The market trusts Warsh but households hesitate

Over the past four months, the American rates market has undergone a complete change of course. In early March, the futures market expected the Federal Reserve to cut rates by around 50 basis points in 2026. By early July, however, the market was pricing in rate hikes instead. This reversal is due to a stronger-than expected American economy, upgraded earnings forecasts in the semiconductor sector, and a new Fed chairman who has made fighting inflation his top priority.

Kevin Warsh has quickly convinced the market of his seriousness. At his first monetary policy meeting in June, he repeatedly emphasized to the central bank's commitment to bringing inflation back to the 2 percent target. Since then, the market's inflation expectations have since fallen below the levels that prevailed before the war between the United States and Iran. The sharp drop in oil prices has contributed to this, but the decline also reflects confidence that the new Fed leadership takes price stability seriously (Bloomberg). At the same time, many speculative investors have positioned themselves for higher US short-term rates (CFTC).

Over the past week, however, the tone has shifted. At the ECB's conference in Sintra, Warsh adopted a softer tone than at his debut and noted that inflation risks have decreased over the past month. The following day, the June jobs report came in well below expectations. Employment rose by just 57,000, compared to an expected figure of just over 110,000, and figures for previous months were revised down (BLS). Consequently, the market is therefore no longer pricing an October rate hike as certain, although at least one rate hike this year is still anticipated.

The market believes in disinflation

The jobs report reveals important about how the market views inflation. If a central bank that stays on hold while core inflation remains above 3 percent, it is taking a risk. If price increases prove to be more persistent than expected, the Fed may have to raise interest rates considerably later on. Therefore, the market could have interpreted the weak report as a reason to demand higher compensation for future inflation. This did not happen. Inflation expectations were largely unchanged after the report, showing that the still expects inflation to return to target.

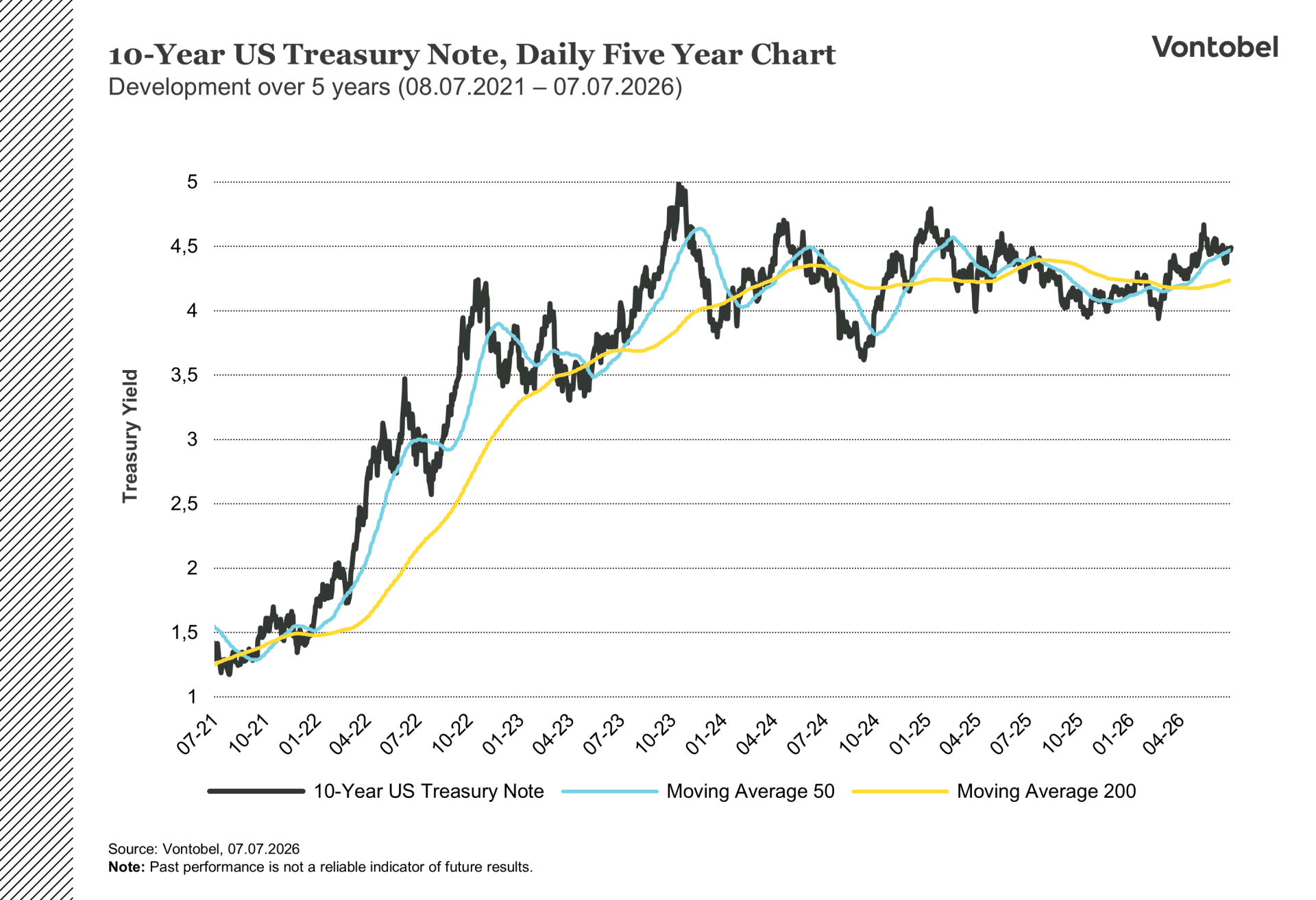

The next test comes on July 14, when the CPI for June is published. The Cleveland Fed's forecasting model points to a slightly negative monthly reading, which would confirm that this spring's energy-driven rise in prices was temporary rather than the beginning of a larger trend (Cleveland Fed). If the figure is as expected, today's ten-year yield of 4.5 percent looks like an attractive level for those who want to extend duration. Moreover, Warsh has never explicitly stated that price stability requires higher interest rates. He has described the rate path as written in pencil, and the five task forces he has set up to review the Fed's analytical work will deliver their conclusions until the end of the year. Until then, the committee can wait and let the temporary energy effects fall out of the inflation figures on their own.

Households still see high inflation

However, there is one group that does not share the market's confidence in the new Fed chairman, namely American households. According to so-called inflation swaps, inflation over the next year is priced at around 2.2 percent in the market. Meanwhile, the N2wew York Fed's household survey meanwhile sits just below 3.5 percent (Bloomberg). This gap is unusually wide, and history does not favor the market. Over the time, household expectations have over time tracked actual inflation more accurately than market pricing, which on several occasions in recent years has priced in a decline in inflation that never materialised.

There is also a structural problem. Some prices, such as hotel rooms and restaurant meals, fall when interest rates rise because demand cools. Others, such as healthcare and insurance, are barely affected by the level of interest rates. According to the San Francisco Fed, it is precisely the rate-sensitive prices that have already slowed, while the insensitive ones continue to rise. In other words, higher rates would hit the wrong part of inflation. If households are correct, this summer's bond rally may prove premature, and a central bank that waits too long may have to raise rates considerably once it finally acts.

For investors who want to take a position in the rates market, Vontobel offers leverage products with US Treasury futures as the underlying asset. Those who believe the peak in rates has passed can increase their exposure to rising bond prices, while those who believe households are right about inflation can position for the opposite.

Related Products

10-Year US Treasury Note, Daily One Year Chart

10-Year US Treasury Note, Daily Five Year Chart

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.