Central banks are buying gold at record prices

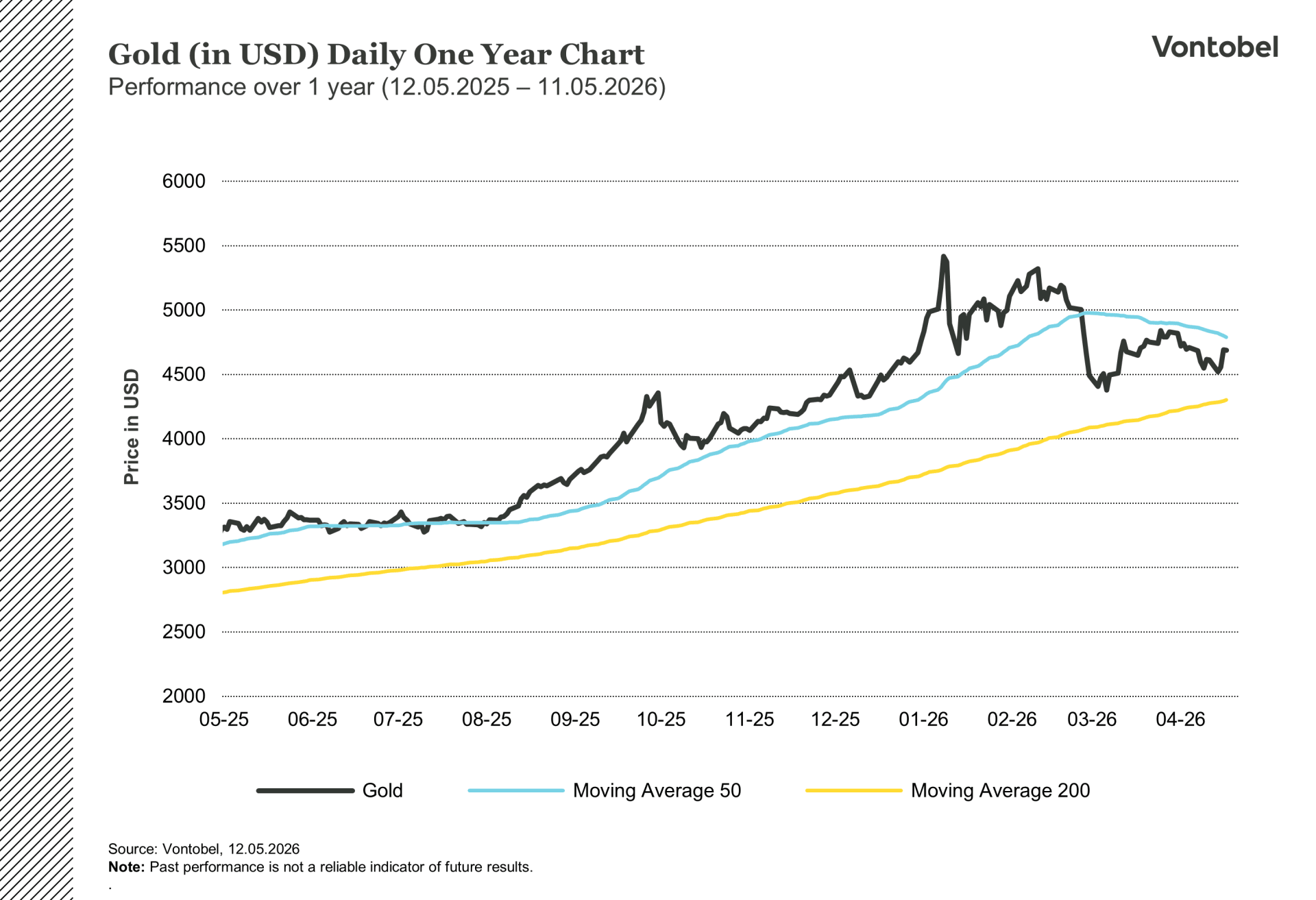

Gold fell 15% from its all-time high in January. Nevertheless, the world's central banks were net buyers of 244 tons during the first quarter of 2026 (World Gold Council, 07.05.2026). The price decline and the reserve build-up point in opposite directions. To understand where the market is heading from here requires a longer view of what central banks are actually doing and why.

