Investors' Outlook: with bated breath

2026 has been defined by uncertainty: the war in the Middle East is pushing energy prices higher and forcing central banks into difficult trade-offs between inflation and growth. At the same time, Japan is undergoing a political and economic transformation under Prime Minister Sanae Takaichi, whose ambitious "Sanaenomics" agenda aims to break decades of stagnation. But how are these global forces shaping markets? What risks lurk beneath the geopolitical turmoil, and where do the opportunities lie?

Quo vadis?

With the war in Iran ongoing, each passing day raises new questions for investors and casts some doubt over the Multi Asset Boutique’s 2026 economic baseline. Positive growth momentum has temporarily stalled, while higher oil and gas prices risk fanning inflation amid attacks on energy infrastructure and escalating rhetoric between the US and Iran. As such, central banks are likely to delay interest rate cuts in the near term.

At present, the likeliest scenario appears to be a relatively short-lived conflict. Rational factors that support this view include limited US public support for a pro- longed, costly war, the fact that a protracted conflict is not in the best interest of regional players such as Saudi Arabia and Qatar, the difficulty of regime change in Iran, and the broader pressure on major economies like China.

Under this scenario, growth is more likely to stall than contract. But the longer the conflict goes on, the greater the risk of a slowdown or recession. And despite the rational arguments listed above, there is no guarantee that all actors will behave rationally. The US may seek de-escalation, but Iran has significant leverage and is unlikely to concede without major concessions.

The war also complicates matters for central banks. Many had been easing or pausing rate cuts, but surging energy prices now cloud the path ahead. US Federal Reserve Chair Jerome Powell acknowledged that higher energy costs will push overall inflation higher and that nobody knows the economic impact of the war. The challenge is even more acute for the European Central Bank, considering Europe’s energy dependence. Rising oil prices increase economic uncertainty and inflation risks.

Is Japan about to bloom again?

Every spring, Japan is transformed by the sakura, a fleeting season when cherry blossoms blanket the archipelago in soft pinks and whites. For centuries, this has been more than a visual spectacle. It is a cultural shorthand for saisei, or renewal. In 2026, the metaphor has rarely felt more apt for the Japanese macroeconomy.

After decades of winterlike stagnation, the political and economic landscape is stirring. The question for investors is no longer whether Japan can wake up, but whether, under the newly minted supermajority of Prime Minister Sanae Takaichi, it is finally able to bloom in a way that is not only vibrant but also sustainable.

Sanae Takaichi is making waves in Japan. A protégé of the late Shinzo Abe, she made history in 2025 as Japan’s first female prime minister and quickly consolidated her power with a historic landslide victory in February 2026. Her Liberal Democratic Party now holds a two-thirds supermajority in the lower house, granting her a legisla-tive mandate for change that her predecessors could only have dreamed of. Her political agenda, often dubbed Sanaenomics, places strong emphasis on fiscal expansion. Key promises include significant investments in economic security, focusing on sectors such as semiconductors, fusion energy, and artificial intelligence. She has also pushed for popular measures like suspending the consumption tax on food to ease the financial burden on households. Unlike previous leaders who prioritized balancing the budget, she argues that growth must come first, asserting that a revitalized economy will eventually outpace its debt. Her dovish position isn’t limited to fiscal policy. She is also a vocal advocate of accommodative monetary conditions, and in 2024 even described Bank of Japan (BoJ) interest-rate hikes as “stupid.”

Beyond the economy, Takaichi is a staunch foreign-policy hawk. She is not only determined to double defense spending to 2 percent of gross domestic product (GDP) but has also pushed for an amendment to Japan’s pacifist constitution. Specifically, she wants to revoke Article 9, which states that Japan renounces “war as a sovereign right of the nation” and “the threat or use of force as a means of settling international disputes” (i.e., it explicitly forbids Japan from going to war). In China, Takaichi has already ruffled feathers by stating that a Chinese attack on Taiwan could constitute a “survival-threatening situation” for Japan, which sparked a diplomatic row with Beijing. Her vision of a strong Japan also extends to promoting traditional social values and adopting a tough stance on immigration.

