Investors' Outlook: A bowl of tricky treats

While the course of monetary policy is being reset and geopolitical tensions continue, questions about growth, inflation and fiscal policy measures are coming into focus. The USA is also facing decisive decisions - from the development of the labor market to the role of the Federal Reserve. What could the outlook for the coming years look like and what developments are on the horizon?

Through the fog

October began with a shutdown of the US government - the twentieth since 1976. Thousands of federal employees were temporarily furloughed and key economic reports were suspended. The Bureau of Labor Statistics, the Bureau of Economic Analysis and the Census Bureau temporarily suspended data collection and publication, with some exceptions.

Market participants therefore turned to alternative sources of information to assess the state of the economy, with a mixed picture emerging. Private employment data from ADP indicated a loss of around 32,000 jobs in September, while credit card and other high-frequency spending data signaled a slowdown in consumer activity. Investors have apparently concluded that the previously hot labor market has cooled and companies are becoming more cautious about hiring, although broad-based layoffs are not yet reflected in the data.

The lack of official data did not stop the Fed from cutting interest rates in October, with monetary authorities expressing concern about the labor market. Opinions differ as to whether a further cut will take place this year. It remains to be seen whether the Fed will decide to cut interest rates again at its meeting on December 9 and 10.

By then, we will already be in the final sprint to the end of the year and the focus will be on 2026. What is the outlook for the multi-asset boutique? Given the prospect of accommodative monetary policy and growth-enhancing measures, the team remains confident about global growth. The team does not expect a repeat of the 2021 - 2022 rise in inflation. In addition, the team believes that US President Donald Trump is likely to have an interest in limiting uncertainty given the 2026 mid-term elections.

A year full of sweet and sour surprises lies behind us - and new ones are just around the corner

"Trick or treat?" - the classic Halloween slogan. But during US President Donald Trump's second term in office, it wasn't children in costumes knocking on doors - it was Trump himself. With his unpredictable trade and foreign policy, he kept the global markets on tenterhooks and unsettled investors with the uncertainty of what was to come next: sour grapes in the form of tariffs, sanctions or geopolitical tensions or sweet treats such as a surprising trade agreement or a stock market boom? In the spirit of Halloween, Trump occasionally handed out candy, giving investors moments of optimism and unexpected gains amidst the chaos.

Since his return to office at the end of January, Trump has pursued a determined agenda: far-reaching trade measures, an aggressive industrial policy, comprehensive deregulation and an expansion of executive power. The interplay of these initiatives has at times raised more questions than answers - for companies and investors as well as for the economy as a whole.

In the trade war, Trump's tariff offensive caused global supply chains to tremble. It led to concerns about rising input costs for companies and ultimately also for consumers. Trading partners threatened retaliatory tariffs and/or looked for new sales markets. Companies - especially those based in the USA - reacted in two ways: First, many stockpiled goods to forestall future tariffs, which significantly distorted several economic metrics - including global export data and US gross domestic product (GDP). Secondly, many companies postponed their investment and hiring plans.

This has also left its mark on the once red-hot US labor market. Although the unemployment rate remains at a historically low level of 4.3%, fewer jobs have been created in the private sector since the summer and the figure has even fallen into negative territory in some cases. The publication of a particularly weak monthly labor market report led to the dismissal of a high-ranking official at the Department of Labor and raised doubts about the reliability of US data. Despite a general slowdown, the labor market remains tight in certain sectors - particularly where migrant workers are in demand - largely due to Trump's restrictive immigration policies.

Trump's policies have also influenced the latest US inflation figures. After falling to 2.3 percent (year-on-year) in April, consumer prices have risen steadily since then, reaching 3.0 percent in September, with prices for goods and food rising particularly sharply. Despite Trump's claim that foreign exporters are bearing the costs of the trade war, inflation in other regions remains moderate - for example in the eurozone (+2.1% in October), China (-0.3% in September) and Switzerland (+0.1% in October).

In view of a weaker labor market, ongoing geopolitical tensions and stubbornly high prices, US consumers have become increasingly skeptical. The University of Michigan's consumer confidence index fell for the third month in a row in October, and the Conference Board's indicator showed a similarly subdued picture. This prompted lower and middle-income households in particular to reduce their spending. Even if this is not immediately visible in retail sales (not adjusted for inflation), the decline is more clearly reflected in the PCE index (Personal Consumption Expenditures), a key component of US GDP.

