Investors’ Outlook Staying ahead, reaching beyond

Inflation up or down, recession yes or no: month after month, the global markets hope for conclusive answers in newly published economic data. Those who wait until they come can only react. But those who think in terms of scenarios can anticipate opportunities. This is precisely what the Vontobel experts lay the foundations for in the Investment Outlook 2024.

Check of the economic status

Central banks spent November emphasizing the need to keep monetary policy restrictive for long enough. Macroeconomic data that showed signs of a weakening US labor and housing market, however, had investors questioning how long “long enough” will actually be. More evidence of a weakened US economy is likely to come as the full impact of the aggressive interest-rate hikes has yet to be felt, which is why the Multi Asset Boutique reiterates its view that the US will ultimately enter a recession in the first half of 2024.

Many of the factors that have supported the US economy and helped it stave off a recession so far are poised to fade away in the coming weeks and months. They include pandemic savings and a more robust-than-expected labor market. Hence, the elephant in the room is the question of how much longer US consumers can prop up the economy.

The global economy is too weak to manage the strong rise in bond yields. So, even without a recession, the Fed may soon need to cut rates as monetary policy is too tight for current inflation levels. US consumer price inflation, for instance, dropped to 3.2 percent from 3.7 percent year-on- year in September. And producer price inflation fell to 1.3 percent from 1.9 percent in that period. This hasn’t gone unnoticed; investors are currently pricing in a nearly 60 percent chance of a rate cut of at least 25 basis points by May 2024.

Across the pond, Eurozone economic growth looks worrisome through the lens of purchasing managers’ indices (PMIs). These indicate that it is “stuck in the mud” and may very well be up for a second consecutive quarter of shrinking gross domestic product (i.e., a technical recession). Given the dire state of the Eurozone economy and the significant slowdown in inflation, the European Central Bank may even start cutting ahead of the Fed. China is unlikely to implement any meaningful stimulus before the second half of 2024.

Outlook for the economic landscape in 2024

As 2023 draws to a close, investors are likely to be able to look back at a pretty decent year on the stock market, especially following a dreadful 2022. This is partly due to economic developments, with growth surprising to the upside and inflation to the downside. Will it be the same story next year?

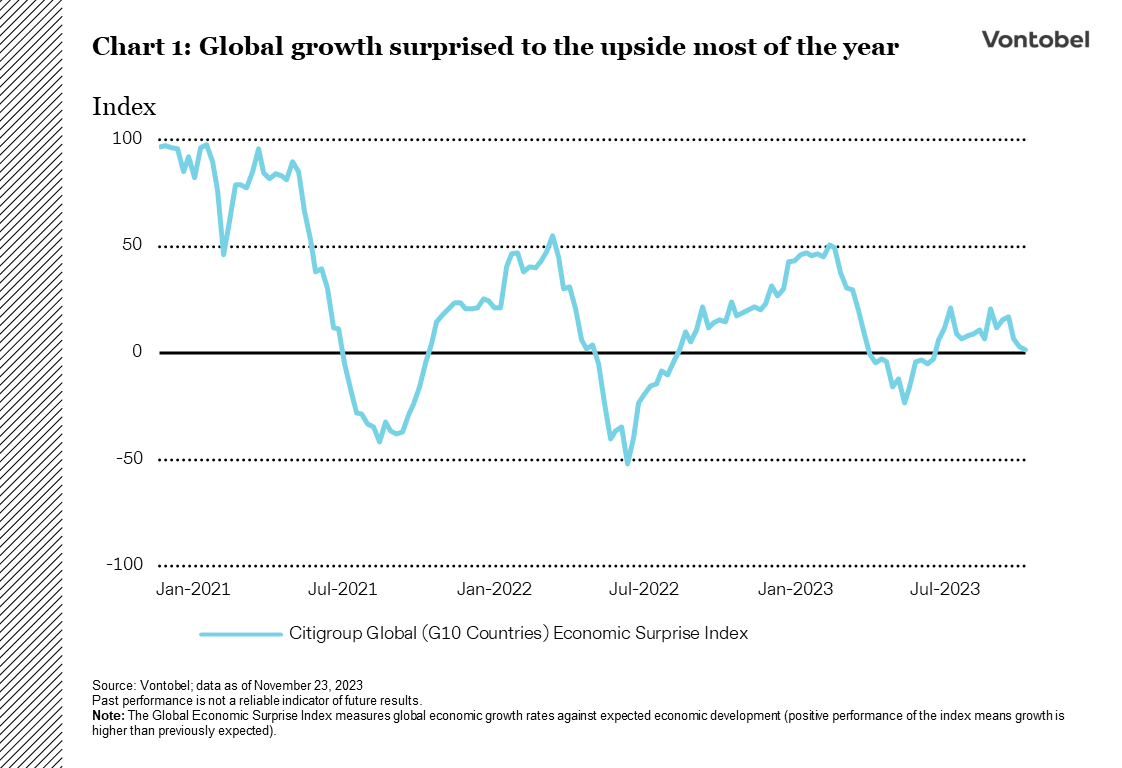

Global economic growth exceeded expectations practically across the board in 2023 (see chart 1), despite posting below-average growth. The majority of economists expected a recession that never ended up materializing this year as high levels of inflation and the steep cycle of interest-rate hikes didn’t harm businesses and consumers as much as had been feared. Companies deferred taking on new loans at high interest rates and reduced vacancies instead of resorting to laying off employees. Consumers were able to tap into the significant savings they accumulated during the pandemic and benefit from a stable labor market. In addition, fiscal policy was surprisingly expansionary, especially in the US, where government support remained generous.

