How long will the war last?

This week's case asks how long President Trump will continue the war against Iran. East Asian economies are more sensitive to high oil prices than those in Europe and the U.S. Therefore, a short war would likely benefit the Nikkei index the most.

Case of the week: According to Trump, peace trade is soon to come

On February 28, the United States and Israel launched a joint military offensive against Iran, killing its Supreme Leader, Ayatollah Ali Khamenei. Mojtaba Khamenei, the son of the slain supreme leader, was named his father's successor. Iran's military and political leaders swiftly pledged allegiance to the new Supreme Leader. Hardliners took to the streets in a show of force. Since then, Iran has launched its first wave of missile strikes under his command.

At the beginning of the conflict, President Donald Trump said the war would last four to five weeks. However, he has since declared that the U.S. is "well ahead" of that estimated timeline. Trump also said, "I think the war is pretty much over," and "They have no navy, no communications, no air force." Conversely, Iran has insisted that it is prepared for a prolonged conflict and sees no room for diplomacy.

Trump should ask himself whether the U.S. military is prepared for a long war. During the presidential campaign, he promised his supporters that he would not involve the military in long wars abroad. Therefore, entering into a long war would break that promise and increase the likelihood that Republicans losing the U.S. midterm elections in November 2026. After that, Trump would be a lame duck for the rest of his term.

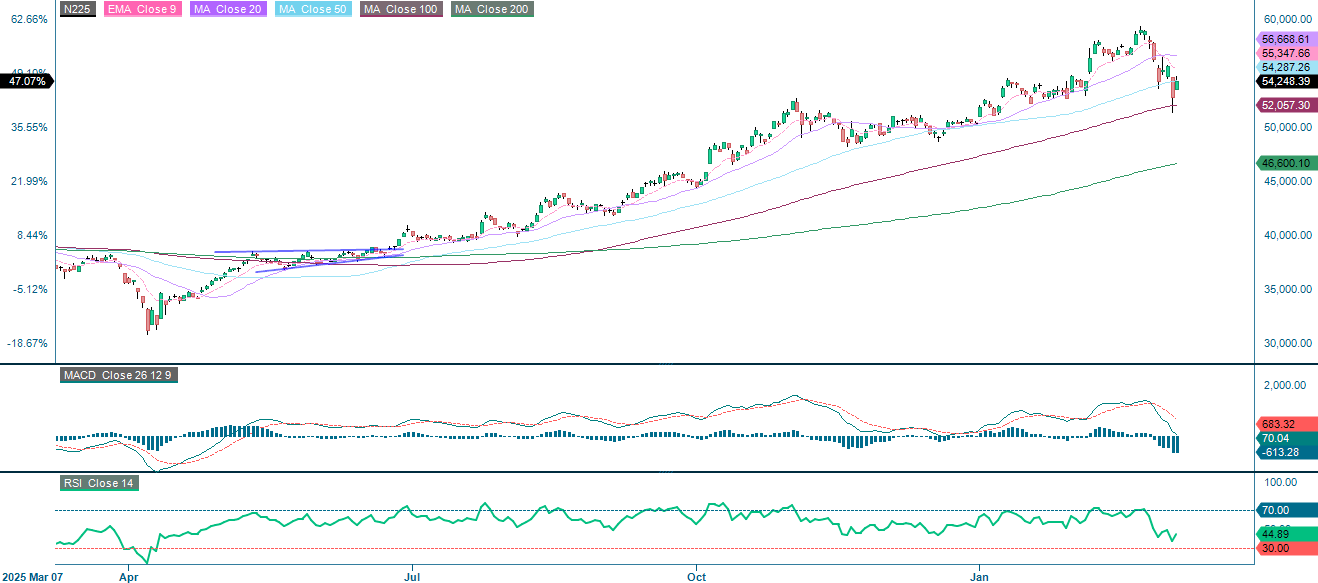

Since the outbreak of hostilities, global oil prices have surged dramatically. Japan is the biggest loser from the war because it imports around 95% of its oil from the Middle East, with around 70% of which transits the Strait of Hormuz. Since February 27, the Nikkei 225 has fallen by 8.1%, while the Dow Jones Industrial Average has fallen by2%. A ceasefire, the release of strategic petroleum reserves by the G7 (to be discussed this week), or interventions by the Bank of Japan to stabilise markets could turn things around. If the war lasted only four to five weeks, the Nikkei would likely outperform other stock indices during the recovery phase. The potential reward is high, but so are the uncertainty and risk.

