Uncertainty persists in equity markets

Coffee prices have stabilised at high levels since February 2025. Supply, which is expected to hit a three-year low this year, is pushing up prices, while tariffs between coffee-producing countries and the US and a strengthening of the Brazilian currency (Real) against the USD are likely to hamper and redirect exports. The situation in global equity markets remains uncertain, as can be seen from the technical analysis charts.

Case of the week: Opportunity during the coffee off-cycle

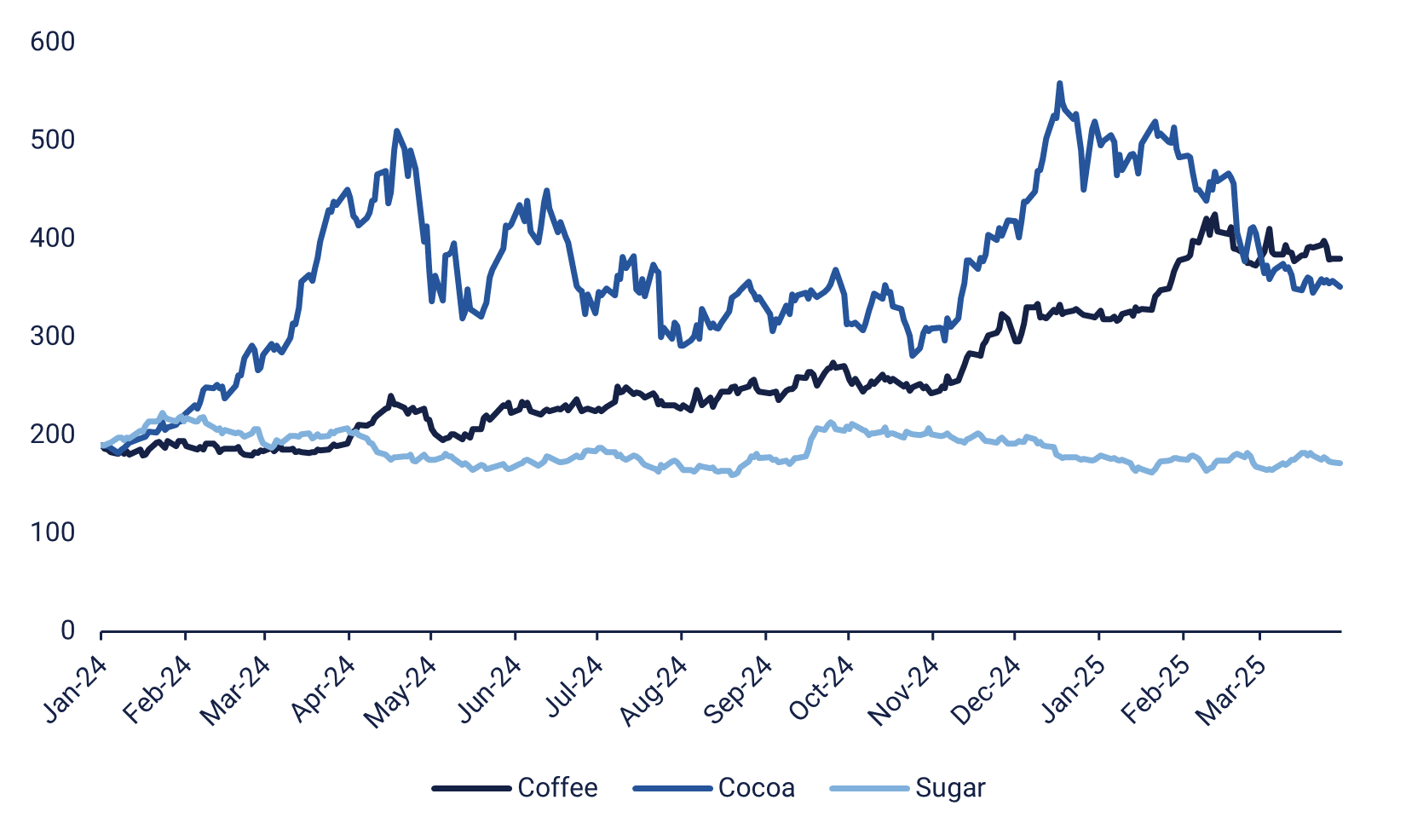

Coffee had a great 2024, with Arabica prices rising steadily throughout the year, with gains accelerating in the last two months. So far in 2025, futures prices have been largely flat as traders struggle to price in a turbulent USD and tariffs. Meanwhile, supplies are expected to remain below previous years, with government forecaster Conab estimating a 4.4% year-on-year decline in harvests to a three-year low of ~52 million bags. As the USD continues to fall, it is possible that exports will slow and Robusta will gain ground against Arabica.

Coffee compared to other softs (Indexed at 2024-01-02)

Cocoa was the main talking point in 2024, with gains far outstripping those of coffee. However, since peaking over the New Year, cocoa has fallen sharply, while coffee has traded sideways. Arabica coffee, mainly grown in Brazil, is currently in the rainy part of the season, with the main harvest expected to start in May. Coffee harvests follow a biennial pattern, with one year "outperforming" the second in terms of yield. This year, 2025, happens to be an out-year, which contributes to the lower expectations for the 2024/25 season. In addition to Conab, Cecafe reported that green coffee exports from Brazil fell 26% year-on-year in March 2025. In addition, Cooxupe, an Arabica cooperative, said that high