Focus on US inflation and the ECB

This week's case is Nordea, which, like its Swedish banking peers, beat analysts' earnings forecasts during the Q3 reporting season. But while the banks have performed better than or in line with the OMX-index, Nordea has lagged the index this year, despite offering an 8% dividend yield. The most important events on the macro agenda this week will be the US Consumer Price Index (CPI) and Producer Price Index (PPI) figures on Wednesday and Thursday, followed by the European Central Bank’s (ECB) interest rate announcement on Thursday 12th.

Case of the week: 8% yield makes Nordea attractive

The S&P500 index outperformed the Eurostoxx and Nordic indices by around 17-18% from August to November this year. One explanation for the outperformance of the US indices can be found in the Q3 earnings results, where 75% of the S&P500 companies delivered positive earnings surprises, but only 46% of the Swedish OMX companies.

In contrast, the four large Nordic banks (Swedbank, Handelsbanken, SEB and Nordea) beat analysts' estimates in their Q3 reports by 21%, 12%, 11% and 5% on earnings and revenues respectively.

There is a perception among analysts that Nordic banks' profits should have peaked with the higher interest rates that were in place until the end of 2023. Put simply, higher interest rates have allowed banks to charge higher interest margins and now interest rates are on their way down.

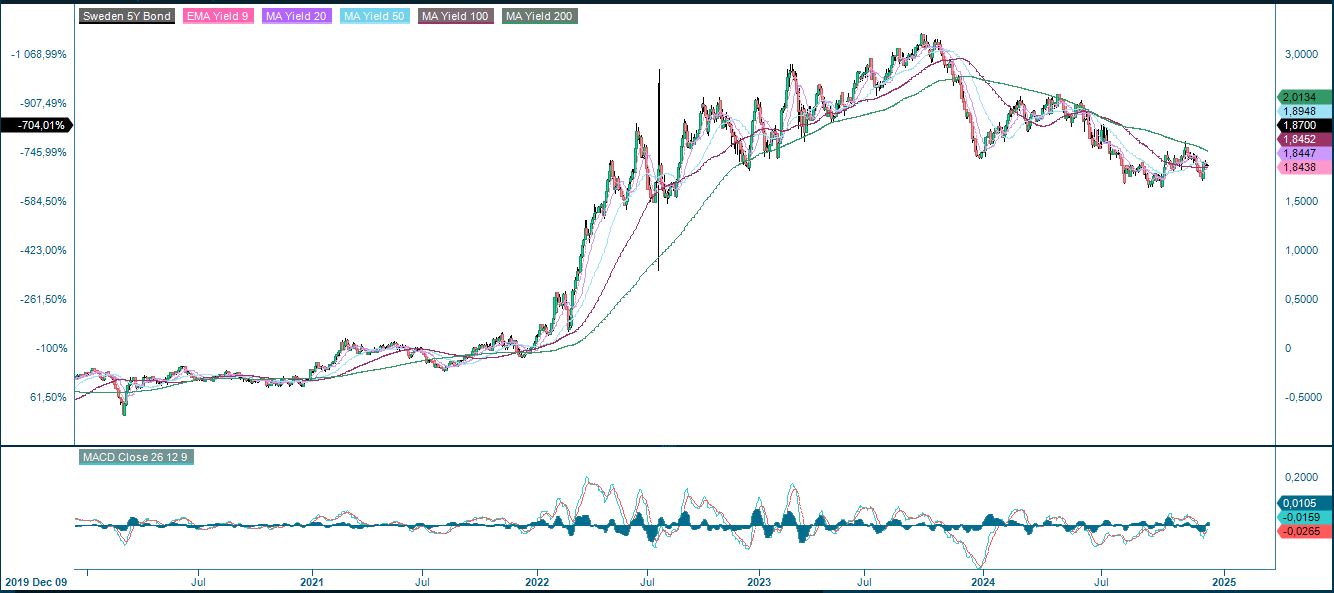

Swedish 5 Year Government Bonds yield (%), weekly five-year chart

Our assessment is that the Nordic banks' profits will not increase very much between 2024 and 2025. At the same time, we believe that there is a lag effect in the banks' mortgage interest margins and profits from mortgage loans, as this market is an oligopoly where the Nordic banks lack sufficient competition. Bank profits from financial transactions are expected to improve after a rising stock market in 2024. In the case of Nordea, net interest income accounted for 63% of total operating income in Q1-Q3 2024.

SEB’s share price has performed the best among the Nordic bank shares so far this year, with a 12% increase. SEB is followed by Swedbank, which is up 8% year to date (YTD), and Handelsbanken, which is up 6%, while Nordea is down by 0.3% this year. Nordea trades at 7.5x price/earnings ratio (P/E) and 1.2x price/book ratio (P/B), the lowest of the Nordic banks.