The combination of slowing growth, stubborn inflation and unclear visibility is making it more difficult for the Fed to cut interest rates. Despite public pressure from Trump to cut interest rates, Fed Chairman Jerome Powell pointed to economic policy uncertainties and inflation risks as reasons for restraint. The Fed therefore remained in a holding pattern for several months before finally resuming interest rate cuts in September. Meanwhile, other major central banks continued their rate cuts relatively unperturbed. Several members of the European Central Bank signaled that the easing cycle was "near or at its end" after eight rate cuts. The Swiss National Bank lowered its key interest rate to 0% and emphasized that the hurdle for the introduction of negative interest rates remains high.

Base scenario for 2026: More sour, but also more sweet

What can we expect in 2026 in terms of growth, inflation and monetary policy? The global growth outlook of the multi-asset boutique remains positive - for several reasons. Firstly, most central banks are still in a rate-cutting cycle rather than tightening mode. This includes the most influential of them all - the Fed - which still has considerable room to maneuver before it reaches a "neutral" interest rate level. According to the Fed's own forecasts, this is around 3%, which would require around four more interest rate cuts to reach this level. As monetary policy stimuli always have a delayed effect on the real economy, the positive effect of previous (and future) cuts is likely to continue well into 2026. A look at the loans and leases of US commercial banks shows that many have expanded their lending - spurred on by lower interest rates and the prospect of looser regulation after Fed member Michelle Bowman was appointed Vice Chair of Banking Supervision and signaled an overhaul of banking regulation.

In terms of fiscal policy, decision-makers around the world will probably be forced to take more growth-promoting measures - at least if they want to survive politically. The pressure to act is particularly great in Europe, as many governments are anything but popular (see chart below). According to estimates by the International Monetary Fund, budget deficits are likely to remain high in the coming year - and even increase in several countries (e.g. Germany, China and India).

In the US, on the other hand, Trump has good reasons to avoid a high level of uncertainty and ensure greater predictability. The upcoming midterm elections on November 3, 2026 will decide the majorities in Congress, where the Republicans currently only hold a narrow lead. As chart 2 shows, political uncertainty has always been at its lowest in previous midterm election years - unsurprisingly, as uncertainty is rarely an election helper. The upcoming review of the USMCA trade agreement (United States-Mexico-Canada Agreement) in July 2026 could also provide Trump with an opportunity to announce further "great" trade deals.

Last but not least, there is potential for higher productivity through the wider use of artificial intelligence (AI). The 1990s are an impressive reminder of how technological advances can boost economic growth without triggering severe inflation (see chart below). Back then, computers, the internet and digital tools boosted productivity across industries - with faster communication, more automation and greater efficiency. Thanks to higher productivity, companies were able to pay higher wages without raising prices.

What does the team expect for inflation? US consumers are likely to feel the impact of higher tariffs in 2026. So far, US companies have only passed on some of the additional costs to consumers - the team expects this effect to increase over the course of the year. In addition, a weaker US dollar is likely to cause import prices to rise. Nevertheless, the multi-asset boutique does not expect a surge in inflation like in 2021 - 2022. why? Firstly, the prices of goods make up a much smaller share of the US inflation basket than services. Secondly, tariffs act like a tax, reducing disposable income and dampening demand. Thirdly, the Fed is only likely to cut interest rates to a "neutral" level in the coming months - but the team does not expect an "accommodative" (i.e. stimulating) monetary policy. Although the US money supply is growing, it remains well below the levels that previously formed the basis for higher inflation (see chart below). Fourthly, employees are losing bargaining power in a weaker US labor market - which reduces the upward pressure on wages. Fifth, there are currently no significant supply bottlenecks or problems in the supply chains: The OPEC+ oil cartel continues to bring additional crude oil onto the market until the end of December, and rising OECD inventories are capping prices between USD 60 and 65 per barrel. In addition, China is likely to continue "exporting" deflation - as a result of massive overcapacity in electric vehicles and solar modules, for example. And finally, the growing use of AI could have a deflationary effect.

