US banks kick off the Q4 2025 earnings season

While precious metals, such as gold, and US- and European equities had a solid year in 2025, Bitcoin lagged. The US dollar could continue to weaken in 2026 due to the risks associated with Trump's trade and interest rate policies. Since Bitcoin is inversely correlated with the US dollar index, it could serve as a hedge against a weaker dollar in 2026. From an overall market perspective, the S&P 500's fourth quarter of 2025 earnings season begins this week, with seven major US banks set to report their results.

Case of the week: Bitcoin is lagging the “everything rally”

In 2025, both risk assets, such as US and European equities, as well as precious metals, showed solid gains. Surprisingly, cryptocurrencies, including Bitcoin, lagged behind. While the gold price is setting new highs almost weekly, Bitcoin is down 27 percent from its record high in early October 2025. Admittedly, the strong performance in 2024 paved the way for some profit-taking. A flash crash on October 10, 2025, exacerbated the sell-off, contributing to panic selling and the unwinding of highly leveraged positions. Additionally, some investors may have migrated to alternative assets, such as gold or stablecoins.

Trump's policies may ultimately bolster non-US Dollar assets

In 2025, a notable feature of financial markets was their susceptibility to of geopolitical influences. This influence is expected to continue into 2026. The US Supreme Court is expected to soon rule on the legality of Trump’s tariffs. This follows the US Court of Appeals for the Federal Circuit's August 29, 2025, decision that President Trump exceeded his authority under the International Emergency Economic Powers Act (IEEPA) when he imposed certain tariffs. According to Polymarket, bettors estimate only a 26 percent chance that the Supreme Court will rule in favor of Trump's tariffs. Treasury Secretary Bessent has stated that the administration has other options to keep the tariffs in place, even if the court strikes down the IEEPA emergency rule. However, an unfavorable ruling would likely lead to increased uncertainty regarding Trump's trade policy and its implementation. Since tariffs could be considered a tax on consumers, risk assets might benefit if the tariffs are deemed illegal.

US monetary policy is also a hot topic right now. President Trump has openly criticized the current Fed Chairman, Jerome Powell, for his stance on the Fed funds rate. Trump believes the rate should be much lower. Powell’s term ends in May 2026, and many expect Trump to nominate a new candidate who shares his views on interest rate policy. Trump has said he will announce the nomination in early 2026. If investors' expectations shift toward a more dovish US monetary policy and uncertainty increases regarding the Federal Reserve's independence, the US dollar may weaken further. As shown in the graph below, there is an inverse relationship between Bitcoin and the US dollar index.

Bitcoin ($BTCUSD) and US dollar index ($USD), five-year weekly chart

In short, a continued appetite for risk assets and a weaker US dollar could lead to a Bitcoin recovery. However, one overall risk is if market sentiment in currently overvalued equity markets suddenly shifts toward risk aversion.

Although the long-term trend for Bitcoin is negative, the short-term trend has recently turned positive. Currently, Bitcoin is trading above the 20-Day Moving Average (MA20) level, around $90,000.

Bitcoin future (USD), one-year daily chart

Bitcoin future (USD), five-year weekly chart

Related Products

Macro comments

The fourth quarter 2025 reporting season of 2025 begins on Tuesday, January 13, with JPMorgan among the first US S&P 500 companies to publish its results. Six other major US banks will post their interim figures on Wednesday and Thursday of this week.