Japan’s long winter: Decades of deflation and demographic challenges

To understand the significance of Takaichi’s bold approach, one must acknowledge the weight of the history she is attempting to overturn. For over three decades, Japan has been a global case study in economic stagnation, low or negative inflation, and demographic decline. The burst of the early-1990s asset-price bubble marked the start of Japan’s “Lost Decades,” a prolonged period of economic malaise. As the first major developed economy to face a shrinking workforce, Japan became a cautionary tale. An aging population and declining birth rates stifled domestic demand, while the bubble’s collapse created a deflationary mindset. Scarred by uncertainty, consumers and businesses hoarded cash instead of spending or investing, deepening the stagnation.

The era of Abenomics, launched in 2012 by Prime Minister Shinzo Abe, attempted to break this cycle through the “three arrows”: aggressive monetary easing by the BoJ to combat deflation and stimulate economic activity, flexible fiscal stimulus to boost short-term demand while addressing long-term fiscal challenges, and structural reforms to enhance Japan’s economic competitiveness. While Abenomics succeeded in weakening the yen and propping up the Japanese housing and equity markets, the BoJ’s 2 percent inflation target remained out of reach— until the pandemic.

The global supply shocks of the early 2020s did what a decade of stimulus could not: they imported inflation and led to a rise in inflation expectations. In April 2022, headline inflation surpassed the BoJ’s target for the first time in years, and remained above it until December 2025. This shift in economic conditions has also changed wage negotiation dynamics. Before the inflation surge, large companies were generally reluctant to grant significant pay increases, typically limiting wage hikes to around 2 percent. However, in 2024 and 2025, businesses were compelled to offer raises exceeding 5 percent to keep pace with rising inflation and retain staff.

Why Takaichi must tread carefully

While Takaichi’s assertive statements have made waves, she must tread carefully in execution. This is because she inherits a Japan that is no longer “cold.” With headline and core inflation still hovering around 2 percent, her challenge is to stimulate the economy with- out overheating it. The Japanese public, accustomed to stable prices for a generation, remains highly sensitive to the rising cost of living. According to an Asahi opinion poll on the country’s most pressing issues, inflation claimed the top spot (at more than 60 percent) in September 2025. This is hardly surprising, as real (i.e., inflation-adjusted) wages have remained in negative territory for years, only recently turning slightly positive.

To mitigate the risk of potential backlash, Takaichi must prioritize supply-side reforms. A critical bottleneck in this effort is labor. With a shrinking population and a strict anti-immigration stance that risks further tightening an already constrained labor market, Japan’s economic growth hinges on improving productivity. This necessitates reforms in labor flexibility, potentially relaxing overtime regulations to allow willing workers to earn more, and deeper integration of automation.

