Investors' Outlook: And now for something completely different

The war in the Middle East has reverberated across economies around the world, disrupting trade, fanning inflation, and forcing central banks to reconsider their plans. But after more than 100 days of conflict, the US and Iran have signed a memorandum of understanding.

Just in time

Under the preliminary agreement, Iran reopened the Strait of Hormuz to commercial shipping, while the US lifted its naval blockade of Persian Gulf ports. Iran will also regain access to frozen assets and receive temporary relief from oil and banking sanctions. This came just in time, as the conflict has contributed to rising inflation and production costs across major economies and eroded consumers’ purchasing power. In May, US consumer price inflation hit 4.2 percent, more than double the Fed’s target, and the Fed has hit pause on what had previously been a path to rate cuts.

Even so, the global economy is likely in sufficiently strong shape to absorb these headwinds. That’s because on the one hand, the US labor market has started to show signs of reacceleration, and on the other, the combination of US President Donald Trump’s “One Big Beautiful Bill Act,” lower tariffs, and the positive impact of AI-related capex are poised to provide additional tailwinds. With US midterm elections approaching, Trump has an incentive to take a more pragmatic course. The US-Iran deal is also likely to ease one of the main drivers of recent inflation, namely energy inflation. With the reopening of the strait, Gulf producers that were unable to export oil during the conflict are likely to bring supply back to market. That’s on top of the impetus the war has given to efforts to boost renewable energy, which could point to lower oil prices. That’s why central banks are unlikely to tighten policy as aggressively as some may fear.

Maintaining a stiff upper lip has been particularly challeng-ing for UK government bondholders.

Will the UK’s stiff upper lip start to tremble?

A sell-off in gilts has pushed yields on 10-year bonds close to 5 percent, while 30-year yields have approached 6 percent (bond yields move inversely to prices). The sell-off reflects a combination of short- and long-term factors. One of the UK’s most immediate vulnerabilities is its sensitivity to international energy markets.

As a significant net energy importer, the country relies on overseas supplies for more than 43 percent of its total primary energy consumption, with oil and gas accounting for over 90 percent of imports. Unlike some continental European peers, the UK has relatively limited gas storage capacity, leaving it exposed to swings in global wholesale prices. When disruptions in the Strait of Hormuz pushed oil and gas prices higher, the impact was almost immediately felt across the British economy. Higher energy costs squeezed households’ budgets and eroded disposable income, and businesses were forced to prioritize liquidity and cost management over investment and expansion.

The surge in energy prices has also fanned fears that the disinflationary trend that had been underway before the war has come to an end. UK consumer price inflation had moderated from around 11 percent in 2022 to roughly 3 percent before the outbreak of the war and was projected to eventually fall back toward the Bank of England’s (BoE) 2 percent target. The BoE now expects inflation to remain a little under 3 percent in the third quarter before rising to just over 3.25 percent toward the end of 2026, reflecting lower energy prices (though with the earlier shock still feeding through). All of this has complicated the BoE’s rate-cut plans. Before the war, markets expected its main interest rate to move lower from 3.75 percent. Instead, the BoE has kept rates steady, while flagging that upside risks to inflation persist. Although policymakers continue to expect inflation to ease over the medium term, they have stressed that policy will need to stay restrictive enough for long enough to return inflation sustainably to the 2 percent target.

Domestic demand remains the economy’s weakest link. Stagnant real (inflation-adjusted) wages have eroded consumer spending power for several quarters, leaving very little room for discretionary expenditure. This pain is also showing up in forward-looking business surveys. According to the Confederation of British Industry, sentiment among UK manufacturers has deteriorated sharply, with optimism about both the business outlook and export prospects falling at their fastest pace since the Covid-19 pandemic. The picture is not much prettier in the services sector: sentiment among consumer-facing businesses has fallen to its lowest level in more than a year, while profitability is declining at the fastest pace since 2020 as costs rose faster than companies were able to raise prices.

