SAAB: Sales up 21 percent, and demand is still rising

Saab is the company behind the Gripen fighter jet, the Carl-Gustaf anti-tank weapon, and a growing range of radar and submarine systems. For most of its history, it was a quiet, well-run Swedish industrial company that few people outside the defence industry paid much attention to. That changed when Russia invaded Ukraine. Since then, Saab has become one of the most closely watched defence stocks in Europe, with higher expectations for every quarterly report. This report, covering January through March 2026, is important because it is the first real test of whether the company can maintain the exceptional growth rate it achieved in 2025, when organic sales, meaning growth excluding currency movements and acquisitions, increased by 26 percent.

The growth shows no signals of slowing

The most important takeaway from this report is that Saab achieved 23.6 percent organic sales growth in the first quarter (Source: Saab AB, Q1 2026 Interim Report, published 23 April 2026.). This is not a fluke or a one-time catch-up effect. It suggests continued acceleration. Total sales reached SEK 19.2 billion, up 21 percent. Operating income, profit after running costs but before interest and taxes, rose 32 percent, lifting the operating margin to 10.0 percent from 9.2 percent a year earlier. Every business area reported double-digit sales growth. This kind of broad-based growth is unusual and indicates that demand is structural rather than driven by a single fortunate contract.

Related Products

Key figures that provide the full picture

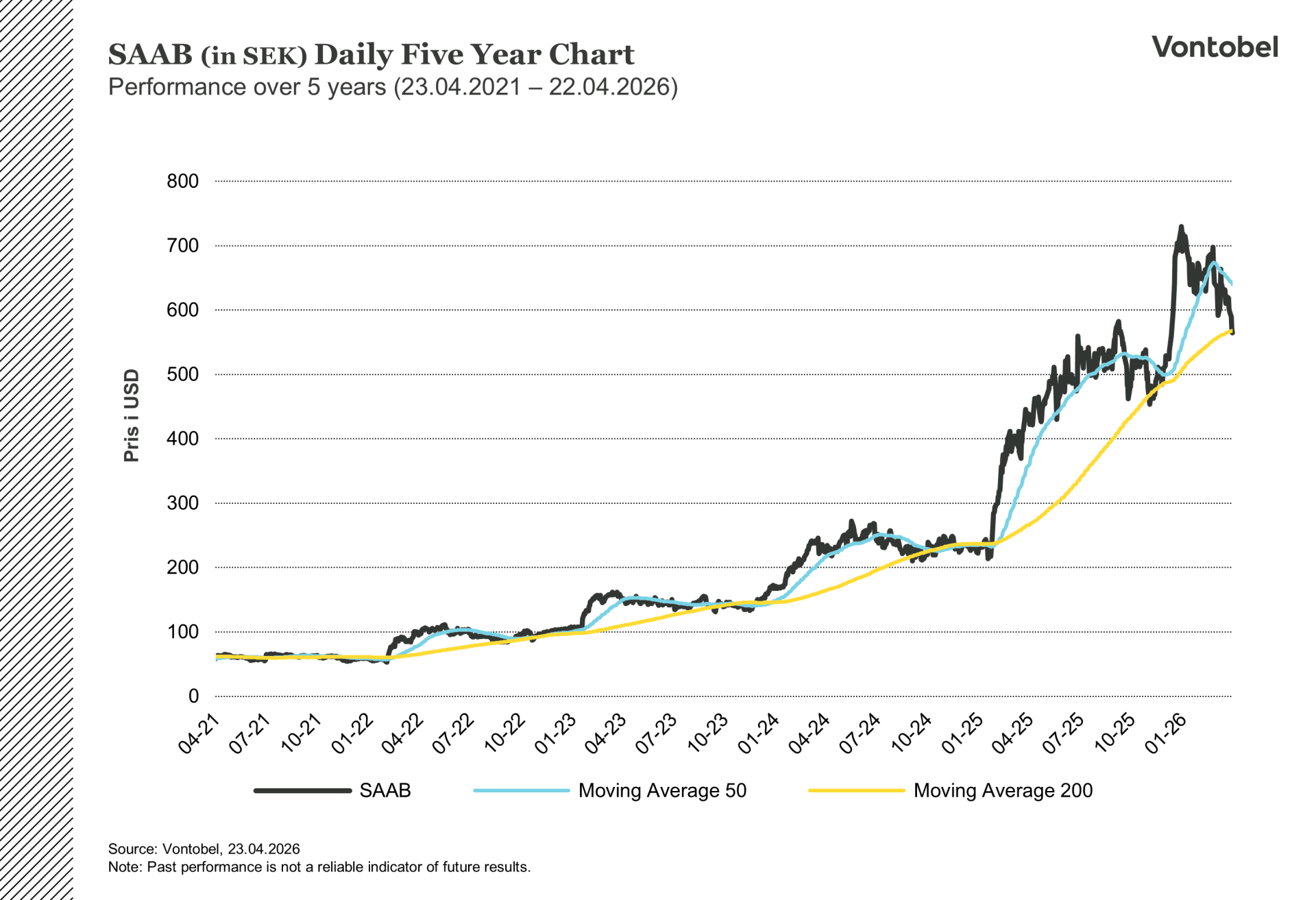

The order backlog, or the total value of contracts that Saab has already won but not yet delivered, stands at SEK 274 billion. A year ago, it was SEK 189 billion. This figure provides Saab with a clear view of future revenue. At the current delivery rate, it represents over three years secured work. The Surveillance unit, the unit that sells radar systems such as the Giraffe 1X, grew sales by 32 percent and increased operating profit by 52 percent, suggesting that higher volumes are starting to support margin improvement. Dynamics, which makes missiles and ground combat weapons, raised its operating margin to 17.5 percent from 14.7 percent, which is a very strong level of profitability for a manufacturer of ammunition. Earnings per share, what the company earned for each share outstanding, came in at SEK 2.65, up from SEK 2.35. According to the Q1 report, as of April 22, the stock was trading at SEK 564.80. Trailing twelve-month earnings per share are therefore SEK 11.98, a useful starting point for any valuation discussion.

