Copper: the market that divides analysts

In early May, copper was trading at around $13,000 per ton, close to record highs, despite growing signs of a global economic slowdown. Mine disruptions, a sulfuric acid shortage and record demand from AI data centers and electric vehicles have created a situation where the major investment banks cannot agree on whether the market is in surplus or deficit.

The metal that became strategic

Both Washington and Beijing now treat copper as a matter of national security. The US is investigating whether the metal should be subject to security tariffs through Section 232, while China has introduced a framework giving the state greater control over the country's copper flows. What they both recognize is that copper is a critical component in virtually every investment the Western world is prioritizing.

The scale of the new demand is hard to overstate. A single large-scale AI data center requires up to 50,000 tonnes of copper, and grid and power infrastructure is expected to account for around 60 percent of copper demand growth over the coming decade (Goldman Sachs, 12.2025). The electrification of transportation complicates matters further: an electric car contains three and a half times more copper than a conventional vehicle, and wind and solar power require several times more copper per megawatt than fossil fuel plants. In total, global copper demand is expected to increase by about 50 percent by 2040, rising from 28 to 42 million tons per year (S&P Global, 01.2026).

In the meantime, the US has already started to take action. American players have been stockpiling copper ahead of potential tariffs and Comex inventories have hit record after record. This is tightening availability in the rest of the world, even when total global inventory appears high.

Related Products

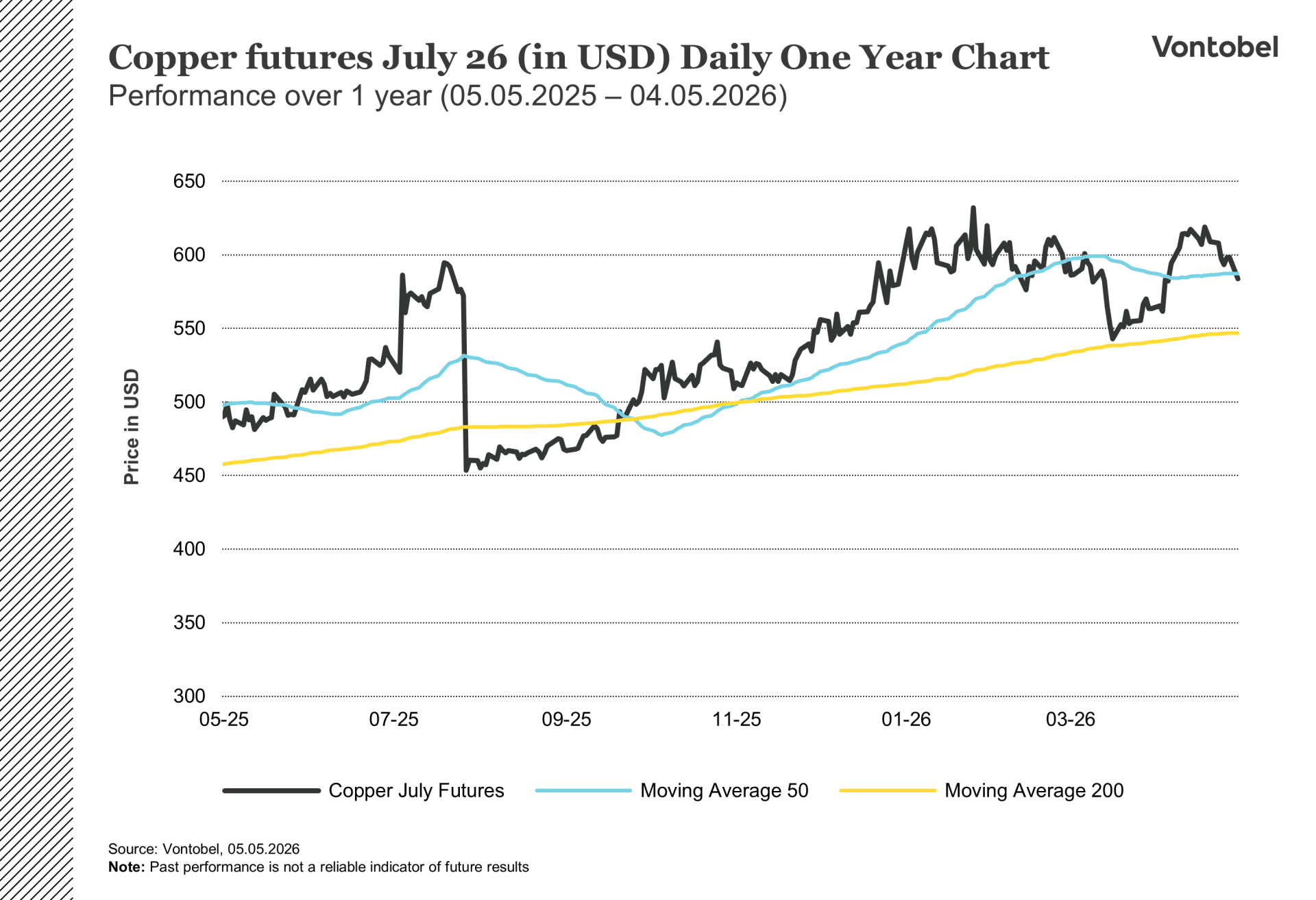

Copper Futures (Jul 2026, USD) One-Year Daily Chart

Copper Futures (Jul 2026, USD) Five-Year Daily Chart

Supply falling behind

It takes an average of 17 years to bring a copper mine from exploration to production, so supply is falling behind Global mine output is expected to peak at around 27 million tons in 2030 before falling back to 22 million tons by 2040, below current levels (S&P Global, 01.2026).

