ABB: Record orders and record cash flow. ABB is running at full speed.

ABB is a Swiss-Swedish industrial group that manufactures and sells the equipment connecting electricity from power grids to buildings, factories and data centers. The company also produces automation systems for ships, refineries and manufacturing plants. In other words, ABB sits at the intersection of two of the most powerful trends in the global economy: electrification and digitalization. When ABB reports, it provides an up-to-date assessment of global industrial demand. This report is especially important because it comes from a tariff-driven trade war and fresh geopolitical escalation in the Middle East, both of which were expected to affect industrial confidence. However, ABB’s Q1 2026 results, published on April 22, 2026, suggest the opposite.

The Headline Is Simple: Demand Is Accelerating, Not Slowing

Orders reached $11.3 billion in the quarter, setting a new record and marking a 32% increase from a year ago, or 24% on a comparable basis. This comparable basis strips out currency movements and acquisitions to show the underlying business performance. This figure is significant because today’s orders will become future revenues and profits. The total backlog, or the stock of booked but undelivered orders, now stands at a record $27.5 billion, up 27% year over year. ABB’s revenue visibility for the rest of 2026 is as strong as it has ever been. The company is not just moving quickly. It is pulling further ahead.

Four figures that say it all

Revenue came in at $8.7 billion, up 18% year on year, or 11% on a comparable basis. Operational EBITA, ABB’s preferred measure of underlying profitability, which excludes interest, taxes and acquisition-related write-downs, increased by 37% to $2.05 billion, pushing the margin to 23.5%, up 3.2 percentage points from a year ago. Earnings per share increased 21% to $0.73. Free cash flow, the actual cash the business generated after investments, reached $1.25 billion, the strongest first quarter in ABB’s history.

By region, the Americas drove exceptional momentum, with the United States alone posting a 67% increase in comparable orders. Electrification, ABB’s largest division, recorded a striking 44% comparable increase in orders, with data centers delivering triple-digit order growth. This is not a rounding error.

