Investors’ Outlook: Adjusting the focus

As we enter the home stretch of the first half of the year, it has become increasingly clear that the Iran war has blurred the upbeat economic baseline scenario the Multi Asset Boutique had projected for 2026. Higher oil prices are weighing on growth, lifting energy costs, fanning inflation, and eroding real wage growth, which could slow US consumer spending. As such, economic momentum may be at risk of losing steam in the next few months.

Blurrier picture

Still, the team doesn’t believe that higher oil prices alone are sufficient to tip the economy into recession. Several offsets are still in place. US tariff rates have likely peaked following the Supreme Court ruling, and tariff refunds have begun to flow through. Fiscal tailwinds are also on the horizon, with Germany yet to roll out much of its planned stimulus and Japan’s “Sanaenomics” agenda still in its early stages.

US inflation jumped in April at its fastest pace in three years, with price pressures spreading to services and food. The Eurozone also saw an uptick, as did Switzerland, where policymakers typically worry more about inflation being too low. Investors have hence scaled back expectations for monetary easing through 2026, and some central banks have indeed already either resumed rate hikes or are expected to do so in order to counter war-driven inflation. Markets now see roughly a 50 percent probability of a 25-basis-point rate hike by the Fed and around a 90 percent chance of a similar move by the European Central Bank (ECB) at its June meeting. The Fed, now under the leadership of Kevin Warsh, is likely to remain in wait-and-see mode longer than markets currently expect, as it has historically tended to react slowly to both overheating and slowing economic conditions.

Will AI byte off more than the economy can chew?

In February 2026, a research note published by Citrini Research sent a chill through global financial markets. The paper, described as a “thought exercise in financial history, from the future,” imagined a world in which artificial intelligence (AI) didn’t merely assist workers but hollowed out the economy itself.

The note outlined a hypothetical scenario in which companies replace white collar employees with AI in order to cut costs. Displaced professionals, now unemployed, reduce spending, denting business revenues. Firms then respond by doubling down on automation to protect their margins, triggering more layoffs. By 2028, Citrini envisioned, US unemployment would climb above 10 percent. Central to the paper was the idea of “ghost GDP”: economic output that appears in national accounts but never reaches the real economy because AI agents do not buy groceries, pay mortgages, or take vacations.

While the report drew criticism, not only for its lack of explicit macroeconomic modeling, but also for its failure to disclose potential conflicts of interest, it nevertheless struck a nerve. Shares of AI-vulnerable software, payments, and financial services companies came under heavy selling pressure.

Fear of technology-driven mass unemployment is everywhere

Skepticism toward technological innovation is nothing new. As early as the 1980s, Nobel Prize-winning economist Wassily Leontief warned, using the analogy of horses and mules, that advanced technologies such as automation could render human labor obsolete, much like tractors and automobiles displaced animals in agriculture and transportation.

AI is the latest, and perhaps most powerful, chapter in this debate, with many US consumers worried about becoming the mule of the AI boom. These concerns are echoed well beyond households. US Sena-tor Bernie Sanders, who identifies himself politically as a democratic socialist, has warned that AI and automation could replace nearly 100 million jobs over the next decade, citing particularly high exposure among fast food workers, accountants, and truck drivers.

Even prominent voices within the technology sector have sounded the alarm. Palantir Chief Executive Officer Alex Karp has repeatedly argued that AI will eliminate large numbers of white-collar jobs, especially among workers who lack scarce, highly technical skills, including many with generalist humanities backgrounds. If the US is not careful, he warned, this disruption could fuel hatred toward “rich people in tech.”

Mass unemployment: Fear vs. facts

How bad is the situation in the US labor market? At first glance, the data appear robust. The unemployment rate has trended downward, reaching a historically low 4.3 percent in April.8 Unemployment among younger workers (those aged 20 – 24 and often seen as particularly ex-posed to AI-driven disruption) has also declined, falling from 9.2 percent in October 2025 to “just” 7.6 percent in April 2026.

