent and relative to stocks 83 percent.

As an example: if at the start of 2007 (the stock market crash only started in October 2007) you had held 40 percent gold and 60 percent S&P 500, your capital at the bottom of the stock market crash would have been worth almost $89,000 compared to if you only owned the S&P 500 then you would have just under $50,000.

It is also important to note that gold not only acts as a protective factor against stock market downturns but also as a long-term investment in itself. Central banks globally have in recent years increased their net purchases of gold as part of their portfolio, showing that gold still has a role to play in a diversified portfolio.

According to the World Gold Council, central banks globally held a total of 35,197 tons of gold in their reserves at the end of 2020, which represents about 17 percent of all gold ever mined. This can be compared with 32,908 tonnes 10 years earlier and 30,412 tonnes 20 years earlier. This shows that central banks continue to see gold as an important part of their portfolio and an important tool to protect their assets.

It is also worth mentioning that the demand for gold for industrial use continued to increase, especially in electronics and medical equipment manufacturing. This increases the demand for gold and may cause the price of gold to rise in the future, which may be an additional reason to consider including gold in one's portfolio.

Risks

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.