European natural gas: between geopolitical turmoil and a growing LNG supply

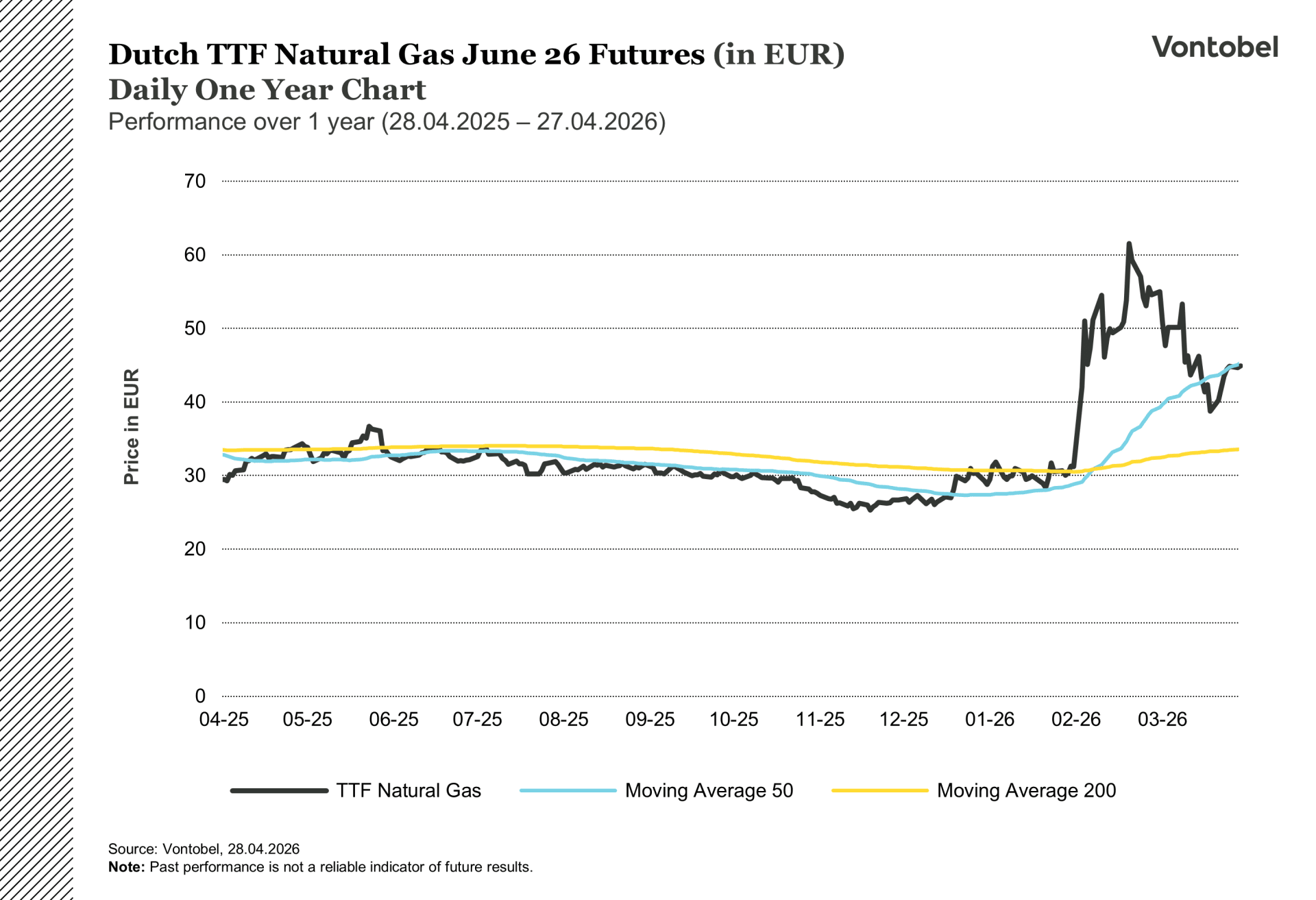

In less than two months, the price of the Dutch TTF gas contract, the most important in Europe, has fluctuated from €27 to €69 and back to €45 per megawatt hour. This price volatility affects everything from electricity prices in southern Sweden and Denmark to the revenues of the Norwegian gas sector. What makes TTF particularly interesting right now is that the market is subject to two opposing forces, neither of which has yet prevailed.

