US dollar benefits from higher oil price

A strong US economy and, more recently, a higher oil price explain much of the US dollar's strength in 2023. After 2020, the inverse relationship between the US Dollar Index and crude oil prices gradually turned positive. The Fed's interest rate decision later today and September Purchasing Managers Index (PMI) figures from France, Germany, the UK and the US on Friday could move markets this week.

Case of the week: A strong US economy and rising oil prices have supported the USD

At the beginning of the year, Wall Street consensus belief was that the main line of the foreign exchange market in 2023 would be a "bearish US-dollar", but now it is caught off guard by the strong dollar. The USD fell back briefly this year but then unexpectedly rose, from falling below 100 to surging above 105. On September 8, the US-dollar index broke a rare eight-week winning streak, its longest since 2014.

USD-index (DXY), five-year weekly chart

With the dollar's rise, non-US currencies are generally "suffering". Over the past month, the world's major currencies have all fallen against the US dollar, with the euro down more than 5.4% since its July peak. The yen broke through 147 to a 10-month high against the US dollar, and the Chinese yuan and Indian rupee also depreciated to a new cycle low.

Meanwhile, the US domestic economy is under relative pressure. At the same time, Russia's extension of crude oil production cuts increased inflation variables. If U.S. inflation rebounds more than expected, the Federal Reserve could reconsider policy direction, and the U.S. dollar's rally could last longer.

The dollar is stronger than expected because of the resilience of the US economy. After a string of positive economic data in the US in recent weeks, recession bets have plummeted, and the chances of a so-called soft landing for the economy are increasingly likely.

Last week, the US ISM non-manufacturing PMI rebounded sharply to 54.5, and new orders employment is also improving. It has a much smaller impact on GDP than the ISM manufacturing index. However, suppose the indicator is higher than expected. In that case, the US dollar should be considered solid/bullish, while the US dollar should be considered weak/bearish if the indicator turns out lower than expected. Unemployment Insurance Weekly Claims at 220,000 versus expectations of 225,000 suggested that the pace of cooling in the US labour market remains limited and may take longer to reach the Fed's target. The favourable macro data could increase the probability of the Federal Reserve raising interest rates again in Q4 2023, delay the Fed rate cut, and increase the probability of a soft landing of the US economy.

In contrast, it is difficult to be optimistic about the economic situation in Asia and Europe. Eurozone GDP growth was revised from 0.3% to 0.1% in the second quarter of 2023, inflation remained stubborn, and the risk of "stagflation" increased.

Higher oil prices are also supporting a stronger US dollar. A coordinated production cut by Saudi Arabia and Russia earlier this year has contributed to oil prices soaring above $90 per barrel for the first time since November 2022. Soaring oil prices have triggered inflation fears, boosting treasury yields and strengthening the US dollar. Further, the dollar will benefit more when energy costs rise since the United States is a net exporter of oil products.

WTI Oil Price (USD per barrel), five-year weekly chart

After 2020, the inverse relationship between the US dollar index and crude oil prices has gradually become positive. In other words, the higher the oil price, the stronger the US dollar index. The dollar index can continue strengthening if global oil prices still have room to rise. OPEC's latest forecast suggests that the fourth quarter global crude oil supply shortage will be more than 3 million barrels per day, meaning that oil prices will likely continue to rise.

EUR/USD, one-year daily chart

Suppose the recovery of energy inflation promotes the United States CPI, which continues to rise. In that case, it may prompt the Federal Reserve to reconsider its policy rate direction. That could affect the US-dollar rally. Should US inflation begin to fall back, the US dollar interest rate hike cycle has ended, weakening one of the US dollar support factors.

EUR/USD, five-year weekly chart

Macro comments

The ECB raised its deposit rate by 25 basis points to 4.00% on Thursday, 14th September, which aligned with expectations. President Christine Lagarde said that the ECB had probably reached the level of interest rates considered appropriate to dampen inflation. This boosted sentiment on the stock markets.

