Friday's PMI figures could help guide markets

This week's case is Saab, which should benefit from the announcement at the Munich Security Conference that Europe can no longer trust the United States and must quickly build up its own military defence. Saab is also undervalued relative to peers such as BAE Systems and Rheinmetall. On Friday 21st February, the G7 Purchasing Mangers’ Index (PMI) for February may provide some insight into the current state of the global economy.

Case of the week: Geopolitical tensions light the fuse for Saab

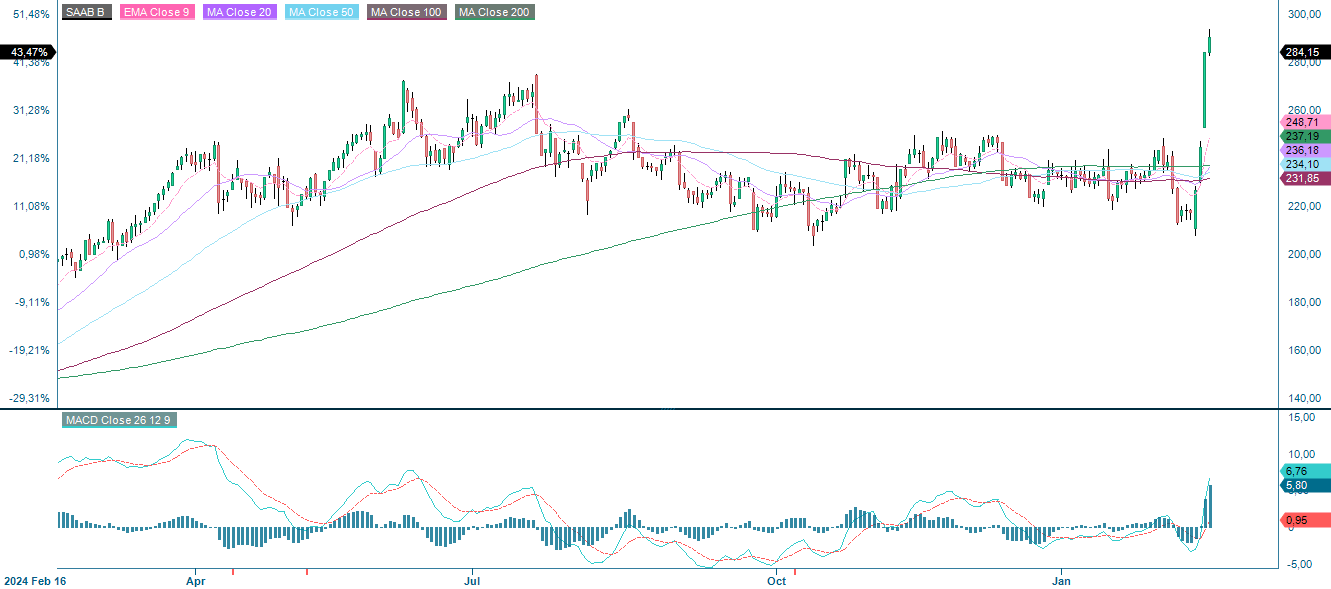

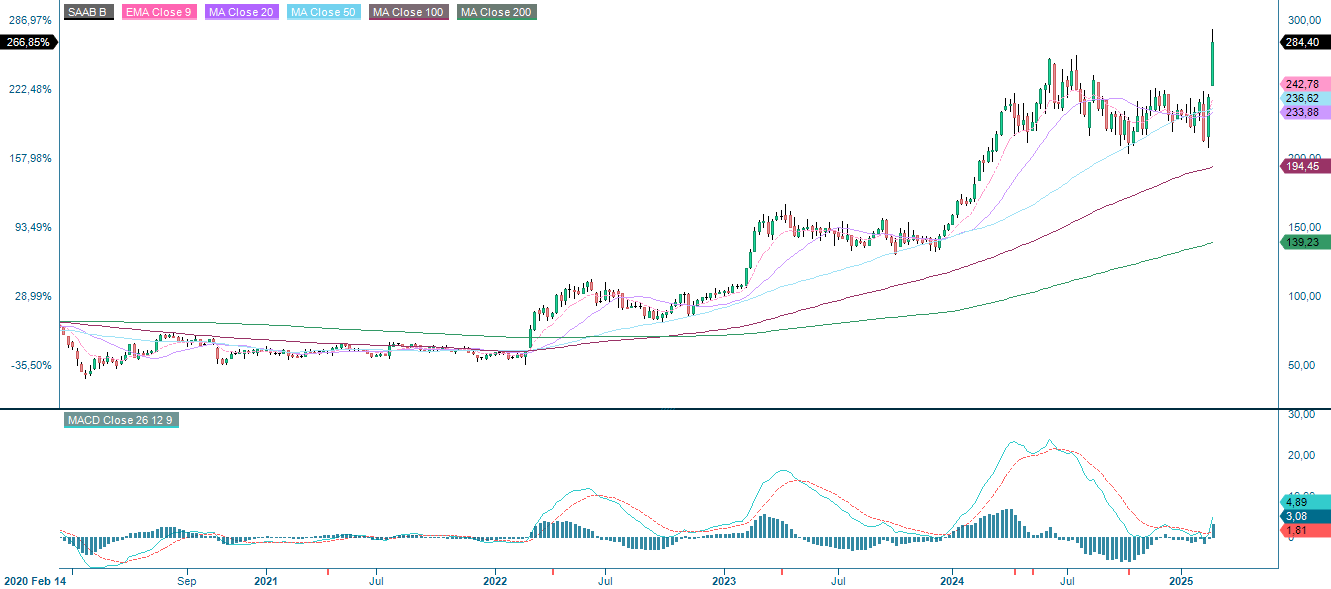

Saab AB, Sweden's leading aerospace and defence company, represents a compelling investment opportunity due to its strong growth prospects and relative undervaluation compared to its peers. Saab has solid financial fundamentals and a growing order book. As global defence spending increases, particularly in Europe, the company is well positioned to benefit from military modernisation efforts.

The war in Ukraine and the major developments at last week's security conference in Munich, which raised concerns about the US commitment to European security, have significantly altered defence policy across the continent. This has led to increased military budgets, with Sweden's NATO (North Atlantic Treaty Organization) membership and wider European rearmament efforts further driving demand for Saab's defence solutions. The company specialises in advanced military technology, including Gripen fighter jets, radar and surveillance systems and naval defence solutions. A recent SEK 13 billion contract with Poland for airborne early warning radar systems underlines Saab's growing role in European security. Similar procurement trends among NATO countries indicate continued demand for its products, underpinning its long-term growth prospects

