DAX recaptures some of the outperformance of US indices

Novo Nordisk's shares have lost around 30% of their value since the summer peak this year but have recovered somewhat in recent weeks. This is since the Q3 report was better than the Q2 report, but also because the market is now awaiting the results of the phase III study (REDEFINE-1) of another of the company's obesity programs, CagriSema, in December. US equity indices have outperformed their European counterparts by 17-18% since August. Over the past week, however, the German DAX index has caught up somewhat with US equity indices.

Case of the week: Will obesity heavyweight Novo rise to the challenge?

Danish pharmaceutical giant Novo Nordisk remains Europe's largest company by market capitalisation, valued at around USD 470 billion. As such, it has a significant influence on investor sentiment in the region. It is also the world leader in the fast-growing obesity sector.

The shares are down around 30% from their summer peak before recovering somewhat in recent weeks. Weaker-than-expected Q2 results and concerns that the Federal Trade Commission (FTC) would block main owner Novo Holdings' purchase of US contract manufacturer Catalent have weighed on the shares. The latter deal addresses capacity constraints in the production of GLP-1 agonists, the active ingredient in Novo's main diabetes and obesity drugs. In contrast, the Q3 report was a relief as sales of core products such as the weight loss drug Wegovy grew faster than expected.

But arguably the most important news of the year is still to come. In December we expect top-line results from a phase III study (REDEFINE-1) of another obesity programme, CagriSema - a combination of the current bestseller semaglutide and the experimental obesity drug cagrilinitide. The aim is to achieve greater weight loss than existing drugs on the market, such as Lilly's Zepbound. Specifically, Novo has said it expects to see a 25 per cent weight loss after 68 weeks of treatment in people with obesity in the REDEFINE-1 trial. Lilly has shown around 21% for Zepbound (72 weeks of treatment) in clinical trials. In an earlier phase II study, CagriSema showed an encouraging 15.6% weight loss after 32 weeks of treatment, albeit in a slightly different patient population (type 2 diabetics with obesity).

More recently, competitor Amgen reported phase II results for its experimental monthly weight-loss injection MariTide. Overweight or obese patients taking MariTide lost an average of 20% of their body weight after one year at the highest dose. Further clinical development is needed, but investors seemed disappointed by the results. It demonstrates the high bar for efficacy and safety set for new obesity drugs in development.

The Novo share will likely move significantly depending on the results. Currently, it is still in bear territory. From the charts, there are no strong signs of a pending reversal yet.

Novo Nordisk A/S B (NOVO B) (DKK), one-year daily chart

Novo Nordisk A/S B (NOVO B) (DKK), five-year weekly chart

However, a positive outcome in REDEFINE-1 could quickly change the narrative and a move of +10-15% seems possible. Previous clinical results and Novo's confidence on the Q3 earnings call provide some reason for optimism (although we note that the outcome was still unknown to Novo's management at the time). If the results are mixed or worse, especially if Novo reports unexpected adverse safety and tolerability events, there is likely to be further downside in the short term.

Macro comments

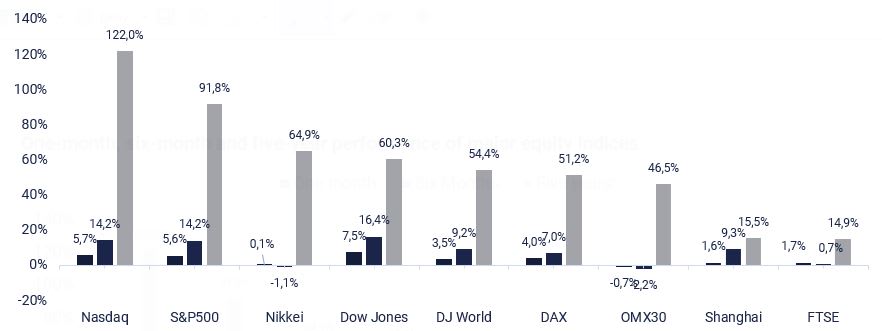

During November, the US stock market index continued to pull away from the European stock market index, a movement that has been ongoing since August. The gap between the S&P500 and Eurostoxx and the Nordic stock market index has widened to around 17-18% since August. However, last week the German DAX and the OMX30 and OMX Nordic 40 indices caught up somewhat with the US indices.

One-month, six-month and five-year performance of major equity indices

The agenda for Wednesday, 4 December, is dominated by the November Service Purchasing Managers’ Indices (PMI) from Japan, China, Sweden, Spain, Italy, France, Germany, the euro area, the UK and the US. The eurozone will also release its November Producer Price Index (PPI). From the US, we also get Automatic Data Processing (ADP) private employment and industrial orders for November, as well as oil inventories (Department of Energy, DOE), weekly statistics and the Beige Book. Clas Ohlsson will present an interim report and sales figures for November. There will also be monthly sales figures from Volvo Cars.

On Thursday, 5 December, the macroeconomic agenda includes Swedish Consumer Price Index (CPI) for November, German industrial orders and Eurozone retail sales for October, and from the US, Continuing jobless claims for November, the trade balance for October and initial jobless claims. Thursday will also see the release of Norwegian traffic figures for November.

Friday the 6th of December begins with Japanese household consumption in October. It continues with the German trade balance and industrial production for October. Before lunch we get Eurozone Gross Domestic Product (GDP) and employment for the third quarter. Today's most important figure will be the US Non-Farm Payrolls for November, where expectations are that 160,000 new jobs were created in November. Before the end of the day we will also get the US Michigan index for December. In the Nordic region, 6th December is Finland's National Day, which means that the Helsinki Stock Exchange will be closed for trading.

The return of the DAX, while the OMXS30 has some catching up to do

The S&P 500 is trading close to sideways, lacking any triggers to decide a new direction. Let the trend be your friend, they say, but keep an eye on the MA20, currently at 5,973. A break below and levels around 5,840 could be next.

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), weekly five-year chart

The Nasdaq 100 is testing the previous high. A further drop in yields could support a break to the upside. On the downside, keep an eye on the MA20, currently at 20,849. A break below this level could see 20,675 as the next target.

Nasdaq 100 (in USD), one-year daily chart

Nasdaq 100 (in USD), weekly five-year chart

The DAX has broken out of its descending trend channel and is currently trading at new highs on the back of falling yields. Momentum is positive and rising. Looking at the Relative Strength Index (RSI), it appears that there is still some energy left despite the strong movement of the past few days. However, if the index runs out of steam, the first support level on the downside is at 19,660.

DAX (in EUR), one-year daily chart

DAX (in EUR), weekly five-year chart

The OMXS is lagging but is currently trading above the MA50. This means that OMXS may have some catching up to do with the other indices. But with little technology in the index - the catch-up is not obvious.

OMXS30 (in SEK), one-year daily chart

OMXS30 (in SEK), weekly five-year chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.