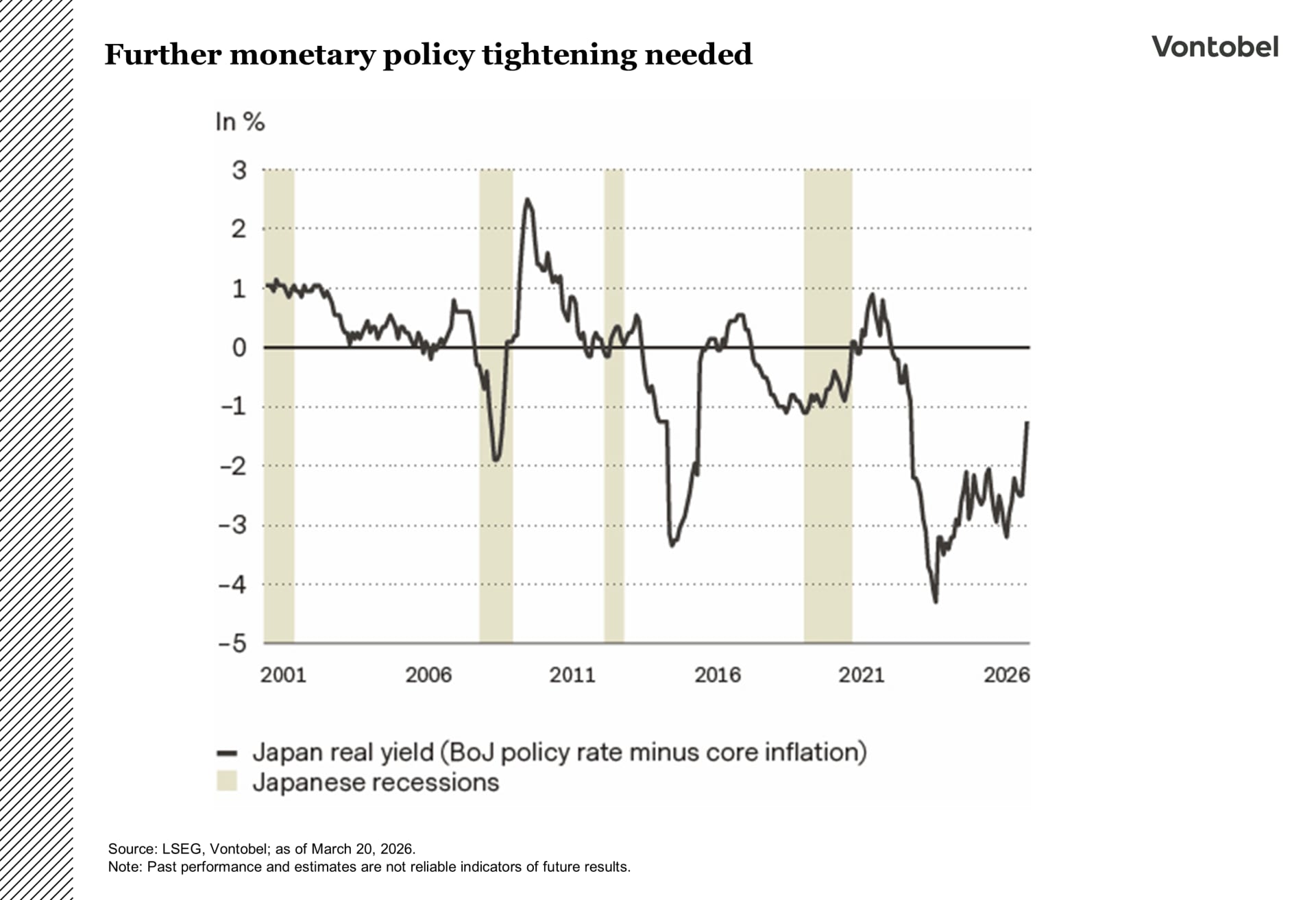

Takaichi may want to tread carefully when navigating monetary policy. While she favors lower interest rates, the BoJ has repeatedly emphasized the necessity of raising them. Why does the BoJ aim to raise interest rates further, even though inflation has recently slowed to around 2 percent? The answer lies in the fact that its monetary policy remains stimulative. Even after increasing the policy rate to 0.75 percent in late 2025, real (inflation-adjusted) interest rates remain deeply negative.

With inflation still somewhat sticky and the yen weak, the BoJ may be forced to hike rates toward a rate of 1.25 – 1.50 percent. This creates a tug-of-war: a government that wants to spend and a central bank that must normalize monetary policy.

The bond market has already begun to voice its concerns. In January 2026, yields on 10-year Japanese government bonds (JGBs) pushed past 2.3 percent, and the 40-year yield breached 4 percent for the first time in decades (bond yields move inversely to prices). Upward pressure intensified again in February following reports that Takaichi met with BoJ Governor Kazuo Ueda and expressed reservations about further interest-rate hikes. Adding to the market’s concerns, she also nominated two “reflationists” to the BoJ’s board.

In short, investors worry that her fiscal boldness, combined with rising interest rates, could render Japan’s massive debt-to-GDP ratio (estimated at around 235 to 250 percent of GDP as of early 2026) unsustainable.

Why a fiscal crisis is unlikely

Despite the return of bond vigilantes to Tokyo, the Multi Asset team is not overly concerned about the likelihood of a full-scale fiscal crisis. This confidence stems from several factors First and foremost, because Japan borrows in its own currency, it is unlikely to run out of money (in a worst-case scenario, Japan could simply print more money to meet its obligations.) Second, Japan’s government debt market is predominantly held by domestic investors. Roughly 90 percent of JGBs are held by domestic institutions, including the BoJ, banks, and insurance companies.