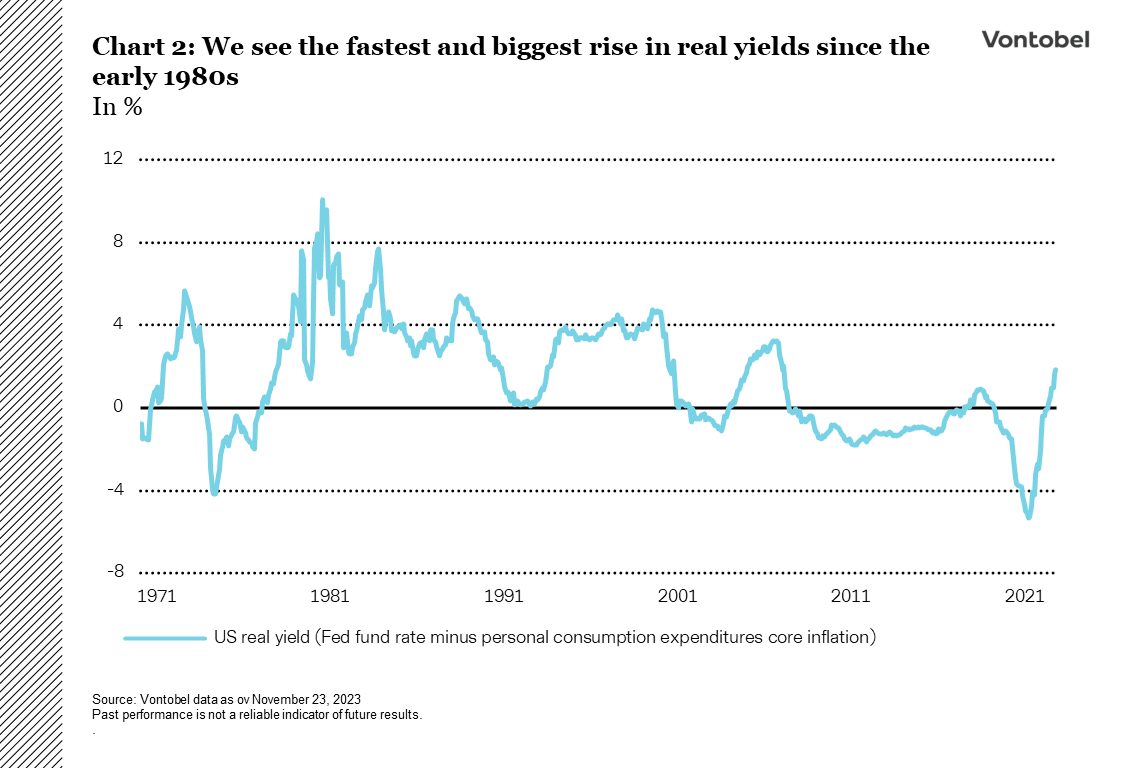

The recession debate—will there, won’t there? The key question facing investors in 2024 is whether it will be possible to defeat inflation without triggering a recession. This is something that has never been achieved before. Higher interest rates come at a cost and are already exposing the first cracks in the economy; just think of last spring’s banking crisis. The longer interest rates stay high, the greater the impact—something to bear in mind when considering the most significant surge in real interest rates since the early 1980s (see chart 2). Inflation-adjusted rates have reached a 15-year peak, but unlike back then, the world is significantly more indebted.

Corporate earnings are no longer on the rise, except at a few major US technology companies and European luxury goods producers. Surveys show that companies keep scaling back planned capital expenditures. Many companies are also forced to meet high wage demands as workers (a commodity in short supply) seek compensation for inflation. If this trend continues, some firms will have no choice but to lay off employees to protect their margins.

