The Swedish krona shifts from strength to weakness

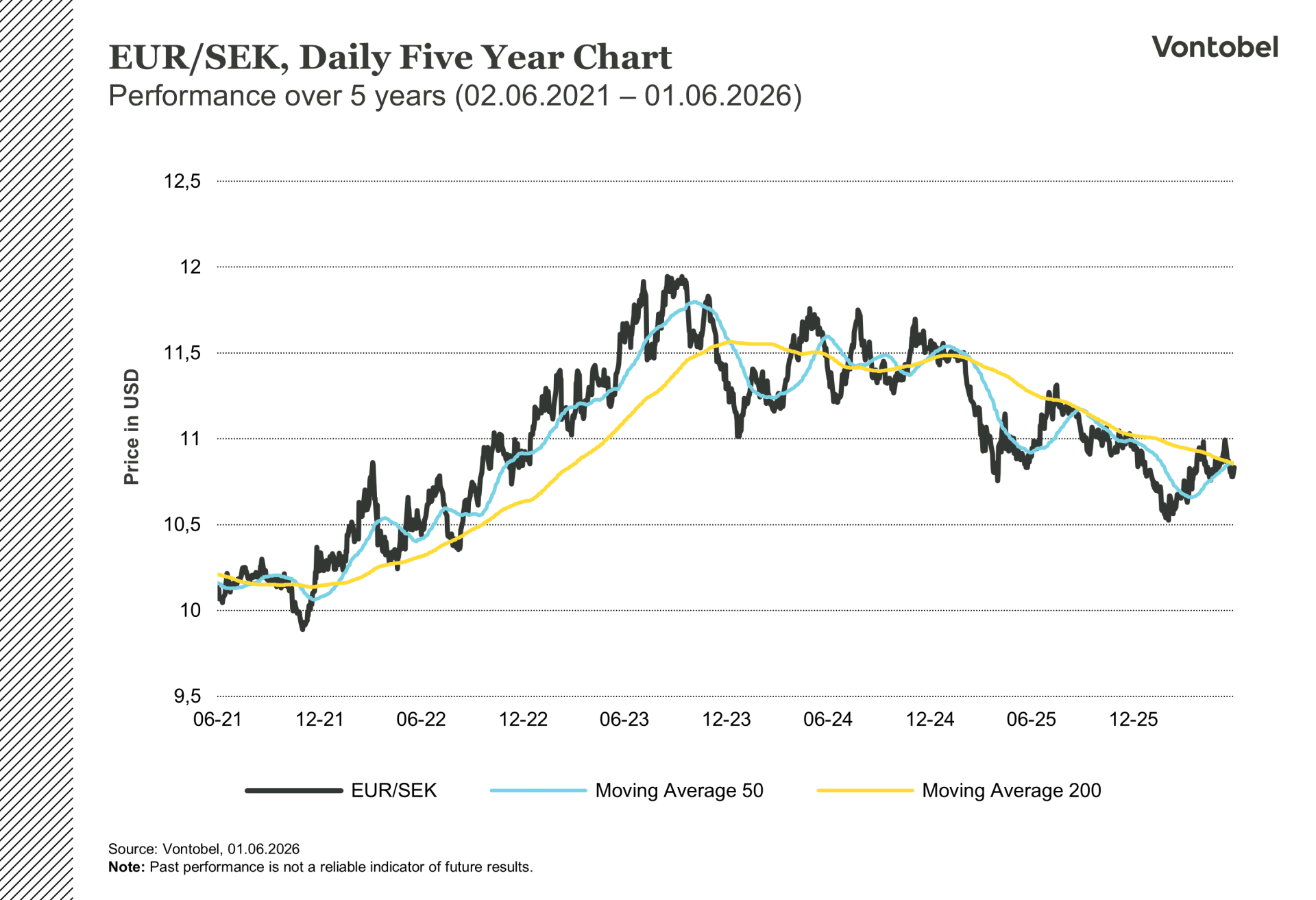

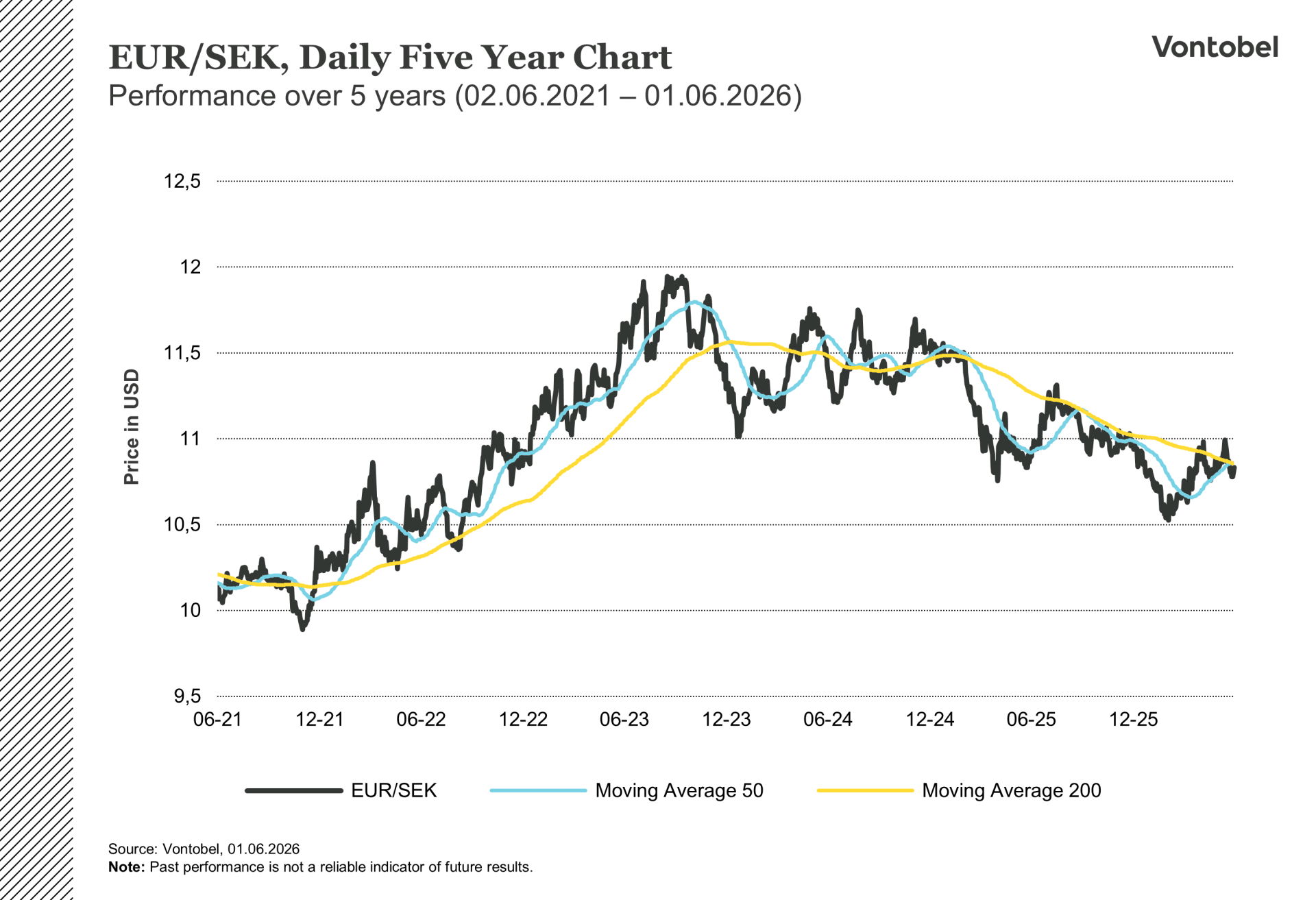

In 2025, the Swedish krona was the best-performing G10 currency, gaining almost 17% against the dollar. However, in 2026, it was the worst performer. Since January it has weakened against all other G10 currencies, with EUR/SEK exchange rate rising from below 10.55 to around 10.85 and the USD/SEK exchange rate rising from around 8.80 to 9.35. In early May, the Norwegian krone climbed above parity with the Swedish krona for the first time since 2018, having gained almost 11% against it in five months (Bloomberg). This weakness has little to do with the Swedish economy itself. In fact, Sweden is growing faster than any other economy in the G10 economy, has the lowest inflation in the EU, and surpluses in both its public finances and current account. The explanation lies in interest rates and energy prices.

Funding currency

At 1.75%, the Riksbank's policy rate is the lowest in the G10 except in Switzerland. This posed little problem while other central banks were cutting alongside it, but the landscape has shifted. The ECB is expected to raise rates on June 11, Norges Bank raised its rate to 4.25% on May 7, and the Reserve Bank of Australia has tightened several times this year. As these gaps have widened, the krona has become a preferred funding currency for carry trades, in which investors borrow cheaply in kronor and invest the money in higher-yielding currencies to earn the interest rate spread.