The corporate sector offers little reason for optimism. Insolvencies have been elevated for the fourth year in a row.

This trend is driven by a combination of high interest rates, rising business rates, and increased labor costs, including adjustments to the national minimum wage. Smaller enterprises, which generally lack the financial buffers and restructuring options available to larger corporations, are bearing the brunt of this environment.

Beyond these shorter-term headwinds, deeper structural forces are also at play. Like many advanced economies, public spending has seen a steady increase since the departure of Margaret Thatcher.

However, much of this rise has been absorbed by demographic pressures, especially an aging population, as well as higher spending on pensions, healthcare, and debt servicing. That has left less room to improve service quality elsewhere. Combined with weak productivity growth and the legacy of earlier spending constraints, many public services are under pressure despite higher aggregate outlays.

In addition, the UK’s decision to withdraw from the European Union (Brexit) has added a further structural drag because it increased trade frictions, reduced labor mobility, and dampened investment, which has weighed on openness and lowered the economy’s long-term growth potential.

Then there is also the politically sensitive issue of immigration. Migration to the UK looks very different today than it did before Brexit.

Although reducing numbers was one of the stated goals, both the scale and composition of arrivals have changed, moving from a predominantly European labor force to one increasingly driven by non-EU workers, students, and humanitarian routes. Restricting the labor supply is easier said than done as it risks stifling growth and fueling wage inflation, while failing to address public concerns risks deeper political instability.

Compounding these structural challenges is a volatile political landscape that has repeatedly undermined investor confidence. Investors haven’t forgotten the turmoil that accompanied Liz Truss’s brief premiership, particularly the gilt market sell-off triggered by the September 2022 mini-budget. Although her successor, Rishi Sunak, helped stabilize the economy, the Conservative Party remained divided by infighting between right-wing populists and moderates, high-profile scandals, and a public weary of the high cost of living.

By the summer of 2024, this desire for change culminated in a historic general election. Keir Starmer led the center-left Labour Party to a sweeping victory, ending 14 years of Conservative rule on a promise of stability and reform. However, while Labour won a massive majority of seats, the election also signaled a fragmenting electorate. The Liberal Democrats made a significant comeback, the Green Party gained ground, and Nigel Farage’s right-wing populist Reform UK party won millions of votes, fracturing the traditional right-wing voting base.

Key Questions for Investors

For domestic and global investors, the UK’s macroeconomic outlook raises questions around governance, debt sustainability, and systemic risk.

First, is the UK heading for a recession? The answer is finely balanced. With the Sahm Rule approaching danger thresholds, consumer confidence at multi-year lows, and manufacturing contracting sharply, it’s difficult to identify where growth will come from. If the BoE is compelled to raise rates to 4 percent or higher this summer to counter imported energy inflation, a technical recession before year-end becomes increasingly likely.

Second, will there be a second wave of inflation? The risk is elevated, but not inevitable. As a net energy importer, the UK is particularly exposed to renewed inflationary pressures if global supply chains remain disrupted. That said, a key difference from the 2021 – 2022 inflation shock is that labor shortages are less acute than in the aftermath of the pandemic, which is poised to reduce the risk of a wage-price spiral.

Third, could the UK government collapse? This is a fair question following Keir Starmer’s resignation on June 22, which marks yet another prime ministerial departure. Prime ministers may change, but the governing party is likely to remain in power. Under the UK’s parliamentary system, governments typically fall only if they lose their majority or fail a formal vote of no confidence. The Labour Party secured 411 of the 650 seats in the 2024 general election and, despite some attrition, still held 403 seats as of April 2026, so the government still maintains a solid working majority through to 2029. That said, political stability is far from assured. Starmer’s departure comes on the heels of a prolonged cost-of-living crisis, a series of unpopular policy decisions, and significant losses in recent local elections, all of which have left the ruling party deeply fragmented. With high-profile cabinet resignations and intense pressure from backbench members of parliament ultimately triggering this leadership transition, the next prime minister faces the immediate challenge of uniting a heavily fractured party.

