Investors' Outlook: A cutback in the market

Geopolitical escalation, a K-shaped economy, AI-driven market dislocations and a weaker US dollar. Capital markets are under pressure in 2026. While stock markets and corporate earnings continue to climb in many places, consumers, bonds, currencies and entire industries are increasingly caught in a crossfire of uncertainty, inequality and structural change. This Investors' Outlook reveals what forces are really driving markets right now, where opportunities are emerging, what risks investors should keep on their radar and why looking beyond the headlines matters more than ever.

Uneven ground

It's usually in spring when winter debris is cleared, and what has grown too dense is thinned so stronger shoots can emerge. In the first two months of the year, policy-makers already sowed new seeds and investors pared back crowded trades, while geopolitical tensions have become more tangled.

Tensions between the US and Iran have escalated into open conflict, triggering turmoil in global oil markets and turning the conflict's focus to energy security.

In the US, President Donald Trump nominated Kevin Warsh to succeed Jerome Powell as chair of the US Federal Reserve when Powell's term ends in May 2026. The choice initially triggered a "Warsh Shock" in early February, causing gold prices to tumble and the US dollar to surge. Markets have since stabilized as investor concerns around the Fed's independence eased. Investors have taken some comfort in Warsh's prior service on the Fed's Board of Governors and in the view that he may not fully yield to political pressure.

In Japan, Prime Minister Sanae Takaichi celebrated a landslide snap-election victory. With a 316-seat supermajority, she now has the legislative muscle to override the Upper House and implement her "Sanaenomics" agenda. Along with her January pledge to end "excessively tight fiscal policy and a lack of investment for the future", the win helped boost Japanese equities, which hit all-time highs.

Investors around the world trimmed some tech-heavy positions in favor of more cyclical ones amid reservations about AI-related software stocks. Market participants also sought safe-haven assets in response to the escalation in Iran.

The Multi Asset Boutique reiterates its economic baseline scenario for 2026, which anticipates a positive economic growth trajectory, moderate inflationary pressures, and accommodative monetary and fiscal policy.

When it's not all o-K

Economics is often seen as a discipline rooted in tradition, relying on age-old concepts like Adam Smith's notion of the "invisible hand" or the government-led policies developed by John Maynard Keynes. However, every so often, a new idea shakes up the conversation. Lately, the hottest phrase in economic circles has been the "K-shaped economy."

The "K-shaped economy" describes an uneven economic recovery, in which certain sectors, industries, or groups of people rebound quickly while others lag behind. The term comes from the visual representation of the recovery: one part of the economy or population experiences growth (the upward stroke of the "K"), while another part experiences stagnation or a decline (the downward stroke of the "K"). This creates a divergence in economic outcomes.

When analyzing post-pandemic economic data, economists frequently come across patterns resembling a "K." One such example is the growing disconnect between the US stock market and consumer sentiment.

The upper arm of the "K" reflects a resilient stock market that has weathered high prices, trade war concerns, and geopolitical tensions. Large corporations have managed to shield (and even expand) their profit margins through aggressive pricing strategies. By passing higher costs on to consumers, these firms have maintained robust earnings.

The lower part of the "K" captures a growing divide between financial markets and the day-to-day reality facing many consumers. Consumer confidence, as measured by the University of Michigan Consumer Sentiment Index, remains subdued. An analysis of consumers' write-in responses sheds light on the root of this pessimism. For many Americans, headlines about the AI boom or the record-breaking S&P 500 Index have little relevance to their daily lives. Instead, they are grappling with the rising costs of goods and services, particularly essentials like groceries, health care, and housing.

Housing affordability, in particular, remains the most pressing pain point. The US Housing Affordability Index dropped below the critical 100 threshold in mid-2022 for the first time since the 1980s and has hovered around that level ever since. In simple terms, this means that over the last few years, the average American family has been unable to afford a new home at current mortgage rates and house prices.