This ranking has remained consistent throughout the year. The strongest currencies belong to the central banks that have raised rates, while the krona, with benign inflation and little pressure to tighten, sits at the bottom. Strong GDP growth, solid retail sales, and rising household lending have failed to support the krona, because the dominant flow is rate-driven selling by international funds rather than a response to Swedish fundamentals.

The Riksbank's bind

Raising rates to close the gap is the obvious response, but Swedish inflation is far too low to justify it. April CPIF was 0.8%, core inflation excluding energy fell to 0.0%, and headline CPI turned negative for the first time since 2020 (SCB).

Board member Per Jansson argued in a recent speech that the current situation is fundamentally different from the 2021 to 2023 inflation episode. Demand is weaker than it was then, policy rates are already higher across most countries, and few indicators point to a meaningful inflation upturn. "I still have not given up hope that the impact might be relatively limited, especially here in Sweden," Jansson said of the Middle East conflict.

This reasoning explains why the Riksbank's held rates at 1.75% on May 7, marking its fifth consecutive hold. The statement left room for interest rate hikes should the war produce "a broad and persistent upturn in inflation," but the threshold is high (Riksbank). If the ECB were to act on June 11 while the Riksbank stays put, the rate gap would widen the rate gap to minus 50 basis points and add further carry pressure on the krona. The first Swedish rate hike is not expected before September, and even that depends on how energy prices develop over the summer.

