Some thoughts about the oil price and oil stocks

Is the oil price high now? And what can explain the decoupling between it and the recent development of oil stocks?

On the list of the world's most traded commodities, we find oil in undisputed first place, ahead of both natural gas, metals, and agricultural “soft” commodities. Oil offers great energy density, and at the same time is relatively easy to store and transport compared to other forms of energy. In addition, it is used to make a number of products. This gives oil a special position in the world economy. Whether a country is an exporter or importer of oil will be significant for the country's balances, and this gives the raw material great political importance. If you add that a cartel (OPEC) controls approx. 1/3 of the supply side and the fact that a couple of the world's largest manufacturers are currently subject to various sanctions, it is easy to understand that oil gets a lot of attention.

High oil prices = high energy costs = higher prices for most things to be transported and produced. Many people have opinions about the oil, but can you say it is expensive now? If so, relative to what? As a technician and fan of quantitative analysis, I have to turn to charts and statistics for answers. Below we see a chart that shows the price of oil over the last 20 years with monthly candlesticks and a logarithmic price scale (to get equal percentage changes over time). The orange curve is a 24-month, or 2-year moving average. The dashed red line is a 48-month (4-year) moving average, and the green and blue lines respectively are a 2 standard deviation Bollinger Band around the latter.

Note: Brent Crude Oil price since 2002 shown with monthly candlesticks. The orange line is a 24 month (2 year) moving average. The dotted red line is a 48 month (4 year) moving average. The chart shows a 2 standard deviation Bollinger Band around this with the green line indicating the upper boundary and the light blue line the lower boundary. Source Infront. Past performance is not a reliable indicator of future results. Prices in USD.

As we can see from the chart, the oil price is now 87 USD/barrel. This is lower than it was 14 years ago in 2008, lower than it was in the years from 2011 to 2015 and 33% lower than the last price peak reached earlier this year. In fact, we see that the price in November has touched the 24-month moving average. If we see it in relation to the 48-month average and a 2 standard deviation band around it, we can conclude that the price is higher than the 4-year average but has fallen back from the movement outside the band. Standard deviation is, as is well known, a statistical measure which in this case illustrates what are "normal" fluctuations. When we are within the band, the prices are per definition not "unusual" from a statistical point of view.

If you add that the chart shows nominal (not inflation-adjusted) prices, and that there has been a lot of inflation since both 2008 and 2011-2015, I will venture to say that oil prices are not unusually high from a technical/quantitative point of view at this point in time.

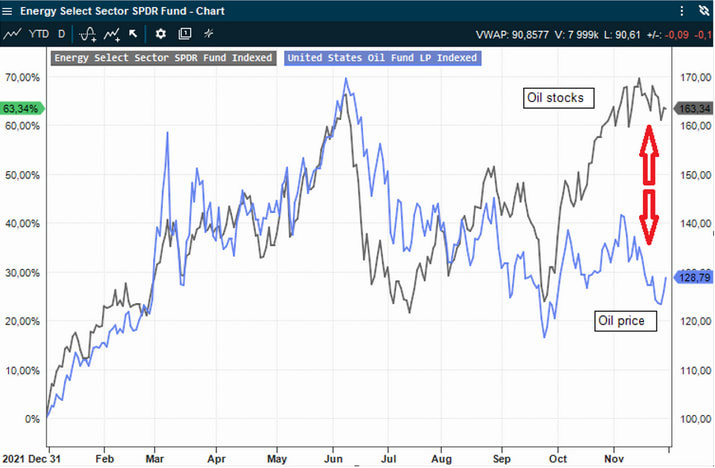

Oil price and oil stocks

The price of oil and the share prices of oil companies are naturally closely linked. In the short term, an overwhelming part of the oil companies' costs are fixed, and the selling price of their oil minus these costs will be a considerable part the companies' profit before tax. You therefore usually see a large co-variation between the fluctuations in the oil price and the stock prices of oil companies. In the longer term, the relationship may be more complicated, but let's stick to the shorter picture here.

The chart below shows the development so far this year of an US ETF that holds a "basket" of crude oil contracts spread over the next 12 months and an ETF that contains the major oil stocks in the United States (Exxon, Chevron etc.). As we can see, they have been moving in lockstep for most of the year, but after the first third of October they started to go their separate ways. The price of oil has fallen back, while oil stocks continued to reach new highs for the year. The gap is now so significant that this is starting to get increased attention in the market.

Oil, together with oil stocks, peaked last summer when the Ukraine unrest was at its worst, and European gas prices also set price records. Since then, oil prices have slipped downwards, while oil stocks have gotten another significant boost. The blue line in the chart above shows a basket/sum of prices distributed over the next 12 months. At the short end, and especially for the American WTI reference oil, the difference is even more pronounced. There, the price actually touched a new annual low last week. If we plot a chart between the WTI spot price and the largest oil stock Exxon, we see that the development is even more extreme than in the chart above:

Related Products

This is not something you see very often. No one has a definitive answer on what’s behind this, but we can make some educated guesses. In general, one can say that unless there is a clear fundamental reason for such a gap to occur, it is often simply due to a trade becoming unusually popular among market players. Fundamentally, I find it difficult to see that so many real changes recently. When it comes to both the oil and oil service sectors, there had been relatively tough times for several years, while the sectors have been unpopular from an ESG point of view. This has led to the sectors' weighting (proportion of) the S&P 500 being close to historic lows. This is a point often made by analysts and bullish investors. Perhaps the energy sector will have many good years ahead of it?

On the other hand, we see that the price of oil itself has started to fall, and that the same arguments were used for nuclear power and uranium until those sectors also peaked earlier this year. Why are oil stocks still hanging high up there in the air? I don't know, but I saw reports last week that Oil/Energy was now the sector most managers were overweight right now. A popular trade, quite simply.

It cannot be ruled out that this will continue, but I see risk in these charts. Either the oil price must start to show a stronger trend relatively soon, or I think it will become more difficult to maintain good momentum in the oil stocks. We'll see. Such gaps or "shark jaws" are usually closed sooner or later.

Disclaimer: After many years in the brokerage industry I started my own business in 2021. I published the book "Paleo Trading: How to trade like a Hunter-Gatherer” and launched Paleo Capital that manages a hedge fund according to the principles described in the book. I emphasize that nothing written on this blog is to be regarded as personal advice or a concrete call to take positions. Everyone must be responsible for their own decisions and familiarize themselves with the products they use.

Risks

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance.