SKANSKA: Currency overshadows stronger report

Skanska is one of the world’s largest construction and property development companies, operating across the Nordics, Central Europe, and the United States. With around 26,000 employees and an order backlog, meaning the total value of work already contracted but not yet built, at a record-high 267 billion kronor, this is not a company fighting for survival. It is, however, a company trying to convince the market that its profitability targets are achievable. It is precisely this tension that makes this Q1 2026 report interesting.

Skanska Looks Weak, but Currency Is the Main Reason

The most important takeaway from this report is that Skanska’s construction business is actually performing well. Currency is what makes it look weaker than it really is. Revenue fell 10 percent compared with the same quarter last year, which sounds alarming. However, if you strip out the effect of a much weaker US dollar and other currency moves, the decline was only 1 percent. Operating profit, i.e. the money left after paying the costs of running the business, grew by 18 percent in local currencies. That is a meaningful difference, and many casual readers will miss it completely.

Related Products

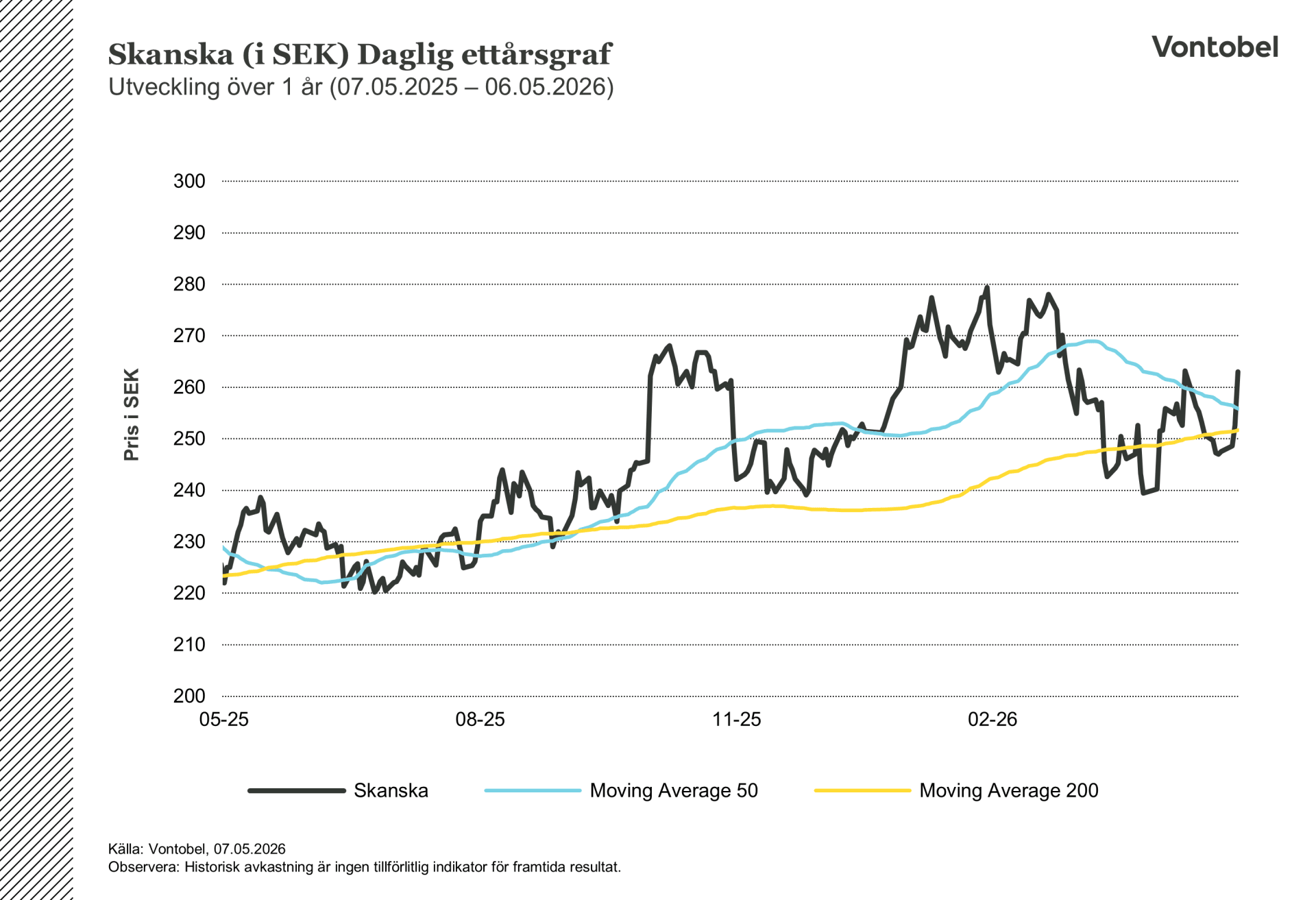

Skanska (in SEK) Daily one-year chart

Skanska (in SEK) Daily five-year graph

Key figures illustrating the context and what they actually mean

The construction margin, which is operating profit as a share of revenue and shows how much of every krona earned turns into profit, came in at 3.0 percent for the quarter, up from 2.8 percent a year ago. On a rolling 12-month basis, it stands at 4.2 percent, just above Skanska’s own target of at least 4 percent. This target has historically been difficult to achieve, so surpassing it is significant. Earnings per share were 2.42 kronor, essentially unchanged from 2.40 last year. Not exciting, but stable.

The order backlog increased to 267.5 billion kronor, equal to 19 months of production, which is genuinely good news. It means Skanska has work secured well into 2027, with strong demand from data centers and semiconductor facilities continuing to support the US pipeline. The company booked 6.9 billion kronor in tech-related construction orders in the quarter alone.

The numbers still look uncomfortable in project development. Return on capital employed, which measures how efficiently the company generates profit from the capital tied up in its property development business, came in at just 2.1 percent against a stated target of 10 percent or more. This significant discrepancy has persisted for several quarters. Commercial property in the US in particular is dragging the whole segment down.