Fourth, is the UK at risk of an imminent fiscal crisis? That’s rather unlikely. A key positive for sovereign credit-worthiness is the government’s clear prioritization of fiscal discipline over populist spending. Unlike during the 2022 mini-budget episode, the current leadership appears acutely aware of the risks of unsettling bond markets. High public debt and a stringent deficit-reduction strategy have resulted in restrained spending and continued freezes to personal tax thresholds. While this fiscal drag weighs on growth and household consumption, it also reduces the risk of a full-scale sovereign debt crisis.

Fifth, are there systemic contagion risks for international markets? The risks appear largely contained within the UK. The extent of contagion depends heavily on who owns the sovereign debt. Unlike certain Eurozone economies that rely on volatile foreign capital flows, the UK benefits from a deep and relatively captive domestic investor base. Pension funds and insurance companies hold a significant share of long-dated gilts to match their long-term liabilities, providing a stabilizing force in the market.

However, this domestic concentration is a double-edged sword: while it reduces the risk of sudden capital flight, it also means that sovereign stress is transmitted directly into the balance sheets of domestic institutions and, ultimately, the broader British public’s savings.

At the end of the day, if markets come under severe strain, there is a high likelihood that, when the burden becomes too heavy, the BoE is likely to step in to make sure bond investors aren’t whistling on their own Calvary Hill for long.

Watching the undercurrent

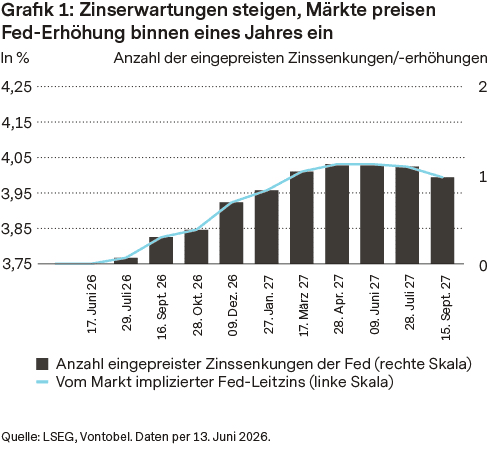

The Fed delivered a hawkish hold at its June meeting, indicating that inflation risks outweigh concerns about slowing growth and leaving the door open to further tightening if needed.

The message that caught attention was not the decision to leave rates unchanged, but the Fed’s more hawkish assessment of inflation. Updated projections suggest a growing number of policymakers believe price pressures could stay above target for longer, with additional tightening no longer off the table. Fed Chair Kevin Warsh stressed that price stability is the central bank’s primary objective. While lower energy prices may provide some respite, policymakers seem to be growing more concerned that inflationary pressures could become more entrenched across the economy. For bond markets, the implications are most significant at the front end of the yield curve. Expectations for looser policy have all but dis-appeared, leaving short-dated yields vulnerable if inflation continues to surprise on the upside. Further out on the curve, slower growth may provide some support, but inflation risks and large fiscal deficits are likely to limit how far long-term yields can decline.

Warsh provided little guidance on the future path of rates, emphasizing flexibility in an uncertain environment. He also signaled a review of the Fed’s forecasting, communication, and policy framework, pointing to a potentially more activist central bank in the years ahead. Money mar-kets still assign some probability to additional tightening.

Credit markets tell a different story. Despite higher inflation, geopolitical uncertainty, and record levels of corporate bond issuance, spreads are still hovering near historically tight levels. Investor demand has consistently exceeded supply, allowing issuers to raise large amounts of capital without offering meaningful concessions. This year has been a case in point. Issuance has already surpassed last year’s elevated pace, driven in part by hyperscalers and other technology companies funding AI-related investment programs. Yet demand remains exceptionally strong and continues to absorb new supply with ease.