Despite strong sales growth and a robust order book, Saab's shares remain undervalued compared with other European and US defence companies. Its price-to-earnings ratio lags peers such as BAE Systems and Rheinmetall, despite comparable financial performance. Analysts say this could present a buying opportunity for investors who believe Saab's valuation does not yet reflect its earnings potential. The company has consistently reported revenue growth, supported by increasing defence procurement. Ongoing investments in innovation - especially in electronic warfare, autonomous systems and next-generation fighter jet technology - further strengthen its competitive position.

While Saab is well positioned for growth, it faces several risks. The defence industry is highly dependent on government contracts, making it vulnerable to potential delays, policy changes or budget reallocations. Competition from large global defence companies such as Lockheed Martin, Northrop Grumman and Airbus poses challenges in securing contracts. Cost management is another factor to watch. Saab's recent hiring spree and investments in production capacity are necessary to meet growing demand, but if revenue growth does not keep pace with rising expenses, profit margins could be affected. Currency fluctuations also remain a concern, as the volatility of the Swedish krona has impacted Saab's share performance in the past.

Saab AB remains a strategically important but undervalued player in the global defence sector. The ongoing rearmament of European nations, Sweden's integration into NATO and increasing military procurement are creating a strong demand environment for its products. While some analysts caution about valuation and cost pressures, Saab's long-term growth potential remains compelling. Given the current geopolitical climate and rising defence budgets, the company is likely to remain a key supplier to European and global militaries. For investors looking to gain exposure to the defence sector, Saab offers an attractive opportunity, especially if the market continues to underestimate its earnings potential.

