Lowered S&P EPS estimates

This week's case concerns the FTSE index, which we believe offers stability given that many of its constituent companies operate in the pharmaceutical, food and beverage, and financial sectors. Although S&P 500 companies reported strong results for the first quarter of 2025, Wall Street analysts have significantly lowered their earnings estimates for Q2 – Q4 2025. From a technical analysis perspective, the S&P 500 and the NASDAQ-100 appear to be stronger than the DAX and the OMX.

Case of the week: FTSE offers stability in troubled times

Ahead of Monday, June 2, increased tension in talks about new tariffs between the US and China dampened the stock market sentiment. US Treasury Secretary Scott Bessent argued that the negotiations had reached a stalemate, while President Trump claimed China had violated previous agreements, including those involving delivery of rare minerals and magnets.

Higher tariffs between the US and the rest of the world will reduce global GDP (Gross Domestic Product). Above all, Trump's directives, which change at least weekly, have put the world's companies in a state of uncertainty. In such circumstances, it would be irrational to make any investment decisions relating to capital expenditure, such as the construction of new plants for example.

Looking at performance for main equity indices over the past month and year-to-date, the German DAX index has performed by far the best. The reason for this is unclear, but perhaps the stock market is starting to anticipate a ceasefire between Russia and Ukraine. However, for German industry to benefit, sanctions on trade with Russia would need to be lifted, which does not seem likely in our view.

One-month, one-year, and five-year performance of equity indices ranked by last month

Of the major equity indices shown in the graph above, the second-best performer is the FTSE (London, UK) index. Unlike the DAX and OMX, the FTSE is primarily composed of companies in the pharmaceutical, food and beverage, and financial sectors. Some major FTSE companies also operate in the energy sector, with Shell ranking third in terms of market weighting among FTSE constituents. Relx, ranked fifth, is a British information and analytics company.

The top 15 FTSE index constituencies, ranked by market capitalisation (in GBP)

Pharmaceutical companies are concerned about the US market and prices, which may come under pressure during Trump's term. It will take time to implement any major changes in this area, though. Higher tariffs are not likely to have a significant impact, as the largest pharmaceutical companies already have local factories. Pharmaceutical companies also have higher profit margins than most other industries, making them less sensitive to higher tariffs.

Larger food companies, which typically have strong brands, should be able to withstand a period of lower GDP growth relatively unscathed. Food companies are also considered to be in the most defensive sector amongst investors, possibly alongside utilities and similar industries. An example of the latter can be found among the larger FTSE companies in the form of National Grid, the UK's national electricity network.

Banks and financial companies tend to remain profitable during recessions, particularly in lending, though perhaps less so in investment banking.

However, commodity-related companies and those in the mining sector should continue to perform weakly for as long as the current recession and uncertainty surrounding US tariffs persist.

FTSE 100-index (in GBP), one-year daily chart

FTSE 100-index (in GBP), five-year weekly chart

Macro comments

For Q1 of 2025, 98% of S&P 500 companies have reported results. Of these, 78% reported a positive earnings per share (EPS) surprise and 64% reported a positive revenue surprise. However, according to Earnings Insight, the expected profit growth rate has been sharply revised down for Q2–Q4 of 2025 since 3 January 2025, as can be seen in the graph below. The forward-looking price-to-earnings (P/E) ratio valuation is currently 21.3 times, which is 7% and 16% higher than the five- and ten-year average P/E ratios, respectively.

Expected earnings growth for S&P 500 companies in each quarter of 2025

On Wednesday 4 June, Volvo Cars will release its May volume sales figures, while Autoliv and Swedbank will host their respective Capital Markets Days. In terms of macroeconomic news, Wednesday will see the release of the May services PMI (Purschasing Mangers’ Index) figures for Japan, Sweden, Spain, Italy, France, Germany, the Eurozone, the UK and the US. From the US, we will also receive the ADP private employment report for May, the weekly oil inventory report (Department of Energy), and the Fed Beige Book. The Bank of Canada will issue an interest rate statement too.

On Thursday 5 June, we will receive a traffic report for May from Norwegian.Early on Thursday morning, we will receive the Caixin Services PMI for May from China. A few hours later, SCB will publish Sweden's CPI (Consumer Price Index) in May and the balance of payments for Q1. About the same time, Germany will release industrial orders and the eurozone will publish PPI (Producer Price Index), both for April. The ECB (European Central Bank) will announce a rate decision after lunch. From the US, we will receive Challenger layoff statistics for May, the April trade balance and weekly initial jobless claims. Broadcom, a US-based multinational manufacturer of semiconductor and infrastructure software products, is expected to publish its interim report on Thursday.