Related Products

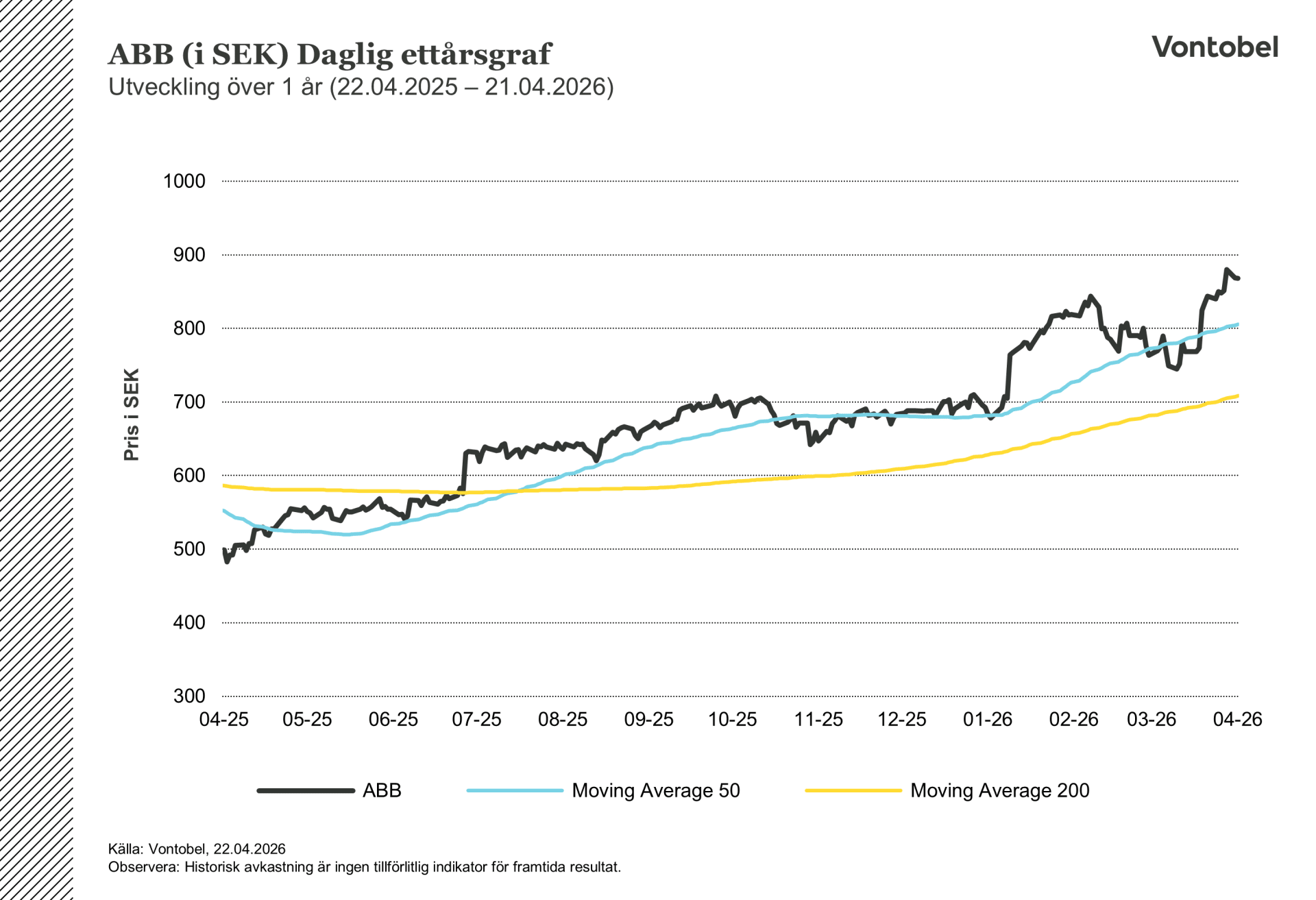

ABB (in SEK) Daily one-year chart

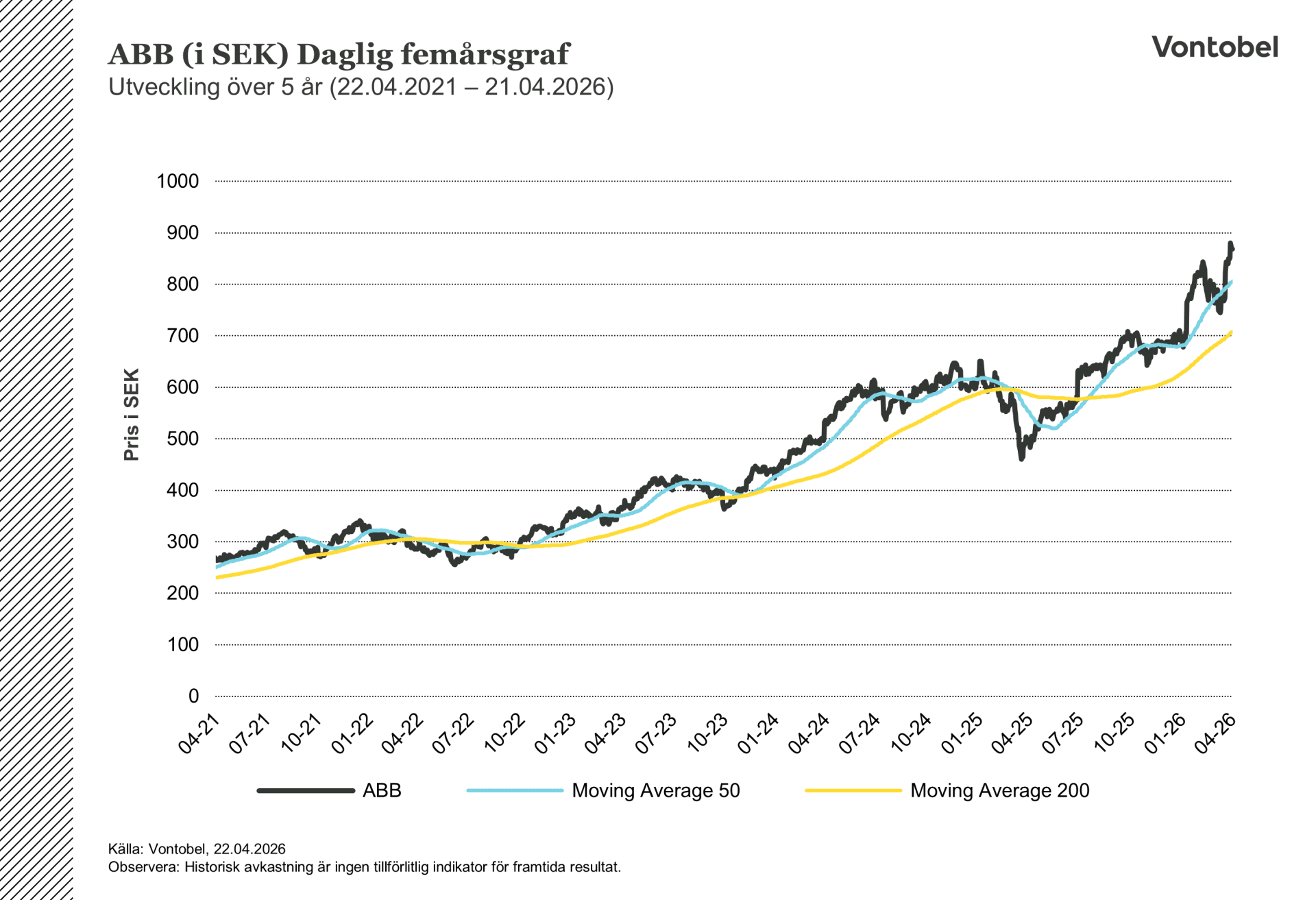

ABB (in SEK) Daily five-year graph

The Margin Story Looks Messy. It Isn’t.

At first glance, the fall in the gross margin, revenue minus the direct cost of making products, by nearly 3 percentage points to 39.4% looks concerning. However, a closer look shows that this was almost entirely a timing effect related to how ABB accounts for currency and commodity hedging contracts, and that ABB is not being squeezed on pricing or hit by commodity costs. These are unrealized paper losses that should reverse when the underlying trades are settled. The underlying business has not deteriorated.

That said, the 320-basis-point improvement in the Operational EBITA margin also warrants closer inspection. Of that increase, 250 basis points came from a one-off gain on the sale of real estate, not from operational improvement. The genuine improvement in the business was a respectable, but more modest, 70 basis points. Both of these factors need to be considered at the same time.

ABB Is Sitting in the Middle of the Biggest Infrastructure Trend

The structural backdrop for ABB could hardly be more supportive. Utilities are investing heavily in grid reliability. Data center operators are racing to increase power capacity for AI infrastructure. Spending tied to the energy transition, including solar, heat pumps and electric vehicle charging, is feeding directly into ABB’s product lines. The company has also introduced an upgraded distributed control system platform that uses AI analytics. In March, ABB shareholders approved a dividend of CHF 0.94 per share, and a new $2 billion share buyback programme has already begun. ABB is growing while also returning capital, a combination that rarely goes unnoticed.

Two Things to Watch From Here

The upgrade to ABB’s guidance is significant. The company now expects comparable revenue growth of between 10% and 20% for the full year, along with margin improvement even after stripping out the real estate gain. This is a confident signal from management.

There are two factors that could move the stock sharply from here. First, tariff escalation. ABB has acknowledged early signs of disruption in the Middle East and some sensitivity in process industries. A further deterioration in the global trade environment could result in a faster decline in order intake than the backlog can offset. Second, the pending $5.2 billion divestment of the Robotics division to SoftBank, expected to close in the second half of 2026, will release significant capital that ABB will need to deploy intelligently. How management handles that cash will reveal a great deal about the next chapter of this story.

Source: ABB's report for the first quarter of 2026, published on April 22, 2026

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.