US consumers’ purse strings

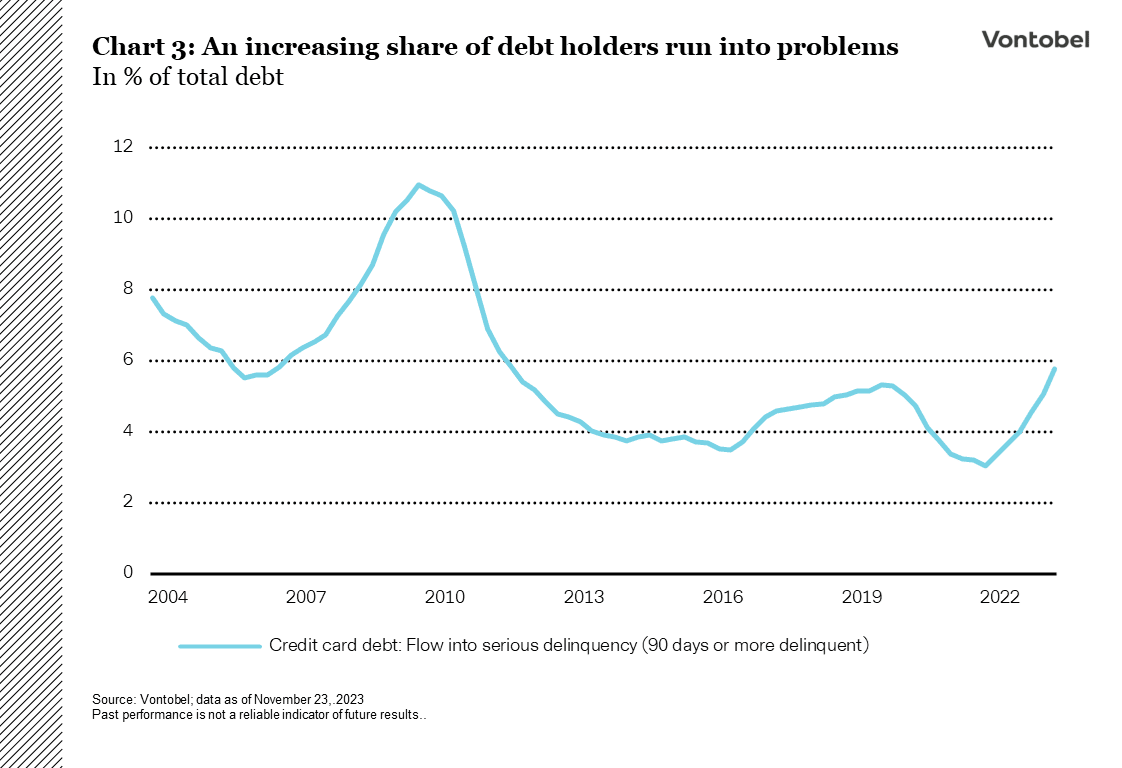

Shoppers have been quite happy splurging, boosting the economy long after pandemic lockdowns were lifted. What if consumers aren’t ready to tighten their purse strings just yet? They are currently spending more than they earn, which means their savings are dwindling or they’re accumulating new debt. In fact, US credit card debt recently reached an all-time high of more than 1 trillion US dollars. At the same time, interest rates of more than 20 percent have sparked an increase in payment delinquencies (see chart 3). It seems rather unlikely that US consumers will be able to save the global economy from a recession for much longer.

The Multi Asset Boutique sees softening demand for goods and services would ultimately push inflation back to pre-pandemic levels, especially considering the fact that global supply chains are running smoothly again and many goods manufacturers are grappling with rising inventory levels. Global central banks would be forced to slash interest rates if unemployment rises and inflation falls.

Potential curveballs

So, what might be the unexpected surprises? One important factor would include a faster- than-anticipated decline in inflation, which would relieve pressure on companies and consumers alike. This would then also lead to faster-than-expected interest rate cuts, providing the economy with further support. Another one to watch would be a larger fiscal stimulus package in China to help the world’s second-biggest economy gain momentum. On the other side of the coin, further escalation in the Middle East could be a catalyst for a second wave of inflation. In that case, central banks would likely remain restrictive.

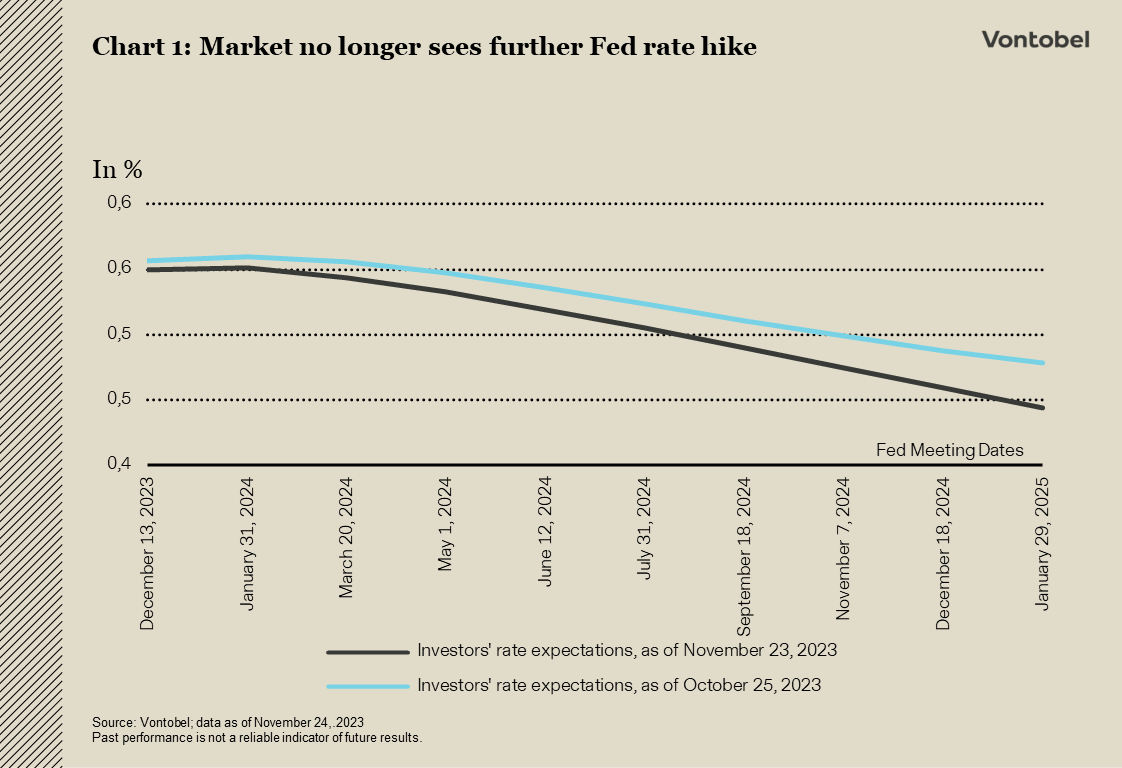

Market twist: Further Fed rate-hike expectations take a dive

Cooler inflation and signs of slower growth in the US revived demand for bonds. Yields on 10-year Treasuries dropped over 50 basis points in a span of one month. In September, Fed funds futures implied a 60 % chance of another hike. But now, they’ve fully priced out increases and anticipate a rate cut by mid-next year (see chart 1).

The US economy has shown impressive resilience amid the most significant monetary tightening in more than four decades, considering both the pace and scale of the interest-rate increases. While the expected pattern of tightened monetary policy leading to reduced private sector credit growth did materialize, the economy has continued to exhibit unusually robust growth.

Investors are now projecting that this economic resilience and the limited likelihood of the Fed tightening further means investors are clear of danger. However, just as optimism that a recession may have been averted begins to take hold, the Conference Board Leading Economic Index extended its losing streak to 19 months. The only comparable periods of such a prolonged negative trend were during the stagflation crisis of the mid-1970s and the global financial crisis. Historically, such a prolonged and marked downturn in this indicator has invariably been a precursor to a recession.

The sharp increase in yields in October may have represented the high point for this cycle. Recent data suggest a pause by the Fed and possibly the initiation of rate cuts in 2024. This sets the stage for potential rate cuts down the road. Typically, before such cuts, yields tend to fall.