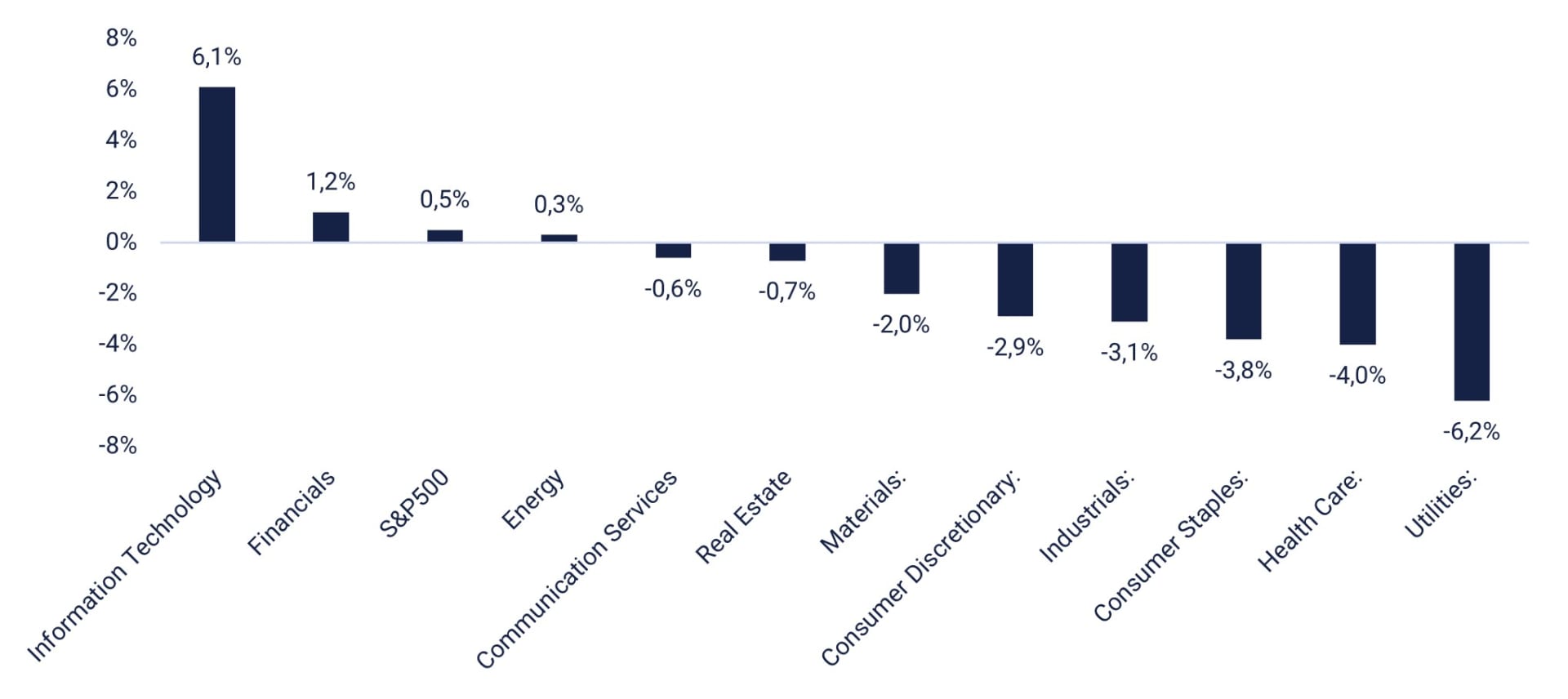

Estimated earnings growth for S&P 500 companies in the fourth quarter of 2025 has increased from 7.2% on September 30 to 8.3%. However, as the chart below shows, only two sectors—Information Technology and Financials—contributed to the expected increase in earnings.

S&P 500: Sector-Level Change in Q4 2025 EPS (September 30 to December 31)

Bank of America, Citigroup, and Wells Fargo are scheduled to release their fourth-quarter 2025 reports on Wednesday, January 14. The release of China's December trade balance will mark the beginning of the macro news flow. A few hours later, the November figures for Swedish industrial orders and household consumption will be released. OPEC will release its monthly oil report. From the US, are expectedthe Producer Price Index and retail sales figures for November, existing home sales figures for December, and weekly oil inventory statistics from the Department of Energy.

On Thursday, January 15, the US interim reporting season continues, with fourth-quarter 2025 results from Goldman Sachs, Morgan Stanley, and BlackRock. Another company releasing its interim earnings on Thursday is Taiwan Semiconductor. On Thursday, the macroeconomic session begins with the release of Statistics Sweden's consumer price index for December, along with UK Gross Domestic Product (GDP) and industrial production figures for November, as well as German wholesale price data for December. Later that morning, France and Spain will release their December consumer price index, along with Germany's full-year 2025 GDP. The Eurozone will publish its trade balance and industrial production figures for November. The US will release November's import prices, initial weekly jobless claims, and the January Empire State Manufacturing Index and Philadelphia Fed Index.

