Europe is buying an army faster than it can build one

Germany approved more defense spending in 2025 than in the previous eight years combined. In December alone, a parliamentary committee signed off on 52 billion euros of new orders for tanks, frigates, air defense systems, and ammunition. However, the vote received little attention (Bloomberg, 2025). Spending of this magnitude, which would have once prompted a national debate, now passes as routine. Germany is not alone in this trend. Across Europe, governments are rearming at a pace unseen since the Cold War. Their commitments now extend years into the future rather than being made on a year-by-year basis.

A decade of rearmament

European NATO members increased military spending faster in 2025 than in any year since 1953, reaching 864 billion dollars (SIPRI, 2026). At the Hague summit last June, the alliance agreed to a new target of spending 5 percent of GDP on defense by 2035, 3.5 percent of which would be allocated to core military capabilities, retiring the 2 percent floor that had stood for over a decade. Unlike earlier pledges, these commitments are hard to walk back. By reforming its constitutional debt brake, Germany has exempted all defense spending above 1 percent of GDP from its borrowing cap, lifting the fiscal constraint that had held its military back since the Cold War. Berlin plans to spend 144.9 billion euros on defense in 2027 and aims to reach the 3.5 percent core target by 2029, which is six years ahead of schedule (Financial Times, 2026). Sweden has also set aside more than 170 billion kronor in additional defense funding through 2030, its largest buildup since the Cold War, with the goal of reaching 3.5 percent of GDP by the end of the decade.

The money is spread unevenly across the continent. Poland, Norway and Denmark already spend above 3 percent of GDP, with Finland and Sweden close behind. Meanwhile, Italy, Spain and France lag well short of the new target (NATO, 2025). The buildup is heaviest in the north and the east, closest to Russia, where the threat is felt most directly and where governments can also afford to act. These are also the countries whose orders flow most directly to their own national champions, Saab in Sweden, Kongsberg in Norway, and Rheinmetall as Germany rebuilds.

The capacity problem

The hard part is not deciding to spend the money but rather turning it into delivered equipment. Rheinmetall, the German group that has come to symbolize the rearmament, reported first-quarter revenue of 1.9 billion euros, below expectations of 2.3 billion. However, it maintained its full-year guidance of 40 to 45 percent revenue growth (Financial Times, 2026). The shortfall did not come from weak demand but rather from approved budgets that were not quickly converting into signed contracts. This occurred after German procurement slowed during an election period and a large artillery contract was sent back for procedural review.

Slow procurement is only a visible part of the problem. After three decades of steadily shrinking its defense industry, Europe simply does not yet have the capacity to produce. Rheinmetall produced around 70,000 artillery shells in 2022 and aims to produce roughly 1.5 million by 2030. However, explosives and propellants remain scarce across the continent. New factories take two to three years to become operational, and skilled workers are difficult to find after a generation of decline. No matter how much governments want to spend, output can only grow as fast as industry can keep up.