A plant that supplies a fifth of the world

In March, Iranian missiles hit Ras Laffan Industrial City in Qatar, home to the world's largest LNG export facility. Ras Laffan accounts for around 20% of global LNG production. When QatarEnergy was forced to shut down parts of its operations, the TTF price surged by almost 50% in a single trading session. (Al Jazeera, 02.03.2026)

It quickly became clear that the damage was extensive. QatarEnergy's management estimates that approximately 17% of export capacity has been knocked out, with repairs expected to take between three and five years. (GMK Center, 04.2026) The Strait of Hormuz, one of the most critical shipping routes for LNG globally, has also been effectively closed since the conflict broke out. Despite an extended ceasefire, Iran has continued to seize vessels in the strait.

The result is that a significant proportion of the world's LNG infrastructure is either damaged or inaccessible. This is the type of supply shock that typically pushes energy prices higher for an extended period.

Related Products

So why has the price fallen?

Despite a fifth of global LNG flows being disrupted, the TTF price has fallen by almost 40% since March. This is due to several other factors are pulling in the opposite direction.

The most obvious explanation is that Asian buyers have sharply reduced their LNG purchases, making cargoes available for Europe. Warmer weather and increased wind power output have also lowered gas demand. However, the most significant counterforce is the expansion of American LNG.

US LNG exports reached record levels in the spring of 2026, and capacity continues to grow. New facilities such as Plaquemines LNG, Corpus Christi Stage 3 and Golden Pass LNG are coming online, and the EIA expects US export capacity to increase further in 2027. In February, 77% of US LNG exports went to European buyers (Pipeline and Gas Journal, 04.2026). This is because the TTF price currently exceeds the Asian gas benchmark JKM, making Europe the most profitable market for American producers.

But is this enough? Rabobank notes that total global LNG supply is expected to remain at around 443 million tonnes in 2026, largely unchanged from 2025. (FXStreet/Rabobank, 23.03.2026) New capacity in the US does not fully offset the loss in the Middle East. At least not yet.

Europe enters summer with thin margins

The situation is particularly sensitive because Europe has little to fall back on. Gas storage levels are around 17 percentage points below the five-year average, and meeting the EU's requirement for storage to be 90% full by winter will require more gas to be injected over the summer than in any recent year (Canada LNG Group, 20.04.2026).

At the same time, the number of supply sources is shrinking. On 25 April, the EU's ban on Russian spot-traded LNG came into effect, the first stage of a gradual phase-out expected to be completed by early 2027. Russia's share of EU gas imports has already fallen from around 40% in 2021 to 12% in 2025 (Consilium, 2026). However, every further reduction is felt when margins are already thin.

The combination of low storage levels, geopolitical disruptions and fewer supply sources means that Europe is entering the summer refill season with minimal buffers. Any additional disruption, whether involving maintenance in Norway or a new escalation in the Middle East, would severely impact an already strained system.

Why TTF matters in the Nordics

Sweden, Denmark and Finland use relatively little gas, and power generation in the Nordic countries is dominated by hydropower, nuclear and wind. Nevertheless, TTF still affects Nordic energy prices, because gas-fired generation determines the marginal price in Europe's interconnected power system increases. When TTF rises, the cost of gas-fired electricity in Germany, Poland and the Baltics, and through the coupling of European power exchanges, this feeds through to prices in southern Sweden and Denmark. In recent months, TTF's swings between €20 and €70 per MWh have contributed to day-ahead power prices of €120 to €150 per MWh across much of the continent (IEEFA, 20.04.2026).

Norway has a different kind of exposure. In 2025, the country delivered nearly 115 billion cubic metres of gas to Europe in 2025 and accounted for around 30% of total EU gas imports. (Gas Processing News, 01.2026) Norwegian gas is a cornerstone of European energy supply, and every move in the TTF price has a direct impact on the revenues of the Norwegian gas sector.

Where does the price go from here?

Sweden, Denmark and Finland use relatively little gas, and power generation in the Nordic countries is dominated by hydropower, nuclear and wind. Nevertheless, TTF still affects Nordic energy prices, because gas-fired generation determines the marginal price in Europe's interconnected power system increases. When TTF rises, the cost of gas-fired electricity in Germany, Poland and the Baltics, and through the coupling of European power exchanges, this feeds through to prices in southern Sweden and Denmark. In recent months, TTF's swings between €20 and €70 per MWh have contributed to day-ahead power prices of €120 to €150 per MWh across much of the continent (IEEFA, 20.04.2026).

