Atlas Copco: Currency Weighs, But Demand Holds

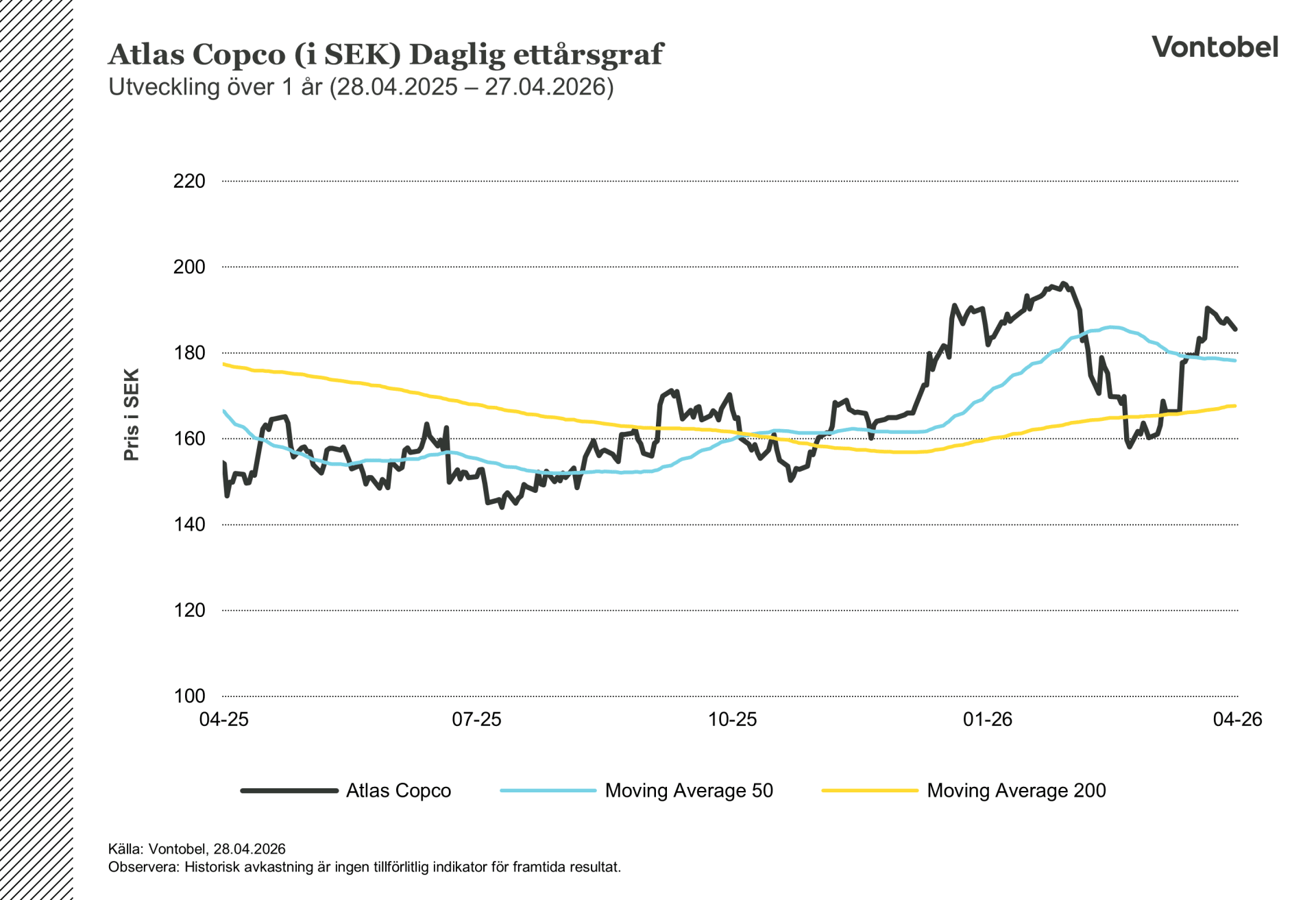

Atlas Copco is one of Sweden's most admired industrial companies, manufacturing compressors, vacuum systems, power tools, and generators sold to factories and semiconductor fabrication around the world. The company is widely regarded as an indicator of the health of the global industrial sector, so when it reports its results, people pay attention. This quarter was more important than usual because investors were looking out for two things. They wanted to know how bad trade tariffs and currency fluctuations would affect the company, and secondly whether the semiconductor recovery was real. The answers came in on April 28, and they are more nuanced than the headline numbers suggest. ATCO A shares closed at 185.55 SEK on April 27, the trading day before the report was published.

