Higher inflation following the war with Iran?

The interest rate on ten-year U.S. government bonds has increased somewhat, though not by much. This is due to the continued rise in U.S. government debt, the inflationary effects of tariffs imposed by President Trump, and the US-Israeli military attack on Iran, all of which has caused higher oil prices. However, concerns about credit have been more closely linked to corporate bonds in the U.S. tech sector.

Case of the week: US interest rates are in a tug-of-war

Despite concerns about inflation, attacks by the White House on Federal Reserve policies, growing US government debt, and trade wars, the market for US Treasuries has remained relatively quiet recently. So far, there are few tangible signs of a "Trump premium," meaning investors are not demanding higher yields for owning US government debt. In fact, Treasury yields are lower now than when President Trump was inaugurated for his second term in January 2025.

A growing concern in 2026 is the state of corporate credit in the technology sector. According to The Economist, the significant increase in AI-related capital expenditures, coupled with the potential threat that AI poses to the business models of many tech companies, has likely contributed to the widening of credit spreads for tech bonds versus US Treasuries. Turbulence in corporate borrowing markets could prevent an increase in Treasury yields.

Meanwhile, US inflation remains elevated, surpassing the central bank's target. This weakens the case for further rate cuts by the Federal Reserve. Key factors to watch regarding interest rates include the labor market and energy prices. The US-Israeli attack on Iran could exacerbate inflation if it results in prolonged disturbances to the global oil supply, such as reduced Iranian oil production or a de facto closure of oil tanker transit through the Strait of Hormuz. Although the US labor market has weakened, which could initially be viewed as disinflationary, some of the weakness stems from deportations, which are arguably inflationary.

The U.S. 10-year Treasury yield has fallen to around four percent. This level has been a turning point for higher yields over the past year. At this level, bonds appear somewhat overbought, suggesting the potential for the yield to rebound.This indicates that it may be time to sell bonds. Conversely, if the yield breaks decisively down from the 3.9 to 4 percent range, one could argue that a trend toward lower rates has been established, which would push bond prices higher.

Related Products

US 10-year yield, one-year daily chart

US 10-year yield, five-year weekly chart

Macro comments

The US-Israeli military attack that began on Saturday, February 28, appears to be escalating. Since February 27, the Brent crude oil price has increased by about 9 USD per barrel, up from around 73 USD per barrel that Friday. If these levels persist, they will obviously have an inflationary effect on the US and European economies. Trade routes via the Strait of Hormuz and flights from Asia to Europe have already been affected as well.

On Wednesday, March 4, Bayer,Continental, Mercedes-Benz and Traton will release their interim reports. In terms of macroeconomic news, the day will be dominated by February's PMI figures for the services sector from Japan, China, Sweden, Spain, Italy, France, Germany, the Eurozone, the United Kingdom, and the United States. China will also release its manufacturing PMI figures. The Eurozone will release January's unemployment and producer price index figures. The U.S. will contribute ADP private employment figures for February and weekly oil stock statistics from the Department of Energy.

On Thursday, March 5, interim reports from the Swedish company Elekta, the British company Entain, and the U.S. companies Gap and Toro are expected. In terms of macro statistics, Sweden's consumer price index for February and France's industrial production for January will be released. The U.S. will provide statistics on Challenger job cuts for February, import prices for January, productivity for the fourth quarter, and initial weekly jobless claims.

The release of macro statistics begins on Friday, March 6, with South Korea's February Consumer Price Index. This will be followed by Germany's January industrial orders and the Eurozone's Q4 GDP. This afternoon, the U.S. will release its nonfarm payroll report for February. It is expected that 70,000 new jobs were added in February 2026, compared to the 172,000 jobs added in January. Statistics on U.S. business inventories will be also received in December.