On Friday 16 January ,the Norwegian company Aker BP is scheduled to release its Q4 2025 report.. Turning to the macroeconmic news, Italy's consumer price index for December is worth mentioning. The US will contribute leading indicators for November and industrial figures for December.

Will Europe continue to outperform the US?

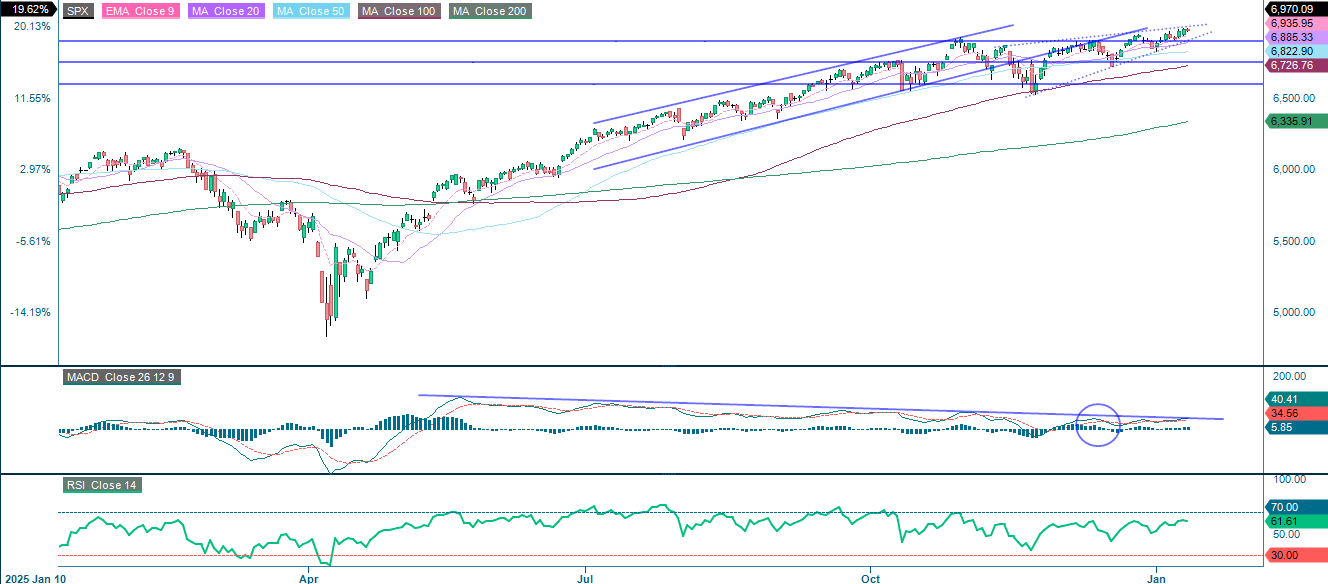

The start of the new trading year has been positive for the S&P 500, though less so than for European equities. Momentum remains positive, and the RSI suggests that further gains are possible to close the gap. However, as the chart below shows, a bearish rising-wedge formation is emerging. If a downside break occurs, the pattern suggests that levels around 6,600 could be reached. On the way down, support is provided by the 50-Day Moving Average (MA50) and 100-Day Moving Average (MA100), which are currently at 6,822 and 6,727, respectively.