Saab (SEK), one-year daily chart

Saab (SEK), five-year weekly chart

Macro comments

For Q4 2024 (with 77% of S&P500 companies reporting on Friday 14 February), 76% of companies reported a positive EPS (Earnings Per Share) surprise, while 62% of companies have reported a positive revenue surprise, according to Earnings Insight. For Q1 2025, 42 S&P500 companies have issued negative EPS guidance, and 33 S&P500 companies have issued positive earnings guidance. Wall Street analysts are quite optimistic about earnings growth for S&P500 companies in 2025.

66% of the Q4 results of the 72 OMX companies that reported their Q4 results between 23 January and 14 February were better than expected. In terms of sales, 78% were positive surprises. 13 OMX companies reported new orders where consensus expectations existed, and here eleven, or 85%, were better than expected.

On the macroeconomic calendar for today, Wednesday 19 February, we have Japan's trade balance for December and China's house prices for January. A few hours later, the UK's CPI (Consumer Price Index) and PPI (Producer Price Index) for January will be released, followed by the Eurozone's current account balance for December. From the US, we get Housing Starts for January, Redbook Retail Sales, weekly data, oil inventories (American Petroleum Institute), weekly statistics and the Federal Reserve (FED) minutes from the FOMC (Federal Open Market Committee) meeting on 28th and 29th January. Interim reports will be released by Castellum and Scandic Hotels (which will also host a capital markets day) in the Nordics, Analog Devices and Carvana in the US, BAE Systems, Glencore and HSBC in continental Europe and Rio Tinto (UK/Australia).

On Thursday, 20th February, the macroeconomic agenda will include German PPI for January and from the Euro-zone the Household Confidence Indicator for February. From the US, we get the Philadelphia Fed index for February, initial jobless claims and leading indicators for January. The Q4 earnings season continues with results from Walmart and Airbus Group in the US, as well as Chinese giant Alibaba.

On Friday, 21 February, the macroeconomic agenda is dominated by the February PMIs from Japan, India, France, Germany, Italy, the Eurozone, the UK and the US. Japan's CPI for January will also be released in the early morning. From the UK, we have CBI industrial trends for February. The US will also contribute with existing home sales for January and the Michigan index for February. On Friday there will be interim reports from Elekta and Sagax in Sweden.

Is long Nasdaq 100 a winning trade?