SAAB (in SEK) Daily one-year chart

SAAB (in SEK) Daily five-year chart

The headline that confused people, and what it really means

At first glance, order bookings appear weak, dropping 5 percent to SEK 18.2 billion from SEK 19.1 billion in the same quarter last year. However, a closer look suggests that this is mainly a comparison issue. The first quarter of 2025 included an unusually high number of large orders worth more than SEK 1 billion each. Excluding those orders, medium-sized orders actually grew 28 percent. The book-to-bill ratio, which compares new orders received with revenue delivered, was 0.95 times, meaning Saab delivered slightly more than it booked during the quarter. At this level of delivery, that ratio appears normal and not a warning sign. Meanwhile, the backlog remained at SEK 274 billion, barely moving from year-end.

Defence spending is entering a new phase, and Saab is well placed

Europe’s NATO members are under steady political pressure to raise defence budgets toward 2 percent of GDP and beyond, with several now aiming for 3 percent. Saab primarily serves this customer group, and the active campaign pipeline indicates that the inflow of new orders is likely to continue. On April 1, the company also created a new business area called Naval bringing together its submarine and naval electronics operations. This is more than just a reorganisation. It is also a strategic signal. Saab is positioning itself for a period in which naval warfare, especially submarine capability, could become one of the next major areas of European defense spending, and the ongoing contract talks with Poland on a next-generation submarine program lend real short-term relevance to this review (Source: Saab AB, Q1 2026 Interim Report, published 23 April 2026.).

Two things that could move the stock from here

The first factor is the margin trend. Saab’s medium-term goal is to grow operating income to grow faster than sales, which it achieved in this quarter. If that continues into the second half of the year, there is a solid case for analysts to raise earnings forecasts. The second is the Polish submarine contract. A formal signing in 2026 could add a programme potentially worth tens of billions of kronor to an already substantial backlog, prompting a quick market reaction. Those are the two key things to watch as the year progresses.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.