temperatures and lower rainfall will negatively impact yields. Meanwhile, the USDA's (U.S. Department of Agriculture) biannual report on coffee prices predicts that Arabica production will increase by 1.5%, while ending stocks will fall by 6.6%. Taken together, from a purely supply and demand perspective, it would appear that coffee prices are set to rise. However, other factors exogenous to this perspective suggest otherwise.

Coffee seasonality (USD and %) 2010-2025 YTD

The USD has plummeted against most of the major currencies. At the time of writing, the USD has lost 6.6% YTD against the Brazilian real. This has significant implications for Brazilian exports, as the US is the main export destination for Arabica coffee. The loss is being offset to some extent by a strengthening Euro, which is helping exports to Germany, the second largest buyer of Arabica. In addition, President Trump increased tariffs on Brazil by 10%. This compares favourably with other major producers, namely Robusta giants Vietnam and Indonesia, which were hit with 46% and 32% respectively. However, the tariffs are on hold and being negotiated, so we can expect more turbulence in the coming months. This also means that while Robusta producers may have been nervous before, there is now hope that exports will continue. This has implications for Brazil, which produces Robusta as well as Arabica.

In summary, although the supply/demand equation for coffee in general is tight, it is reasonable to assume that exports of Robusta will be favoured over exports of Arabica. With prices already at all-time highs, it is unclear whether there is any further upside for coffee. Perhaps more likely is that trade and currency dynamics will keep a lid on prices over the coming months. A key turning point for traders will be the first crop reports in May, with yield data pointing the way for the rest of 2025.