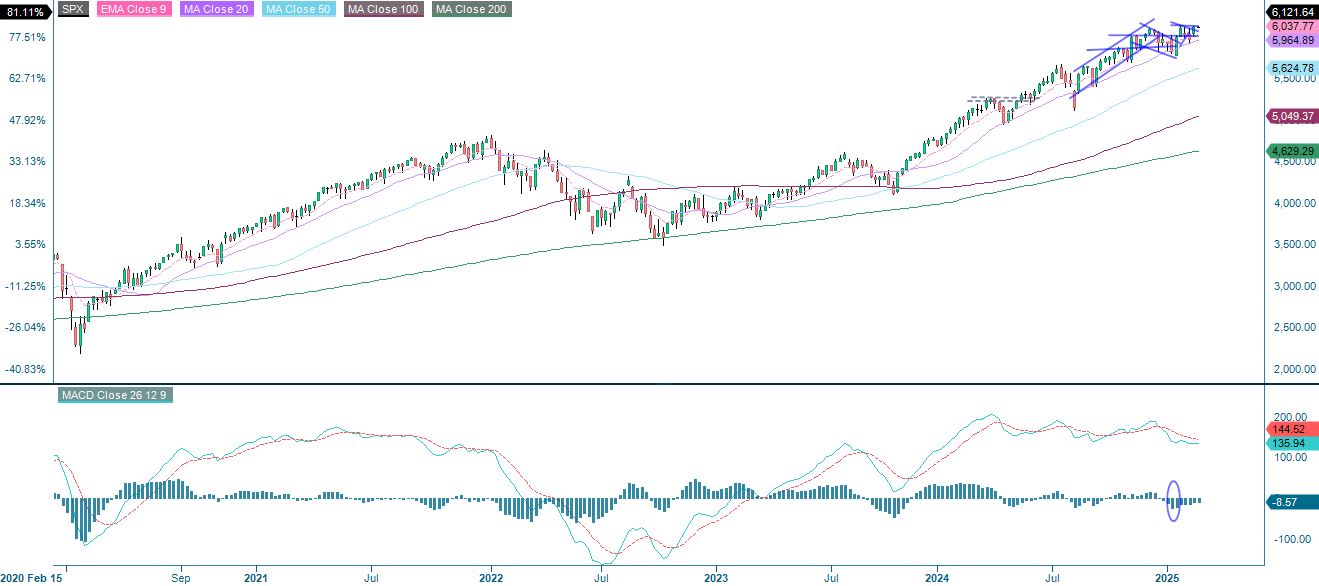

The S&P 500 is close to resistance at 6,120. Meanwhile, the US 10 year Treasury yield is in a bearish trend close to resistance at the MA100. A break to the downside could act as a trigger for equities and push the S&P 500 to new highs. The market is also awaiting Nvidia's interim report next week.

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), weekly five-year chart

Meanwhile, the Nasdaq 100 has broken out of a neutral wedge formation. The formation has a target level of 22,840. Falling yields will help the Nasdaq.

Nasdaq 100 (in USD), one-year daily chart

Nasdaq 100 (in USD), weekly five-year chart

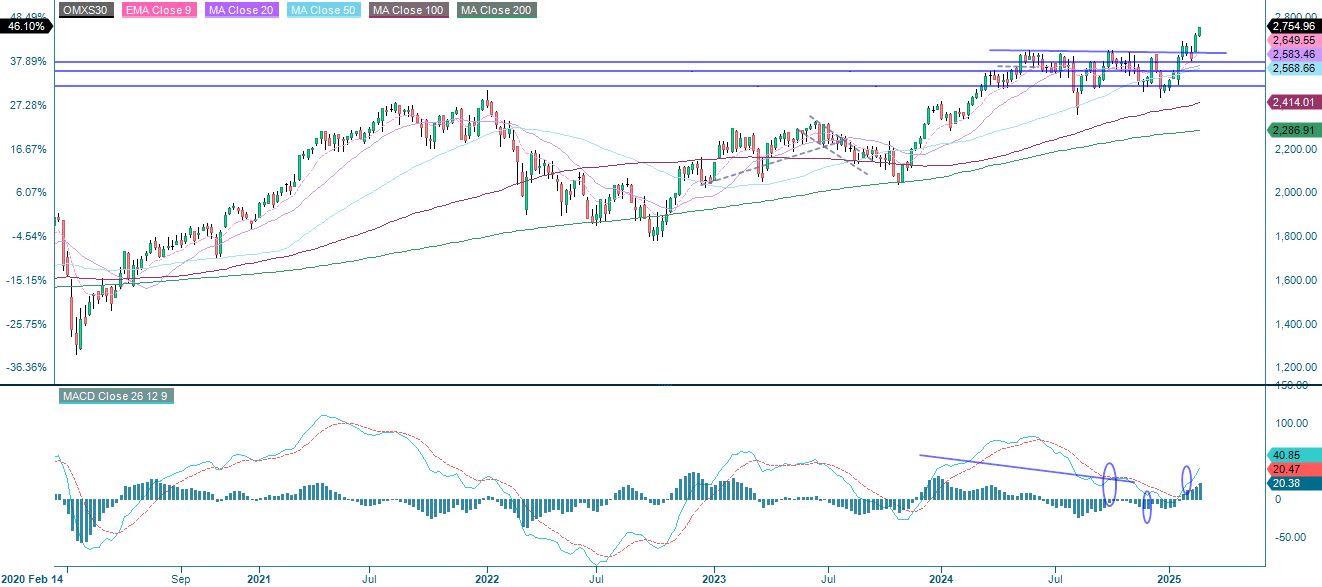

The OMXS30 has broken above the bullish pennant that we pointed out in the previous trading note. The 2,750 level has also been reached, while the Relative Strength Index (RSI) is overbought. Taking some profits at this point may not be a bad idea.

OMXS30 (in SEK), one-year daily chart

OMXS30 (in SEK), weekly five-year chart

The German DAX is on a roll and is currently up almost 15% since the start of the year. Meanwhile, the OMXS30 is up almost 11% year-to-date. Therefore, going long OMXS30 and short DAX may not be an unattractive spread.

DAX (in EUR), one-year daily chart

DAX (in EUR), weekly five-year chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.