Gold's role in the global reserve system

Gold selling off in the early phase of an acute crisis is nothing new. The same dynamic played out during the 2008 financial crisis and the onset of the pandemic in March 2020. Gold is a liquid asset, and many investors had large, unrealized gains that they could secure. At the same time, the dollar strengthened, real rates rose, and the inflationary impact of the oil shock triggered by the Iran conflict led the market to price out expected rate cuts from the Fed. A stronger dollar became a headwind for assets that generate no running yield.

Central bank behavior, however, is driven by different forces. Until the 1990s, gold made up a larger share of global central bank reserves than the US dollar, a pattern that had held for decades (Deutsche Bank, 30.04.2026). The shift away from gold did not occur in the 1970s when Nixon ended gold convertibility, as many assume, but rather in the 1990s. This was when the geopolitical landscape changed fundamentally. The US emerged as the world's sole superpower after the collapse of the Soviet Union, boasting robust public finances and stable inflation. Global trade expanded at an unprecedented pace, and emerging economies accumulated substantial dollar reserves through export earnings. In that environment, US Treasuries were far and away the most attractive asset for any central bank to hold. Gold's share of global reserves fell from roughly 40% to 10% (Deutsche Bank, 30.04.2026).

That era was based on specific conditions: the US as the guarantor of the global trading system, globalization proceeding without major disruptions, and US fiscal health being perceived as sound by the markets. None of these factors are the same in 2026. US budget deficits are running at around 6–7% of GDP despite full employment, geopolitical uncertainty has escalated sharply, and the global trading system is being renegotiated.

Against this backdrop, the dollar-dominated reserve structure of the 1990s increasingly looks like the exception rather than the norm. Since the financial crisis, central banks have been accumulating gold on a large scale, and the pace picked up markedly after February 2022 when the West froze $300 billion in Russian central bank reserves (Bloomberg, 26.02.2022). This action sent a clear signal to central banks outside the Western alliance: assets denominated in dollars, euros or pounds can be seized by whoever controls the payment infrastructure, while gold is the only major reserve asset that carries no such risk.

Poland has been one of the most aggressive buyers, setting a target of 700 tons in gold reserves. The People's Bank of China has reported sixteen consecutive months of purchases. New buyers, including Malaysia, Uganda and South Korea, have also entered the market (World Gold Council, 07.05.2026). In February 2026, a milestone was passed: For the first time since 1996, the world's central banks collectively hold more gold than US Treasuries (Bloomberg, 08.04.2026).

The contrast with the Nordics is striking. The Riksbank has held 125.7 tons of gold since 2009 (Riksbanken, 2026). Norges Bank holds 37 tons, Danmarks Nationalbank 66.5 tons and the Bank of Finland 49 tons (IMF International Financial Statistics, 2026). None of them have adjusted their gold holdings in over a decade, even though the market value of their existing reserves has increased significantly. The Nordic central banks have chosen to sit out the reallocation unfolding globally.

Related Products

What determines the path from here

Although central bank purchases provide structural support beneath the gold market, the rate environment is putting pressure on the price in the near term. The oil shock resulting from the Iran conflict has pushed inflation expectations higher, making it harder for the Fed to cut rates. Currently, the market is currently pricing in no cuts at all for 2026 and even assigns some probability to a further hike. As long as rates remain at current levels, gold lacks one of its most important catalysts for price appreciation. Kevin Warsh, who is about to take over as the new Fed Chair, could change that picture, but the outcome is uncertain.

Meanwhile, Western investment flows have reversed. In March, North American gold ETFs recorded their largest outflows in at least five years, equivalent to 85 tons. In April, Europe swung back to inflows, and Asia has seen eight straight months of positive flows (World Gold Council, 07.05.2026). However, North America, historically the largest market, has not yet returned. If it does, as occurred after similar outflows in 2020, a significant demand component will come back into play. If it does not, a key piece of the puzzle is missing.

Forecasts from the major banks reflect the uncertainty. Goldman Sachs predicts $5,400 by year-end, JP Morgan $6,300, while HSBC points to $4,450 (Bloomberg, 08.05.2026). The price currently sits around $4,700 per ounce. Where it goes from here depends largely on the interest rate environment and how long the conflict lasts. The direction of central bank reserves, on the other hand, looks increasingly clear. Vontobel offers a wide range of leveraged products with gold as the underlying, giving investors the ability to take both long and short exposure based on their market view.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.