Strong technicals therefore continue to be a key source of support. However, valuations leave little room for disappointment. With spreads already near cycle lows, future returns are increasingly likely to come from carry rather than further spread compression, leaving investors with limited compensation for macroeconomic, geopolitical, and supply-related risks.

Mega-IPOs, a warning sign for equity markets?

A historic wave of mega-IPOs is sweeping through markets in 2026. Tied to AI and frontier technology, this surge has become one of the main talking points for investors. Giants like Anthropic, said to be mapping out a debut for later this year, and OpenAI, now reportedly eyeing 2027, are widely expected to follow what has already become a milestone: the public debut of SpaceX. Together, these listings are set to form one of the largest issuance cycles in modern financial history.

SpaceX raised USD 75 billion in early June at a valuation of USD 1.77 trillion, completing the largest IPO valuation on record and making Elon Musk the world’s first trillionaire.

With AI titans like Anthropic and OpenAI preparing their own trillion-dollar public debuts in 2026 or 2027, fears have crept in that this deluge of issuance, alongside capital raises from companies such as Alphabet and Meta, could overwhelm market demand and drag down stock prices across the board. However, the risk of a market crash due to this supply alone is probably overblown.

These companies are floating only around 5 percent of their total shares, limiting the amount of stock initially released to the public. In total, the volume of new equity expected to come to market this year amounts to about 1 percent of overall market capitalization, well below historical averages.

If immediate supply is not the main risk, attention may instead turn to what follows. While newly listed companies have historically had strong market debuts, their shares have typically underperformed the broader market over the following three years. One reason is that companies deliberately choose to go public when private-market enthusiasm is at its strongest and growth expectations are highly optimistic. Once public discipline forces more transparency, valuations have historically compressed. The SpaceX debut may be exemplifying this.

While the offering’s two-times oversubscription and post-listing peak showed that market appetite for structural growth and AI remains fierce, the stock has now retreated from its initial highs.

Skeptics also argue that high-profile listings tend to precede market downturns. Examples include Ford in the 1950s, Apple in the late 1970s, Goldman Sachs in 1999, and the SPAC boom in 2021. But the notion that every large IPO signals a market peak may be a stretch born of selective memory. For instance, when Google and Facebook went public, no corrections ensued. IPO activity actually tends to mirror market sentiment. If history is any guide, downturns are triggered by the conditions that follow, such as a sharp tightening in financial conditions.

When El Niño plays tricks

Anyone who’s ever raised a young child recognizes the signs: they’re quiet for a moment too long, a little too innocent, and you realize they’re already up to something, testing limits. Out in the Pacific, a familiar trouble-maker is beginning to stir again. El Niño, with its warm ocean currents and knack for bending weather patterns out of shape, is making its way back onto the stage. And much like that spirited child, it rarely arrives without shaking things up.

El Niño (“the boy”) and La Niña (“the girl”) are two siblings within the same climate cycle (ENSO: El Niño–Southern Oscillation), but with very different temperaments. El Niño is the warmer, more unpredictable of the two. During an El Niño event, the water-surface temperatures in the central and eastern Pacific rise above normal, weakening the trade winds that typically push warm water westward. El Niño is associated with temperature anomalies of at least 0.5°C above average, while La Niña is associated with anomalies of at least 0.5°C below average.

In the El Niño case, warm water spreads eastward, dragging rainfall patterns with it. Regions like Indonesia, Australia, and parts of India, which usually depend on steady tropical rains, can face unwelcome dryness, while the western coasts of the Americas tend to become wetter. Some of the earliest signs of El Niño are usually felt in these regions. The result is a reshuffling of agricultural conditions worldwide: fields that depend on regular moisture may wither, while others contend with floods at the worst possible time. La Niña pushes in the opposite direction. Trade winds strengthen, driving warm waters farther west and allowing colder water to rise in the eastern Pacific. This intensifies existing weather patterns: the western Pacific becomes wetter, often to the point of flooding, while parts of the Americas turn drier and cooler.