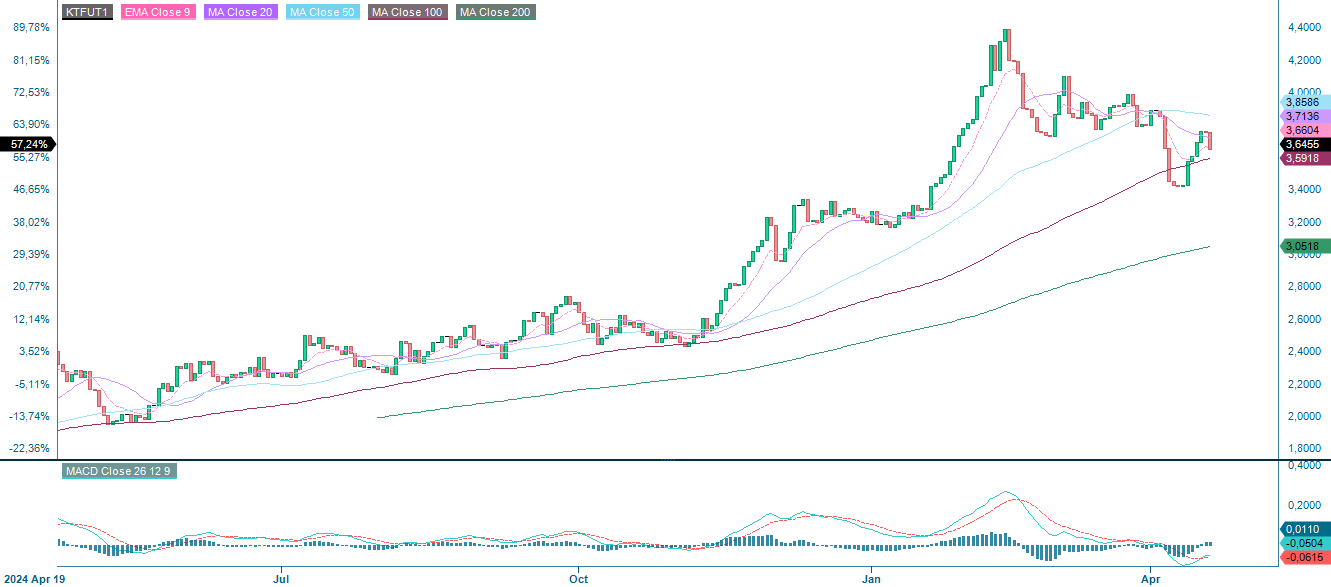

Coffee, July future (USD/Lbs), one-year daily chart

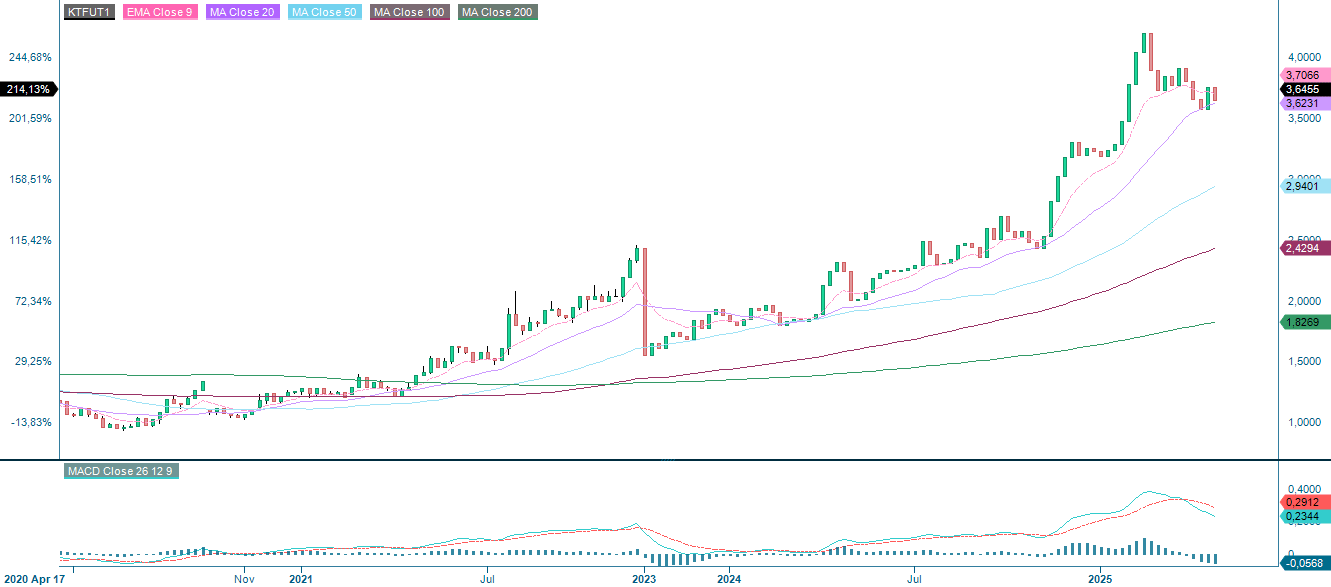

Coffee, July future (USD/Lbs), weekly five-year chart

Macro comments

For Q1 2025, with 12% of S&P500 companies reporting by 17 April 2025, 71% have reported positive EPS (Earnings per Share) surprises and 61% have reported positive revenue surprises. S&P500 earnings growth is expected to be 7.2% in Q1 2025. The forward P/E (Price to Earnings) is 19.0x, below the five-year average of 19.9x but above the ten-year average of 18.3x.