U.S. Private Nonfarm Payrolls (Number of New Jobs) , five-year monthly chart

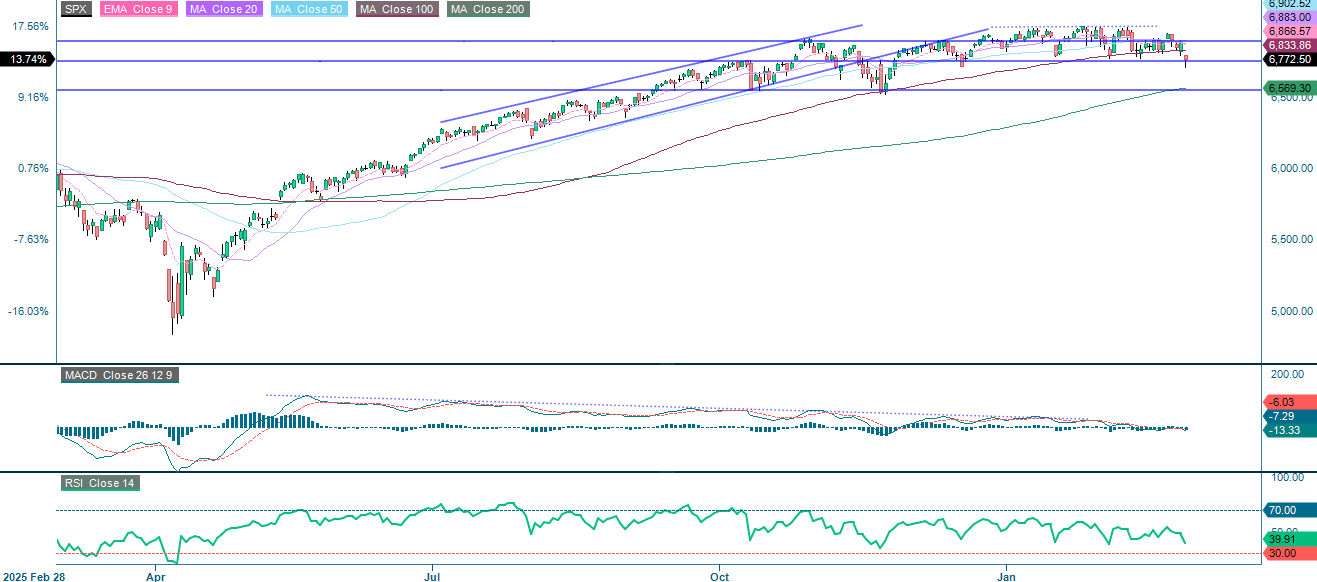

Do geopolitical tensions have short-lived effects on equities?

Nvidia's interim report turned out to be a "sell the news" event, adding to the pressure caused by rising geopolitical tensions. The S&P 500 is under pressure. As the chart below shows, the index is clinging to support around 5,750. A clean break below this level could open the door to the MA200, which is currently at 5,569. However, intraday price action has been volatile, and geopolitical flare-ups, including those resulting from higher oil prices, tend to be short-lived. On the upside, the first level of resistance is the MA100 (5,833), followed by 5,900. Key catalysts from here include Friday's U.S. nonfarm payrolls report, escalation or de-escalation of the conflict in Iran, and oil price direction.