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), five-year weekly chart

Related Products

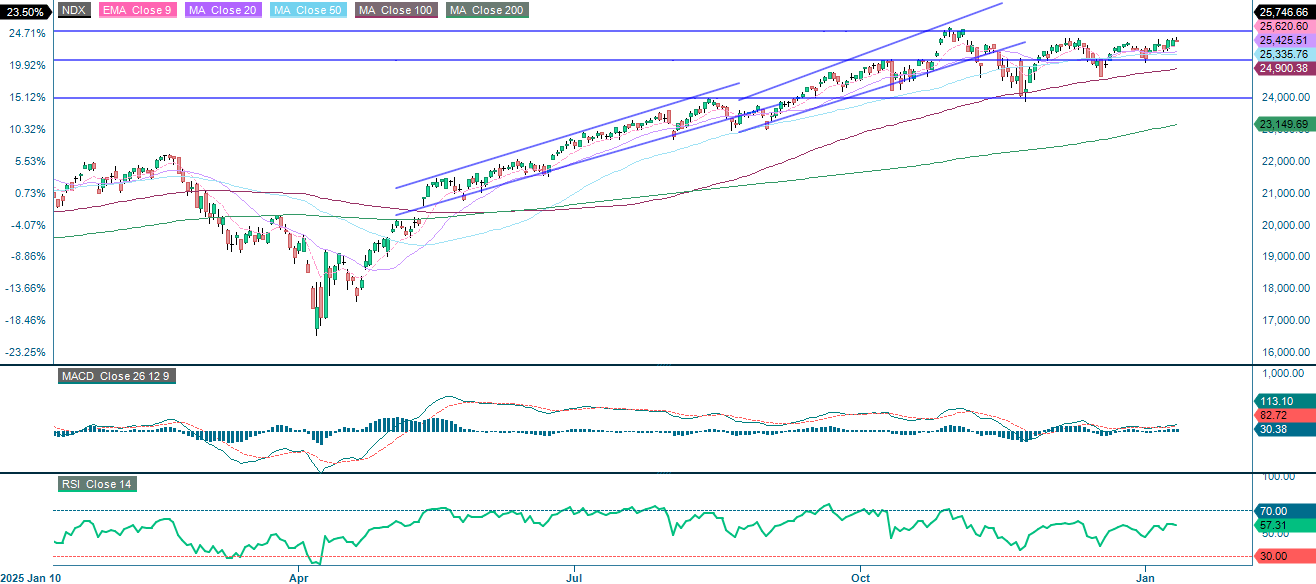

Meanwhile, the NASDAQ-100 has not reached new highs since peaking in October 2022. At the same time, the two-year US Treasury yield is testing resistance. Continued interest rate hikes will likely hinder the index’s ability to rise, and vice versa.