These institutions, have a vested interest in stability. This reduces the risk of foreign capital flight, which often triggers sovereign defaults. Third, a look at Japan’s net international investment position—a key economic metric representing the difference between a nation’s stock of foreign financial assets and its liabilities to foreign residents—suggests that Japan is a net creditor nation that holds a massive portfolio of international investments. This effectively means that it is not reliant on the kindness of strangers (read: foreign capital) to fund its deficit

Fourth, investors should also consider that Japan’s gross debt, currently at around 235 percent of GDP, needs to be adjusted for public sector assets and the central bank’s government bond holdings. After these adjustments, Japan’s debt burden decreases to a net debt level of “only” 134 percent of GDP, or 45 percent of GDP when BoJ holdings are excluded. Another often-overlooked reason is that Japan incurs very low interest expenses compared to its peers. In 2024, the general government’s net interest expense, as a percentage of total expenditures, was approximately 1 percent. For context, the Eurozone spent around 3.2 percent, while the US allocated more than 9 percent to interest payments.

Lastly, inflation (as unpopular as it may be) also has a silver lining. By inflating tax revenues and nominal GDP, it naturally shrinks the relative size of the debt.

Why a yen appreciation is likely

While Takaichi has historically been a vocal proponent of a weak yen to support exports, the macro regime shift of 2026 is creating a perfect storm that points toward yen appreciation. The bull case for the yen rests on several arguments.

First, with USD / JPY trading at around 159, the yen remains undervalued according to purchasing power parity models.

Second, narrowing interest-rate differentials and the unwinding of the yen carry trade. For years, the yen was the global funding currency for the carry trade, a strategy where an investor borrows capital at a lower interest rate to invest in assets with potentially higher returns, because Japanese rates were stuck at zero (or below), while the rest of the world was hiking rates. As long as the BoJ raises rates while others are either holding them steady or cutting them, the yield disadvantage of the yen is diminishing. This reduces the appeal of the yen carry trade, which essentially represents a massive short position in the currency. As a result, the yen is becoming fundamentally more attractive to hold.

Third, a likely repatriation wave. In 2025, Japan was the world’s second-largest creditor nation after Germany. As yields on 10-year JGBs approach 2.5 percent and those on 40-year JGBs breach 4 percent, the “risk-free” return at home is finally becoming interesting again.

As such, Japanese life insurers and pension funds have an incentive to sell US Treasuries and European Bunds to buy JGBs. A massive flow of capital back into the country could create structural demand for the yen that could override Takaichi’s rhetorical preference for a weak currency.

Reassessing the situation

What once looked like a fairly straightforward easing story no longer does. The Fed has moved into a wait andsee phase as growth is slowing and the labor market is softening, while higher oil prices have pushed inflation risks back to the forefront. This tradeoff keeps monetary policy on hold for now.

Markets have already repriced.

Expectations for near-term rate cuts have been deferred, and front-end yields have moved higher. As long as energy prices remain elevated, the Fed has limited room to ease without risking a renewed inflation impulse. That said, the direction has not changed, only the timing. If growth continues to weaken and labor market slack increases, the Fed is still likely to cut. The key difference is that the easing cycle is now expected to continue later and be more gradual than previously expected. For rates, that tempers the case for a strong duration position in the near term. Yields could stay elevated and volatile as markets weigh inflation risks against slowing growth. But duration still provides protection in downside scenarios.

A more challenging backdrop for credit

Since the start of the war, credit has started to underperform as higher oil prices, rising uncertainty, and a repricing of rate expectations have weighed on sentiment and pushed spreads wider. On the one hand, slower growth, higher funding costs, and uncertainty around inflation and central bank policy make the environment less supportive for spread products. Credit can absorb one of these pressures, but not all at once. On the other hand, stress in parts of the private credit market, whether through tighter lending terms, weaker liquidity, or isolated credit events, can spill over into public markets by triggering a broader reassessment of credit risk. And supply is also a headwind.

Investment grade is facing a growing wave of issuance, especially from hyperscalers funding AI-related capital expenditure. The market has absorbed that supply so far, but it adds pressure at a time when investors are becoming more selective. If issuance continues to run above its historical norm, the market has to digest more paper, which makes further spread tightening harder even if fundamentals remain reasonably solid. This means that credit is increasingly exposed to a combination of macroeconomic pressure, structural risks, and rising supply, which argues for a more cautious stance.

Holding steady

The escalation in the Middle East has put stock markets under additional pressure after an already choppy start to the year.