That said, layoffs have picked up in certain sectors—ironically, especially in tech. AI tools are increasingly automating or accelerating tasks such as basic coding, testing, and customer support, allowing firms to operate with fewer junior or support staff. However, we do not view AI as the sole driver behind these cuts. Many companies are also reducing payrolls to correct for pandemic-era overhiring or, in the case of tech companies, to free up capital for substantial investments in AI infrastructure.

The case against mass unemployment

While it is still too early to gauge AI’s full impact on labor markets, there is a credible case that large scale joblessness is not the most likely outcome. Why?

First, history suggests otherwise. A useful point of reference is the Industrial Revolution. In the late eighteenth and early nineteenth centuries, rapid technological advances disrupted traditional forms of employment, particularly in agriculture and artisanal manufacturing.

Handloom weavers lost their livelihoods to mechanized textile production, while rural workers were displaced by improvements in agricultural productivity. These changes generated insecurity, depressed wages for certain groups, and sparked episodes of social unrest. Yet there is little evidence that this period produced persistent, economy wide unemployment.

Over time, industrialization expanded labor demand. Factories, mines, transport networks, and urban services absorbed workers displaced from agriculture and traditional crafts, while population growth and rising investment supported further job creation. Rather than eliminating work, technology reallocated labor—first from agriculture to industry, and later into services.

The verdict is still out on which jobs will emerge in the long term, but if history is any guide, we might be up for some surprises. A paper by David Autor et al. suggests that 85 percent of job gains over the past 85 years have come from entirely new occupations, driven by techno-logical advancements and evolving consumer prefer-ences.9 Occupations emerging from technological innovation include airplane designers (1950), circuit layout designers (1990), AI specialists (2000), wind turbine technicians (2010), and cybersecurity analysts (2018). Those arising from changes in taste include acrobatic dancers (1940), tattoo artists (1950), mental health counselors (1970), hypnotherapists (1980), sommeliers (2010), and drama therapists (2018).

We may also want to keep in mind that AI faces political, adoption, and performance limits. On the political side, governments and regulators are moving more cautiously as concerns mount around data privacy, intellectual property, and accountability. Firms deploying AI face growing uncertainty about liability, particularly in sectors such as finance or healthcare, while geopolitical tensions are fragmenting access to critical inputs like advanced semi-conductors.

At the same time, the social dimension cannot be ignored. Public skepticism about AI is rising. According to a Quinnipiac University poll conducted in March 2026, 55 percent of Americans believe AI will do more harm than good in their day-to-day lives (up from 44 percent in April 2025). When asked how often they think they can trust information generated by AI, 76 percent of Americans say they can trust it either hardly ever (27 percent) or only some of the time (49 percent), while

21 percent believe it can be trusted most of the time (18 percent) or almost all of the time (3 percent). A striking 70 percent of Americans believe that advancements in AI are likely to reduce job opportunities, with Gen Z (those born between 1997 and 2008) the most concerned at 81 percent. Efforts to replace man with machine will likely eventually lead to stronger labor protection initiatives, even in countries not typically known for them, such as the US.

If we are to believe a Pew Research survey conducted in January 2026, the public may also be starting to push back against the pace of AI progress. Most Americans oppose large-scale AI infrastructure projects in their communities. Far more respondents view data centers as mostly harmful rather than beneficial for the environment (39 percent vs. 4 percent), home energy costs (38 per-cent vs. 6 percent), and nearby residents’ quality of life (30 percent vs. 6 percent).

Even where political barriers are manageable, AI adoption is uneven. Integrating AI into existing organizations is far more complex than simply deploying a new tool. Many firms are constrained by legacy IT systems, fragmented data, and a shortage of workers with the expertise needed to implement and manage AI solutions effectively. More fundamentally, adoption often requires a redesign of work-flows and decision-making processes, which takes time and carries execution risk. The economics are also not always straightforward: while AI promises efficiency gains, the upfront costs (in infrastructure, talent, and experimentation) can be substantial, and returns are often uncertain in the near term. As a result, AI may well be deployed only in specific pockets rather than across entire firms or industries.