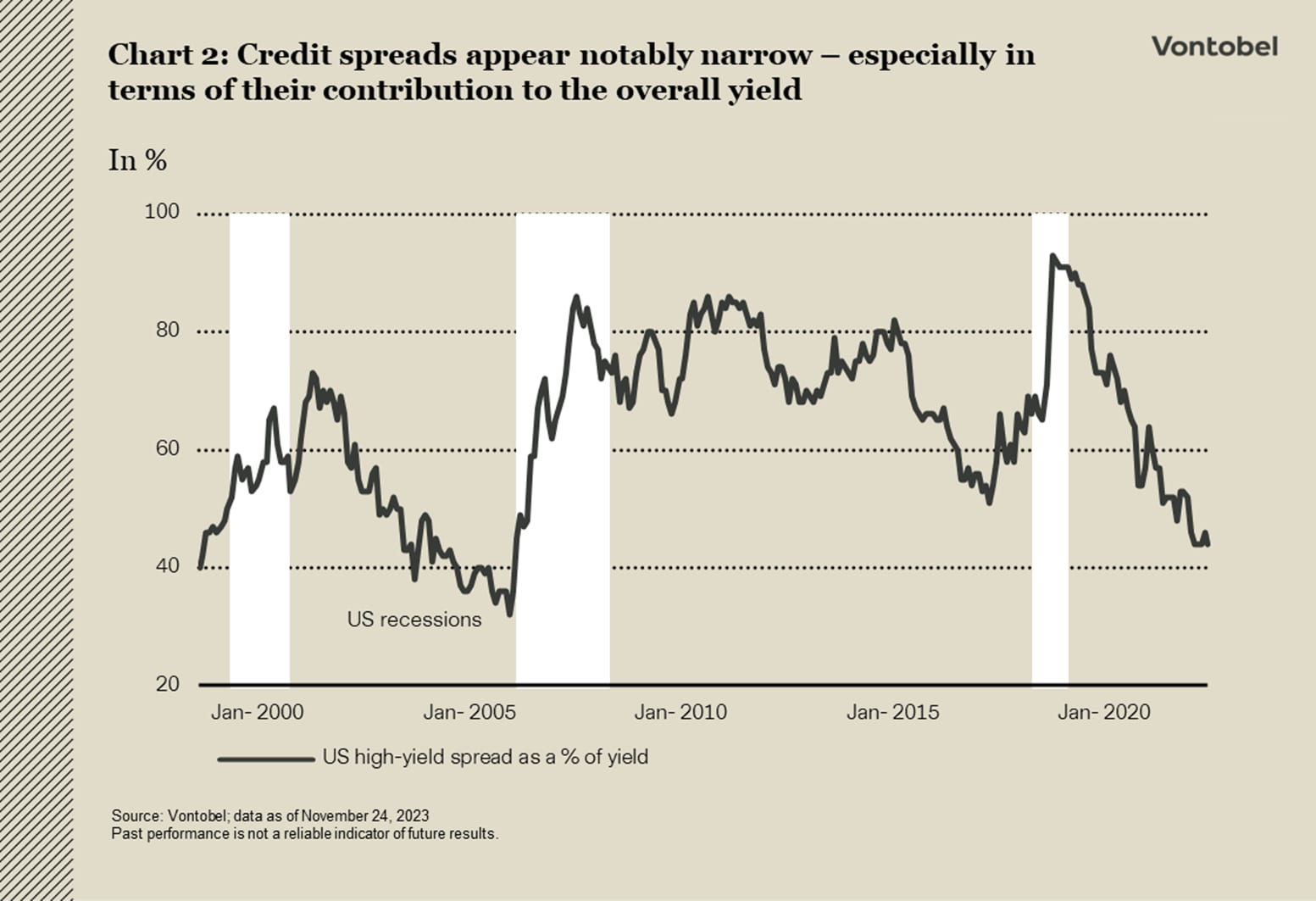

Focus on worsening credit fundamentals, tight monetary policy

Bond investors should focus on the worsening credit fundamentals and tight monetary policy. Chart 2 illustrates the percentage of US high-yield corporate bond yields that are attributable to credit spreads. The current level of 43 percent is the lowest since 2007. According to Moody’s, the high-yield default rate in the US is running above 5 percent, the highest since the first half of 2021, when credit markets were recovering from a wave of defaults caused by the pandemic. Rising defaults suggest that high borrowing costs have started to hit credit markets more significantly and that the economy is softening.

A no-exception November

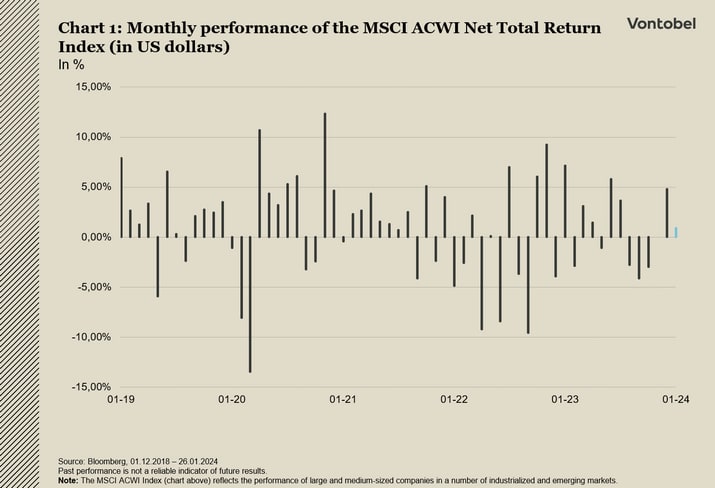

November is typically the best month for stocks, and it didn’t fail to deliver again this year. This time, the market didn’t just reverse October’s negative performance, but posted the best monthly returns since the Covid-19 vaccine breakthroughs in late 2020 (see chart 1). Too good to be true?