The uncertainties markets currently face boil down to three main variables: the likely duration of the conflict (weeks or months?), how long the Strait of Hormuz is effectively closed or disrupted (with knock-on effects on global energy prices), and the extent to which the war weighs on global economic growth as risks range from stagflation to outright recession. It may be a relatively short-duration conflict or, alternatively, a prolonged but contained stalemate, potentially lasting a few more weeks with intermittent de-escalation signals. Even in a modestly extended stalemate, the impact on markets and the economy would likely be manageable. Credible de-escalation would probably bring oil prices back to more reasonable levels, causing only a short-term drag on economic growth. This view reflects a less energy-intensive global economy, with oil playing a smaller role in inflation today than in the 1970s or 2022. Starting points for oil and inflation also differ from past episodes. Another mitigation factor includes the International Energy Agency’s emergency release, which provides a buffer and valuable time for policymakers.

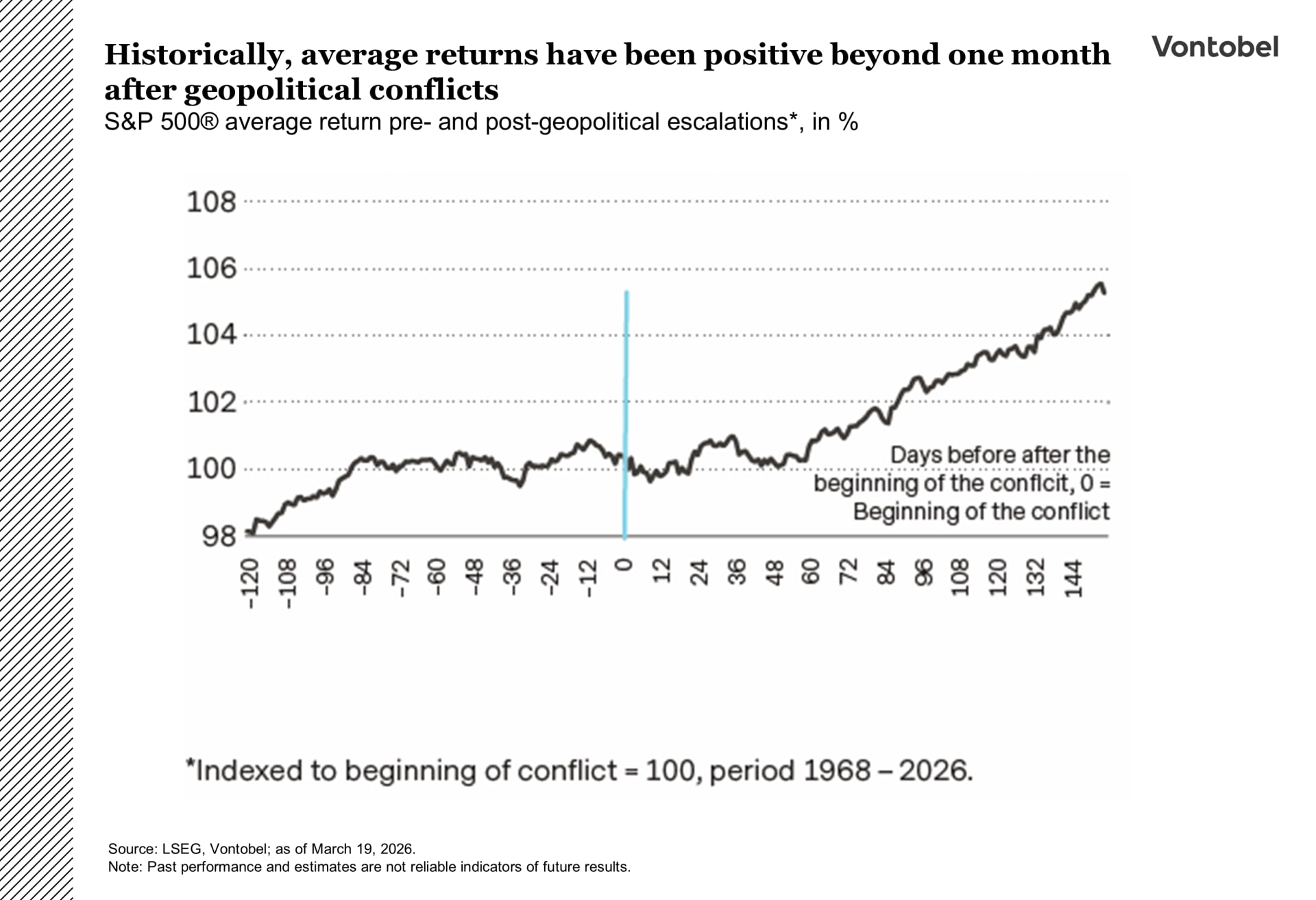

A de-escalation scenario would potentially set up a phased recovery: continued pressure in the first half, especially in the second quarter, followed by anticipation of improvement in the second half and easier year-on-year comparisons into 2027. Historically, stock markets have rebounded once there were credible signs of de-escalation. Global equities are currently down 5 to 10 percent from their early-year peaks, in line with the average length and magnitude of pullbacks observed during geopolitical instability episodes over the past 80 years.

Past patterns suggest markets typically digest geopolitical conflicts relatively quickly, whereby initial drawdowns often recover, on average, within a matter of weeks. Looking at three, six, and nine months after major escalations, forward returns have typically been positive.

Food-flation falling on fertile ground?

When geopolitical tensions in the Middle East escalate into open conflict, the world’s attention usually fixates on the impact on oil prices. But an often overlooked risk is the secondwave shock it can send to global dinner tables.

Agriculture is energy-intensive. When oil prices spike because tankers are stuck or diverted, the cost of running tractors and harvesters climbs—as does the cost of transporting food from exporting hubs like Brazil or the US to the rest of the world. However, the most severe damage happens through natural gas markets.

