Bi-Weekly Commodity Insight: M&A mania

Profit-taking has characterised the commodities market since our last visit. The S&P GSCI broad commodity index is trading down and the previously red-hot market seems to have cooled off. However, the decline has been followed by another market, the M&A market, coming back to life. Join us as we delve into the growth ambitions of BHP and ConocoPhillips this week!

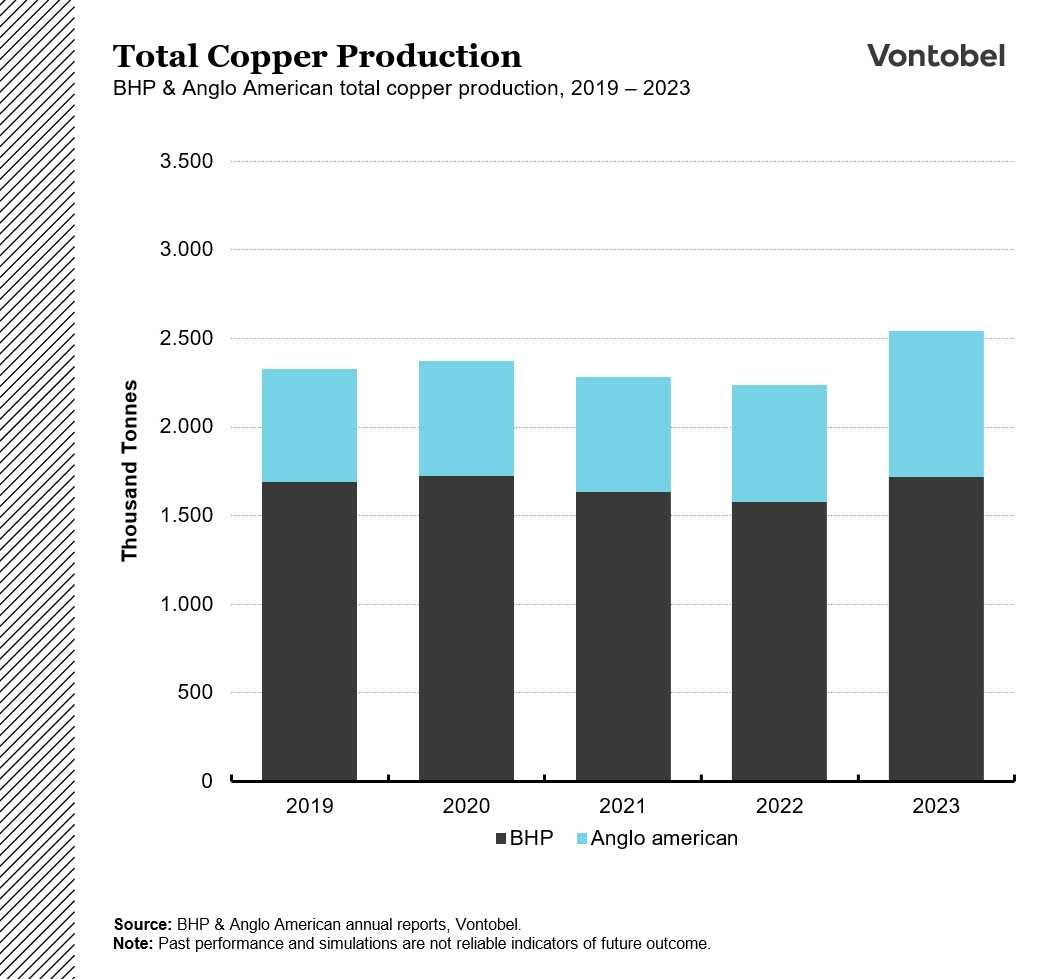

A giant, not least in copper

The world's largest mining company is BHP, an Australian-based company founded in 1885 that has grown to become the world's second largest producer of copper. However, its growth ambitions do not seem to have waned, as in mid-April the company made a bid for Anglo American, the world's 13th largest mining company according to CompaniesMarketcap.

The bid comes in the wake of increased interest in copper. The red metal is one of the most important components in electronics, with demand expected to grow strongly as a result of the energy transition and the electrification of society. It seems obvious, therefore, why a company like BHP would want to grow in the sector with a bid for copper-heavy Anglo American. Together, the companies would have accounted for about 10 per cent of world copper production, according to Bloomberg.

During week 22, the bid fell apart. BHP backed out of the bid after Anglo American had repeatedly rejected various alternatives. The reason? BHP asked Anglo to spin off less profitable subsidiaries in the event of a takeover, a condition that ultimately proved too much for Anglo.

The copper price has fallen back below USD 10 000/tonne since we last visited the metal. However, copper is still near 5-year highs, and above the 50 and 200 moving averages.

Activity in the oil sector

It is not only in the mining sector that there has been talk of acquisitions, oil companies have also been active on that front. On 29 May, oil giant ConocoPhilips, one of the largest in the US, announced that it had acquired fellow sector competitor Marathon oil. The acquisition is done with equity and represents a premium from the 28 March close of 14.7%.

The acquisition widens the gap from British petroleum in terms of market cap and means that ConocoPhillips is closing in, albeit slightly, on the giants Exxon and Chevron. With the buyout, ConocoPhillips is growing its market share in US shale oil.

The price of oil (WTI) continued to fall in week 22, with a barrel of oil now trading below USD 80. The price has broken down below the moving average 50 and is at the moving average 200 which acts as support.

Risks

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Product costs:

Product and possible financing costs reduce the value of the products.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.