Norway has a different kind of exposure. In 2025, the country delivered nearly 115 billion cubic metres of gas to Europe in 2025 and accounted for around 30% of total EU gas imports. (Gas Processing News, 01.2026) Norwegian gas is a cornerstone of European energy supply, and every move in the TTF price has a direct impact on the revenues of the Norwegian gas sector.

Dutch TTF natural gas futures June 26 (in EUR) daily one-year chart

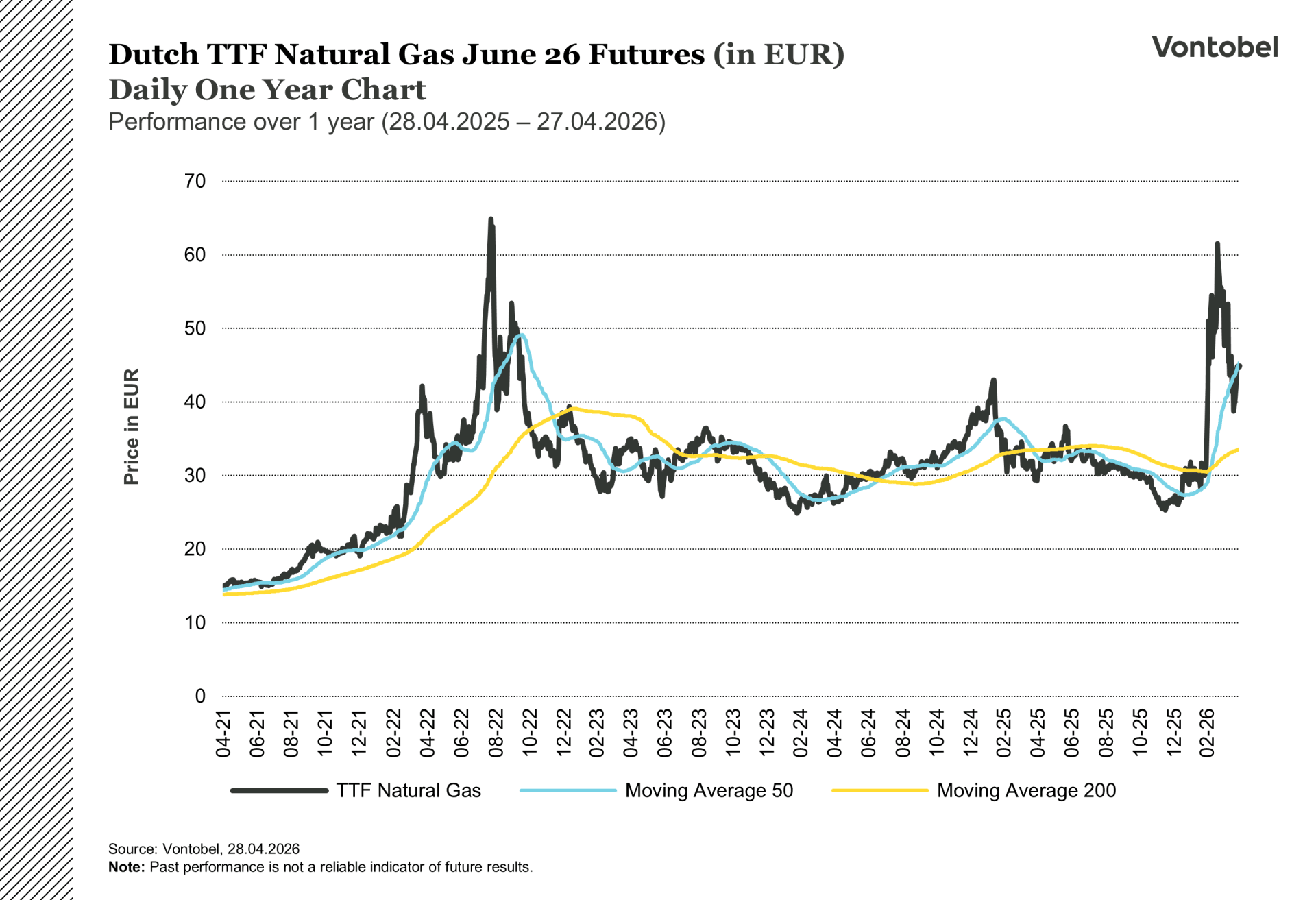

Dutch TTF natural gas futures June 26 (in EUR) daily five-year chart

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.