US banks in focus as Q4 2024 season kicks off

We return to the Nordic banking sector this week with a case on Danske Bank. Since Trump's election as US president in November 2024, bank shares have outperformed broader equity indices in both the US and Europe. This is due to the expected more favorable guidelines for US banks, but also to higher interest rates. Danske Bank's shares have one of the most attractive valuations in the Nordic banking sector.

Case of the week: Still room for higher valuation of Nordic bank stocks

Following the US presidential election, the financial sector, especially banks, has been a relative winner. This is true for the US, but also for the European banks.

Drivers of the relative outperformance include the recent rise in interest rates, low valuation multiples relative to the broader market and expectations of a more lenient regulatory environment under the incoming Trump administration. The latter could include more relaxed capital requirements and possibly a more open attitude towards Mergers & Acquisitions (M&A) in the banking sector compared to the Biden administration, which implemented stricter guidelines in 2023. In addition, banks and other financials are arguably less exposed to the impact of tariffs.

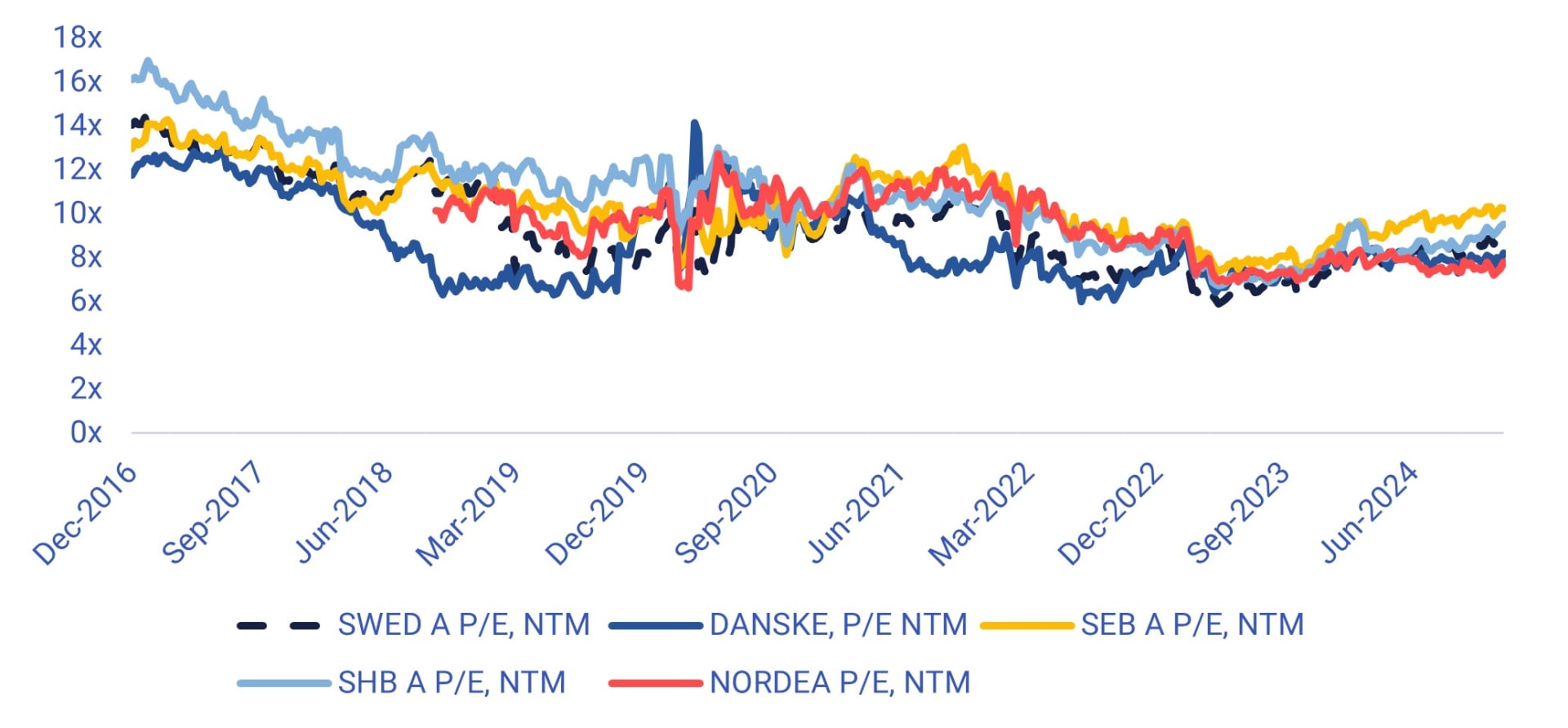

Nordic banks are among the most profitable in Europe. Valuations also appear to be low by historical standards (see the historical development of forward NTM, next twelve months) Price to Earnings (P/E) multiples below). However, in the short to medium term, there is some concern about how lower interest rates will affect net interest income, especially for Swedish banks.

NTM P/E multiples for Nordic banks

In relative terms, Danske Bank is expected to have a more favourable earnings momentum to 2025 than most of its Nordic peers. This is partly due to better loan growth in Denmark than, for example, in Sweden. According to consensus estimates compiled by S&P Capital IQ, Danske Bank has one of the lowest valuations in the Nordic region. The shares currently trade at a price/tangible book of 1.03x and a P/E NTM of 8.2x.