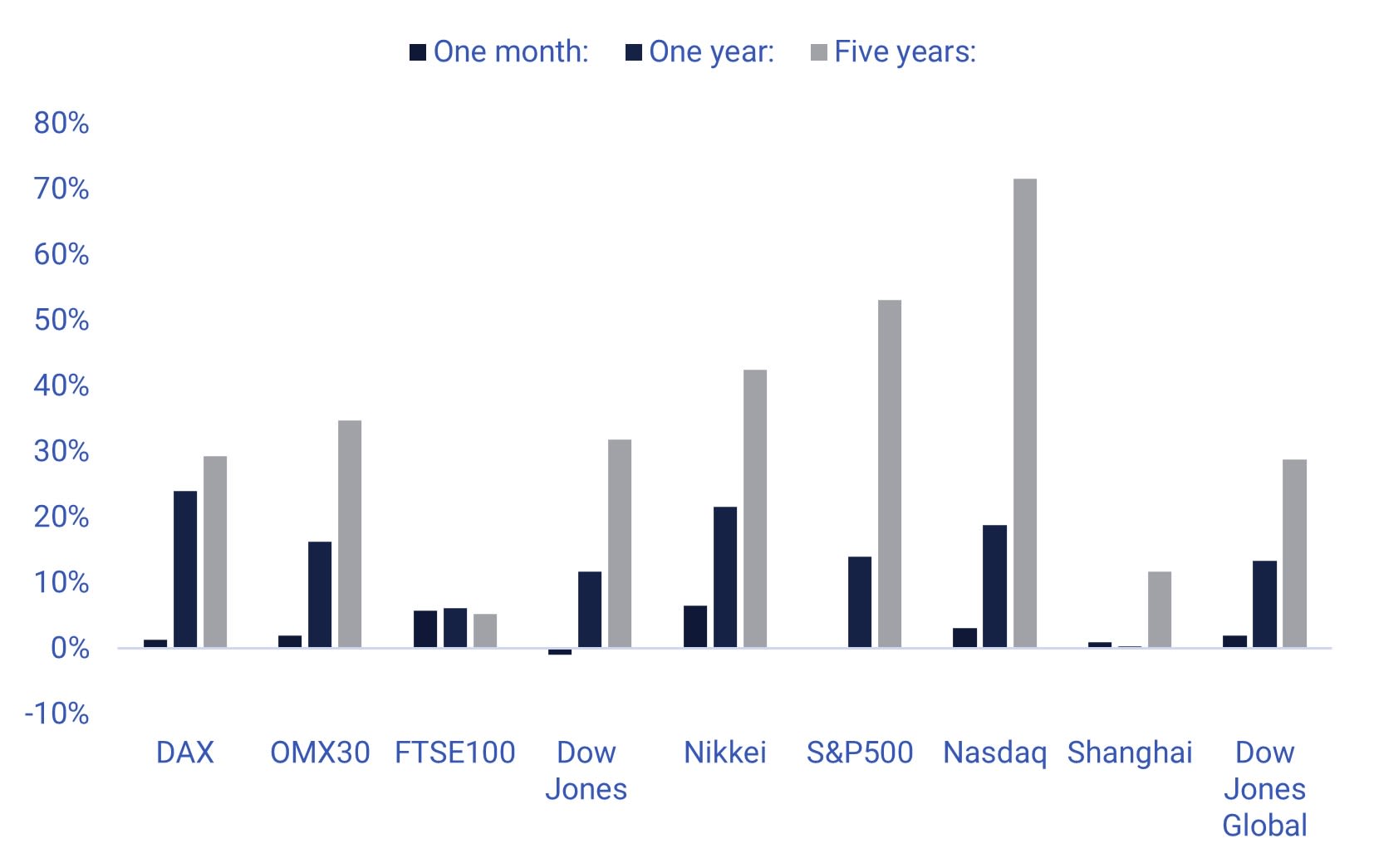

Significant stock indices performance in one month, one year and five years

Related Products

US equity markets fell on Friday, 15th September. The semiconductor sub-index fell 3% on rumours that Taiwan Semiconductor Manufacturing Company is worried about falling demand. The chip maker was rumoured to ask suppliers to delay deliveries due to lower demand. Most large technology stocks, including Microsoft, Amazon and Meta, fell on these rumours.