Related Products

EUR/SEK Daily One Year Chart

EUR/SEK Daily Five Year Chart

The Norwegian mirror

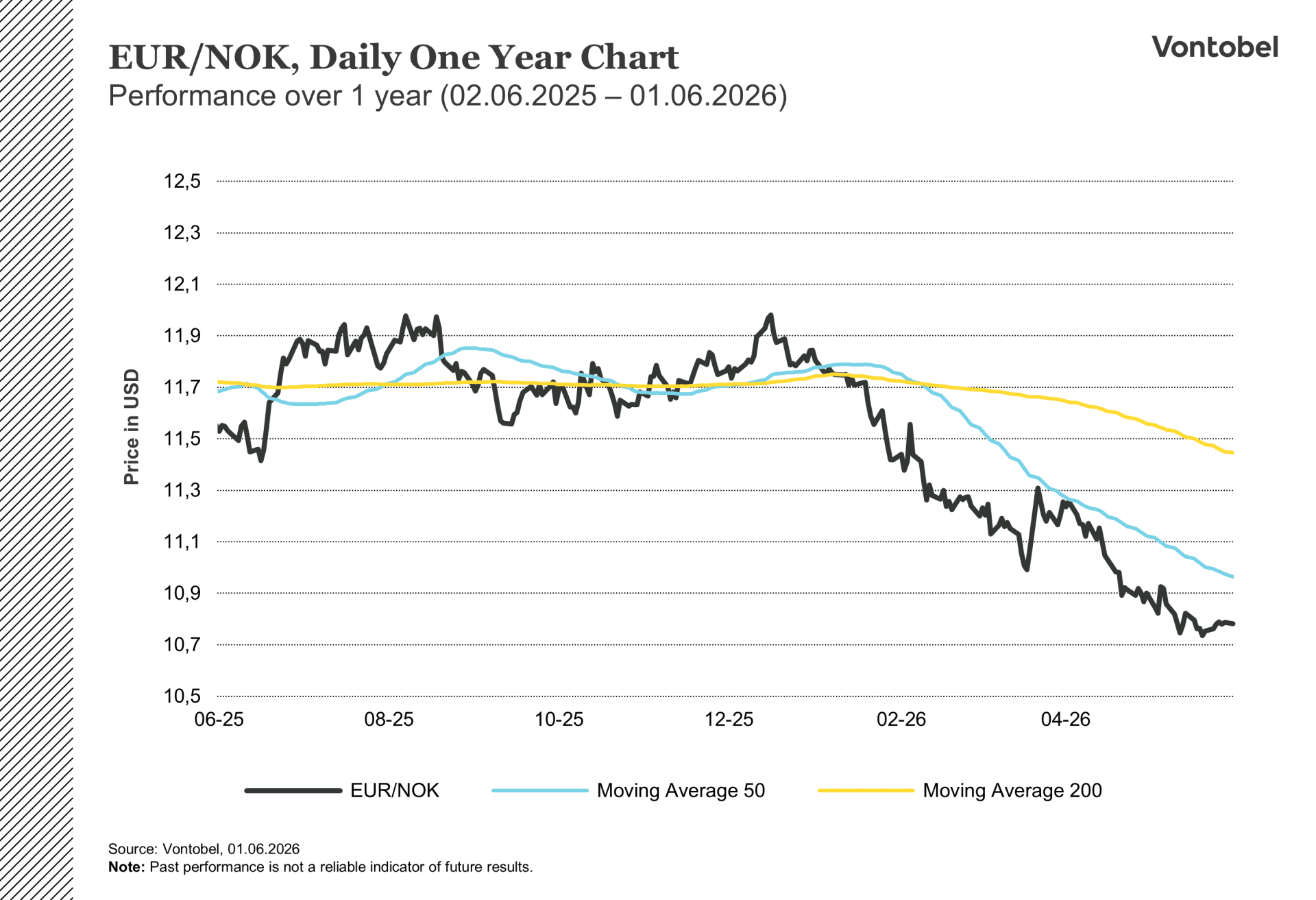

Norway presents the opposite picture, which is why the krone has moved so sharply in the opposite direction. On May 7, Norges Bank raised its policy rate by 25 basis points to 4.25% surprising most forecasters. Governor Ida Wolden Bache cited inflation running above target for several years and wage growth of 4.4% in the latest round (Norges Bank). Norges Bank's quarterly expectations survey, published later in May, showed Norwegian consumers expect inflation to reach 4.4% and wage growth of 4.5% over the next twelve months, both of which are well above the 2% target. This is consistent with a tightening cycle that may not yet be over (Norges Bank).

As the largest oil and gas exporter in Western Europe, Norway directly benefits from the elevated energy prices that burden net importers like Sweden and the Eurozone. With Brent crude at around $99 per barrel, roughly 40% above pre-war levels, export revenues remain strong, supporting a current account surplus of around 14% of GDP and a sovereign wealth fund worth approximately $2 trillion (Bloomberg). This surplus, combined with a 250 basis point rate advantage over Sweden, provides unusually firm support for the krone. Swap markets are pricing at least one further Norges Bank hike before year-end.

The near-term case for the krone is strong, but this should not be extrapolated too far. Danske Bank, among others, points to a building stagflation risk: the forces lifting the currency are beginning to weigh on the economy. Leading growth indicators have fallen to their lowest level since the pandemic, while high wage settlements and elevated business costs keep inflation sticky. Weak growth alongside persistent inflation is the textbook definition of stagflation, and it is a difficult environment for any central bank to navigate. Higher interest rates are currently supporting the krone now, but should they slow the economy further while oil prices eventually retreat, the currency would lose its principal support just as growth deteriorates.