In addition, there are still meaningful performance limitations. While AI can perform many tasks in isolation, it rarely matches humans on complete, end to end work as done in practice. AI systems remain prone to errors, particularly in complex or ambiguous tasks, and can produce confident but incorrect outputs. Current automation rates for full tasks remain low, even among the most advanced models.

The verdict is still out on which jobs will emerge in the long term, but if history is any guide, we might be up for some surprises. A paper by David Autor et al. suggests that 85 percent of job gains over the past 85 years have come from entirely new occupations, driven by techno-logical advancements and evolving consumer prefer-ences.9 Occupations emerging from technological innovation include airplane designers (1950), circuit layout designers (1990), AI specialists (2000), wind turbine technicians (2010), and cybersecurity analysts (2018). Those arising from changes in taste include acrobatic dancers (1940), tattoo artists (1950), mental health counselors (1970), hypnotherapists (1980), sommeliers (2010), and drama therapists (2018).

We may also want to keep in mind that AI faces political, adoption, and performance limits. On the political side, governments and regulators are moving more cautiously as concerns mount around data privacy, intellectual property, and accountability. Firms deploying AI face growing uncertainty about liability, particularly in sectors such as finance or healthcare, while geopolitical tensions are fragmenting access to critical inputs like advanced semi-conductors.

At the same time, the social dimension cannot be ignored. Public skepticism about AI is rising. According to a Quinnipiac University poll conducted in March 2026, 55 percent of Americans believe AI will do more harm than good in their day-to-day lives (up from 44 percent in April 2025). When asked how often they think they can trust information generated by AI, 76 percent of Americans say they can trust it either hardly ever (27 percent) or only some of the time (49 percent), while

21 percent believe it can be trusted most of the time (18 percent) or almost all of the time (3 percent). A striking 70 percent of Americans believe that advancements in AI are likely to reduce job opportunities, with Gen Z (those born between 1997 and 2008) the most concerned at 81 percent. Efforts to replace man with machine will likely eventually lead to stronger labor protection initiatives, even in countries not typically known for them, such as the US.

If we are to believe a Pew Research survey conducted in January 2026, the public may also be starting to push back against the pace of AI progress. Most Americans oppose large-scale AI infrastructure projects in their communities. Far more respondents view data centers as mostly harmful rather than beneficial for the environment (39 percent vs. 4 percent), home energy costs (38 per-cent vs. 6 percent), and nearby residents’ quality of life (30 percent vs. 6 percent).

Even where political barriers are manageable, AI adoption is uneven. Integrating AI into existing organizations is far more complex than simply deploying a new tool. Many firms are constrained by legacy IT systems, fragmented data, and a shortage of workers with the expertise needed to implement and manage AI solutions effectively. More fundamentally, adoption often requires a redesign of work-flows and decision-making processes, which takes time and carries execution risk. The economics are also not always straightforward: while AI promises efficiency gains, the upfront costs (in infrastructure, talent, and experimentation) can be substantial, and returns are often uncertain in the near term. As a result, AI may well be deployed only in specific pockets rather than across entire firms or industries.

In addition, there are still meaningful performance limitations. While AI can perform many tasks in isolation, it rarely matches humans on complete, end to end work as done in practice. AI systems remain prone to errors, particularly in complex or ambiguous tasks, and can produce confident but incorrect outputs. Current automation rates for full tasks remain low, even among the most advanced models.

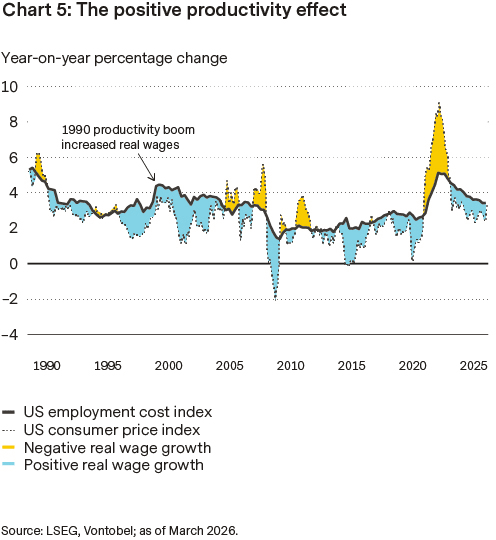

Another reason why mass unemployment is unlikely lies in how companies respond to technology. Firms adopt AI primarily to raise efficiency, manage costs, and scale output, not to eliminate labor indiscriminately. Higher productivity often leads to lower prices for goods and services, which can raise real (i.e., inflation-adjusted) incomes and boost consumption. This pattern was evident during the productivity boom of the 1990s.