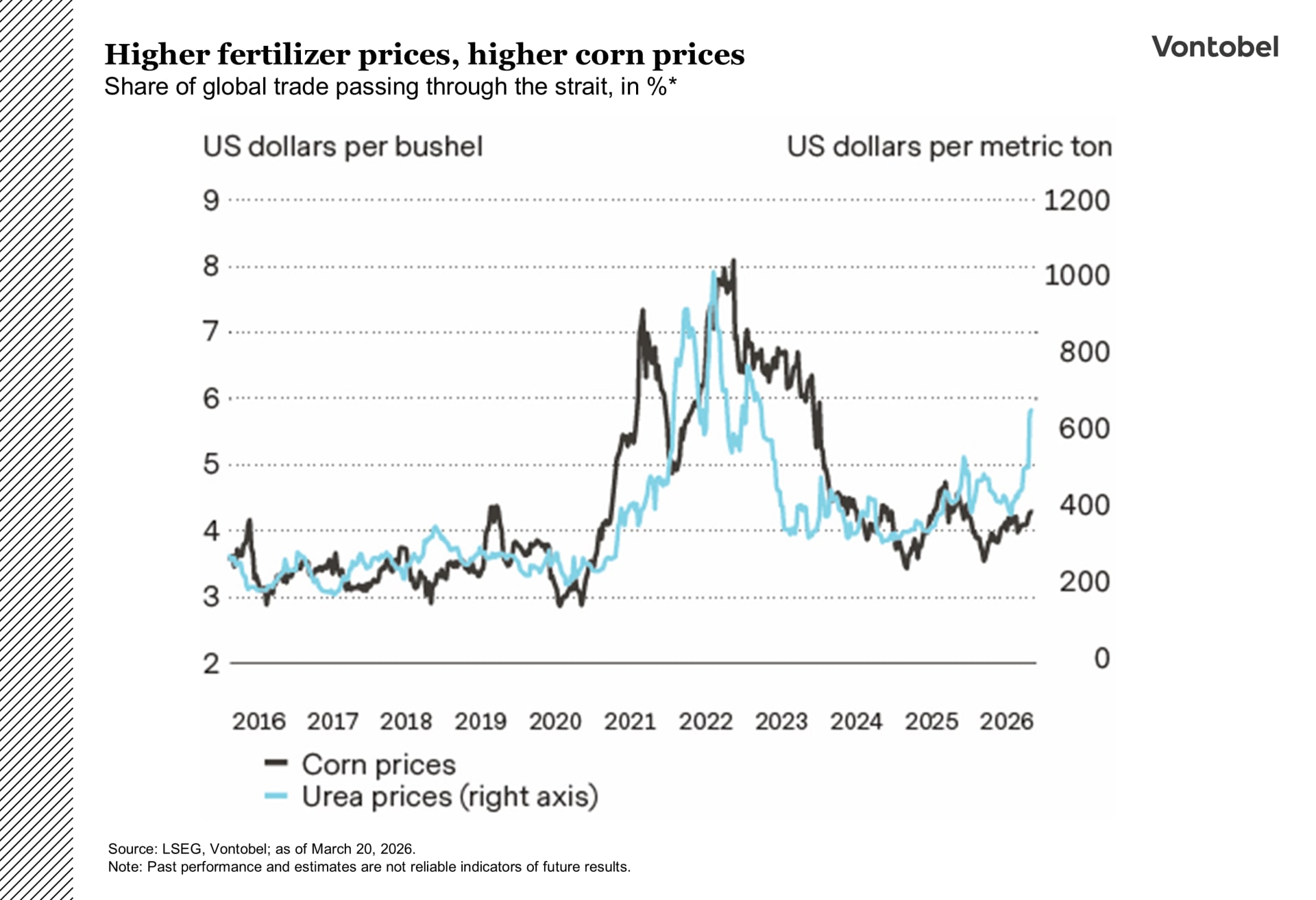

Nitrogen-based fertilizers, such as urea, which support crops responsible for roughly half of the world’s food supply, rely on gas as their primary feedstock. After strikes forced Qatar, a liquefied natural gas heavyweight, to declare force majeure and halt exports, gas prices surged, driving fertilizer prices higher as well. The fertilizer market has been hit two-fold. First, when gas prices surge, fertilizer plants are often forced to scale back production or shut down entirely, as manufacturing becomes economically unviable. Second, the closure of the Strait of Hormuz also left many fertilizer exports sidelined.

Within the grains complex, corn is the most exposed. It is highly fertilizer-intensive, with fertilizer accounting for up to 40 percent of production costs. To put that in perspective, wheat stands at about 30 percent, while soybeans are much lower at 15 percent. While higher fertilizer prices could eventually contribute to rising grain prices (via higher production costs), the largest potential impact on prices may come from reduced supply. Sustained high fertilizer costs may lead farmers to apply less fertilizer, resulting in suboptimal yields. Additionally, high fertilizer prices could prompt farmers to shift acreage away from fertilizer-intensive crops, such as corn, toward less fertilizer-dependent crops like soybeans. This shift could reduce corn supplies and drive up prices.

In this environment, countries that are somewhat “better off” are those that sit on their own energy or mineral reserves. Russia and the US are in a somewhat better position as they possess the domestic natural gas needed to fuel their own production.

Countries like Brazil and India face a more challenging backdrop. Despite being major food producers, they are heavily dependent on imported fertilizers. At the end of the day, higher food prices will also show up differently in inflation data. Developed economies like the US have a relatively low weighting of food in their inflation baskets. But in emerging markets, food can account for 30 to 50 percent of the average household’s spending.