One might assume that high-performing companies could step up and raise wages, right? Not so fast. While companies did grant nominal pay increases in response to the post-pandemic inflation surge, real (inflation-adjusted) wage growth didn't turn positive until mid-2023. Even now, though wages are rising faster than the current inflation rate, the cumulative impact of high inflation has left many workers struggling to regain their previous purchasing power. A look at the chart below reveals that companies seem reluctant to increase wages further, even as their 12-month forward profit margins have soared to record highs (enter another "K").

Winners and losers in a K-shaped economy

In a K-shaped economy, the primary beneficiaries are wealthy individuals and large corporations that hold significant capital. The former's net worth climbs because they own assets like stocks and real estate. Those left behind tend to be service-sector workers, small business owners, and individuals without substantial savings. They make up the downward stroke of the "K" and often work in roles that require physical presence, like in hospitality, retail, and traditional manufacturing. The result is a growing divide, where the "haves" see their wealth increasingly detached from the economic struggles of the "have-nots," making social mobility feel more like an impossible leap than a climb up a ladder.

The K may be new, the knots of inequality are not

While the term "K-shaped economy" is a relatively recent addition to the economic lexicon, popularized during the Covid-19 pandemic, inequality and bifurcation are far from new. An analysis of so-called Gini coefficients suggests that social inequality is a predominantly US-specific issue that has lasted for decades.

The US Gini coefficient has trended steadily upward, signaling a widening gap between the country's highest and lowest earners. While many peers (G7 and other developed nations) have kept their coefficients lower through more aggressive redistribution and social safety nets, the US stands out among advanced economies for its consistently higher level of income disparity. Other alternative measures, such as the so-called Palma ratio, which focuses on the extremes of income distribution, convey a similar message.

Stuck on a lower rung

Looking ahead, the situation is unlikely to improve. US President Donald Trump's One Big Beautiful Bill Act (OBBBA), promoted as a "once-in-a-generation" initiative to "jumpstart the economy and guarantee the safety and prosperity of Americans for decades to come," may be far less "beautiful" for many consumers than originally anticipated. According to the Congressional Budget Office and the Joint Committee on Taxation, low-income households are expected to fare significantly worse than middle- and high-income households, largely due to the bill's tax changes and cuts to programs like Medicaid and the Supplemental Nutrition Assistance Program. Similarly, the Tax Policy Center argues that the proposed tax cuts will disproportionately benefit higher-income households, with 60 percent of the tax benefits going to the top 25 percent of earners.

AI may deepen these fault lines. Jobs involving predictable, repetitive tasks, such as data entry, basic administrative support, and certain manufacturing roles, could be most at risk. This trend could result in a polarized labor market, where high-skill roles expand while mid-to-low-tier "stepping-stone" jobs vanish. Many entry-level positions that once served as career starters for young or low-skilled workers are also increasingly at risk of automation, potentially making it more difficult to get a foot in the door.

How to kick the "K" to the curb

Republicans and Democrats alike say they're on the side of those on the downward stroke of the "K", though they take fundamentally different approaches. Over the past decades, Republicans have leaned toward supply-side relief, while Democrats have focused on demand-side support. Republican measures include tax cuts (e.g., the 2017 Tax Cuts and Jobs Act or OBBBA), deregulation (e.g., the rollback of the Dodd-Frank Act), and protectionist policies such as tariffs. Democrats have sought to strengthen the consumer base (e.g., through the Affordable Care Act) and regulating Big Tech and Big Retail (e.g., enforcing stronger antitrust measures to prevent giants like Amazon or Walmart from using predatory pricing to drive "Main Street" competitors out of business). Interestingly, neither party's approach seems to have worked: measures like the Gini coefficient have been on a (fairly) consistent upward climb regardless of which party held the White House.