Risks for the outlook for 2026

As always, there are risks lurking in the shadows. One growth risk is - unsurprisingly - Trump himself. Although it would be rational to avoid uncertainty in an election year, it remains to be seen whether Trump shares this view. The US tariff rate - measured in terms of customs revenue in relation to imports of durable goods - is currently at a decade high of around 10%. Historically speaking, however, there is still room for improvement: In the first half of the 20th century, the tariff rate was around twice as high. The war between Russia and Ukraine remains a further risk. Even if a ceasefire is conceivable, the conflict could still escalate and trigger an oil price shock before any settlement is reached. Not forgetting the strained public finances of many countries: France is struggling with high deficits amid political deadlock and the USA with high debt and rising borrowing costs. Things could also get dicey legally if the Supreme Court were to declare Trump's trade war illegal. Several small businesses and Democratic-led states are challenging the import tariffs, arguing that they amount to a USD 3 trillion tax hike on the American people and exceed the president's powers. If the US government is forced to repay the tariff revenue, this could trigger a fiscal crisis. There is also the risk of a worsening credit crunch - most recently illustrated by the insolvencies of automotive supplier First Brands and lender Tricolor, which prompted JPMorgan CEO Jamie Dimon to warn that there could be "more cockroaches" hiding in the US economy.

One risk to the inflation outlook lies in the depreciation of the US dollar. The currency has already lost around 10 percent against a basket of major currencies in 2025, and many of Trump's measures - in particular a possible replacement of Fed Chairman Powell with an expansionary successor - could put additional pressure on the greenback. A significantly weaker dollar could further fuel imported inflation.

In the long term, however, US inflation expectations have moved away from the framework of Trump's first term in office. After peaking at over 3.5% during the inflation crisis of 2022 - 2023, they are now at a new, higher level. This is significant because rising inflation expectations can easily become a self-fulfilling prophecy: They shape consumer behavior and can thus continue to drive inflation. This leaves little room for political "tricks" without them quickly becoming a boomerang.

Sound trumps trend when the data goes silent

As the US government is currently not publishing any official economic data due to the shutdown, the markets are navigating without their usual compass. The flow of figures on employment, consumption, prices and production has dried up, replaced by sentiment indicators and anecdotal evidence. In this vacuum, tone beats trend. Investors take every speech by the Fed, every company announcement and every credit card indicator as a guide. Perception itself becomes a market force.

At its most recent meeting, the Fed lowered the key interest rate by 25 basis points to 4.0 percent. The move was expected, but Fed Chairman Jerome Powell emphasized that a further cut this year was not guaranteed. There were differing opinions in the committee: Powell spoke of significantly differing assessments of risks and the economic outlook. Powell referred to the difficulty of acting without complete data. "When you drive in fog, you drive slower," he said. Possibly an indication that the data freeze could influence the December meeting. The markets are already pricing in more rate cuts for the coming year than the Fed is currently signaling (see chart below), although the labor market data so far shows little sign of further weakening. Nevertheless, the team does not believe this is the right time to return to bearish positions: Sensitivity to credit quality and ongoing trade tensions remain high.

High-yield bonds: carry yes, buffer no

High-yield bonds continue to offer attractive current income (carry), but hardly any risk buffer. The credit premium is low. Yield premiums currently account for around 42% of the total return - compared to a long-term average of around 66%. A look at the chart below shows how the remuneration for credit risks has decreased significantly over the past ten years. Although total returns are close to their multi-year highs, a smaller and smaller proportion of these returns comes from yield premiums. In other words, investors are now receiving the risk-free rate rather than real compensation for credit risk. Even if overall returns therefore appear solid and the yield outlook acceptable, the margin of error is not sufficient according to Multi Asset Boutique. In their view, there is little buffer for weaker growth or an increase in defaults.

For the team, this is a carry without a safety net and they believe it is unlikely that yields will improve as spreads tighten. Overall, the team believes that the case for broadly diversified bond positions is currently weak. Selectivity therefore plays a crucial role. The team prefers issuers with solid quality, a sustainable structure and sufficient liquidity - this is where active management can develop its added value.

AI - investment boom or bubble?