Today, Wednesday, 20 September, the Fed makes its interest rate announcement, followed by Powell's press conference (20:00 and 20:30 CET).

On Thursday, 21 September, from the United States, we will receive the Philadelphia Fed index for September, weekly unemployment data, the July household confidence indicator, and existing home sales for August. We also get interest rate announcements from the Bank of England and the central banks of Sweden, Norway, and Switzerland.

The most crucial macro news on Friday, 22 September, is the PMI figures for September from Germany, France, the United Kingdom and the United States.

Risk shifted to the downside ahead of the Fed

In the US, the S&P 500 is struggling to find a direction ahead of today's rate decision from the Fed. The chart below shows that the S&P 500 consolidates in a neutral wedge formation. If the wedge is broken on the upside, the formation indicates an upward movement of about 250 index points and vice versa. Note MACD in the weekly chart that has generated a soft sell signal.

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), weekly five-year chart

The Nasdaq 100 is under pressure and trading close to the floor of the rising trend channel. In case of a break to the downside, MA10, currently at 14,769, maybe next.

Nasdaq 100 (in USD), one-year daily chart

Nasdaq 100 (in USD), weekly five-year chart

In the daily chart, OMXS has established a short upward-sloping trend. Momentum remains negative but is improving. In the weekly chart, the index has bounced nicely on MA50.

OMXS30 (in SEK), one-year daily chart

OMXS30 (in SEK), weekly five-year chart

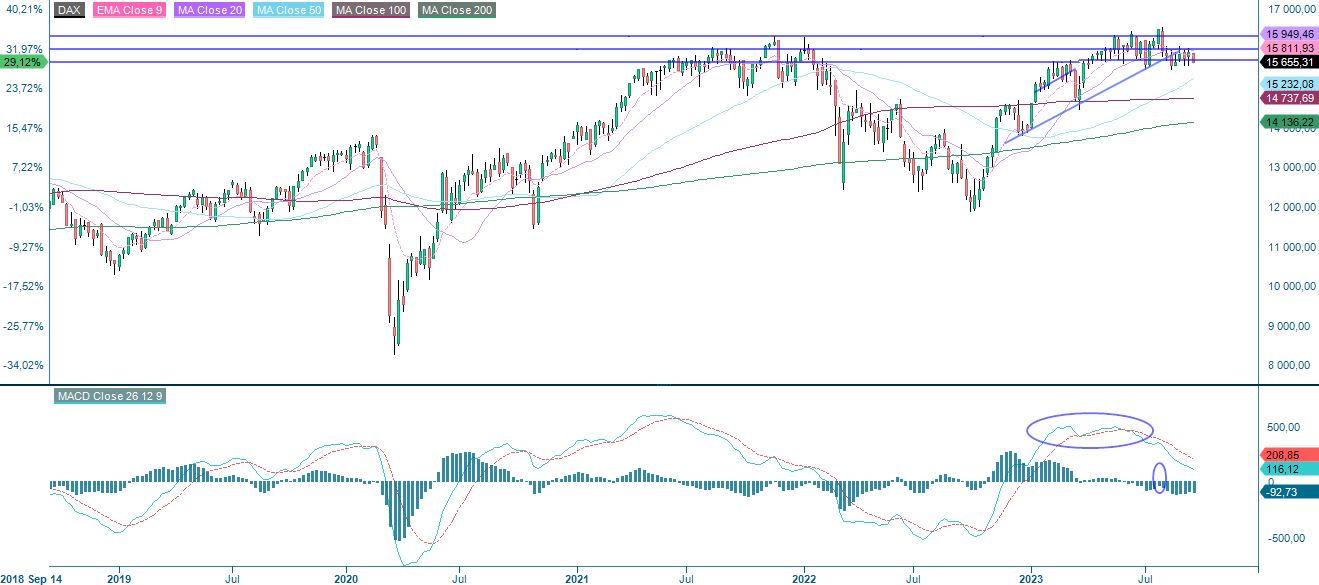

Like the S&P 500, the German DAX has difficulty finding a direction.

DAX (in EUR), one-year daily chart

DAX (in EUR), weekly five-year chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.