The search for safe havens

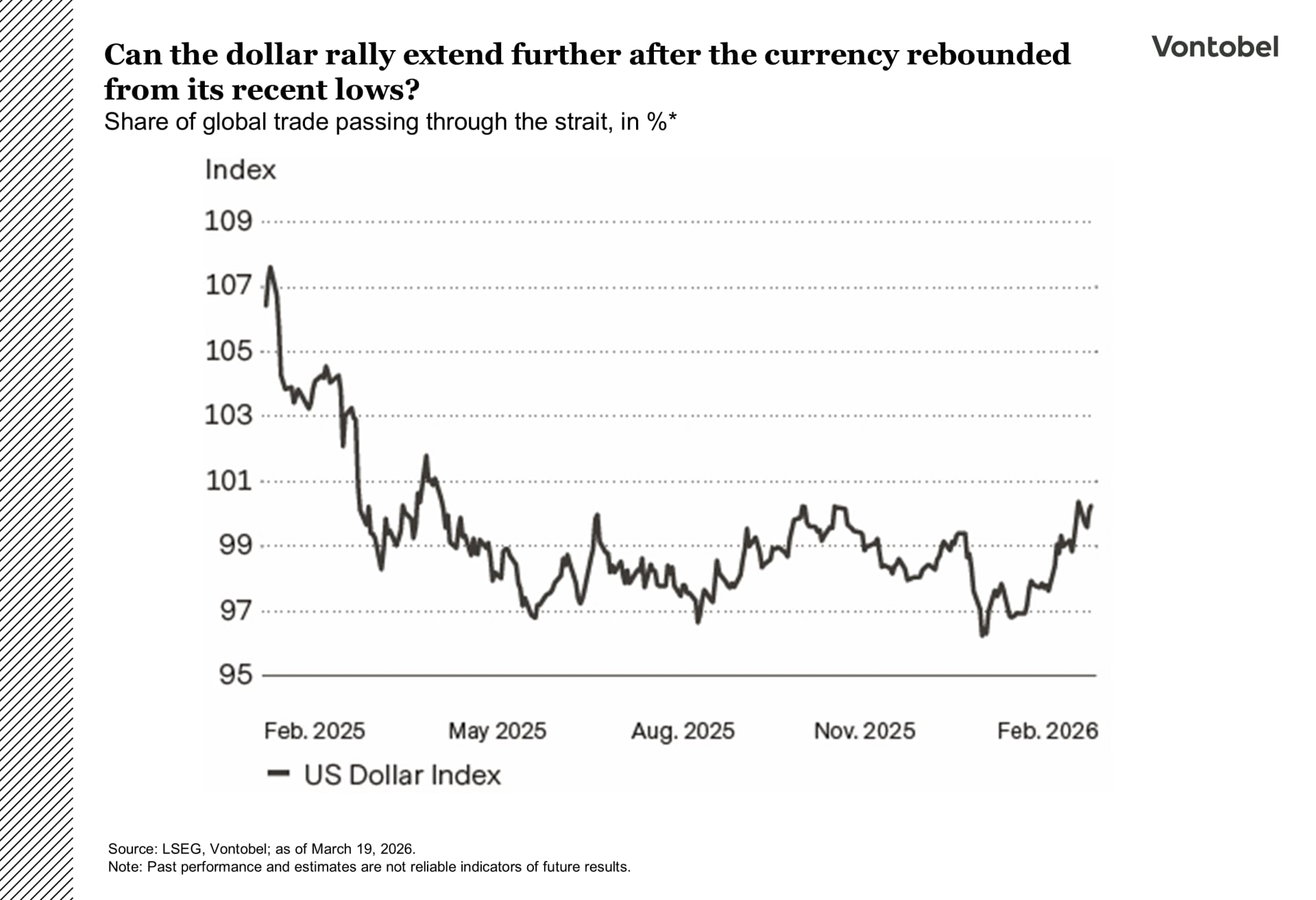

The 2026 bear narrative for the US dollar has been challenged by an evolving macroeconomic backdrop, as geopolitical tensions and higher oil prices have reintroduced two important sources of dollar support.

First, a classic risk-off environment has revived the dollar’s safe-haven appeal. Second, higher energy prices have increased inflation risks, forcing markets to scale back expectations for Fed easing. This combination has pushed up short-end US yields and supported the dollar even as growth shows signs of slowing.

As long as uncertainty remains elevated and oil prices stay firm, the Fed has limited room to cut, which keeps the rate support for the dollar intact.

But that support is mainly driven by the current risk backdrop, not by stronger long-term fundamentals. Once geopolitical risks recede and the focus returns to fundamentals, structural headwinds are likely to reemerge. The US fiscal position remains weak, Treasury supply is high, and external balances have not improved. These factors tend to matter more in stable environments. In the near term, the dollar is supported by risk and rates. Further out, the case for a softer dollar still holds if inflation stabilizes and the Fed eventually resumes easing.

Strong Swiss franc

Elsewhere, the Swiss franc stands out for combining classic safe-haven support with stronger longterm fundamentals, even as policy resistance builds. The franc shares the US dollar’s safe-haven characteristics but rests on firmer foundations. In periods of stress, the franc has historically remained strong, and the current environment is no exception.

Switzerland’s persistent current account surplus, relatively disciplined fiscal policy, and low inflation give the Swiss National Bank (SNB) more flexibility than most central banks and provide the currency with a stronger medium-term anchor. At the same time, that strength comes with an important policy constraint.

The SNB is unlikely to welcome excessive franc appreciation, as it tightens financial conditions and risks pushing inflation even lower. It has already leaned against further franc strength through verbal intervention, explicitly signaling a greater willingness to step into FX markets if moves become too rapid or excessive. The franc is poised to remain supported as long as geopolitical risks abound. Over the medium term, the franc still looks fundamentally strong, but further gains may become harder to sustain if the SNB pushes back more actively.