The Trump administration has recently taken a more creative approach, introducing a range of unconventional ideas to tackle the affordability crisis. One proposal calls for a temporary 10 percent cap on credit card interest rates. In a post on Truth Social, Trump suggested this move would ensure that Americans are no longer "ripped off by Credit Card Companies that are charging Interest Rates of 20 to 30 percent, and even more, which festered unimpeded during the Sleepy Joe Biden Administration." Another idea is the introduction of a 50-year mortgage loan. For context, the 30-year fixed-rate mortgage is currently the most popular and common home loan in the US. Though details are sparse, National Economic Council Director Kevin Hassett has suggested that extending the loan term could "reduce the monthly payment quite a bit for a typical home for middle America by a few hundred dollars a month".

There is another unconventional measure, this time from both ends of the political spectrum: taxing the rich. After his landslide victory, New York City's left-wing Mayor Zohran Mamdani said that the time has come to tax the richest New Yorkers and most profitable corporations. His campaign centered on raising taxes by 2 percent on millionaires and raising the combined corporate tax rate to just over 22 percent.

Meanwhile, right-wing figure Steve Bannon, who previously advocated for tax hikes during his tenure as White House chief strategist in 2017, has again signaled support for increasing taxes. As he put it, the numbers behind the massive tax cuts for working- and middle-class households only add up if taxes on the wealthy are increased.

Even Trump has expressed personal sympathy for the concept. In an interview with TIME magazine, he said he wouldn't mind paying more taxes himself and that he wouldn't really be raising taxes in the true sense, he'd be raising them on the wealthy to take care of the middle class, adding: "I actually love the concept, but I don't want it to be used against me politically, because I've seen people lose elections for less."