Friday 6 June is Sweden's National Day, so the Stockholm Stock Exchange will be closed for trading. Japan will kick off Friday's macro agenda with household consumption figures for April. A few hours later, Germany will release its trade balance and industrial production figures for April, followed by France's industrial production figures for the same month. From the eurozone, we will receive Q1 GDP and employment figures, as well as April's retail sales figures. Finally, the most important figures of the week will be published in North America: the US's nonfarm payroll figures for May.

Awaiting an upside break in the S&P 500 while DAX is losing momentum

As the chart below shows, since mid-April the S&P 500 has been consolidating just below the resistance level of 5,965, testing it multiple times without breaking out. However, the index is trading above the rising EMA9 and MA20. Meanwhile, the pattern of higher lows remains intact, suggesting that the bulls are defending dips. The next step may be a break on the upside and the previous top from early 2025. Note also that the MACD has generated a buy signal in the weekly chart.

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), five-year weekly chart

As can be seen from the Nasdaq 100 chart below, the index has broken above key resistance, forming higher highs and higher lows. This, alongside the fact that the index is trading above all its moving averages, is a bullish sign, and previous tops from early 2025 appear to be on the cards. Additionally, the weekly chart shows that MACD has generated a buy signal.

NASDAQ-100 (in USD), one-year daily chart

NASDAQ-100 (in USD), five-year weekly chart

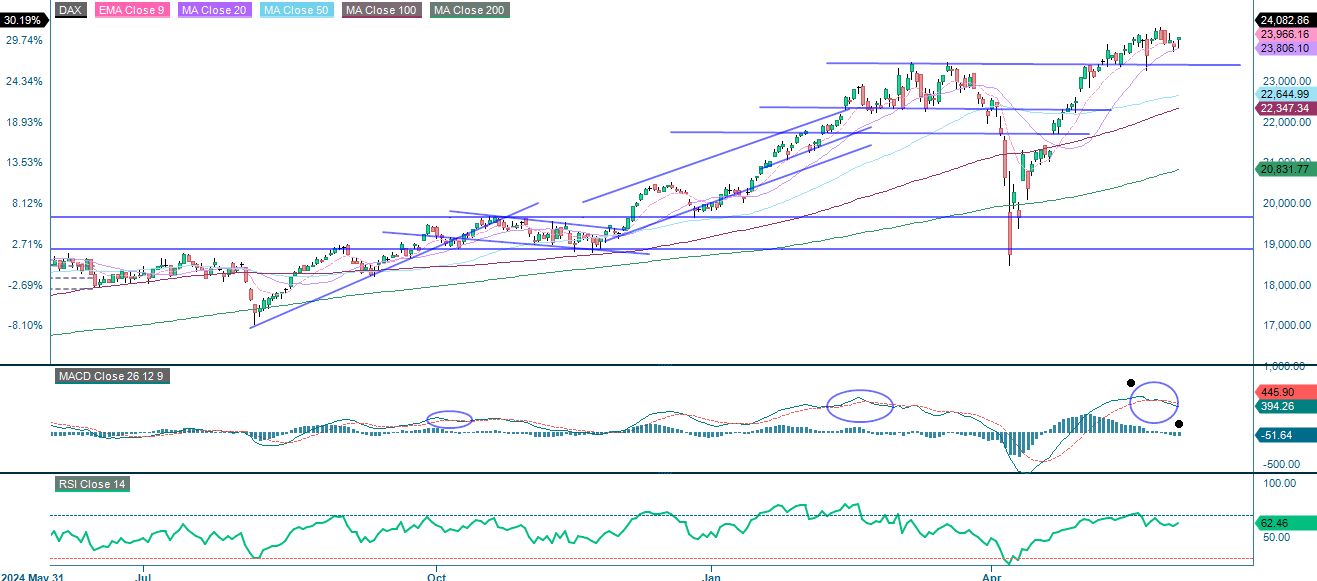

In Europe, the DAX is losing momentum. This is evident from the fact that MACD has generated a soft sell signal. This is also evident in the loss of momentum for EMA9, which is now sloping downwards. A break below the MA20, which is currently just above 23,800, could be next, followed by a fall to 23,400.

DAX (in EUR), one-year daily chart

DAX (in EUR), five-year weekly chart

OMXS30 is under pressure, partly due to a strong SEK. Note the MACD, which has generated a soft sell signal. The next step could be a break below 2,480 and 2,400.

OMX30 (in SEK), one-year daily chart

OMX30 (in SEK), five-year weekly chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.