Related Products

Nikkei 225 (JPY), one-year daily chart

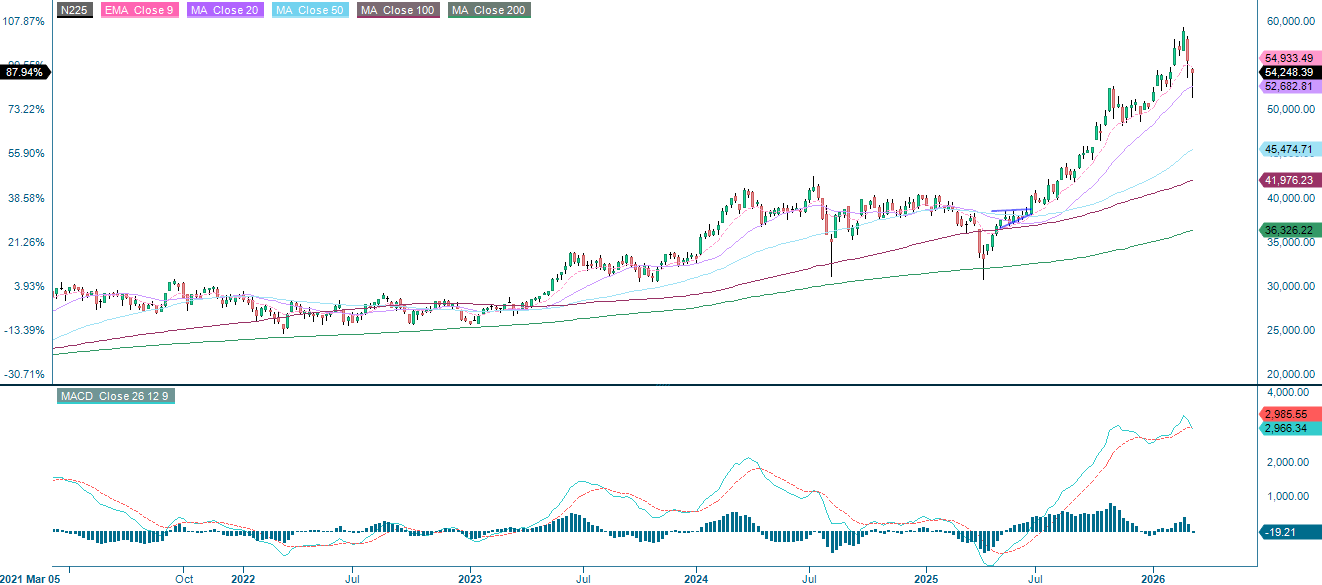

Nikkei 225 (JPY), five-year daily chart

Macro comments

Stock markets around the world have been very volatile over the past week, with rising oil prices being the most concerning factor for investors. This concerns increased transportation costs for companies, as well as inflationary impulses that can drive up market interest rates. U.S. stock market indices have been less affected, while Asian and European indices have been greatly affected. This is because Asian and European countries are more sensitive to higher oil prices and disruptions in world trade.

On Wednesday, March 11, interim reports from Clas Ohlson, Inditex, Klöckner, and Rheinmetall are expected. The macro news feed begins with Japan's February producer price index. Next are the consumer price indexes for February in Germany and the US (see graph below). The US Department of Energy will release weekly oil stock statistics. OPEC will also release a monthly oil report.

