Unlimited Turbos

Unlimited Turbos, also called Open-End Knock-out Warrants, allow investors to participate disproportionately in the performance of an underlying. The leverage effect results from the fact that less capital has to be invested than for an investment in the respective underlying. Investors can speculate on a rising or falling underlying with a small capital investment. These products can be used to speculate on various asset classes such as shares, indices, commodities, precious metals, interest rate instruments or currency pairs.

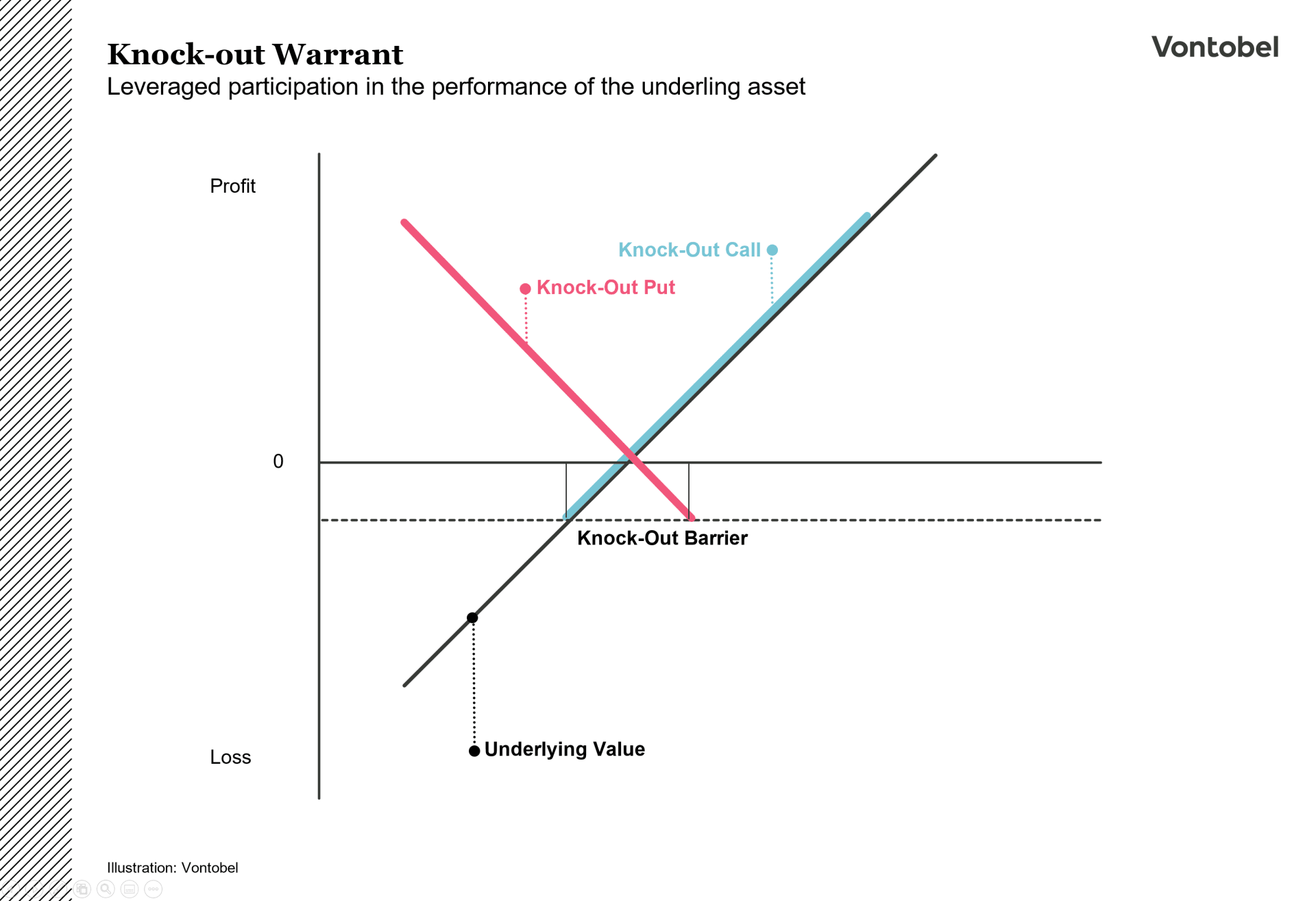

How these products work

Unlimited Turbos (Open-End Knock-out Warrants) disproportionately reflect the performance of an underlying due to their leverage effect. Compared to a direct investment in an underlying, this product requires a lower capital investment. This creates a leverage effect. Investors finance only part of the price of the underlying asset, while the issuer covers the rest. In return, the product incurs financing costs. This allows investors to participate in the performance of the underlying, while only a fraction of the capital is required compared to a direct investment.

Unlimited Turbos offer a high degree of transparency, as the price can be derived directly from the underlying. Basically, the intrinsic value of the product is formed by the difference between the current price of the underlying and the strike of the product. The ratio must also be taken into account.

The lower the difference between the current price of the underlying and strike price, the greater the leverage. A smaller difference also means a closer approach to the knock-out barrier, which is associated with a higher risk.

Special features

Investors can speculate on rising prices with call products or on falling prices with put products. Unlimited Turbos are available with open-end maturity. These products may be subject to a premium in addition to the intrinsic value. In the case of products without a fixed term, only the risk premium is taken into account by a premium, as the financing costs are included in the daily adjustment of the strike for these products.