According to the US Climate Prediction Center, El Niño is likely to emerge soon (97 percent probability between May and July) and is expected to last through the Northern Hemisphere winter of 2026 – 27 (99 percent probability for December to February). Even more concerning for commodity markets is how strong it becomes. In its June report, the National Oceanic and Atmospheric Administration (NOAA) raised the probability of a strong or very strong event—often dubbed a “super El Niño”—to 89 percent, threatening to disrupt global weather patterns on a scale not seen in years.

From ocean heat to economic uncertainty

Historical evidence suggests that global agricultural supply is often more resilient than initially feared. Production losses in drought-affected regions have frequently been offset by gains elsewhere, resulting in only a limited aggregate supply shock. This has meant that even strong El Niño events have not always translated into broad-based food price inflation.

However, there is a caveat: concentration. Certain commodities are geographically clustered in regions that are systematically exposed to El Niño-induced weather patterns. In these cases, localized climate stress can turn into a global supply risk. This is particularly evident in agricultural commodities. Palm oil production, for exam-ple, is heavily concentrated in Southeast Asia, a region that typically experiences drier conditions during El Niño episodes. A strong event can hence translate directly into tighter supply conditions and upward price pressure. Tighter palm oil production then spills over into higher prices for other vegetable oils like soybean oil or canola oil and can even impact imports for used cooking oil.

Similar dynamics apply, albeit to varying degrees, to sugar, coffee, and cocoa, where both yield sensitivity and regional concentration increase exposure to adverse weather shocks. All three markets are heavily concentrated geographically and have proven vulnerable supply chains in the recent past, leading to price volatility. Vietnam, the world’s biggest producer of Robusta coffee, and Brazil, a major producer of sugar, Arabica coffee, soybeans, and corn, are both facing drier weather patterns in the second half of this year. A super El Niño event can also bring drier weather conditions across the Atlantic to West Africa, the world’s most important cocoa-producing region. Grains such as rice and wheat can also be affected. Here, the risk often stems not from physical shortages but from behavioral and policy responses. Governments may act preemptively to secure domestic supplies and even restrict exports, which then amplifies price movements well beyond what underlying fundamentals would justify.

And beyond agriculture?

Beyond agriculture, El Niño also influences energy demand, infrastructure stress, and trade dynamics. Higher temperatures tend to increase electricity consumption, particularly in rapidly urbanizing regions where cooling demand is rising structurally. At the same time, droughts can reduce hydropower generation, while flooding can impact logistics, tightening energy balances.

Another important channel is hurricane activity. El Niño is generally associated with fewer Atlantic hurricanes, as stronger wind shear suppresses storm formation, while bringing above-average activity in parts of the Pacific. Forecasts for 2026 point to a quieter hurricane season along the US Gulf Coast. This is relevant because a large share of US liquefied natural gas capacity is concentrated in the region and is therefore exposed to episodic disruptions.

Unwelcome weather meets stressed supply chains

Another, less visible transmission channel runs through global trade. El Niño-driven changes in rainfall patterns can affect key transit routes such as the Panama Canal, where water levels directly constrain shipping capacity. Reduced rainfall can limit cargo loads and transit volumes, creating bottlenecks that ripple across supply chains. In a world already grappling with tight inventories and geopolitical fragmentation, such disruptions can add to cost pressures and extend lead times across industries. In practical terms, El Niño tends to progress through a sequence of market phases. First comes rising confidence in forecasts and early positioning, often in commodity and volatility markets. Next comes a realization phase, when weather impacts either validate or challenge expectations, driving spot price adjustments. The final stage encompasses broader economic consequences and policy responses, inflation pass-through, and potential second-round effects on growth and financial condi-tions. Ultimately, El Niño acts like a stress test for the global system.