The Danske Bank share has had a moderately positive performance in 2024 and is currently in an uptrend. The Q4 2024 report will be due on 7 February 2025.

Danske Bank (DKK), one-year daily chart

Danske Bank (DKK), five-year weekly chart

Macro comments

256,000 new jobs were created in the US in December according to non-farm payrolls figures published on Friday 10th January. This compares to expectations of 154,000 new jobs in December and 212,000 new jobs in November. US Treasury yields rose by 8-9 basis points as a result of the strong employment data. The S&P500 and Nasdaq fell by 1.5% and 1.6% respectively during Friday's trading session.

The US fourth-quarter reporting season kicks off on Wednesday 15 January with results from Citigroup, Goldman Sachs, JP Morgan and Wells Fargo. Bank of America, Morgan Stanley and United Health follow on Thursday 16 January, as does Taiwan Semiconductor Manufacturing from Asia.

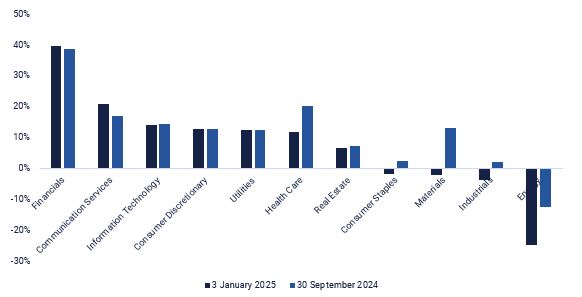

For Q4 2024, earnings growth for S&P500 companies is forecast at 10.9%, down from 14.5% as of 30 September 2024, according to Earnings Insight. By sector, the S&P500 Financials sector is forecast to have the highest earnings growth in Q4 2024, with earnings growth of 39%, while the Energy sector is expected to be the worst performer, with estimated earnings declines of 25% in Q4 2024. Within the Financials sector, there is a wide divergence, with Banks expected to deliver earnings growth of 187% in Q4 2024, followed by Consumer Financials and Capital Markets with expected earnings growth of 35% and 33% respectively. At the other end of the spectrum are Financial Services, where profits are expected to grow by only 12% in Q4 2024, and Insurance, where profits are expected to fall by 11% in Q4 2024.

S&P500 Earnings Growth Estimate by Sector (Year-over-Year) (in %): Q4 2024

Statistics Sweden will release December 2024 Consumer Price Index (CPI) on Wednesday 15th of Januray 2025 at 8.00 CET. Meanwhile, UK CPI and Producer Price Index (PPI) for December and German wholesale prices for December 2024 are due. France and Spain will also release CPI for December an hour or so later. Before lunch, German Q4 Gross Domestic Product (GDP) and industrial production for November are due from the Eurozone, as well as two oil reports from the International Energy Agency (IEA) and OPEC respectively. The US will contribute with its CPI for December 2024, which will be important given last Friday's strong Non-Farm Payroll figure. The Empire Manufacturing Index for January and weekly oil inventories from the Department of Energy (DOE) are also due from the US on Wednesday 15th of January

On Thursday, 16th January, the macroeconomic agenda will begin with UK GDP and Industrial Production for November. This will be followed by German and Italian CPI for December and the Euro-zone trade balance for November. The minutes of the European Central Bank (ECB) meeting on 12th December 2024 will also be published. From the US, we get December 2024 retail sales and import prices, January Philadelphia Fed index, November jobless claims, November inventories of unsold goods and January NAHB (National Associations of Home Builders) housing market index.

On Friday morning, 17th January, we get a block of statistics from China with house prices, industrial production, retail sales, investment and unemployment for December as well as GDP for Q4.

From Europe, we get UK retail sales for December as well as the eurozone current account for November and CPI for December. The US will contribute with housing starts and industrial production for December.

Risk remains on the downside – will the DAX follow?

On Monday 13th January the S&P 500 rallied nicely from its opening close just above the MA100. The strength continues in current trading. A break above MA20, currently at 5,935, improves the odds of a test of the December 2024 highs. However, the risk remains to the downside - should markets turn sour, the downside is relatively large compared to the potential upside.

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), weekly five-year chart

The Nasdaq 100 has also bounced nicely off support. A break above 21,120 would reduce the risk. However, the MACD recently gave a sell signal, and the risk remains to the downside. A break below 20,590, followed by a break below the MA100, currently at 20436, and the MA200, currently at 19, 625 could be next.

Nasdaq 100 (in USD), one-year daily chart

Nasdaq 100 (in USD), weekly five-year chart

The German DAX is stuck above the MA20. However, as the risk for US equities remains to the downside, a specific trigger is likely to be needed to give the DAX fresh impetus.

DAX (in EUR), one-year daily chart

DAX (in EUR), weekly five-year chart

Meanwhile, the OMXS30 is currently attempting to regain the MA20 and the MA50.

OMXS30 (in SEK), one-year daily chart

OMXS30 (in SEK), weekly five-year chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.