Related Products

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), five-year weekly chart

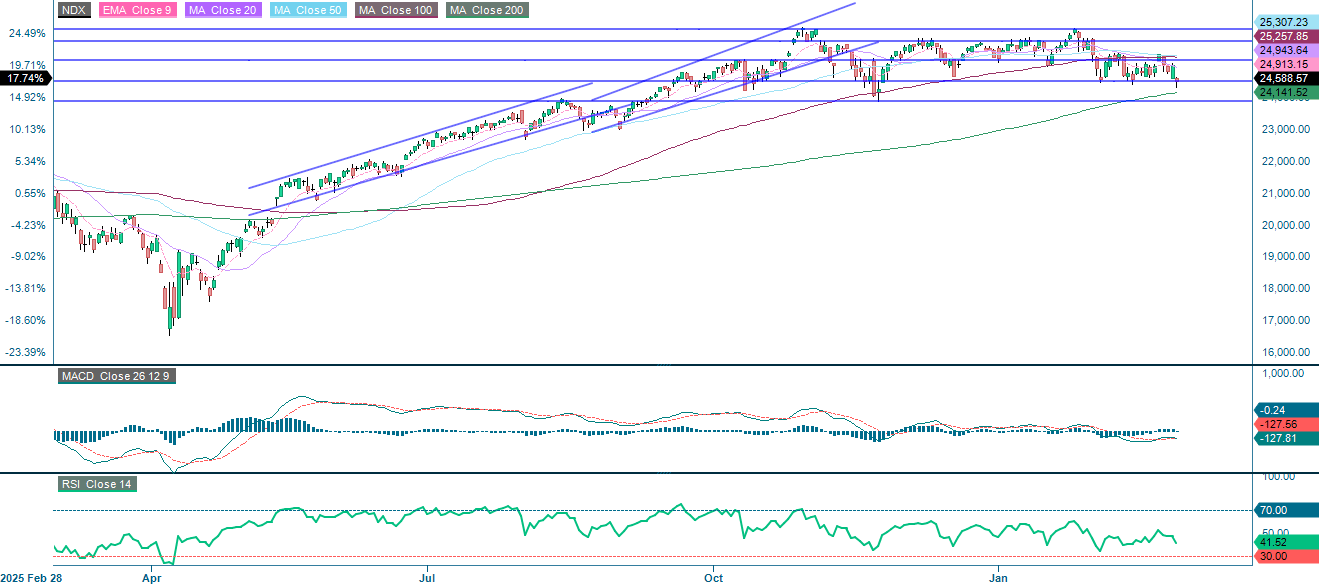

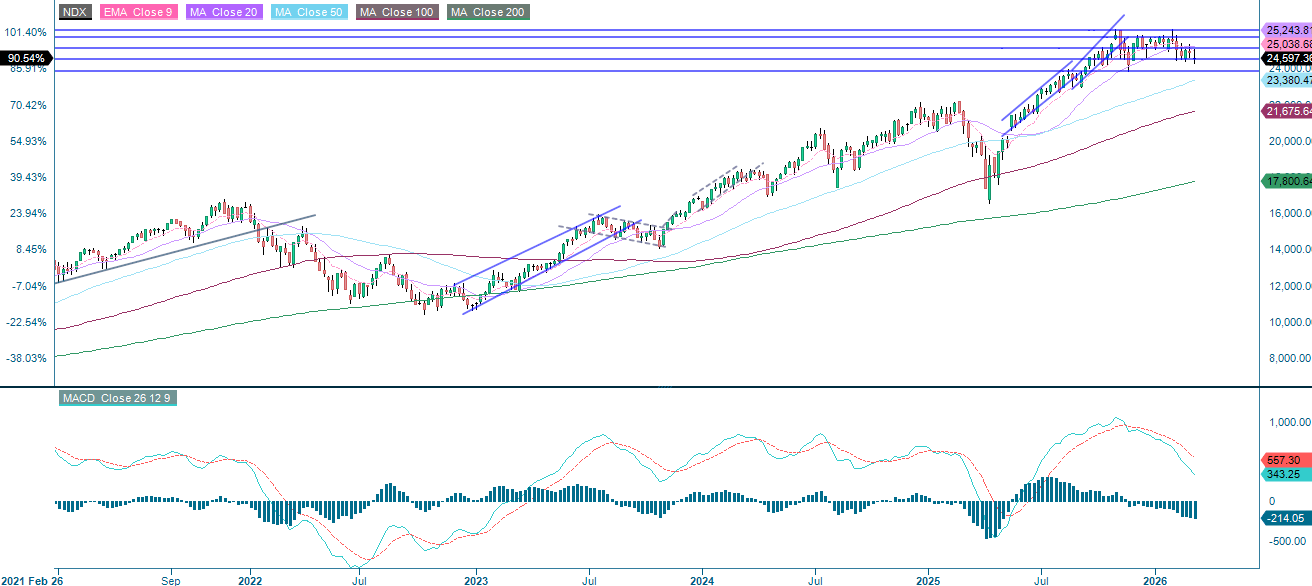

Like the S&P 500, the NASDAQ-100 is holding onto support at around 24,500. The next level to watch below that is the MA200 at 24,142, followed by the 23,900 area. On the upside, the first level of resistance sits around 25,150.