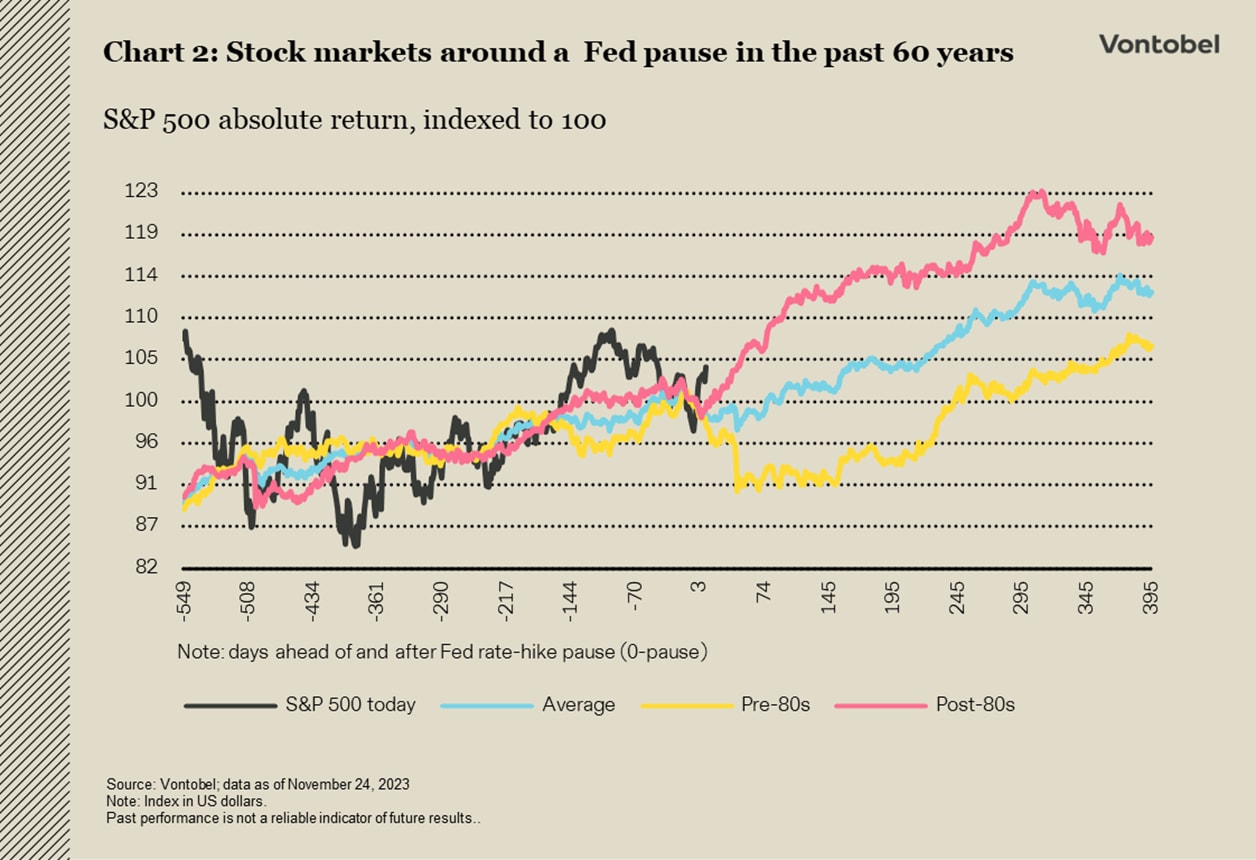

Two out of three key macroeconomic factors dominating the scene already seem to be behind us. First, US inflation peaked more than 12 months ago, which has since also been the case in other developed markets. Second, central banks appear to have reached the finish line in their rate-hiking campaigns. Historically, both events have set off positive market reactions over the following year (see chart 2).

The third and final missing piece is a recession that, as a reflection of a very atypical economic cycle, has been slow to materialize in the US. But to what extent have investors already priced in a recession? And how severe would one be?

Scratching the surface of the MSCI ACWI Net Total Return Index’s absolute year-to-date mid- to low double digit gains, investors should consider that few sectors (technology, communication services, consumer discretionary) have boosted its performance with common traits like quality, excess liquidity and low leverage and large market capitalizations. Excluding these sectors, performance beneath the surface has been flat at best.

What can we expect for 2024?

The good news is that earnings-per-share (EPS) growth forecasts have moderated recently, leaving room for upside surprises. Valuation multiples remain below peak levels reached in 2021, perhaps because a slowing macroeconomic outlook is already priced in. EPS growth for 2024 – 2025 might come across as ambitious, but taking into account the relevance, contribution, and visibility of large dominant sectors, it’s not too surprising.

Difficult times for “black gold”, good times for regular gold

Oil markets witnessed a sharp sell-off in November. Contrary to “black gold,” “real” gold proved to be more resilient. Oil prices fell to a four-month low towards mid-November. The fact that the conflict between Israel and Hamas has so far not expanded further into the region seems to have pushed concerns about a possible oil shock into the background for many investors. Instead, the focus has shifted to US oil production, which recently reached an all-time high of 13.2 million barrels per day. Rising US oil inventories, mixed US economic data, and a slowdown in Chinese refinery activity also weighed on sentiment. There are also doubts as to whether the new voluntary oil supply cutback announced by the Organization of the Petroleum Exporting Countries and its allies (OPEC+) at the end of November will be fully implemented. Angola, for instance, has rejected its quota.