What it means for Saab

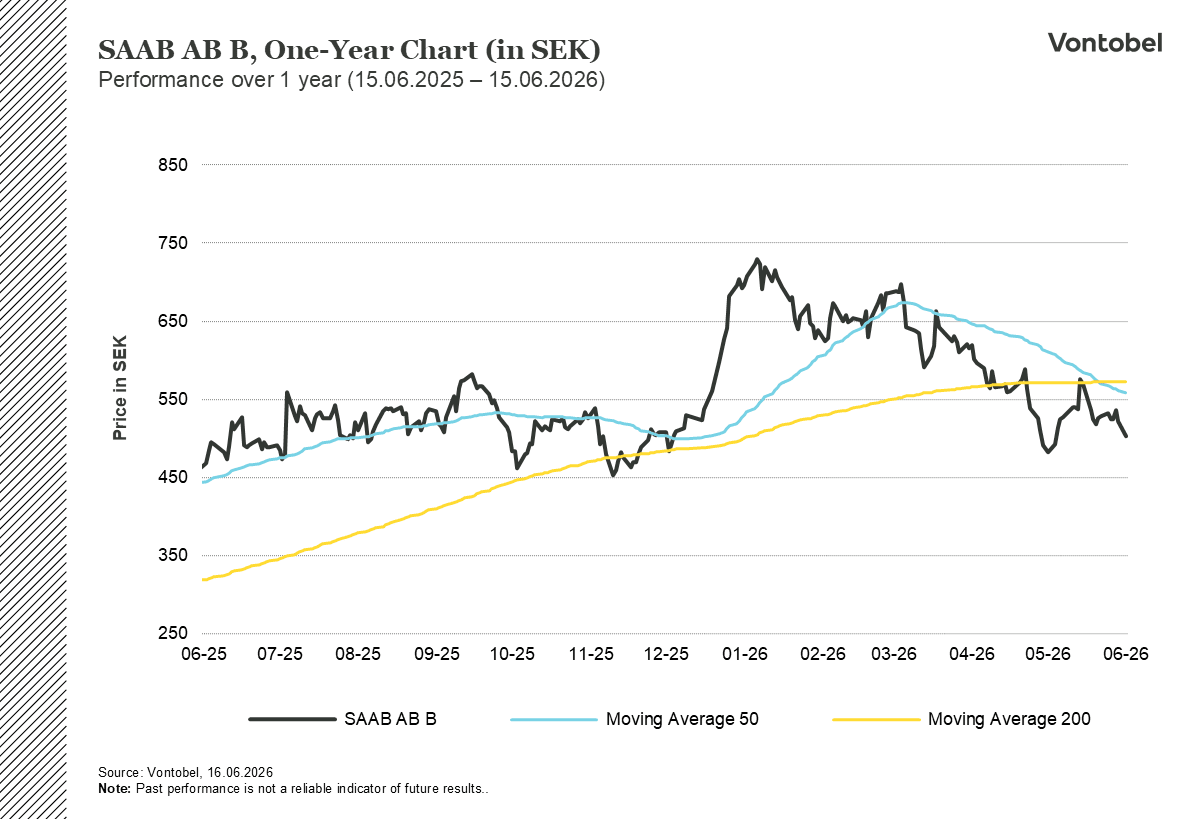

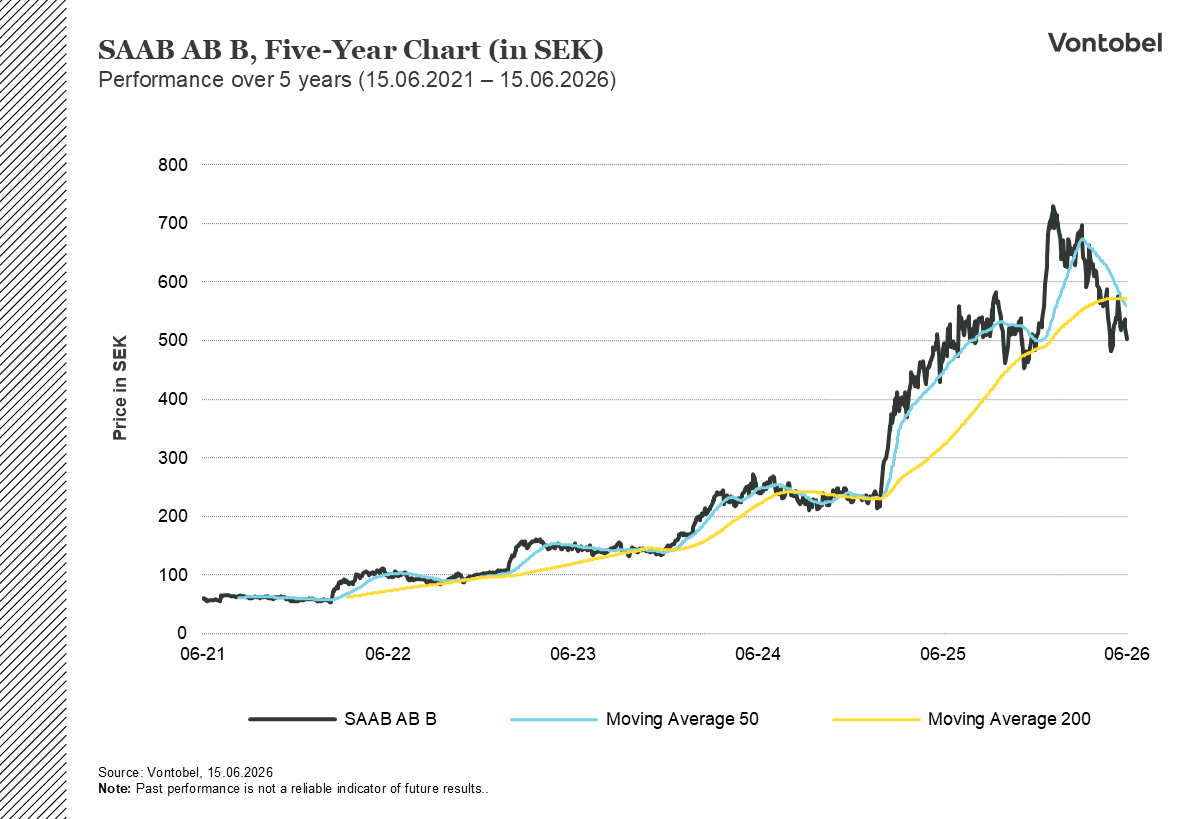

The same tension between order book and delivery runs through Sweden's Saab. At the end of the first quarter, the Swedish company had a backlog of orders worth 274 billion kronor, equivalent to about three and a half years of sales and spread across a large number of programs (Bloomberg Intelligence, 2026). These include Gripen fighters for Colombia and Thailand, GlobalEye surveillance aircraft for France, and submarines for Sweden with Poland likely to follow. Other orders include electronic warfare systems for Germany's Eurofighter fleet. Ukraine has expressed interest in 100 to 150 Gripen aircraft, and Saab is competing to supply Canada with up to 58 aircraft. Gripen output runs at about 15 aircraft per year. The planned increase to 25 or more aircraft per year will take years and billions of dollars in investments. New facilities will not be available for some time.

The ceasefire question

The obvious question for investors is what a ceasefire in Ukraine would mean. Defense shares have repeatedly fallen 4 to 6 percent in a day on nothing more than rumors of negotiations. An end to the war would, of course, be more welcome than a change in share price. However, the buildup does not depend on the war continuing. The Hague commitments, the German debt brake reform and the Nordic spending plans are based on the long-term assessment that Russia's posture would not change. Defense planners have also noted that a ceasefire would allow Moscow time to recover rather than provide a reason to hold back. Genuine peace would still weigh on these shares in the short term, but it would not alter the decade of contracted demand already sitting in the order books.

The coming months will reveal how much of the spending will materialize. July's quarterly results will show whether backlogs are converting into revenue on schedule. The NATO summit in Ankara in early July should reveal whether members are turning the 5 percent pledge into concrete national plans. Several large contracts remain undecided, Ukraine's Gripen order, Poland's submarine purchase, and Canada's fighter jet selection. These contracts will show whether new orders will replenish the book as quickly as deliveries accelerate. Europe's rearmament is a settled matter. The question is whether its industry can produce at the pace that its governments are now willing to pay for.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Product costs:

Product and possible financing costs reduce the value of the products.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.