Nowhere is the strain more visible than in the concentrate market. When Antofagasta and China's Jiangxi Copper negotiated their annual copper smelting fee for 2026, they agreed to a fee of zero dollars per ton, the lowest level on record (Kitco, 12.2025.) Normally, mining companies pay smelters to process their ore. However, in March the relationship was reversed: the spot fee stood at minus $70 per ton, meaning smelters are paying mines for access to raw materials (S&P Global, 04.2026). The reason for this is that over the past three years, China has expanded its smelting capacity far faster than mine production has grown. There is simply not enough ore.

Over the past eighteen months, three of the world's most important copper mines have experienced significant disruptions. At Grasberg in Indonesia, force majeure has been in effect since September 2025 and production is expected to be one third lower in 2026 than planned. At Kamoa-Kakula in the Democratic Republic of Congo (DRC), an earthquake halved production in the first quarter. At Codelco's El Teniente mine in Chile, operations were suspended following a tunnel collapse. The market expects mine production to grow by nearly 3 percent in 2026, but that figure may be too optimistic. A more conservative estimate predicts growth of no more than 1 percent at most (Bloomberg, 01.2026).

A review of 27 mining projects worldwide also shows that new mines require a copper price of at least $10,000 per ton to be viable (Bloomberg, 01.2026). If the price falls below that level, investment dries up and future supply shrinks further.

In addition to mine disruptions, the conflict around the Strait of Hormuz has created a parallel crisis. Roughly half of all seaborne sulfur previously passed through the strait. Now that it is effectively closed, sulfuric acid prices have surged, and China has announced it will halt sulfuric acid exports in May 2026. This directly affects copper production. The so-called SX-EW method, an extraction process that requires sulfuric acid, accounts for around 17 percent of global copper output (Goldman Sachs, 04.2026). Chile, the world's largest copper producer, imports more than one million tons of sulfuric acid from China each year, and the country's copper output fell to a nine-year low in February.

Oil threatening the equation

The same geopolitical crisis choking copper supply also threatens to dampen demand. The Iran conflict has pushed oil prices above $100 per barrel. If Brent remains around $110 for the rest of the year, copper demand growth could fall by an estimated 1.4 percentage points (J.P. Morgan, 04.2026). In a market close to balance, that could be the difference between deficit and surplus.

China accounts for around 60 percent of global copper consumption, and the signals are mixed. Fabricators' operating rates have fallen to around 50 percent, the lowest since the 2020 pandemic (Bloomberg, 04.2026). Imports of refined copper have dropped significantly so far this year. At the same time, prices around $13,000 per ton are starting to incentivize substitution with cheaper aluminum, a shift that has historically accelerated once the price gap between the two metals widens sufficiently. Global inventory levels stand near 1.4 million tons, but much of the build-up reflects American stockpiling ahead of tariffs rather than actual overproduction (J.P. Morgan, 04.2026).

Analysts disagree more than usual. Goldman Sachs sees a surplus and an average price of around $10,700 per ton (Goldman Sachs, 12.2025). Citigroup expects $13,000 as early as the second quarter (Citigroup, 04.2026.) Over the longer term, however, there is broader agreement: Goldman sees $15,000 per tonne by 2035, a view supported by the fact that new mining projects need at least $10,000 per tonne to be viable.

What it means for copper going forward

The copper market in 2026 is defined by an unusual tension. Long-term structural demand driven by electrification, AI and renewable energy sits alongside supply constrained by decades of underinvestment, mine disruptions and an unprecedented sulfuric acid crisis. Working against that are macroeconomic headwinds in the form of high oil prices, weaker Chinese industrial activity and increasing substitution. The disagreement among analysts reflects that uncertainty, but on one point there is consensus: the long-term direction points toward a structural deficit and higher prices. The question is whether the path ahead runs through further volatility or a more gradual transition.

Boliden at the center

Boliden is the Nordic region's largest copper producer and one of few European players with integrated operations from mine to smelter. The company is investing SEK 4.8 billion in a new tankhouse line at the Rönnskär smelter in Skelleftehamn with a capacity of 230,000 tons, on track to reach full operation in the fourth quarter of 2026. This is happening in the most strained concentrate market in decades. At Aitik near Gällivare, one of Europe's largest open-pit copper mines, an expansion of the dam facility is also underway. Both projects coincide with the EU's Critical Raw Materials Act, which encourages domestic European production.

The quarterly report on 28 April showed what a copper price near record levels means in practice: operating profit increased by 70 percent over the year (Boliden, Q1 2026). Whether Rönnskär's new capacity will reach full operation in a market defined by shortage or surplus will not be decided in Skelleftehamn. Rather, it will be decided in the Strait of Hormuz, in Beijing's export policy, and in the mining projects that have yet to receive their permits.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.