There will still be losers

That said, AI may deepen an existing trend: the decoupling of profit growth from employment growth. Over the past decade, corporate profits have risen much faster than payrolls, reflecting capital light business models, automation, and greater scalability. AI could amplify this trend, allowing firms to grow revenues without com-mensurate increases in headcount. These dynamic feeds understandable concerns that the gains from AI will accrue disproportionately to capital owners and highly skilled workers, while others face stagnant wages or declining job security.

Data provided by Goldman Sachs shows that it can take technology displaced workers up to one month longer to find a new job, while their inflation-adjusted earnings also tend to take larger hits (more than 3 percent) compared with other workers (for whom the effect is negligible). A decade after a job loss, technology displaced workers’ real earnings are about 10 percentage points below those of non-displaced workers. They also experience slower wealth accumulation, as well as delayed homeownership and household formation. The risk, therefore, is not so much mass unemployment as mass insecurity and polarization.

At the end of the day, it might all come down to the pace of adjustment. Technological revolutions create strain not because work disappears overnight, but because skills, institutions, and education systems adapt more slowly than technology itself. Workers displaced from shrinking roles may struggle to transition quickly into growing ones, particularly without retraining or geographic mobility. If policy responses lag, whether in education, social safety nets, or labor market flexibility, the social costs can become significant even in the absence of high headline unemployment.

To end on a positive note …

There are good reasons to think that techno-logical change is ultimately more creative than destructive. To return to Wassily Leontief: he not only feared that humans might follow the fate of horses and mules, but also struggled to envision a world in which new jobs would emerge at scale. As he put it, “Think what would happen if all unemployed steel and auto workers were re-trained to operate computers… There aren’t enough computers to go around. We’d have created a worse problem.”

In hindsight, it is clear how much this view underestimated both technological progress and society’s capacity to adapt. Not only were there enough computers to go around, but we built entire industries, economies, and ways of life around them. Today, most of us are, quite literally, sitting in front of them.

(G)rate expectations?

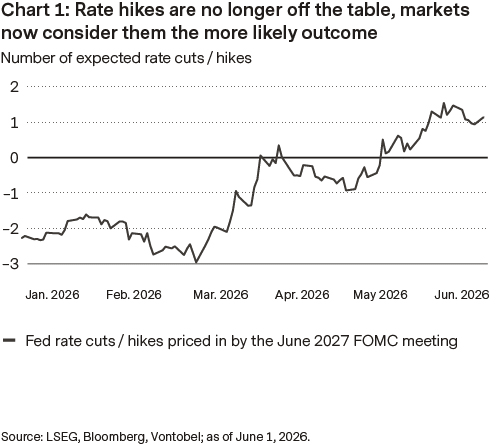

Markets have started to question whether central banks are actually restrictive enough in a world of recurring supply shocks and geopolitical inflation pressure.

The market narrative has changed quite a bit. What had looked like a fairly straightforward path toward lower inflation and Fed rate cuts has become much less clear as the war in Iran pushes energy prices and inflation expectations higher again.

Investors are increasingly focused on inflation drivers that central banks have limited control over. Higher oil prices, shipping disruptions, and broader supply-side pressures are seeping into transportation, production, and eventually consumer prices. Inflation swaps briefly moved close to pricing in 4 % headline inflation, exposing growing concern that these pressures could spread more broadly through the economy.

This has directly impacted rate expectations. Markets have repriced the outlook for the Fed’s monetary policy, with investors having moved on from debating when cuts may come to whether current policy is restrictive enough at all. Treasury options markets show strong demand for protection against higher yields, reflecting concerns around structurally higher inflation, large deficits, and rising sovereign issuance. Still, current yields increasingly appear closer to the upper end of the pricing range, especially since oil shocks tend to weigh on growth over time.