Compared to classic warrants and futures, Unlimited Turbos have special features. In contrast to classic warrants, volatility plays only a minor role. In addition, compared to classic warrants, Unlimited Turbos have no time value. In contrast to futures, the maximum loss is limited to the capital invested, which means that there is no obligation to make additional payments.

The risks of this product category must also be mentioned. The leverage works in both directions. This can lead to disproportionate gains, but also corresponding losses. Furthermore, Unlimited Turbos (Open-End Knock-out Warrants) are equipped with a knock-out barrier. If the underlying reaches this barrier, the product immediately expires worthless. In such a case, an investor suffers a total loss of the capital invested.

Cost

In order to achieve the leverage effect in the product, the strike price is financed. Costs are incurred for this, which are reflected in the form of financing costs in the amount of the money market interest rate (reference interest rate) and a financing spread. For products without a fixed term (open-end), the costs are reflected in a daily adjustment of the strike price.

Wide choice of underlyings

For investors, Unlimited Turbos open up a diverse selection of investable asset classes. Disproportionate participation through this product category is possible for shares, indices, commodities, precious metals, interest rate instruments and currency pairs.

Hedging of existing positions

Unlimited Turbos can also be used to hedge existing positions. Investors can use Unlimited Turbos to protect their existing portfolio against a possible price decline and losses by, for example, supplementing an existing (long) portfolio that is benefitting from a price increase in the portfolio's components with an opposing (short) position via Unlimited Turbos. The hedge takes effect immediately after the purchase. The hedge immediately ends when the knock-out barrier is reached.

Benefits

· Volatility plays only a minor role compared to classic warrants

· Capital investment is lower than with a direct investment in the underlying asset

· Allows participation in rising or falling prices of the underlying

· Pricing is easy to understand

· Various asset classes are available

Risks

· Market risk of the underlying

· Leverage works in both directions

· Disproportionate loss up to total loss possible

· Currency risk if the currency of the underlying differs from the product currency

· Issuer risk (default of the issuer)

· Issuer's ordinary right of termination for open-end products

What influence does volatility have on an Knock-out Warrant?

Changes in the implied volatility of the underlying only have a minimal or no impact on the price development of the this product type. The pricing is therefore transparent and easy to understand from the product parameters.

What happens when the knock-out barrier is reached?

If the price of the underlying reaches or falls below the knock-out barrier during the observation period, the Knock-out Warrant expires worthless immediately. The knock-out barrier is continuously monitored from the initial fixing date.

A knock-out event for a Knock-out Warrant occurs if the price of the respective underlying touches or falls below the current knock-out barrier at any time during the trading hours of the underlying on the reference exchange or fixing point (continuous observation). In the case of a put Unlimited Turbo / Knock-out Warrant, a knock-out event is triggered by the knock-out barrier being touched or exceeded.

Can these products also be knocked out outside the trading hours of the product?

A distinction must be made here between the trading hours of the product and the underlying. The products are listed and can be bought or sold during regular trading hours. Depending on the type of underlying, different trading hours may apply. It should be noted, for example, that a knock-out event on foreign exchange can happen almost anytime, as the underlying currency pairs are traded practically worldwide. Thus, the knock-out event may occur without the investor being able to sell the product in his or her country. Investors should therefore find out about the trading hours of the underlying before buying the product.

A share pays a dividend. How does a distribution affect an Knock-out Warrant?

The price of a share is adjusted by the amount of the dividend on the ex-dividend date. A similar process is carried out on an Knock-out Warrant.

In the case of a call product, the net dividend is deducted from the strike price on the ex-dividend day of a share. The net dividend takes into account the tax factor of any dividend payment.

In the case of a put product, an adjustment is also made. However, the gross dividend is taken into account here. The strike price is the increased by the gross dividend.

What does premium mean?

In the case of an Knock-out Warrant, a premium may be charged in addition to the intrinsic value. The premium represents risk premium for products with open-end maturity

The risk premium serves to hedge the so-called gap risk and liquidity risk. The gap risk describes the issuer's risk that the hedge cannot be liquidated at the strike price in the event of a knock-out event. The liquidity risk reflects the tradability of the underlying.

An important component of an Knock-out Warrant is the knock-out barrier. Does the knock-out barrier change over time?

In the case of an open-end product, the knock-out barrier is adjusted at the end of each adjustment date. An adjustment day is any day from Monday to Friday after the initial fixing day. A daily adjustment is made to take into account the issuer's financing costs.

In practice, an adjustment of the knock-out barrier means an increase of the knock-out barrier for call products and a reduction of the knock-out barrier for put products.

What happens in the case of a Knock-out Warrant with a futures contract as underlying if the underlying future reaches its maturity?

Future contracts have a fixed maturity. For a product without a fixed maturity (open-end), the underlying must therefore be replaced in order to be able to ensure the continuation of the product.

In the case of a call product, the issuer removes the previously valid contract and replaces it with a longer-dated contract. This exchange is also called a "rollover".

Such an exchange also occurs in the case of a short product. The short position of the previous contract is closed by a purchase position and a new short position in the longer-running contract is built up again.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Product costs:

Product and possible financing costs reduce the value of the products.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.