The US dollar’s decline and the rising tide of de-dollarization

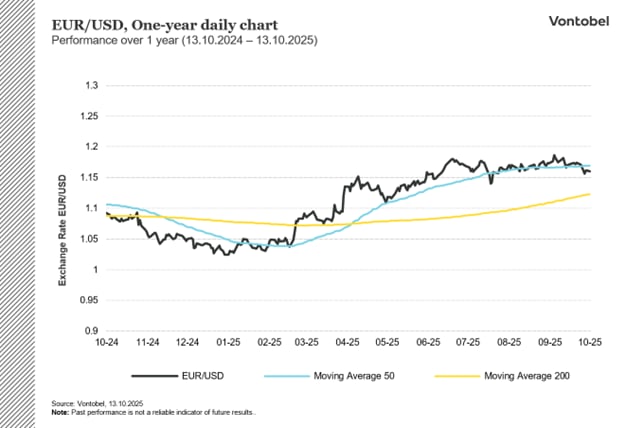

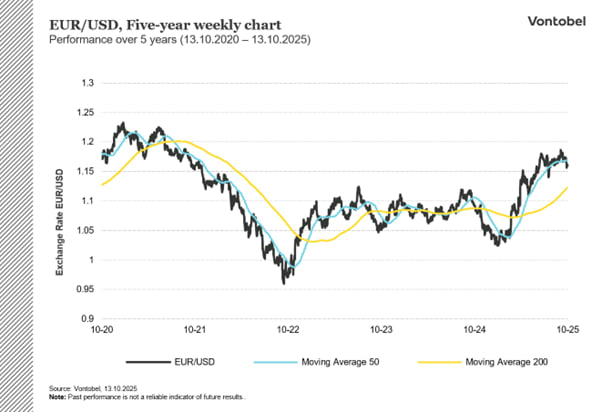

Since the start of 2025, the US dollar has steadily weakened against the euro. The EUR/USD currency pair has moved away from near parity to favor the euro significantly. In mid-January the EUR/USD exchange rate was about 1.03 (Yahoo Finance, 13.10.2025), whereas it is currently hovering around 1.16 (Yahoo Finance, 13.10.2025). The exchange rate has increased significantly since January, with the current rate being approximately 1.16 dollars for one euro. Against other major currencies the US dollar dropped about 11 % in the first half of the year (Morgan Stanley, 13.10.2025), the biggest decline in more than 50 years. What is the reason for this weakening of the US dollar?

The US dollar still holds status as the world's primary reserve currency. This was achieved after the Second World War through the Bretton Woods Agreement, and it continues to dominate the world today. In recent years the share of USD in official foreign exchange reserves in central banks around the world has dipped below prior peaks, even as total reserves rose. The dollar is still dominating in the total traded FX volumes. According to the Bank for International Settlements (BIS), in 2022, the US dollar accounted for 88 % of all traded FX volumes globally.

Even though the weakening of the US dollar started at the beginning of the year, the recent shutdown of the US government has increased uncertainty in the global markets. It has compounded fears about the US’ governance, fiscal discipline, and crisis management capacity. The reputational cost is real; policy reversals and unpredictable trade decisions all feed the narrative that the US might no longer offer the stability that was once taken for granted.

Related Products

At the same time a gradual shift is happening. Large commodity exporters and some BRICS nations are increasingly settling trades in local currencies instead of dollars. De-dollarization is also happening in the bond markets, where the share of foreign ownership in the US Treasury market has been declining over the last 15 years. Foreign central banks have reduced their holdings of US dollars and treasuries, in favor of gold, alternative currencies and digital assets. Today a large and growing proportion of energy is being priced in non-dollar-denominated contracts. Russian oil exported east, and south are sold in the local currencies of buyers, or in currencies of countries that Russia perceives as friendly.

Although the US dollar still holds a strong position in the global economy, it is facing growing challenges. While it is unlikely to lose its status as the world reserve currency overnight, its dominance is slowly eroding. The dollar is backed by deep financial markets, trusted institutions and high global demand. Most international trade, loans and investments are still done in dollars. However, there are also growing risks. The US government has a rising debt level, frequent political fights like the ongoing shutdown, and questions about long-term stability are being raised. The dollar is not disappearing, but its role is changing. To remain strong, the US will need to show it can manage its economy and politics more responsibly. If it doesn’t, the world may seek alternatives.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.