Further insights below the surface

A significant takeaway from this report is that Atlas Copco is growing organically, however the currency effect is significant to give the impression that the company is shrinking. Revenues fell by 5 percent and orders by 3 percent. Strip out the currency impact, which knocked 11 percentage points off both figures, and the underlying business actually grew: Orders rose by 5 percent organically and revenues by 3 percent. This distinction is important when deciding whether the company has a demand or an exchange rate problem. Currently, it is almost entirely the latter, though it is worth bearing in mind that FX cuts both ways and a future reversal is not a sufficient basis for a thesis in itself.

Related Products

Key figures illustrating the context

Orders received came in at MSEK 45 395, down from MSEK 46 604 last year in reported terms, while organic order growth of 5 percent points to real demand momentum. The reported operating margin landed at 20.4 percent, slightly better than the 20.1 percent a year ago, though it is worth noting that the adjusted operating margin, which excludes items affecting comparability, was 20.5 percent versus 20.8 percent. On an underlying basis, margins are therefore marginally softer year-on-year, even if the resilience is still notable given the currency drag and tariff costs. Earnings per share came in at SEK 1.28 versus SEK 1.35 last year, a modest decline. The figure warranting closer attention is operating cash flow, which dropped from MSEK 6 575 to MSEK 4 355, a decline of 34 percent. This was driven mainly by an increase in inventories and trade receivables during the quarter. It is worth watching but not yet alarming.

The semiconductor surge running underneath the print

At first glance, Vacuum Technique's revenue decline of 5 percent looks weak, but a closer inspection reveals that this is largely due to currency effects. Organic revenue growth was 8 percent, with order growth came in at 32 percent organically. Vacuum is the most interesting division in the report because it supplies equipment to chipmakers, and the semiconductor industry is in the middle of a clear upcycle. Orders for vacuum equipment to the semiconductor and flat panel display industry grew strongly in all major regions, both year-on-year and sequentially. This is a leading indicator. Orders today will become revenue in the coming quarters, and the order book currently being built in Vacuum Technique suggests the possibility of a stronger second half of the year.

Compressor Technique is the larger swing factor

Compressor Technique is the largest division by some distance and remains the engine of group earnings, which is why its weaker performance deserves attention. Reported orders were down 10 percent with organic orders down 3 percent. The bulk of the headline fall driven by a 10 percent currency hit rather than operational weakness. The decline came mainly from gas and process compressors, where the comparison quarter benefited from large marine LNG and air separation orders that did not repeat. Industrial compressor demand was essentially unchanged on an underlying basis, and service was a clear bright spot, with healthy order growth across all major regions. Nevertheless, the slower order intake on large equipment serves as a reminder that the Vacuum upside story alone cannot carry the group. For the overall trajectory to improve from here, Compressor needs to stabilise alongside continued strength in Vacuum.

Currency dominates, tariffs are a secondary drag

The macro backdrop for this report is genuinely difficult, but it is important to understand the relative weight of the headwinds. The dominant problem is currency, which has knocked 11 percentage points off both orders and revenues. Trade tariffs are also evident in the costs, but management considers them to be a smaller factor in the margin factor than currency. With manufacturing spread across multiple continents and operations in over 180 countries, the company has more flexibility than most to reroute supply chains and adjust pricing. The near-term outlook remains unchanged, with customer activity expected to stay at current level. This is not particularly exciting, but it is steady, and in today's macroeconomic climate, stability is underrated.

Two things that could move the stock from here

The first is whether the surge in orders for Vacuum Technique translates into revenue over the next two quarters. If so, the organic growth picture becomes considerably harder to overlook. The second is the cash flow trajectory. A single-quarter increase in working capital is not a concern in isolation, but if it continues into Q2 it will start to raise questions about operational discipline. The business is performing better than the reported figures suggest, the semiconductor tailwind is real, and the headline drag from currency will not last forever. Whether this will be enough to change the share price trajectory depends on how the next two reports develop.