NASDAQ-100 (in USD), one-year daily chart

NASDAQ-100 (in USD), five-year weekly chart

Related Products

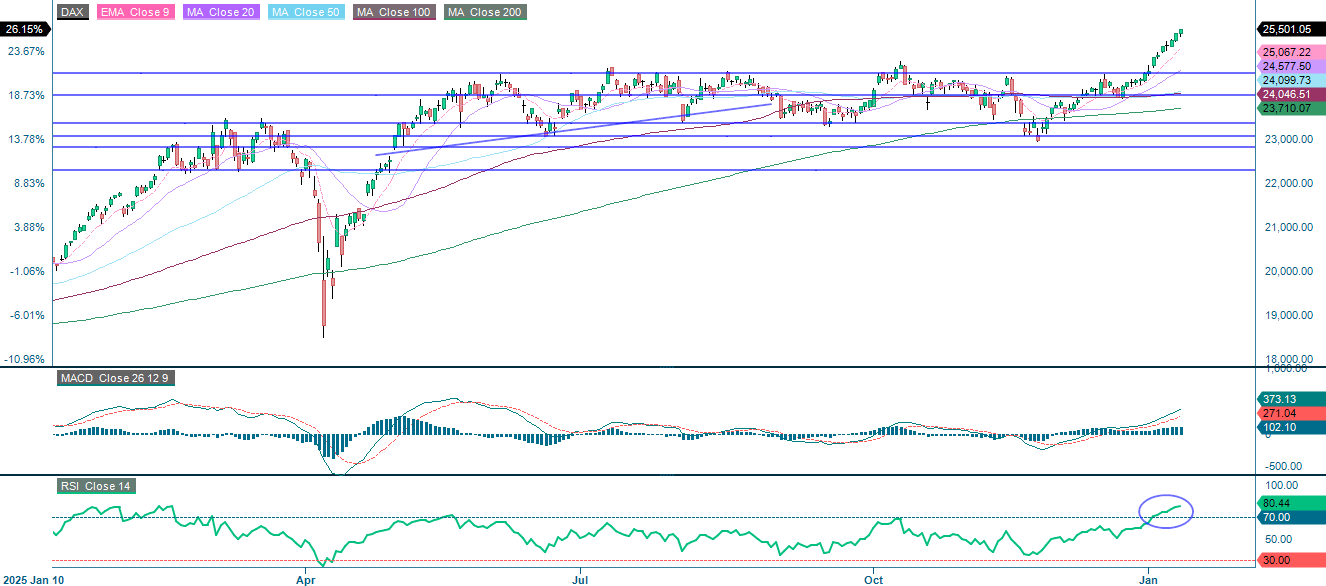

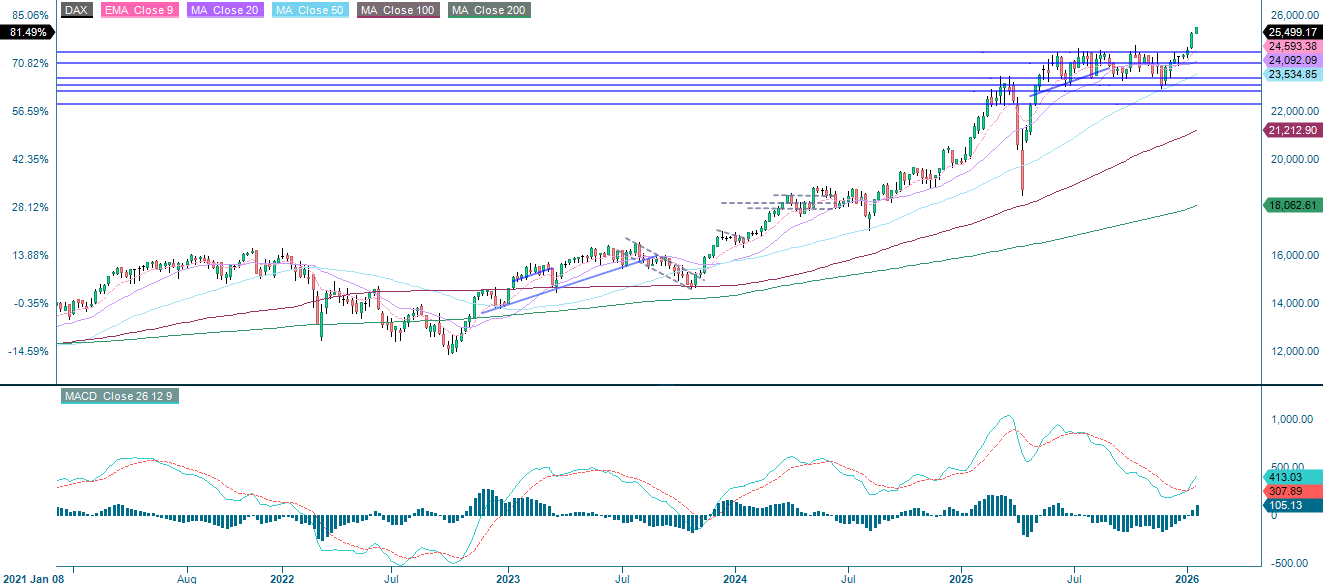

It took until the beginning of the year for the German DAX to break above the 24,500 resistance level. Its strong performance thus far has been bolstered by an improved outlook for the German economy and easing inflation, which has fuelled industrials and other cyclical sectors. However, as the chart below shows, the RSI is currently at overbought levels, suggesting that it may be wise to take some profits. With positive momentum still in place, any forthcoming dips could present opportunities to establish long positions.

DAX (in EUR), one-year daily chart

DAX (in EUR), five-year weekly chart

Related Products

Year-to-date (YTD), the OMXS30's performance lags behind the DAX but outperforms the S&P 500 and the NASDAQ-100. However, the RSI again indicates overbought levels. The index's performance has indeed benefited from Saab, which is up 30% YTD.

OMX30 (in SEK), one-year daily chart

OMX30 (in SEK), five-year weekly chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day Exponential Moving Average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-Day Moving Average

MA50: 50-Day Moving Average

MA100: 100-Day Moving Average

MA200: 200-Day Moving average

MACD: Moving Average Convergence Divergence

N.B.: Please insert the ’General Disclaimer’ and the ‘Risks Disclaimer’ related to the products

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.