The cash flow number looks like a crisis. It isn’t.

At first glance, an operating cash flow of minus 1.3 billion kronor seems like a serious problem, and it is more than five times worse than in the same quarter last year. However, closer inspection reveals that the main cause is a significant land acquisition in Stockholm, where Skanska bought land in a prime location near St. Erik’s Eye Hospital for future residential and office development. Land purchases are capital outlays, meaning money spent today on assets that are expected to generate future returns, and this is very different from cash disappearing into a loss.

Furthermore, Skanska already has 5.4 billion kronor of sold but not yet handed-over commercial properties in the pipeline, of which 4.7 billion is expected to affect cash flow before year-end. The underlying liquidity position, meaning the total cash and credit available to the company, stands at a comfortable 27.7 billion kronor.

A sector that is nowhere near uniform

The construction market is broadly holding up, but the details are uneven. Skanska’s Nordic residential development business is still struggling with a continued slump in demand for new housing across Sweden and Norway, with low sales volumes, weak pricing, and projects carrying narrow profit margins. Central Europe, especially Poland and the Czech Republic, looks very different, with growing economies, lower interest rates, and strong demand for new homes.

Meanwhile, the commercial real estate transaction market in the Nordics and Central Europe is recovering gradually, while the US market remains subdued. Skanska is dealing with all of these conditions at the same time, which makes the overall result harder to read than it would be for a more specialized competitor.

Two things that will determine what happens next

The first thing to watch is whether the expected commercial property sales for the rest of 2026 actually close on schedule. The expected cash inflows of 4.7 billion kronor are significant, and any delay would put pressure on both cash flow and the market’s confidence in management’s guidance.

Secondly, it is important to see how Skanska handles the ongoing gap between its return targets and actual performance in project development. The construction division is now meeting its margin target, which represents real progress. However, as long as the development side earns 2 percent on capital while targeting 10 percent, the overall investment case remains more of a story of potential than delivery. Closing that gap in a more structural way, not just quarter by quarter, is what would really change the narrative.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.