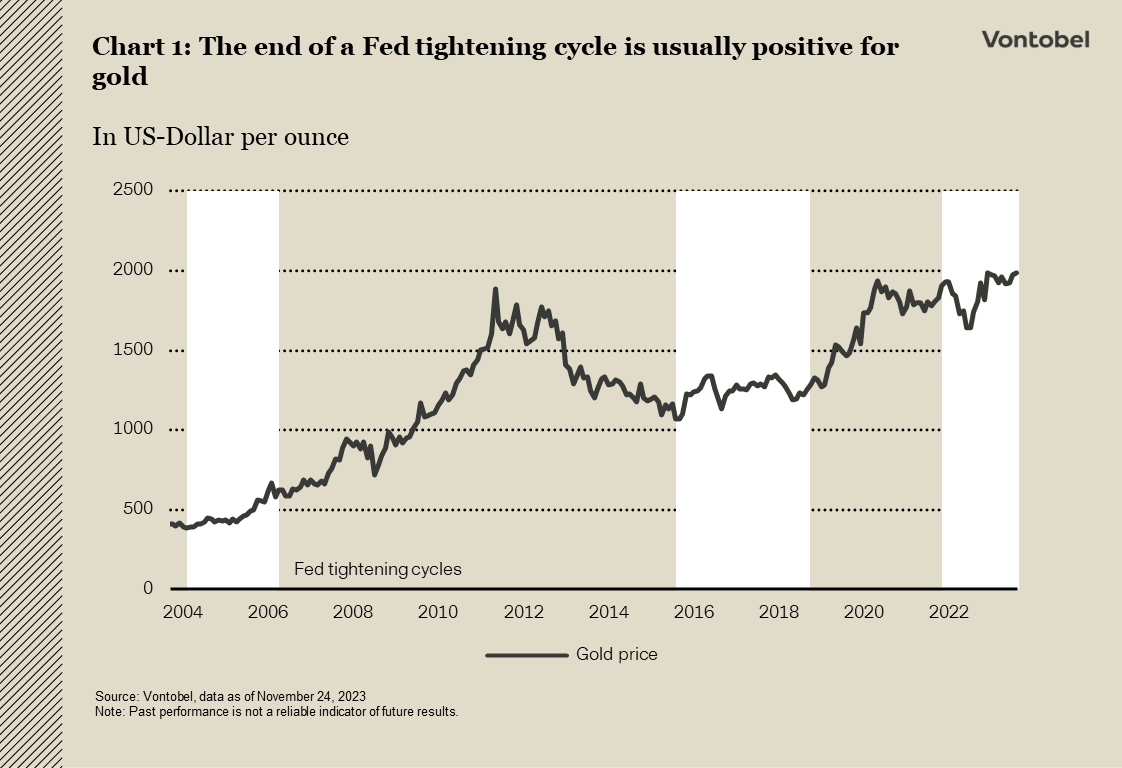

Gold, on the other hand, was unperturbed by the declining war risk premium: it was able to hold on to its October gains and even briefly flirted with the psychologically important 2,000 US dollar per ounce threshold in late November. That’s due to a string of weaker-than-expected economic data and easing inflation levels in the world’s largest economy, which prompted investors to price in a first Fed interest-rate cut in the first half of 2024. The end of the Fed’s tightening cycle and everything that it entails, such as falling real yields and a weaker US dollar, has often been a positive catalyst for gold in the past (see chart 1).