On Thursday, March 12, interim reports from the Danish company Bavarian Nordic, the German companies BMW, Daimler Truck and Zalando, and the German bank Deutsche Bank will be released. Turning to the macroeconomic news, Sweden's Consumer Price Index (CPI) will be released in February. The IEA will present a monthly oil report. From the U.S., data on housing starts and the goods trade balance in January, as well as weekly initial jobless claims.

On Friday, March 13, the release of major macroeconomic data begins with the UK's January GDP and industrial production, followed by Germany's February wholesale prices. Next are the February CPI figures for France and Spain's and the Eurozone's industrial production in January. Finally, the US will release macroeconomic data on personal consumption and the January inflation (PCE), durable goods orders, and JOLTS vacancies.. Additionally, the Michigan index for March will be published.

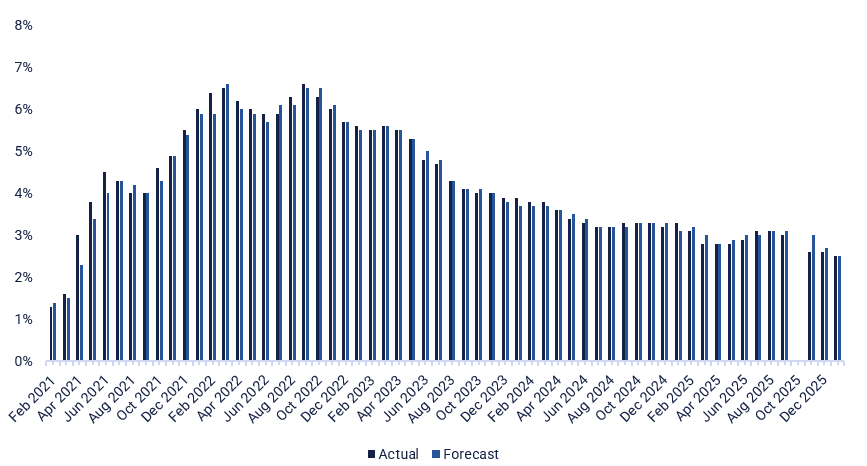

U.S. Core CPI Index, five-year monthly chart

Hopes for better times lead to larger gains to be made for European indices

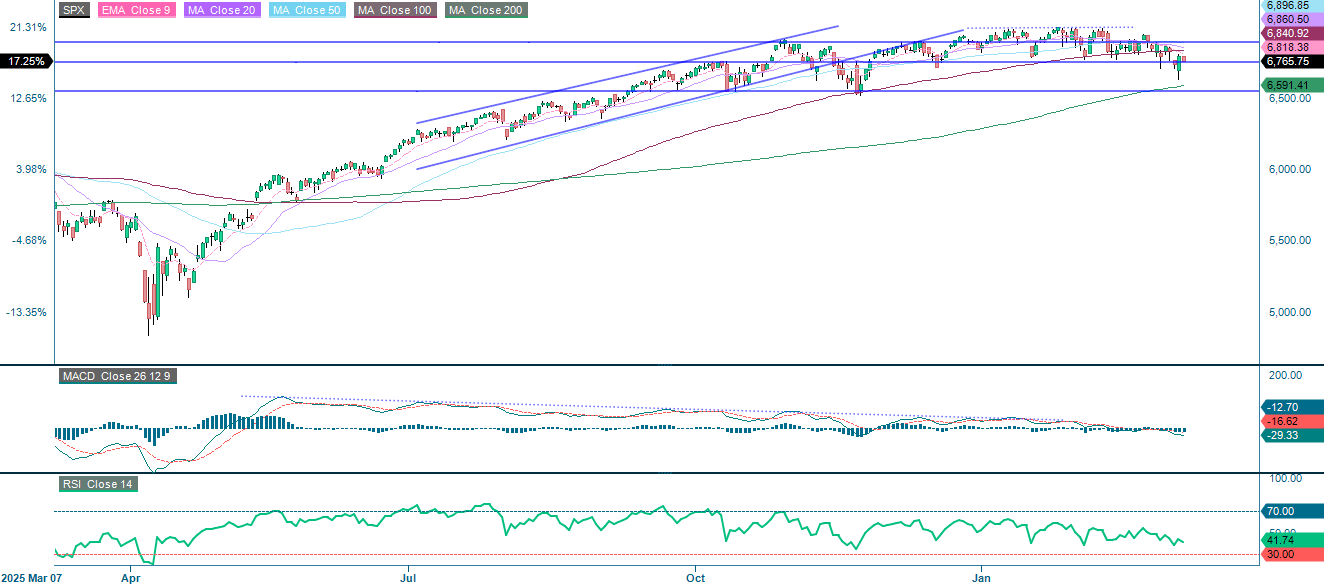

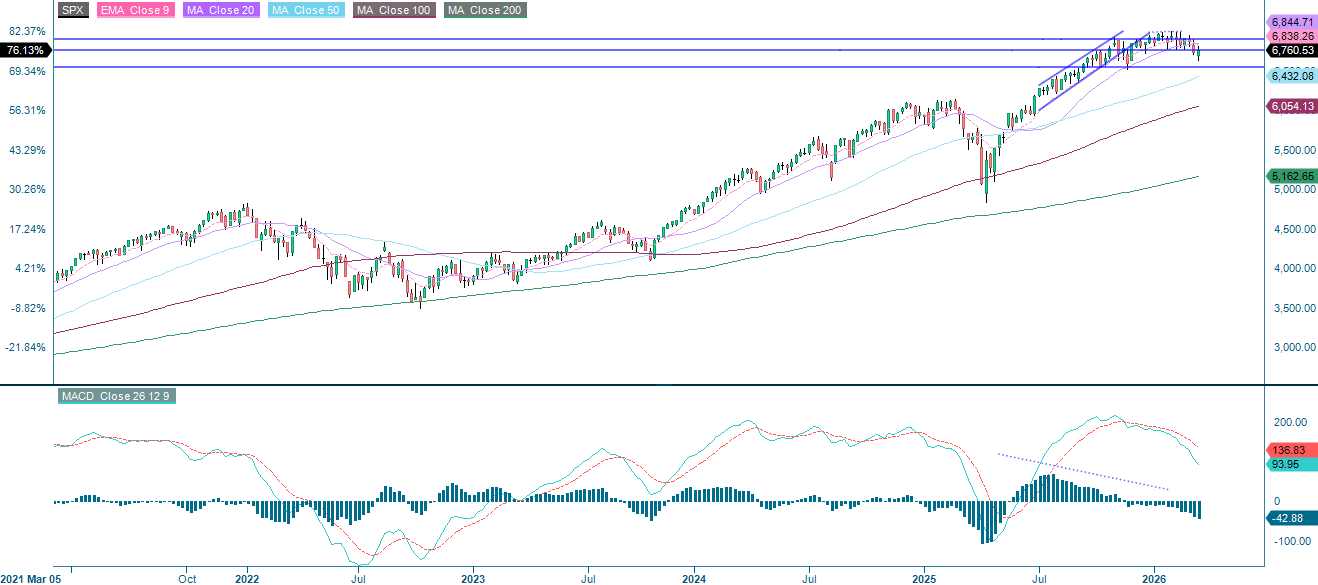

The U.S.-Israel military operation against Iran, which began around February 27, pushed oil prices above $110 per barrel by midweek. This triggered widespread risk-off flows due to renewed inflation concerns. On Monday, March 9, Trump's comments caused a sharp intraday reversal. As the chart below shows, the S&P 500 is currently trading below its EMA9 of 6,181. The next resistance level is in the 6,840–6,861 range, followed by 6,900. On the downside, initial support is in the range of 6,760, followed by the MA200 at 6,591. In the near term, headlines from the Middle East and signals from the G7 regarding a coordinated release of strategic oil reserves are likely to be the main catalysts for global equities.