Related Products

NASDAQ-100 (in USD), one-year daily chart

NASDAQ-100 (in USD), five-year weekly chart

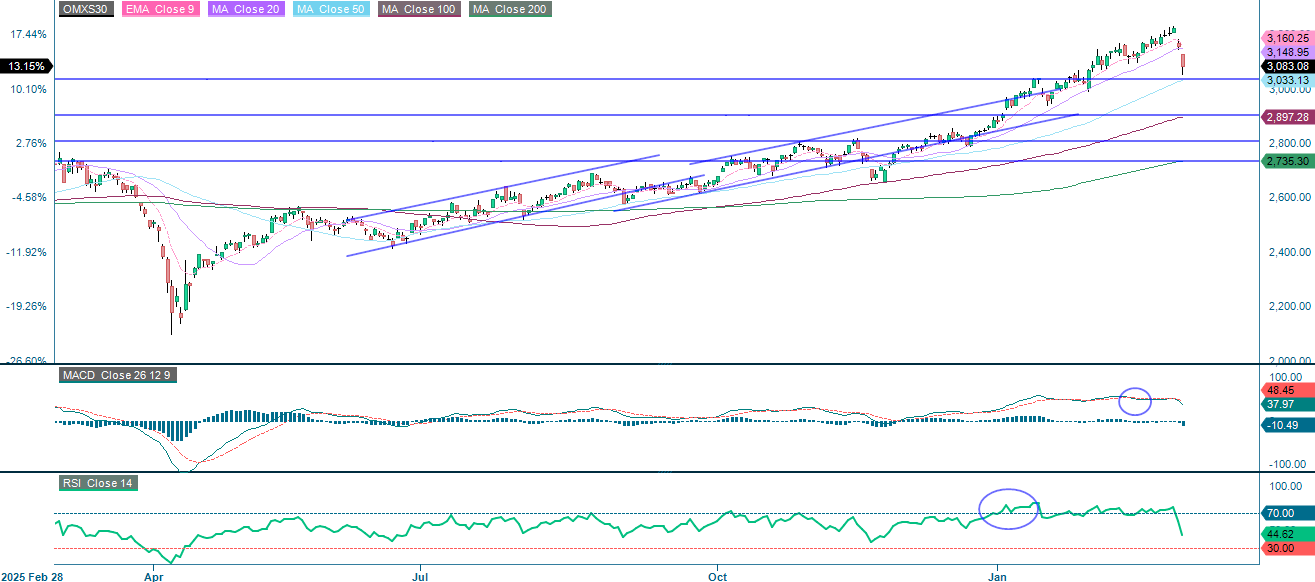

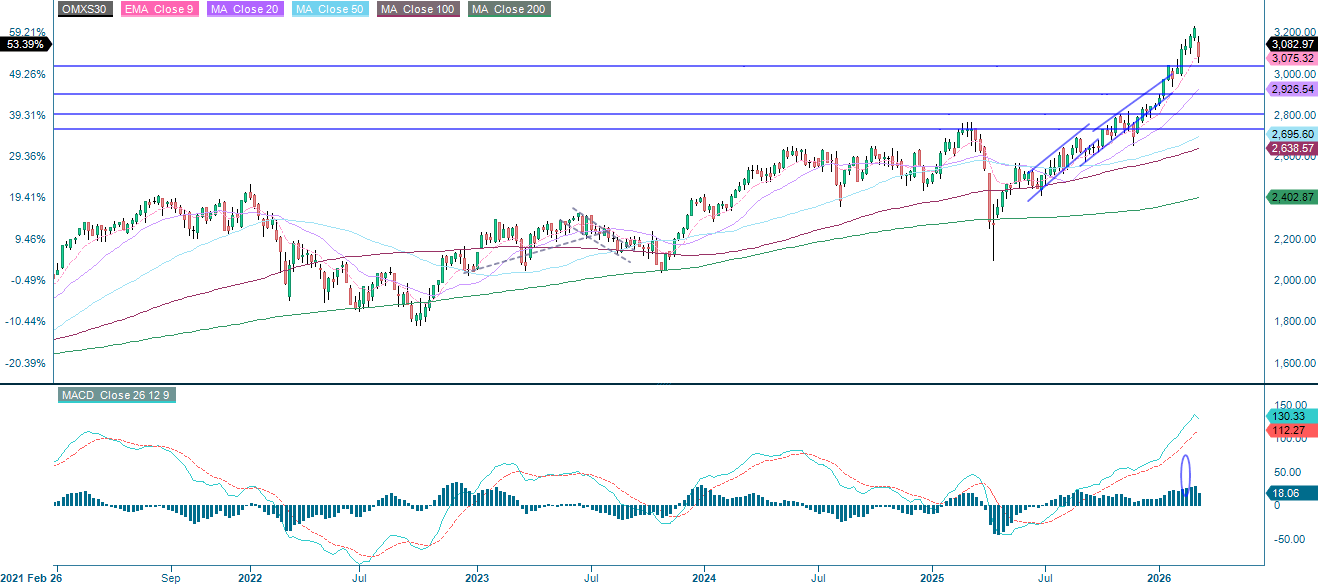

The spike in oil prices is a headwind for Swedish industrials, but the bigger issue is that the OMXS30 cannot escape the broader risk-off sentiment stemming from the conflict in Iran. Currently, the index is holding above support around 3,040. If it breaks below that level, 2,900 will come into play. On the upside, the first level of resistance is the MA20, which is currently at 3,148.

Related Products

OMX30 (in SEK), one-year daily chart

OMX30 (in SEK), five-year weekly chart

The DAX is not happy. It is trading below the MA200, which is currently at 24,175. Meanwhile, support is found at the level between 22,825 and 23,365.

Related Products

DAX (in EUR), one-year daily chart

DAX (in EUR), five-year weekly chart

The full name for abbreviations used in the previous text:

EMA 9: 9-Day Exponential Moving Average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-Day Moving Average

MA50: 50-Day Moving Average

MA100: 100-Day Moving Average

MA200: 200-Day Moving Average

MACD: Moving Average Convergence Divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.