SEB Q1 2026: Costs Down, Discipline Up

SEB is one of Scandinavia's largest banks, built around serving large Nordic corporations, wealthy individuals, and Baltic retail customers. It is not a consumer app or a high-growth tech company. It is a traditional, well-run institution that has been around long enough to weather a few crises. That track record is valuable, especially in the context of Q1 2026, which saw a military conflict in the Middle East, an effectively closed Strait of Hormuz, surging energy prices, volatile equity markets, and renewed inflation concerns. Against that backdrop, SEB's recent report is more encouraging than the headline numbers suggest.

The Operating Jaws Story

Operating profit, which is what a company earns after costs but before taxes, rose 7 percent compared to the previous quarter to SEK 9.4 billion. That is a decent number, but it is not the main point. The more important figure is what management calls "operating jaws," meaning income growing faster than costs. In Q1, SEB's revenue fell 7 percent year-on-year, but costs fell 8 percent. That one percentage point gap is what SEB has been promising investors for two years. In a quarter where the macro environment handed out problems freely, the bank tightened its belt faster than conditions loosened its income. That is what cost discipline actually looks like in practice.

Key Figures Illustrating the Context

Return on equity was 13.1 percent, up from 12.9 percent last quarter but still below the 13.4 percent from a year ago. SEB's long-term target is 15 percent, so there is still ground to cover, but the trend is positive. Total operating costs decreased to SEK 7.6 billion, a 10 percent drop from Q4 2025 and the sharpest quarterly cost reduction in recent memory. Net interest income, reflecting what a bank earns on loans minus what it pays on deposits, slipped 1 percent to SEK 10.2 billion, due to fewer calendar days and the lingering effects of last year's rate cuts. Asset quality remains exceptionally clean, with net expected credit losses at just 7 basis points, where a basis point is one-hundredth of a percent, meaning barely anything in the loan book is going bad. The CET1 ratio, which measures how much of a capital buffer a bank holds against potential losses, stands at 17.5 percent, well above regulatory requirements.