Related Products

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), five-year weekly chart

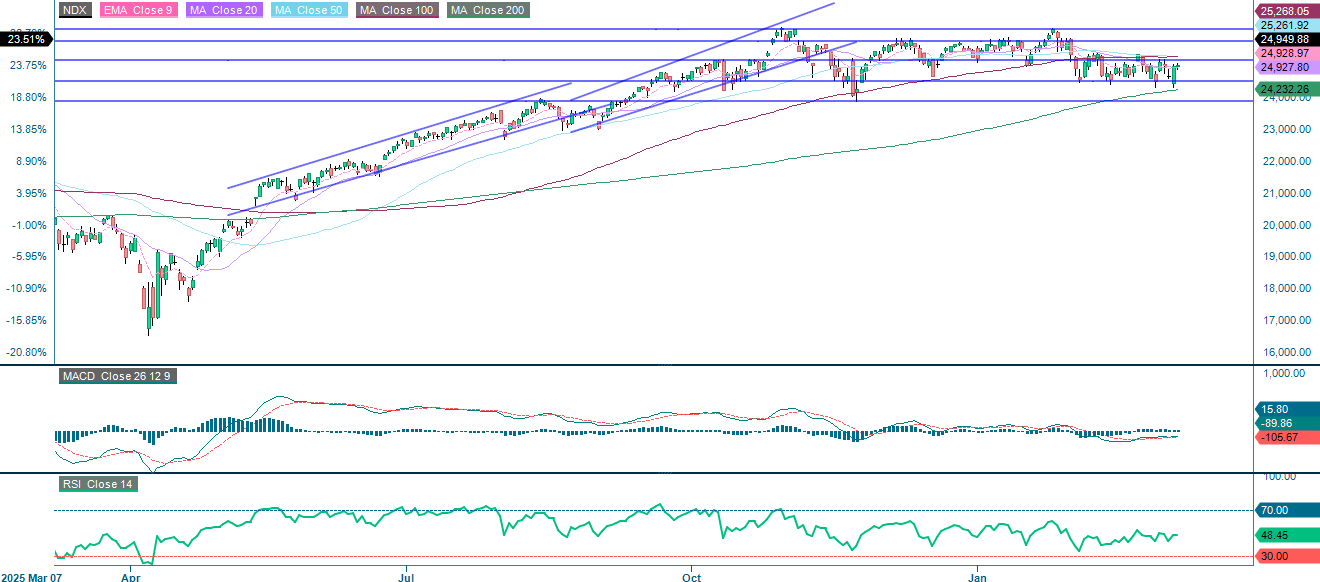

Large-cap tech stocks, which dominate the Nasdaq 100, have been relatively insulated from the conflict in Iran, given their minimal direct exposure to the energy sector. The trading range of 24,500–25,150 remains intact. An upside break would target the MA50/MA100, followed by 25,745. A downside break would open the door to the MA200 at 24,232 and then to 23,865.