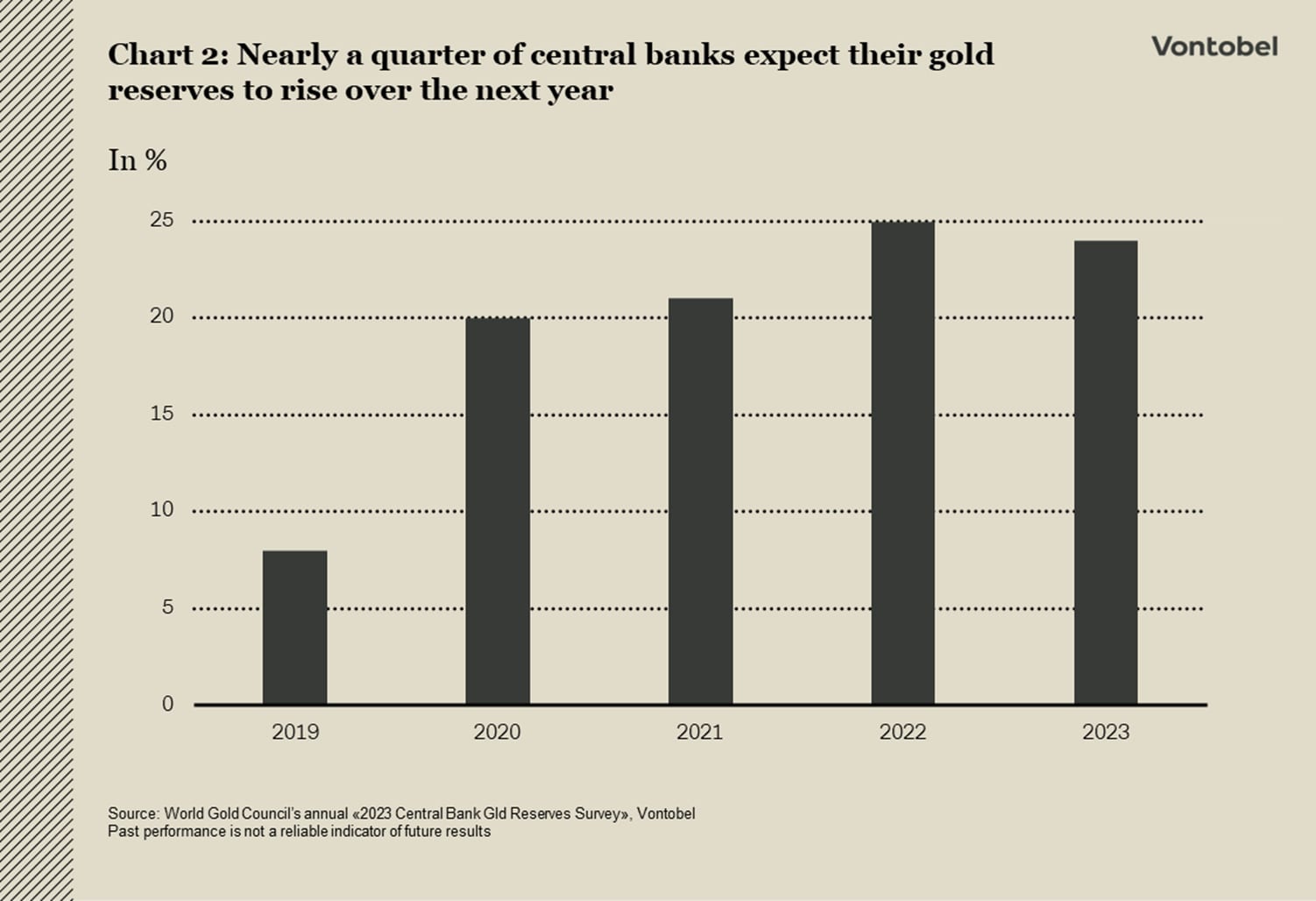

Demand also appears solid on the physical side. Switzerland, an important gold trading hub, exported more than 150 tons of gold in October, the most since May. A considerable proportion of this—around 49 tons (+60 percent compared with the year-earlier period)—went to India. India is the world’s second-biggest bullion-consuming nation and celebrates a series of festive days from October to November, during which gold is a popular gift. A longer-term tailwind comes from central banks. While they were net sellers in the three decades following the collapse of the Bretton Woods system, they started to build up their reserves again after the global financial crisis. This trend has intensified in recent years, particularly after Western countries froze Russia’s central bank reserves. According to the World Gold Council, about a quarter of the world’s central banks also expect to increase their gold reserves in the coming year (see chart 2).

US dollar’s rise loses steam— is it approaching a pivot?

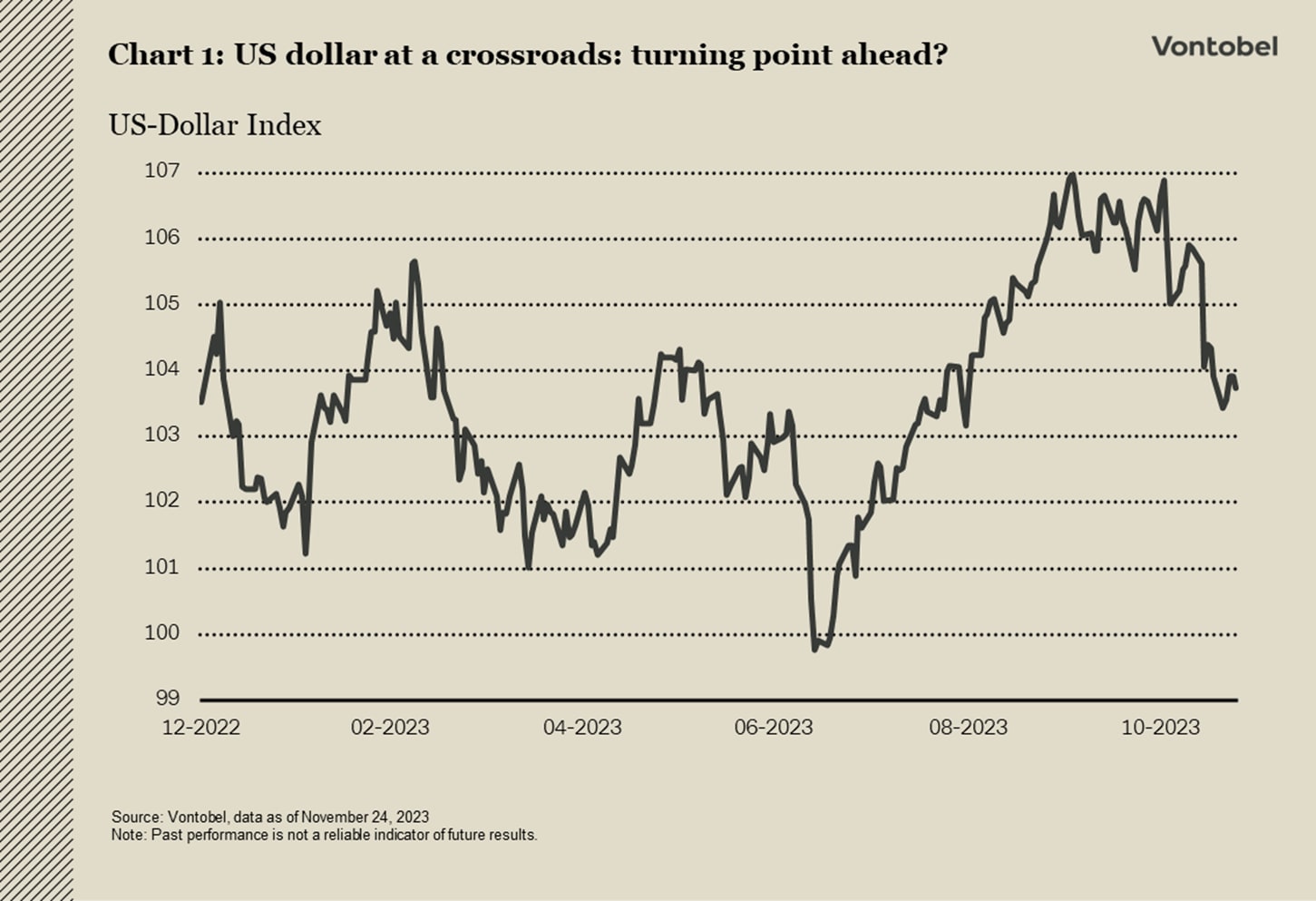

The US dollar’s upward momentum seems to be losing steam and may be nearing a turning point (see chart 1). Lower US yields and indications of emerging frailties in the world’s biggest economy are negatively affecting market sentiment. The ongoing economic impact of the Fed’s monetary tightening, combined with diminishing fiscal support, leaves the US dollar vulnerable in the short term.