Related Products

EUR/NOK Daily One Year Chart

EUR/NOK Daily Five Year Chart

The euro and the dollar

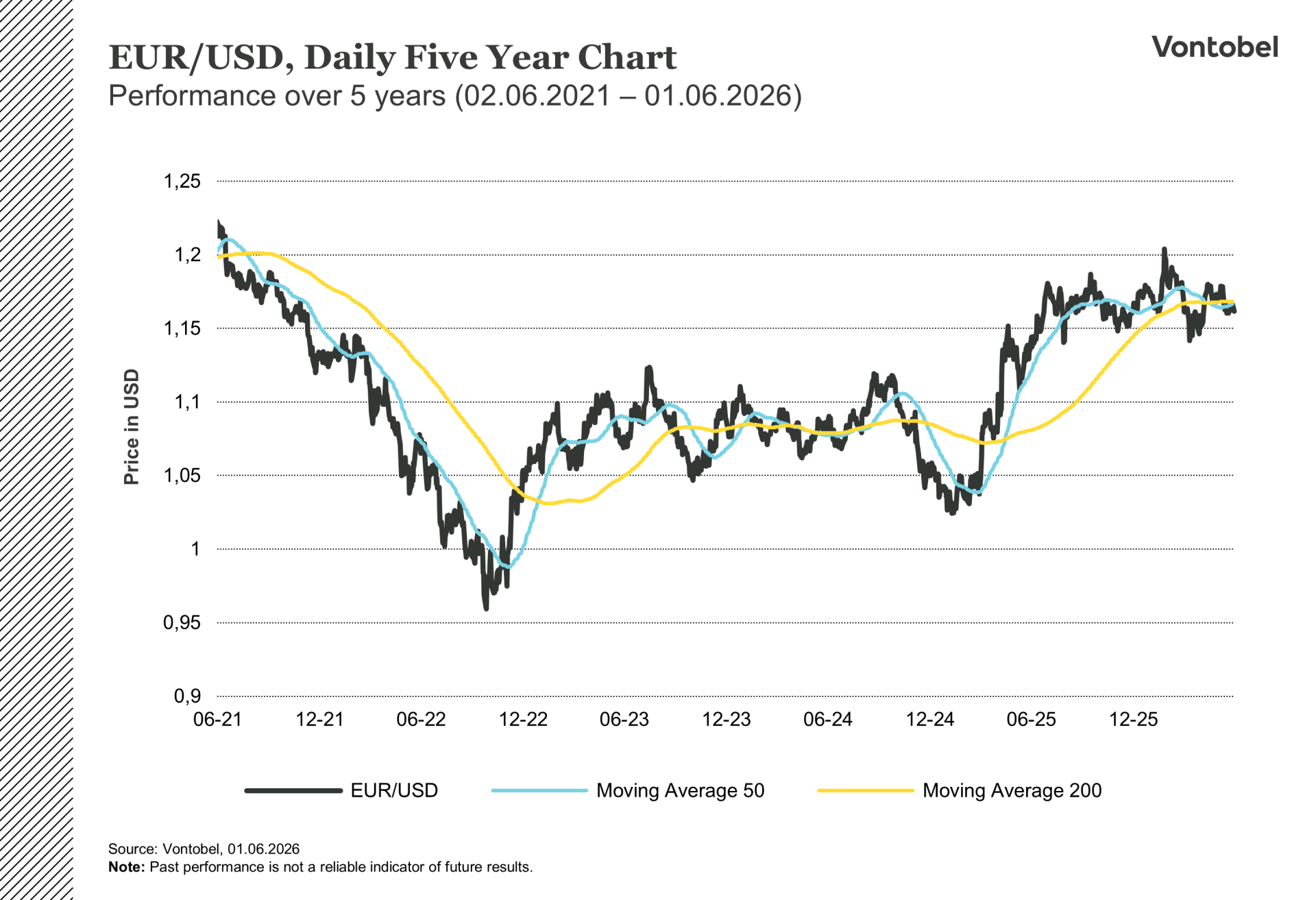

The EUR/USD outlook has shifted in recent weeks. At the start of the year, the consensus expected the euro to grind toward $1.20 or higher, supported by improving eurozone data and a dovish Fed. A prolonged Iran war has undermined that view, hitting the eurozone, a net energy importer, harder than the United States. Eurozone growth expectations for 2026 have been cut to around 0.8%, against roughly 2.2% for the US, according to consensus forecasts compiled by Bloomberg.

While the ECB is still expected to raise interest rates in June, this move is largely priced in. A second increase in July depends on the path of energy prices and whether second-round inflation effects emerge. The US picture is shifting as well. Stronger-than-expected inflation data in May has prompted the market to reprice Fed expectations, with some forecasters now anticipating rate hikes rather than cuts as the next move under Kevin Warsh. That would reverse the rate convergence that supported the euro earlier in the year.

The outcome is more uncertain than the start-of-year consensus implied. Resolving the Iran conflict to lower oil prices would revive the case for EUR/USD above $1.20. A prolonged war with persistently high energy costs and a hawkish Fed pivot could push the pair toward $1.15 or below. For now it trades around $1.16, balanced between those two outcomes.

EUR/USD Daily One Year Chart

EUR/USD Daily Five Year Chart

Related Products

Looking ahead

The decisive dates are close together: the ECB on June 11, the Riksbank on June 17, and Norges Bank on June 18. If the ECB hikes and the Riksbank holds, EUR/SEK could push toward 11.00. A number of analysts regard that level as closer to fair value than it appears, once account is taken of the steady outflow from Swedish savers and pension funds buying foreign assets, a structural drag that conventional valuation models understate.

The krona remains the G10 currency most exposed to events in the Middle East, and a credible ceasefire would support it quickly stabilize markets and lower energy prices. The benefit would be smaller than for some peers, however. With almost no Riksbank hikes priced in, a peace deal would leave little to unwind on the Swedish rate side. The krona would benefit from improved sentiment and cheaper oil, rather from any change in the Riksbank’s expected path.

Sweden's economy continues to deliver solid figures. However, its currency continues to move in the opposite direction. Until either the interest rate outlook or the geopolitical backdrop changes, this divergence is unlikely to close.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.