Related Products

NASDAQ-100 (in USD), one-year daily chart

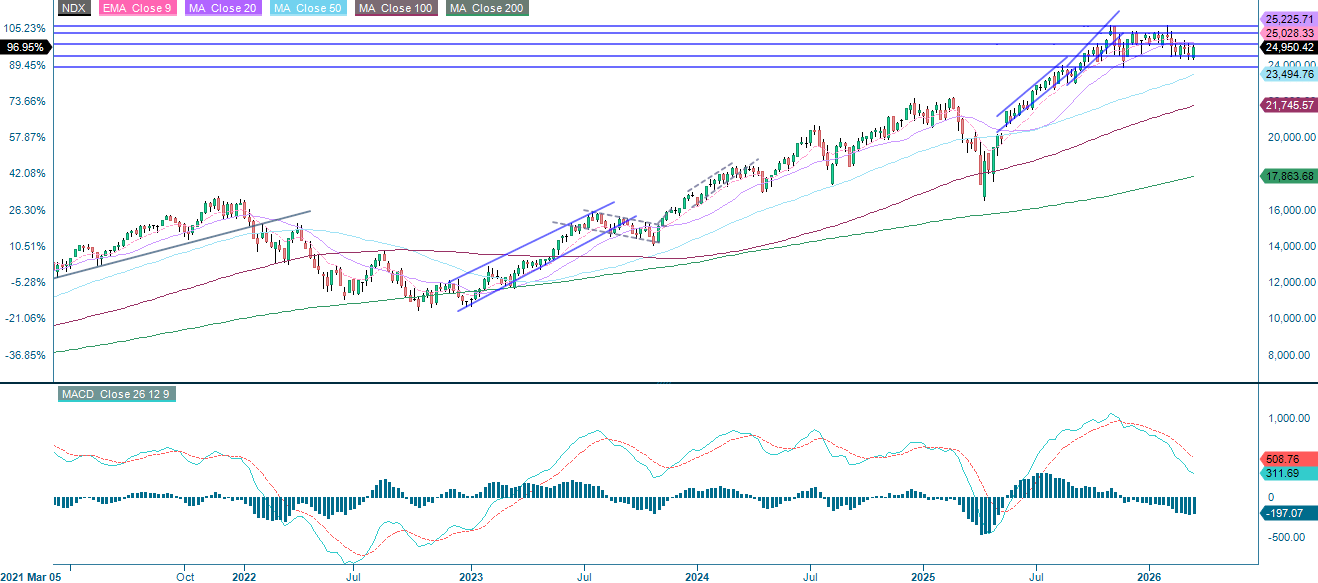

NASDAQ-100 (in USD), five-year weekly chart

Due to Iran- and oil-related headlines, the OMXS30 gapped up and is currently stuck between the EMA9 and the MA50. An upside break would target the MA20 at 3,134. However, a break below the MA50 at 3,067 and the support level at 3,040 suggests that the gap will likely be filled.