Related Products

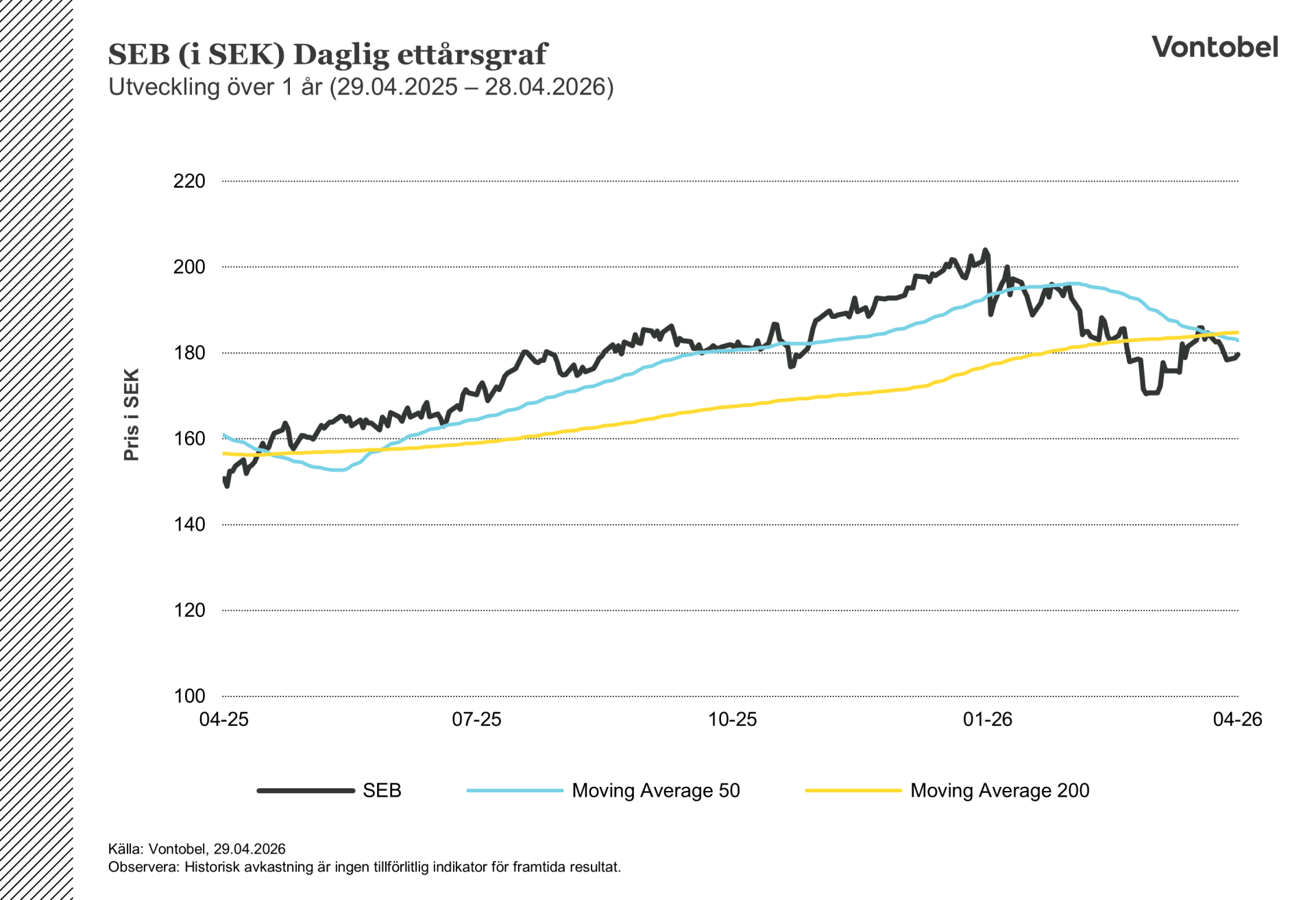

SEB (in SEK) Daily one-year chart

SEB(in SEK) Daily five-year graph

The Baltic Numbers Are Less Concerning Than They Appear

At first glance, the Baltic division appears alarming, with return on equity dropping from 26.3 percent a year ago to 16.9 percent this quarter. Upon closer inspection, however, it is almost entirely an accounting and regulatory issue. SEB is in the process of building new internal risk models for the Baltic business, and as a result the allocated capital, meaning the equity assigned to that division for calculation purposes, ballooned by 47 percent in local currency. The same profit spread across a much larger capital base mathematically reduces the return ratio. The underlying Baltic business is doing well, with record customer satisfaction scores, solid lending growth, and clean credit quality, including a net reversal of provisions.

The Rate Environment and What SEB Is Doing About It

European and Nordic central banks have largely completed their rate-cutting cycles, which removes a headwind for bank margins but also caps the upside from rate-driven income growth. SEB's net interest income has been declining since 2025 due to lower rates, and this trend will not reverse quickly. Peers across the Nordic region face the same structural challenge. SEB is not waiting for rates to rescue the income line. Instead, the bank is cutting costs while pushing fee-based growth in wealth management and capital markets, where Q1 saw strong institutional fund flows and historically high activity in secondary equity trading.

What to Watch From Here

The most important thing to monitor is whether the positive operating jaws can persist as the situation in the Middle East either stabilises or escalates further. If energy prices remain high and corporate clients stay cautious, fee income will stay soft even as costs improve, creating an uncomfortably narrow gap.

The second thing worth watching is the Baltic IRB model process, where IRB refers to the bank's own internal approach for calculating risk. Once SEB receives regulatory approval for its updated models, the inflated capital base will reset and that division's return on equity will mechanically recover, which may be a tailwind the market is currently underpricing. For a stock trading at SEK 179.65 as of 28 April 2026, investors are getting a conservatively managed bank with a clean balance sheet and a management team that is finally delivering on the efficiency promises it has been making for years.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.