Short-term noise vs. long-term trends

Currency markets are caught between short-term geopolitical developments and longer-term structural trends. Recent market volatility has lent support to defensive currencies such as the US dollar and Swiss franc, but underlying factors, including fiscal imbalances, capital flows, and relative economic fundamentals, will likely become increasingly important.

Recent market turbulence has temporarily strengthened the US dollar, reflecting its traditional safe-haven status and the relative resilience of the US economy. However, these factors are unlikely to change the broader trend. Ongoing concerns about the US fiscal outlook, rising debt levels, and the gradual diversification of global portfolios away from US assets are poised to be a source of pressure over the longer term. The dollar’s recent rebound therefore seems more like a pause in its decline, rather than the start of sustained appreciation.

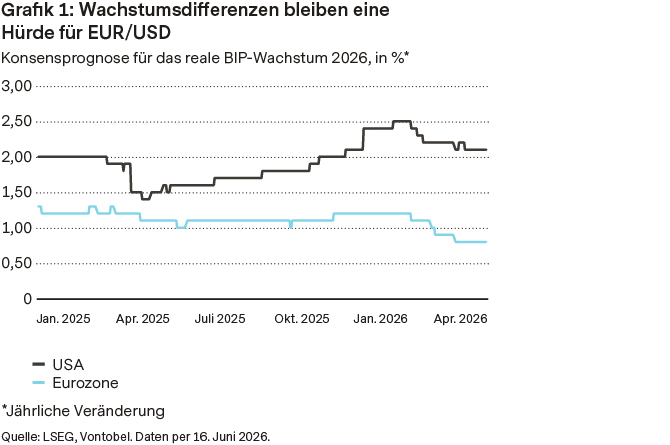

The euro’s short-term prospects remain mixed. The ECB’s recent rate hike initially supported the currency, but markets have since scaled back expectations for further tightening as oil prices retreated and fears of a prolonged energy shock eased. Relative growth dynamics also con-tinue to favor the US, limiting the euro’s scope for a strong move higher against the dollar. A more durable appreciation is likely to require stronger growth momentum in the euro area.

The medium- to longer-term outlook appears more constructive. The euro area benefits from a sizeable current-account surplus, improving capital flows, and a stronger external position than the US, and growing concerns about US fiscal sustainability may encourage a gradual reallocation of global capital toward other markets, including Europe. While these factors are unlikely to trigger a rapid appreciation, they could provide a supportive backdrop for the euro over time.

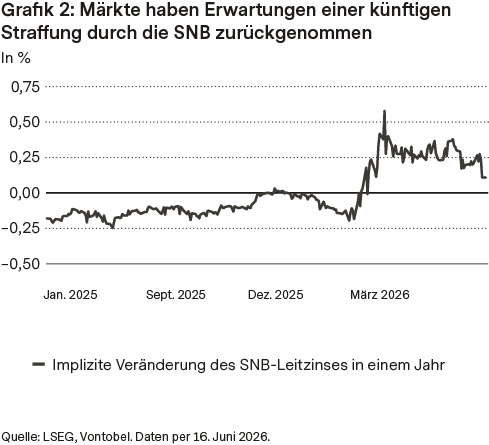

The Swiss franc continues to draw strength from its role as a defensive currency, although its appreciation has become a cause for concern for policymakers. The Swiss National Bank (SNB) has recently stepped up verbal interventions, signaling discomfort with further franc strength and its disinflationary effects. In the short run, the outlook appears more balanced. Markets have lowered expectations for future SNB tightening, while the ECB’s recent rate hike has widened the expected policy gap between the euro area and Switzerland. Combined with the SNB’s rhetoric, this could curb further gains in the franc, especially if geopolitical tensions continue to ease. Looking further ahead, Switzerland’s strong public finances, current-account surplus, and reputation as a safe destination for capital will likely continue to provide support for the franc.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.