Related Products

OMX30 (in SEK), one-year daily chart

OMX30 (in SEK), five-year weekly chart

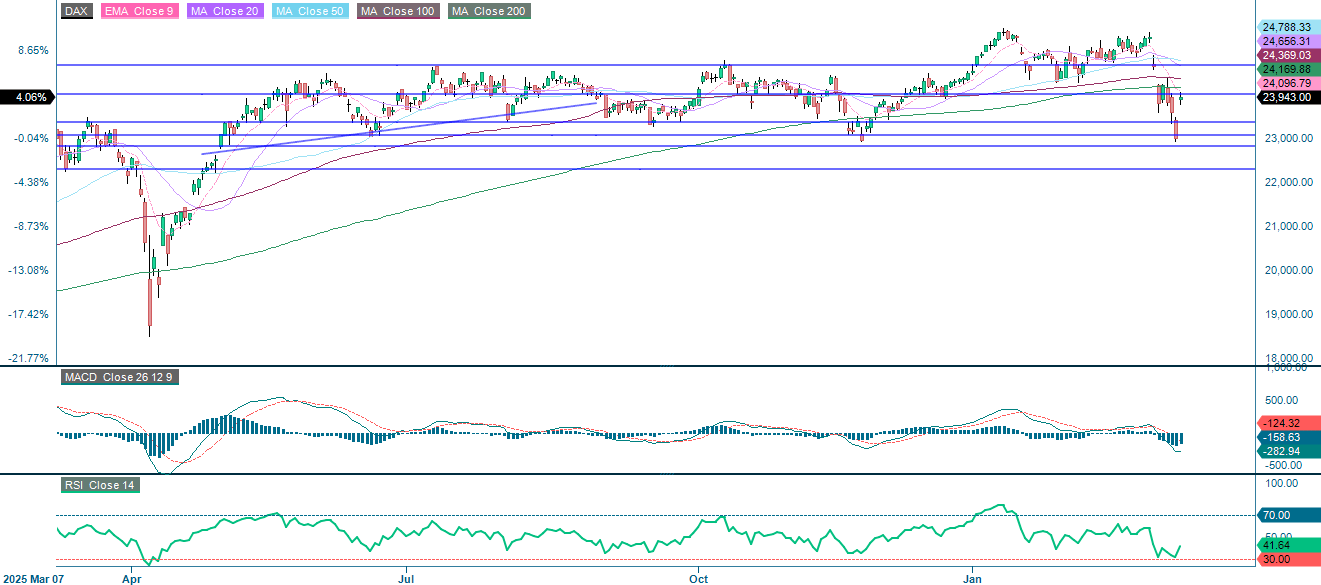

German industry has taken a harder hit than the Dow Jones Industrial Average due to its heavy exposure to energy costs. Nevertheless, the index has risen by 2.3% in response to recent Iran- and oil-related headlines. This highlights the higher beta that European indices have with regard to shifts in oil prices and geopolitical sentiment.

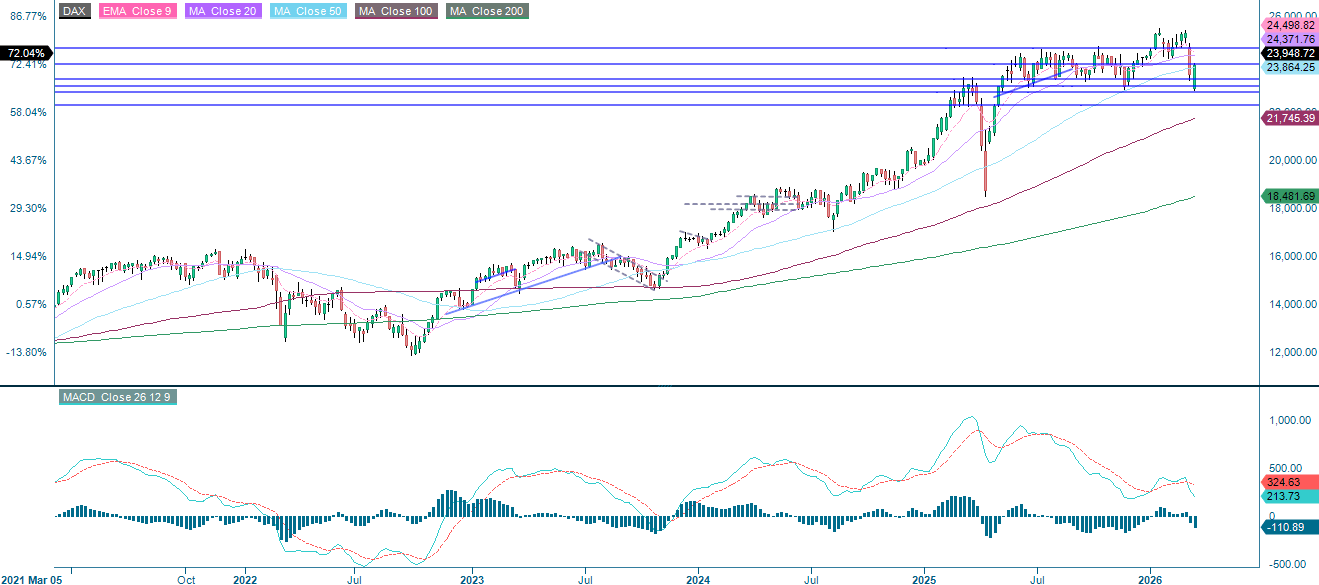

As the chart below shows, the DAX remains below the 24,000-resistance level. Above that, the next hurdles are the MA200, followed by the MA100 and 24,665. On the downside, reasonably firm support sits at around 23,365.

Related Products

DAX (in EUR), one-year daily chart

DAX (in EUR), five-year weekly chart

The full name for abbreviations used in the previous text:

EMA 9: 9-Day Exponential Moving Average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-Day Moving Average

MA50: 50-Day Moving Average

MA100: 100-Day Moving Average

MA200: 200-Day Moving Average

MACD: Moving Average Convergence Divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.