As of Tuesday 22 April 2025, eleven Swedish OMX companies with consensus expectations had reported their Q1 2025 results. In terms of both operating results and sales, 55% of these Q1 2025 reports were better than expected.

Today, Wednesday 23 April, Q1 2025 results from Tele2, Volvo, Coor, Boliden, Assa Abloy, Investor and Alleima on the Stockholm Stock Exchange and from Norske Skog, Orion and Valmet in the other Nordic countries are expected. Among the US companies reporting we find AT&T, Boeing, Boston Scientific, IBM, NextEra Energy, Philip Morris, Service Now, Thermo Fisher Scientific and Texas Instruments will be published. The macro news flow will be dominated by preliminary PMI (Purchasing Manager’s Index) figures for April from Japan, France, Germany, the Eurozone, the UK and the US. From the US, new home sales for March, the FED (Federal Reserve) Beige Book and weekly oil inventories (Department of Energy) are also due.

On Thursday, 24 April, there will be another round of interim reports with Axfood, Essity, Husqvarna, JM, Kinnevik, Nordnet, Telia, AAK and Trelleborg in Sweden, Huhtamäki, Konecranes, Metso, Nokia and UPM among the Finnish companies and Alphabet, Bristol Myers Squibb, Comcast, Gilead Sciences, Intel, Merck, PepsiCo, Procter & Gamble, TMobile US and Union Pacific in the US. We’ll also get key sentiment and activity data from Europe and the US. In Europe, April figures for the French Household Confidence Indicator, the German IFO Business Climate Index (Institut für Wirtschaftsforschung) and the UK Confederation of British Industry (CBI) Industrial Trends Survey will be released. From the US, we’ll see March data for Durable Goods Orders, the Chicago Fed National Activity Index, and Existing Home Sales, along with the latest weekly jobless claims and the Kansas City Fed Manufacturing Index for April.

On Friday 25 April 2025 interim reports from Gränges, Indutrade, Lifco, Saab, SKF, SCA, Hemnet and Hexpol in Sweden, from Stora Enso, Kemira and Wärtsilä in Finland, from Yara and Salmar in Norway and from Abbvie and Colgate Palmolive in the US will follow. France will provide with industry expectations in April, while the US will contribute with the Michigan index in April.

S&P500 earnings growth (Year over Year) Q1 2025

Still high uncertainty

The S&P is currently bouncing off support at 5,120. The declining EMA9 at 5,280 acts as the first level of resistance on the upside, followed by 5,400 where the MA20 meets. Uncertainty remains high.

Related Products

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), weekly five-year chart

The NASDAQ is still trading below the EMA9 at 18,310 which acts as the first level of resistance. A break below support at 17,850 and 17,000 could be next.

Related Products

NASDAQ-100 (in USD), one-year daily chart

NASDAQ-100 (in USD), weekly five-year chart

The OMXS30 is currently trading just above support at 2,345, supported by the rising EMA9. However, it remains capped below resistance at the 2,400 level. With momentum starting to fade, the near-term risk appears to be tilted to the downside. Should the index break lower, the next support levels are around 2,275, followed by 2,200.

Related Products

OMXS30 (in SEK), one-year daily chart

OMXS30 (in SEK), weekly five-year chart

The German DAX tested resistance made up by MA100, but failed and is currently trading just above EMA9, currently at 21,056, serving as first level of support. A break on the downside and MA200, currently just above 20,000 may be next.

DAX (in EUR), one-year daily chart

DAX (in EUR), weekly five-year chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.