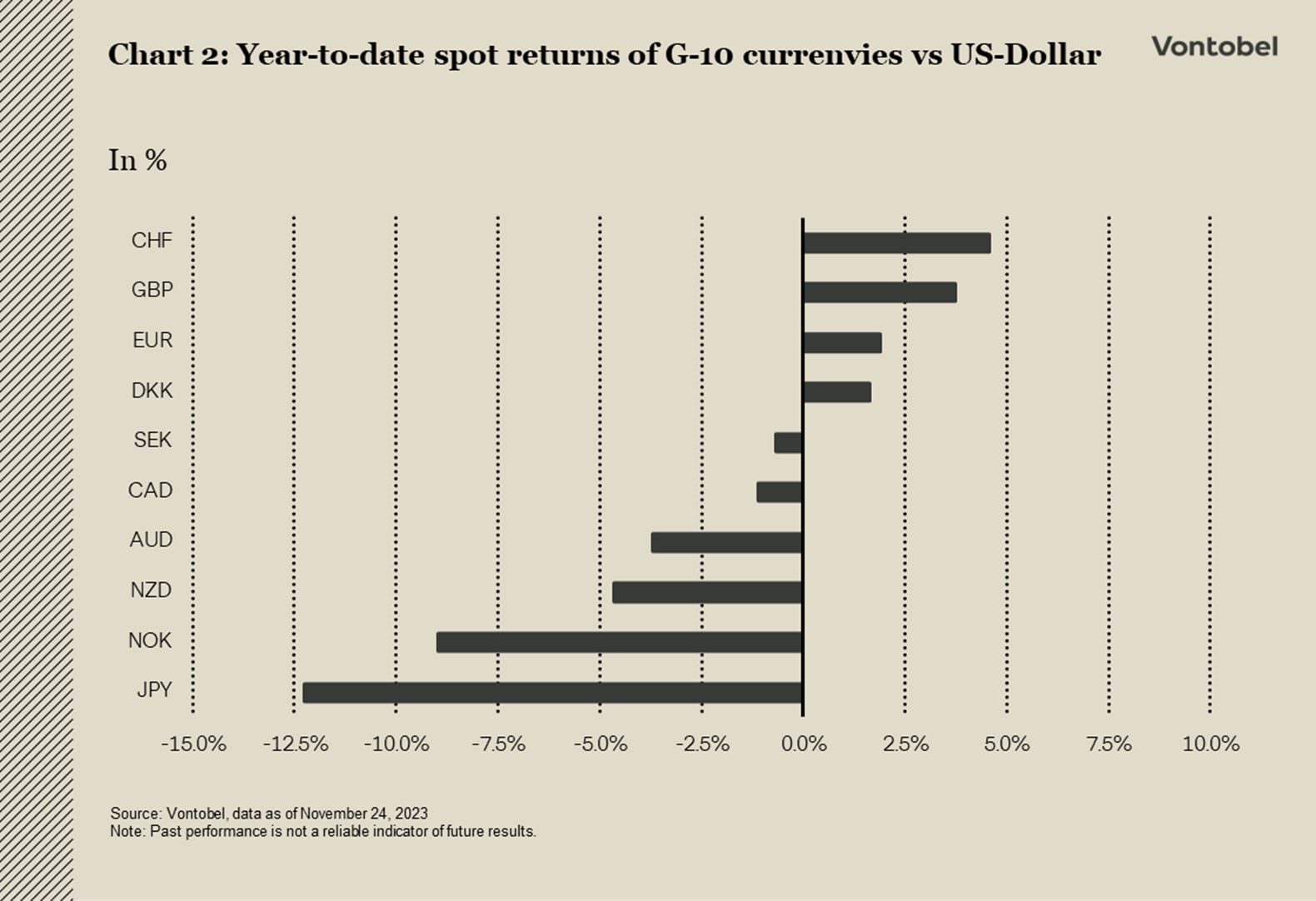

Over the past month, the euro has strengthened against most G-10 currencies, with the notable exception of the Swiss franc, buoyed by geopolitical factors. Interestingly, the euro’s rise comes despite a lack of particularly favorable news. This resilience may be attributed to a combination of negative economic developments already factored into its price and growing speculation that a downturn in the US economy is imminent. These factors have collectively bolstered the euro-dollar pair and the euro more broadly. The Fed’s medium-term monetary policy trajectory and, crucially, the market’s perception of this trajectory continue to be key drivers for the euro. For euro-dollar bulls, a focus on the dollar side of the equation might be crucial for identifying short-term opportunities. Increasing signs of an economic slowdown in the US could reignite discussions about a potential Fed rate cut, further supporting the bullish case for the euro-dollar pair.

The Swiss franc’s qualities as a safe haven gain attention

This year, the Swiss franc stands out as the strongest performer among the G-10 currencies, maintaining an approximate 4.5 percent gain against the US dollar in terms of spot return (see chart 2). The Swiss National Bank (SNB) seems to prefer maintaining a strong exchange rate to counter inflation rather than raising its key interest rate above 1.75 percent. With one more SNB meeting scheduled for December 14, market expectations are now leaning towards no further interest-rate hikes and rate cuts to commence next year, with projections suggesting a first reduction by September.

If local inflation does not intensify again, the Swiss franc is expected to soften moderately over the medium term. But in the short term, sustained demand for the currency cannot be overlooked given the ongoing geopolitical uncertainties and a market that’s increasingly driven by risk factors beyond just fundamentals.

Authors

Frank Häusler, Chief Investment Strategist

Stefan Eppenberger, Head Multi Asset Strategy

Christopher Koslowski, Senior Fixed Income & FX Strategist

Mario Montagnani, Senior Investment Strategist

Michaela Huber, Cross-Asset Strategist