As for credit markets, which still benefit from strong demand, spreads remain tight against a macroeconomic backdrop that has become more uncertain. Higher rates, elevated volatility, and geopolitical uncertainty are starting to challenge a market that had previously been supported by strong growth and abundant liquidity.

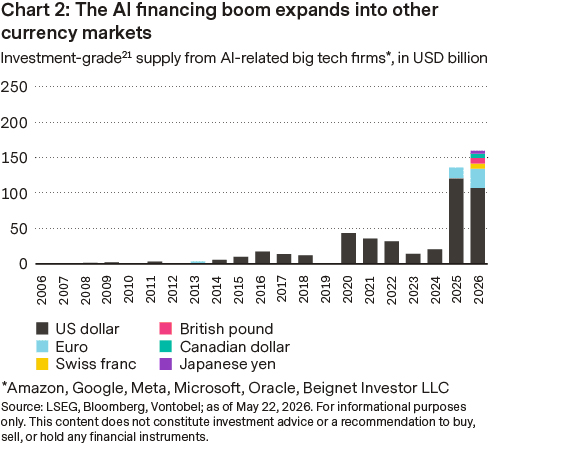

One major driver is the surge in AI-related bond issuance. Financing needs tied to AI infrastructure are adding substantial duration supply at a time when sovereign borrowing is already historically high, contributing to upward pressure on long-end yields. Spreads remain unusually tight relative to current volatility levels, despite tighter financial conditions and rising refinancing risks. Carry may still look appealing at first glance, but more of it now comes from the risk-free component rather than from credit spreads themselves. In other words, investors are being compensated more for duration than for taking spread risk, leaving valuations vulnerable if volatility stays high or growth slows further.

Selective exposure

Equity markets advanced across the major regions in May, although the nature of those returns merits closer attention.

The first-quarter reporting season ranked among the strongest of the past two decades in the US, lifting earnings-per-share (EPS) growth forecasts and boosting earnings momentum.

The engine powering that trend is still AI-related capital expenditure (capex), which continues to translate into tangible revenue and margin gains for the companies at the heart of the cycle. The broader read-through has been encouraging: order books, guidance and capex commitments all point to a cycle with further room to run.

However, the foundations of the stock rally stayed conspicuously narrow. Performance was concentrated in a small group of large-cap technology names, semiconductors above all. And this is a pattern that’s now spreading outside the US as well. That same leadership has done much of the heavy-lifting to help offset a less favor-able inflation backdrop, as energy prices run hot amid the unresolved stalemate in the Middle East. Narrow market breadth may boost index returns, but it also leaves markets more sensitive to any stumble at the top, a risk worth monitoring.

So, what has been priced into equity markets? Despite the rebound since the end of March, valuations don’t appear to be stretched across the board, particularly in the US and even less so in emerging markets. This is evident in for-ward P/E multiples16 relative to 2026 – 2027 earnings growth expectations. That combination likely leaves room for further upside should global growth remain on track.

What comes after the supply shock?

Energy supply shocks, by definition, capture headlines. For investors, the more important question is what happens after the headlines fade.

Historically the engine of global demand growth, Asia is now leading the market’s contraction as high prices and supply anxieties force adjustments. This is manifesting not just in industrial slowdowns, but also in daily life: Paki-stan, the Philippines, and Sri Lanka have introduced four-day work weeks to reduce commuting and conserve fuel. Beyond immediate conservation measures, the supply shock may be accelerating a push toward renewable energy across the region. Security of supply has become synonymous with domestic transition. South Korean Pres-ident Lee Jae Myung recently warned, “Our future will be at serious risk if we continue to rely on fossil fuels.”

While demand cools, non-Gulf producers are trying to help on the supply side. US producers pushed output close to 14 million barrels this spring. Interestingly, these increases are driven more by operational efficiency improvements of existing facilities than by an increase in new drilling. Burned by past boom-and-bust cycles, producers seem to weigh political pressure to “drill, baby, drill” against Wall Street expectations for capital discipline, debt repayment, and shareholder returns.