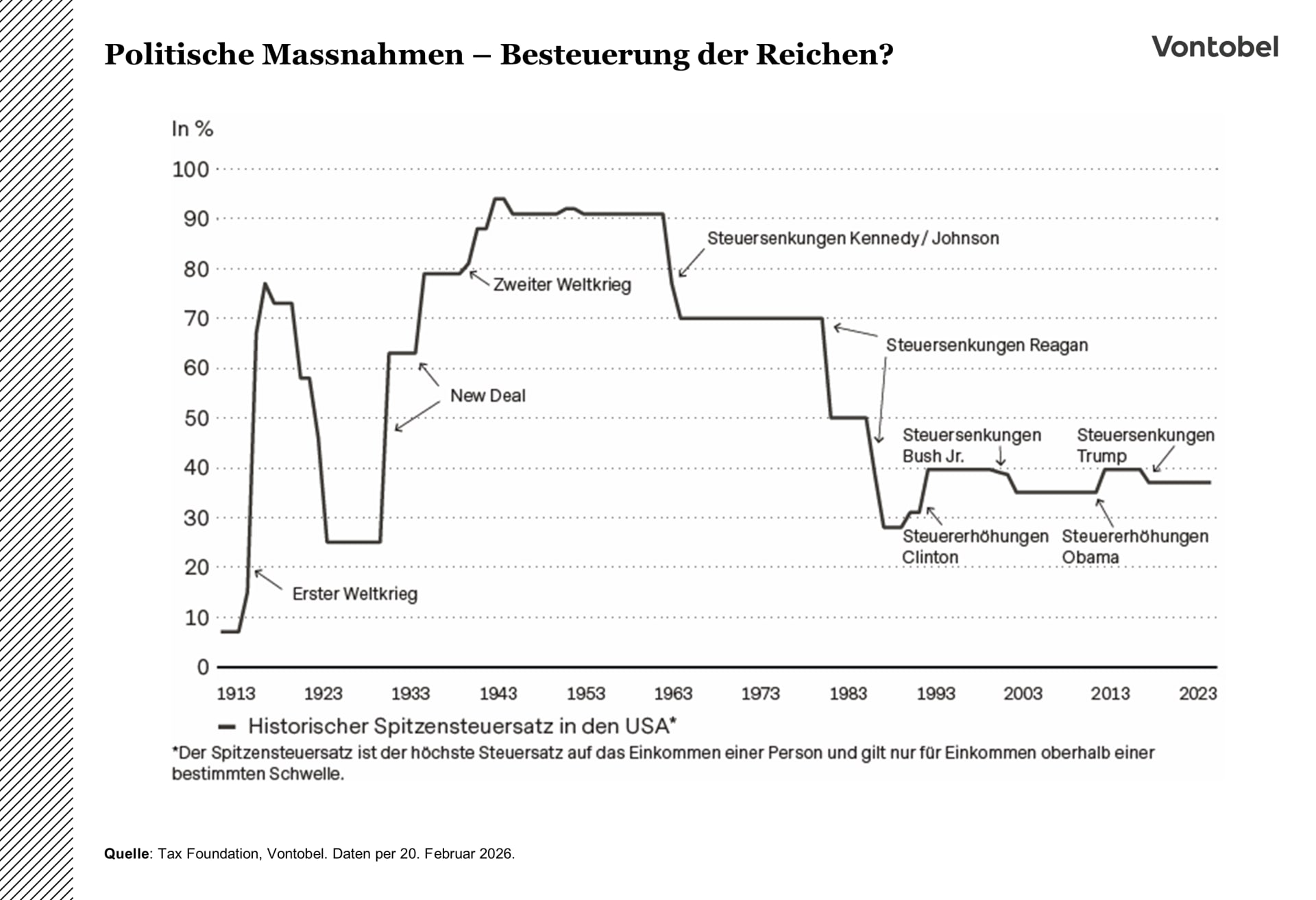

There's little question that tax hikes are hugely unpopular. However, if history is any guide, there is room for higher taxes. For example, the highest marginal income tax rate in the US was significantly higher in the past, particularly in the pre- and post-World War II era, when elevated tax rates were used to bring down high levels of national debt.

If taxing the wealthy is not politically feasible, Trump could instead look to corporations. While not currently on the political agenda, higher corporate taxes targeting monopolies (think of Big Tech heavyweights) could be an effective alternative approach.

K-shaped economy: Four scenarios

There are four potential (not mutually exclusive) scenarios for how the situation could develop. The base case scenario, "Status quo continues" (75 percent probability), assumes no major changes to the K-shaped economy. In this scenario, Trump's policies (e.g., tariffs and the OBBBA) and advancements in AI would likely exacerbate existing inequalities. In such an environment, investors may favor equities and momentum strategies.

The second scenario, "Help for K-economy losers" (50 percent probability), envisions a future where lower US interest rates eventually translate into reduced mortgage rates. Additionally, some unconventional measures might be introduced to tackle affordability issues, particularly in the housing sector. Under this scenario, investors may show a preference for small caps and cyclical stocks.

The third scenario, "Cap for K-economy winners" (25 percent probability), involves measures to limit the gains of the wealthiest individuals and corporations, potentially through higher taxes or stricter regulations. In such a setting, investors may opt to hold cash positions and avoid US large-cap stocks.

The final and most severe scenario, labeled "US civil war" (10 percent probability), envisions no significant changes to the K-shaped economy. Instead, it assumes that Trump's policies (e.g., OBBBA and tariffs) may exacerbate existing issues, potentially resulting in escalating social and political tensions, which could lead to widespread unrest and division within the country. In this scenario, investors would likely go long on gold and short on the US dollar.

