Oil prices at a crossroads after a downturn

After a somewhat volatile stock market session yesterday (Wednesday, March 16), the Fed's interest rate announcement was made. The rate hikes increased to one per meeting and seven policy rate hikes in total. It caused long-term U.S. treasury rates to rise while the short-term rates declined, indicating that the fixed-income market began to discount a recession.

The Fed faces a challenge to curb inflation with higher interest rates. For three weeks, war is also going on in eastern Europe. On top of that, the Fed has committed itself to shrink its balance sheet. This equation is not going to add up. During the press conference, stock market investors took note of Fed chief Powell saying that the risk of a recession is low. But Powell also admitted that Fed is behind the curb and chasing. Fixed-income investors have historically been better in their forecasts of changes in the economic cycle than both the Fed and the stock market.

S&P500 Index (in USD) from August 2, 2021, to March 17, 2022

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

The S&P500 index closed at daily highs on Wednesday evening. According to indications, there is a wall of put options expiring on Friday on the New York Stock Exchange. Therefore, the big banks are interested in keeping the market up until then. So, the U.S. stock market could fall back again early next week.

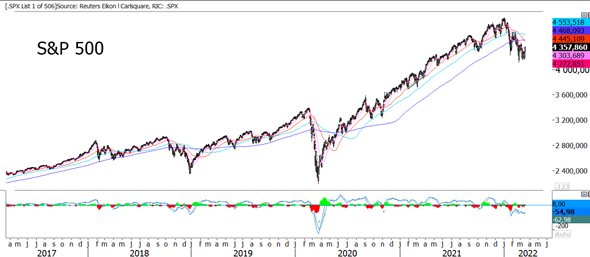

S&P500 Index (in USD), five-year-chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results

The Russian offensive in Ukraine seems to have stalled. It is due to stiff Ukrainian resistance and Russian maintenance problems. Military analysts believe that Russia will not be able to mount a full-scale offensive for more than another ten days. Then it will have to slow down or withdraw. An alternative could be a low-scale war along the current front lines. For the stock market, this is positive news. Both the oil and gold prices have plummeted.

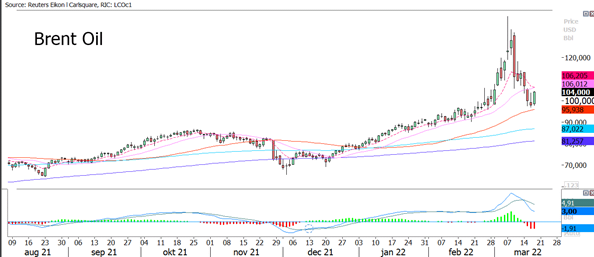

Brent oil price (in USD) from August 9, 2021, to March 17, 2022

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Products

Oil prices are falling, despite the disappearance of Russia's share of the world market. However, we expect China to buy discounted oil in Russia right now, with the quid pro quo of supplying Russia with weapons, although it is susceptible on China's part.

We better understand the rebound in the gold price than in oil. After all, Russia is the world's second-largest oil producer, with 13% of world production by 2020. Large volumes need to come from other countries to achieve the same balance as before.

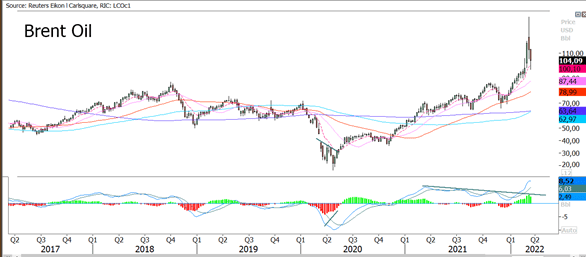

There also appears to be some form of technical support at current lower oil prices. Although this support is still somewhat vague, there is a possible rising secondary line from where the recent price rise began.

Brent oil price (in USD), weekly-five-year-chart

Source: Refinitiv Eikon and Carlsquare. Note: Past performance is not a reliable indicator of future results.

Risks

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance.

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Product costs:

Product and possible financing costs reduce the value of the products.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.