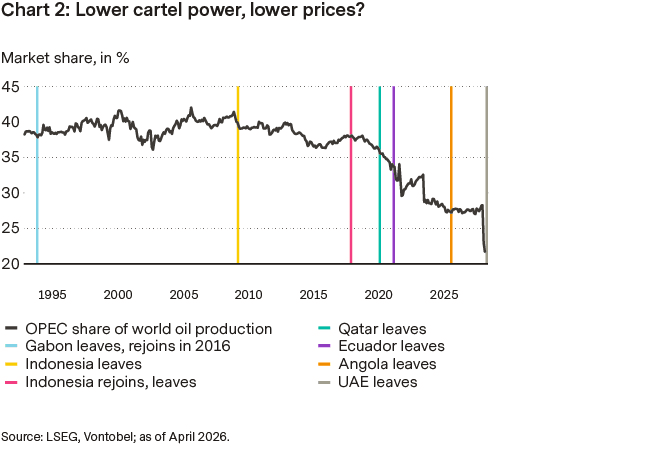

Further down the road, oil prices may also be driven by the fraying cohesion within the OPEC.18 At the start of May, the United Arab Emirates (UAE) formally ended its nearly 60-year membership, leaving both OPEC and the wider OPEC+ alliance. The reason may be due to tensions between the UAE and Saudi Arabia. The UAE has spent over USD 150 billion to expand production capacity toward 5 million barrels per day. Its leadership seems increasingly frustrated by restrictive Saudi-driven quotas that left costly infrastructure sitting idle while Abu Dhabi sought to monetize its resources ahead of the global energy transition.

OPEC has a long history of member departures, including recent exits like Angola and earlier ones by Qatar and Ecuador. However, the UAE’s withdrawal is different. Those countries represented marginal production with limited ability to sway global prices. But the UAE was its third-largest producer, which now removes some 13 percent of the cartel’s output and a massive chunk of its global spare capacity buffer. That leaves Saudi Arabia to carry a heavier economic burden, making future production cuts more expensive and less effective for the country. As Abu Dhabi prepares to bring its sidelined capacity to market, the structural floor under long-term oil prices looks increasingly fragile to us.

Shelter over structure?

Currency markets are increasingly reacting to developments around higher oil prices, geopolitical uncertainty, and evolving growth expectations, temporarily pushing longer-term structural themes into the background.

The dollar has been a key beneficiary of this environment. Safe-haven demand, higher US yields, and the relative resilience of the US economy as a net energy exporter have all supported the currency. Relative growth dynamics also continue to favor the US in the near term, particularly compared to more energy-sensitive economies such as the euro area.

Concerns around rising US debt levels, fiscal deficits, and the long-term US policy outlook have not disappeared, but they’re not what markets are trading right now. The setup therefore remains highly binary. If tensions continue and oil prices remain high, the dollar could continue to hold up well. But if geopolitical risks ease more decisively, markets may quickly return to a more bearish medium-term view on the currency.

Elsewhere, the euro has remained more resilient than expected despite higher oil prices and weaker risk sentiment, which suggests investor positioning had already become relatively cautious and that the euro doesn’t need a perfect environment to stabilize.

Still, Europe is more exposed to the inflationary impact of higher energy prices than the US. Prolonged oil strength would likely push inflation higher and weigh on growth, even if expectations for the region have so far remained relatively resilient and have not yet materially deteriorated. That suggests markets still believe Europe can absorb part of the shock, especially if energy prices stabilize and geopolitical tensions ease. A more durable recovery in the euro would nevertheless benefit from lower energy prices and stronger relative growth dynamics over time.

The Swiss franc is widely viewed as one of the clearest defensive currencies among the G10. Safe-haven demand, low inflation, strong external balances, and Switzerland’s relatively stable macro backdrop continue to support the franc structurally. While the Swiss National Bank may try to slow excessive appreciation in the near term via intervention or verbal pushback, the broader environment may continue to favor structurally stronger currencies such as the franc, Norwegian krone, and Swedish krona over time.