Optimists and pessimists on the financial markets are currently discussing the rapid increase in AI investments, the high valuations of the companies concerned and the emerging closed ecosystem. Many are already wondering whether we are heading for the next big bubble.

In recent months, warnings of a potential AI bubble have been mounting - both from financial institutions and from executives at the forefront of this megatrend. While few doubt the long-term transformative potential of AI, many warn of potential setbacks along the way. These concerns arise against the backdrop of a seemingly unstoppable bull market in shares, driven primarily by a few large US technology companies in the AI sector with high valuations. Even the US government has acquired stakes in some of these companies, promoting projects such as "Stargate" and calling on the tech giants to invest billions in AI domestically. However, capital expenditure on data centers is only one side of the coin. Energy requirements are the other - and are increasingly becoming a crucial bottleneck. For example, the contracts recently signed by OpenAI, the owner of ChatGPT, include a commitment to purchase 17 gigawatts. This is roughly equivalent to the capacity of 17 nuclear power plants. This has raised fears that the combination of high valuations, circular investment flows and growing electricity consumption is creating a vicious circle that is growing ever larger - without it being clear yet how the companies actually intend to monetize the returns on these investments.

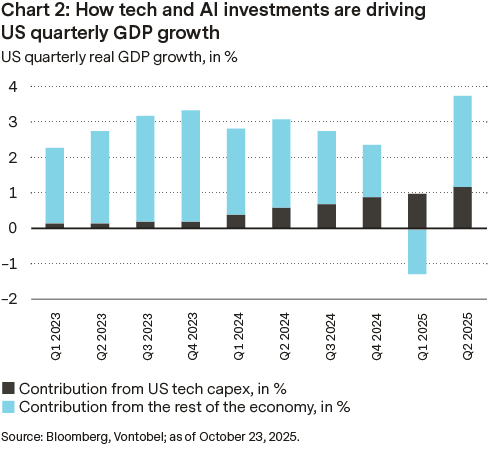

The impact of AI-related investments on real GDP growth in the US is already clear (see chart below). With annual GDP approaching USD 30 trillion, AI-related spending now contributes more than 1 percent of quarterly growth - or around a third of total growth. In other words, AI has become a key driver of growth in the US economy. But does this mean that a bubble has formed? The Multi Asset Boutique's multi-criteria analysis, which compares the current environment with previous bubbles, reveals a differentiated picture. Some signals point to increasing risks of overheating, while others highlight the differences to earlier speculative phases. Lower leverage, fewer unprofitable IPOs, more realistic relative valuations and strong earnings contributions from leading AI companies to the S&P 500 Index point to a more balanced, sustainable market environment - comparable to the early adoption phases of revolutionary technologies in the past. Although vigilance is required, the team believes that AI-related US technology stocks are not currently in a bubble - at least not yet.

Every sweetness has its acidity

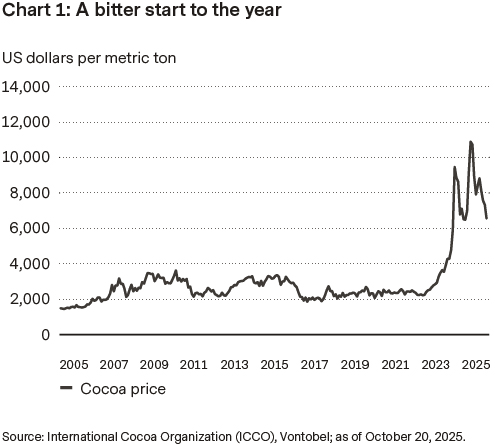

Once the star of rising commodity prices, cocoa prices have now come back down to earth - traders and producers are facing a market that has taken on a slightly bitter note instead of rich and creamy. For years, cocoa prices only seemed to go in one direction: up. Last year, prices for the small beans climbed to over USD 12,000 per tonne at times. However, as this article goes to press, cocoa prices are trading at around USD 6,000.

Several factors have contributed to this turnaround. Most importantly, the global supply outlook has improved after several seasons of weather-related shortfalls. In West Africa, where around 70% of the world's cocoa is grown, conditions have stabilized. Rainfall in the largest producer country, Côte d'Ivoire, has reduced supply pressure. The second-largest producer, Ghana, has brought forward its 2024 / 2025 harvest by two months - this has also alleviated concerns about shortages. The European Union is also planning another one-year postponement of its deforestation law.

