Financial Markets Q3 2025: Technology sector led the markets

The third quarter of 2025 was a mixed one for financial markets: stock markets rose, but political uncertainty and trade tensions kept the mood nervous. Technology and artificial intelligence companies in particular were once again at the forefront of price increases, while new tariffs and policy decisions by US President Donald Trump's administration caused uncertainty.

Strong development in the stock market – technology at the forefront

During the third quarter, the technology and artificial intelligence sector continued its rapid growth, , a major trend that has persisted for some time. Large US companies, the so-called Magnificent Seven, accounted for a significant portion of the overall market's return. Several companies exceeded earnings expectations, which increased confidence in the sector's growth.

At the same time, small companies also performed well as investors sought diversification from a market dominated by large companies.

Global markets also saw a fairly positive quarter overall, including in many European and Asian countries.

Related Products

S&P 500 (in USD), 5-year chart

Related Products

Russell 2000 (in USD), 5-year chart

Related Products

DAX (in EUR), 5-year chart

The FED cut interest rates, the ECB held steady

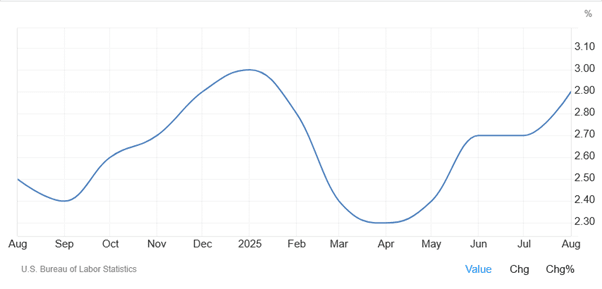

The US Federal Reserve cut interest rates for the first time since December 2024 in Q3. This provided a tailwind for the stock market and provided grounds for a rise. Further interest rate cuts of 0.50 % are expected in Q4. However, a cause for concern for interest rate cuts may be inflation in the US, which has started to rise slightly from the lows of spring 2025.

US inflation, 1-year graph

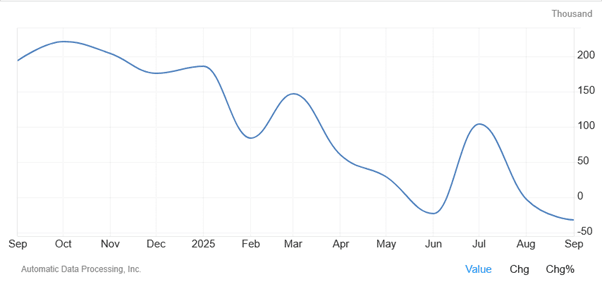

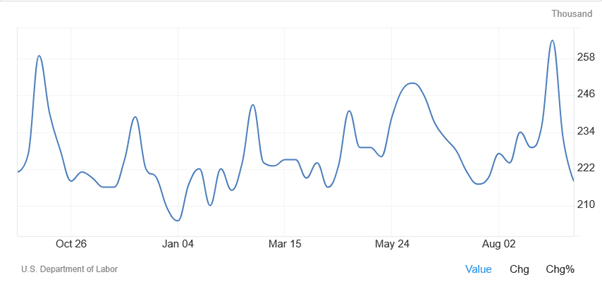

Another important consideration regarding interest rate cuts is the US labor market. The labor market has long remained strong, but the latest figures have shown more pronounced weakness. However, uncertainty in the employment data is introduced by the US government shutdown. The latest unemployment claims figures have not been obtained for this reason, which could introduce uncertainty into the market if the shutdown lasts longer.

US ADP numbers, 1-year graph

US Initial Jobless Claims, 1-year graph

The European Central Bank kept its key interest rates unchanged at 2.15% during Q3. The last rate cut was in June 2025, after which the ECB has kept interest rates unchanged. Inflation in Europe is clearly lower than in the United States.

Euro-area inflation, 1-year graph

Oil and gold in opposite directions

Commodity markets saw a sharp divergence across underlying assets, with oil prices remaining under pressure due to rising production expectations and weaker demand forecasts.

Related Products

Brent Crude Oil (in USD), 5-year chart

Meanwhile, gold and silver have been on a strong rise as investors have sought a safe haven amid political uncertainty and expectationsof lower interest rate expectations.

Related Products

Gold (in USD), 5-year chart

Silver (in USD), 5-year chart

Political uncertainty

Although the economic data has not weakened significantly overall despite the tariffs, the tariff policy imposed by US President Donald Trump has brought uncertainty to the markets. However, the effects may be reflected far into the future, which may cause uncertainty for investors. The transfer of capital to known safe havens, such as gold and silver, is already one sign of this.

European markets have also been nervous, particularly due to the political situation in France. Government instability and budget disputes have caused uncertainty among investors.

Corporate results surprised positively

Analysts' expectations for the third quarter results were cautious, but many companies' reports exceeded these expectations. Technology companies in particular can be singled out as a second boost. These positive results have increased confidence that companies' profitability can withstand a potential slowdown in growth.

Investors' concern: concentrated market

Despite the good performance in Q3, it is important to remember that the majority of the gains came from a small number of large companies, raising questions about the market's vulnerability if the largest companies' prices turn downward.

Summary: strong quarter, but risks remain

In summary, Q3 2025 was favorable for investors, but risks have not disappeared from the markets. Central bank decisions, political tensions and market concentration continue to maintain uncertainty. Investors' attention will now shift to whether the strong momentum continues into the rest of the year or whether we will see a correction.

—

Indicators shown on the graphs:

Simple moving average, 200

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.