Atlas Copco (in SEK) Daily one-year chart

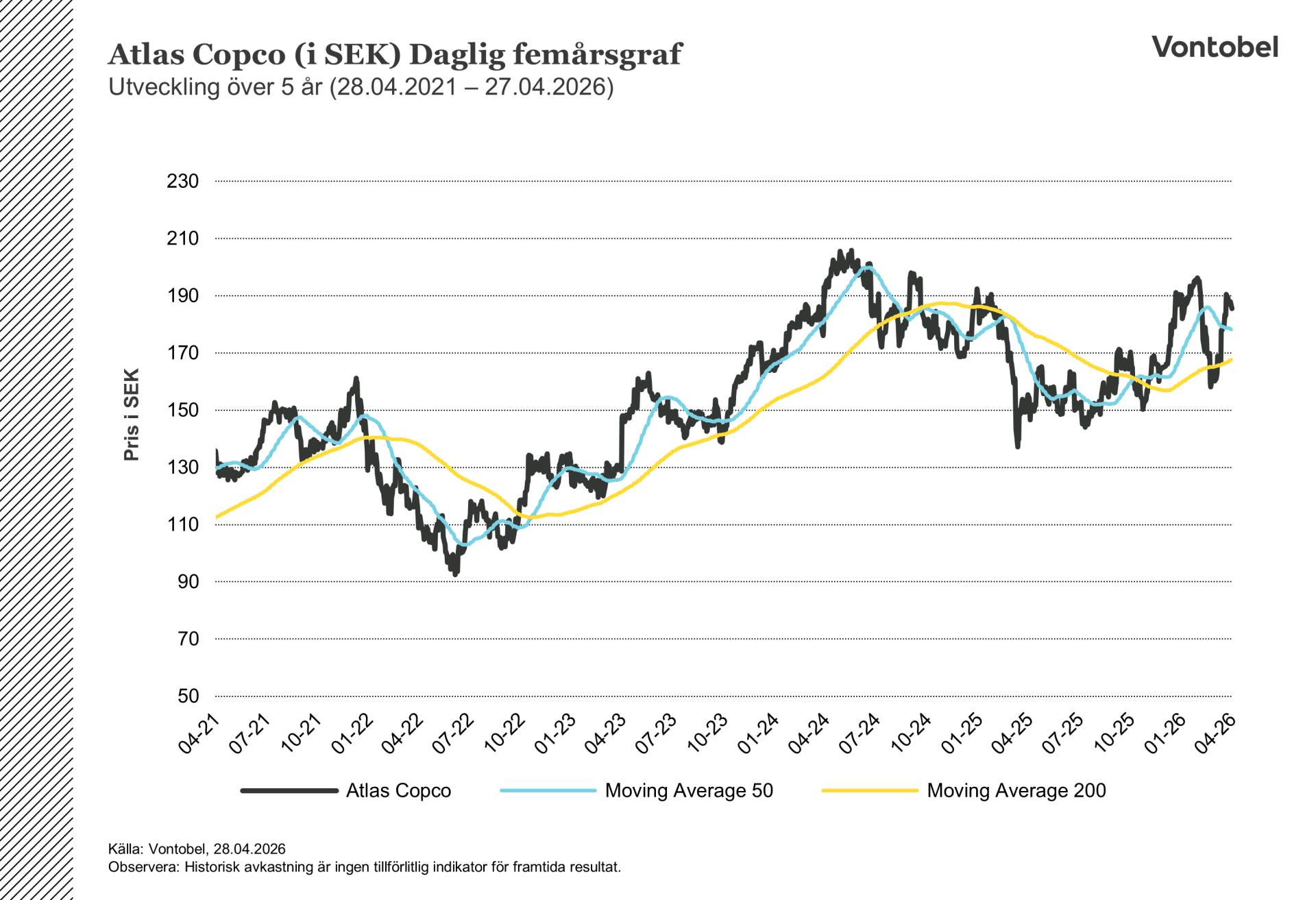

Atlas Copco (in SEK) Daily five-year graph

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.