In the first nine months of 2024, Nordea bought back its own shares for EUR 239 million. During the same period, dividends paid to shareholders totalled EUR 3,218 million. Between October 2024 and February 2025, Nordea plans to buy back a further EUR 250 million of its own shares. Nordea's most recently approved dividend of EUR 0.92/share gives a dividend yield of 8.5% based on the latest Helsinki market price of EUR 10.83/share. The consensus estimate for fiscal year 2024 is a dividend of EUR 1.00/share according to Capital IQ.

We believe that the high yield might be an argument to buy Nordea shares. The main risks are if credit losses increase. Historically, Nordea has reported significant credit losses in the shipping segment, for example.

Nordea (NDA SE) (in SEK), one-year daily chart

Nordea (NDA SE) (in SEK), five-year weekly chart

As a result of the weakening of the SEK against the EUR, the recent high of SEK 134 in May for the Nordea share corresponds to EUR 11.88 on the Helsinki Stock Exchange. Today, SEK 134 is equivalent to around EUR 11.62 per share.

Macro comments

On Friday 6th December the US Non-Farm Payrolls report showed 194 000 new jobs created in November versus expectations for 160 000. It reinforces the perception of a strong US economy.

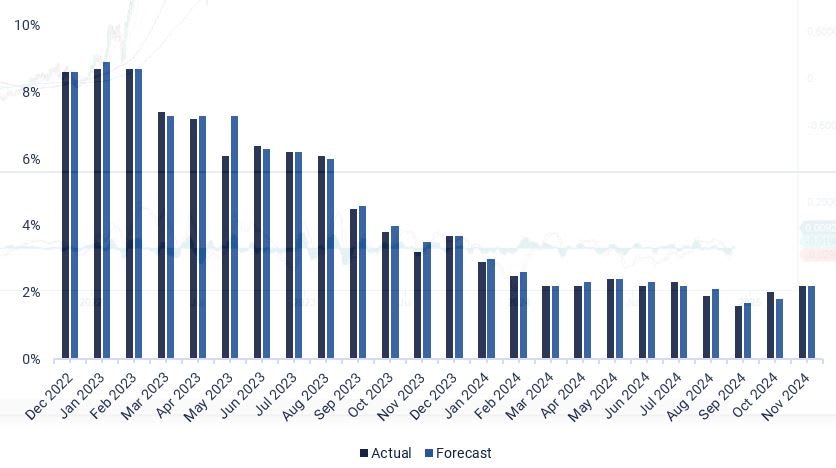

This week, the ECB rate announcement on Thursday 12th will be the most important for the markets, along with the US CPI and PPI figures on Wednesday 11th and Thursday 12th respectively. The chart below shows the development of the German CPI since December 2022, where a rapid decline has turned into a small rebound for November up to 2.2% per year.

Germany Consumer Price Index, Year-over-Year-change since December 2022 (in %)

Wednesday 11 December begins with Japan's November PPI. Later in the day, we get Opec's monthly oil report, US CPI for November and weekly oil inventories (Department of Energy), as well as an interest rate announcement from the Bank of Canada. There will also be interim reports from Adobe and Inditex.

Thursday the 12th will start with Swedish CPI for November and UK Gross Domestic Product (GDP) and Industrial Production for October. This will be followed by the IEA's monthly oil report. The highlight of the day may be the ECB's rate announcement and press conference. From the US, we get the NFIB (National Federation of Independent Business) Small Business Index and the PPI for November, as well as initial jobless claims. Thursday will also see the release of interim reports from Broadcom and Costco.

On Friday the 13th of December we start with Japan's Industrial Production for October. Then we get the German trade balance for October and the French and Spanish CPIs for November. Also on the agenda are Eurozone Industrial Production for October and US Import Prices for November.

Time to take some profits

The S&P 500 has managed to climb higher, but the MACD is close to generating a soft sell signal while the Relative Strength Index (RSI) is close to overbought levels. A break below 6,000 could take the index to the bottom of a narrow rising trend channel. Taking some profits may not be a bad idea.

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), weekly five-year chart

As US interest rates are coming down, being long Nasdaq 100 and short S&P 500 may be an interesting spread.

Related Products

Nasdaq 100 (in USD), one-year daily chart

Nasdaq 100 (in USD), weekly five-year chart

After a strong rally, the DAX is currently overbought on the RSI. Taking some profits might not be a bad idea. The first level of resistance is the EMA9, currently at 20,090. This is followed by levels around 19,660.

DAX (in EUR), one-year daily chart

DAX (in EUR), weekly five-year chart

The OMXS is still lagging as new highs are yet to be seen. Momentum is fading but a spread, long OMXS30, short DAX could be an interesting trade.

OMXS30 (in SEK), one-year daily chart

OMXS30 (in SEK), weekly five-year chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.