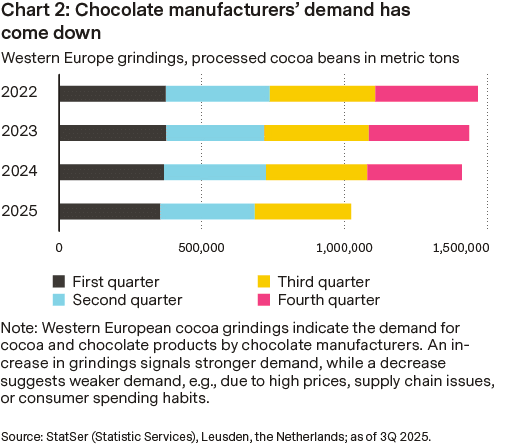

This delay should temporarily mitigate rising costs and production complexities, as Europe accounts for more than a third (36%) of global cocoa demand. At the same time, demand indicators have weakened (see chart below). Cocoa grindings - a key indicator of demand in the chocolate sector - fell by 4.8% in Europe and 3.4% in Asia in the third quarter compared to the previous year. As prices remain high by historical standards, manufacturers have restricted their purchases or adjusted their recipes, which has exerted additional downward pressure. Speculative positioning has also changed. Hedge funds and other investors, who had bet heavily on cocoa in 2024, began to rapidly liquidate their positions at the beginning of 2025 - which intensified the downward trend. The governments of the producing countries have since reacted to the changed market situation. In October, Côte d'Ivoire increased its producer price for the 2025 / 2026 main harvest to a record XOF 2800 per kilogram to support farmers. This could encourage farmers to bring more of their beans to market instead of holding them back to artificially drive up prices.

Since October, the cocoa market appears to be in a more stable phase with lower, less volatile prices. Although a renewed rise cannot be ruled out, for example in the event of weaker harvests or unexpectedly strong demand, the panic-driven highs of 2024 appear to be over. Market participants are now closely monitoring the grinding data for the fourth quarter and the results of the main West African harvest. Currently, the cocoa market seems to have settled into a more fundamentally driven trading environment.

No scary moments for the US dollar, the franc enchants

The US government shutdown that began on October 1 has so far had little immediate impact on the US dollar - similar to previous shutdowns, including that of 2018 - 2019, when the currency remained relatively stable.

US Treasury Secretary Scott Bessent warned that the shutdown could cost the economy USD 15 billion per week and reduce GDP growth by 0.1 to 0.2 percentage points per week. The Council of Economic Advisers also expects consumer spending to fall by USD 30 billion in the event of a month-long shutdown. The biggest impact will come from the lack of salary payments - especially for federal employees and contractors. While federal employees are generally compensated in arrears, this does not apply to contractors, which could increase the financial burden, dampen consumer spending and in turn impact indicators such as consumer confidence and retail sales. Despite these uncertainties, the US dollar index proved robust between October 1 and 23, gaining 1.3%.

Record gains for the Swiss franc

The Swiss franc is set for a record year in 2025. Its appeal is based on structural strengths such as solid public finances, moderate debt and consistent foreign trade surpluses - factors that should continue to put it in a better position than other G10 currencies. A look at the annual performance of the Swiss franc against the US dollar (CHF / USD) since 1971 shows: 1974 marked its strongest appreciation to date (see chart below). However, 2025 is already shaping up to be one of the most successful starts to a year in recent history, as the franc is noticeably gaining ground against the US dollar.

If this momentum continues, 2025 could be a year of potentially unprecedented gains for the Swiss franc. Ongoing global uncertainties, from trade disputes to geopolitical tensions, as well as Switzerland's robust economic fundamentals - low unemployment and political stability - further strengthen demand for the franc as a safe haven.

The attractiveness of the Swiss franc is likely to remain high, especially as structural factors such as sound public finances, stable debt dynamics and close trade and financial ties with other countries are becoming increasingly important for the G10 currencies. Currencies with a healthy budget situation, manageable debt and foreign trade surpluses are therefore likely to continue to outperform in the future.

Note: Past performance and estimates are not a reliable indicator of future results