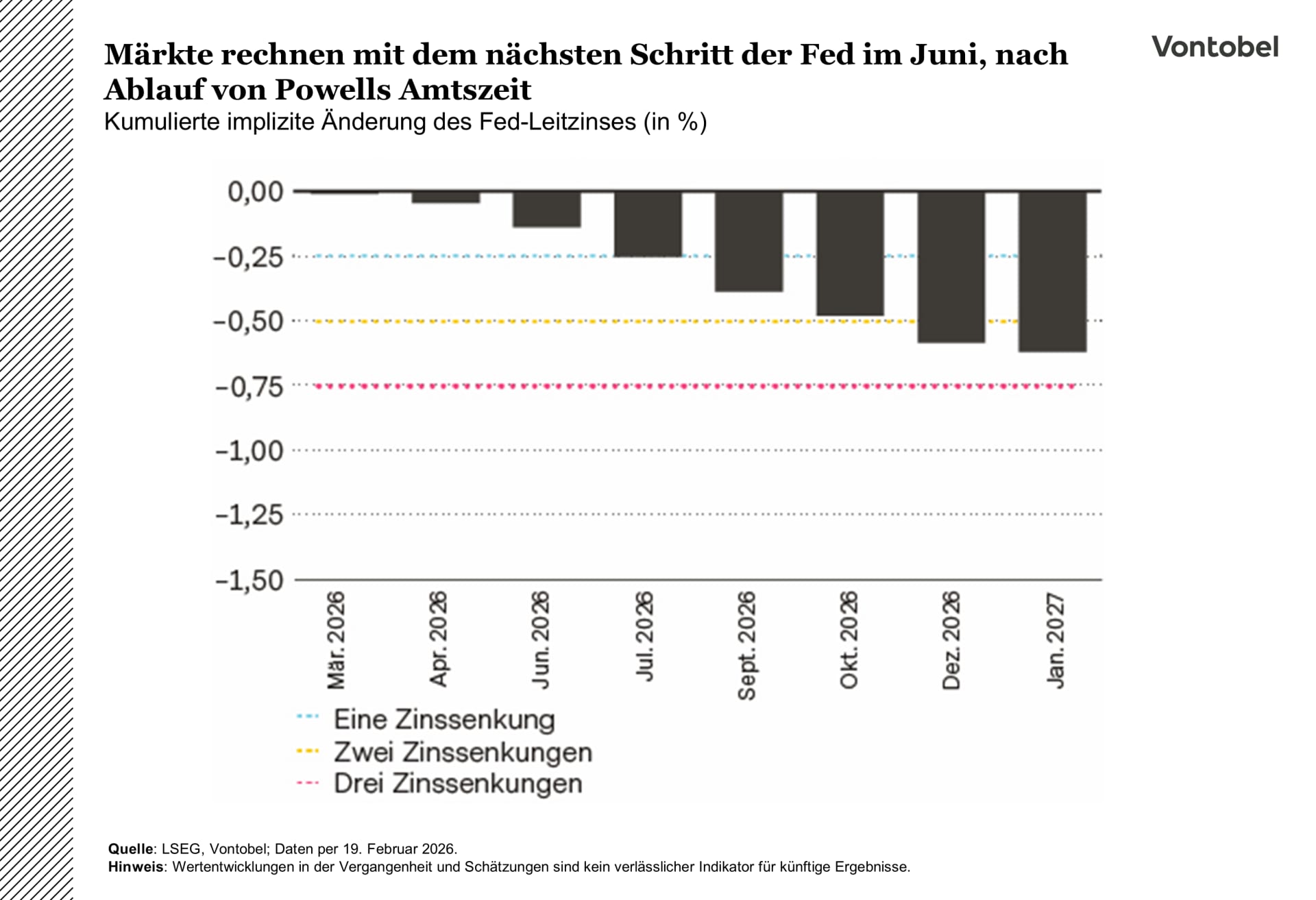

Waiting for the cut

The Fed left the funds rate unchanged at 3.50 percent to 3.75 percent on January 28, with Stephen Miran and Christopher Waller dissenting in favor of a quarter-point cut. Officials also removed language that had pointed to rising downside risks to employment, and Chair Jerome Powell cited a "clear improvement" in the outlook alongside a steadier labor market. That raises the bar for near-term easing. Futures still lean toward no move before June, by which time Powell's term as chair will have ended and a successor is likely in place.

Warsh's nomination could be the bigger driver of the curve. If Warsh takes over, 2-year yields would likely drift lower, as the front end mostly follows the expected policy path and markets price in a clearer easing bias around the leadership change. The 10-year yield may behave differently. Warsh has signaled a preference for a materially smaller Fed balance sheet. A faster-than-expected reduction from the current roughly USD 6.7 trillion level could lift term premia and keep long yields stickier, even amid rate cuts, because investors demand more compensation for liquidity and funding uncertainty.

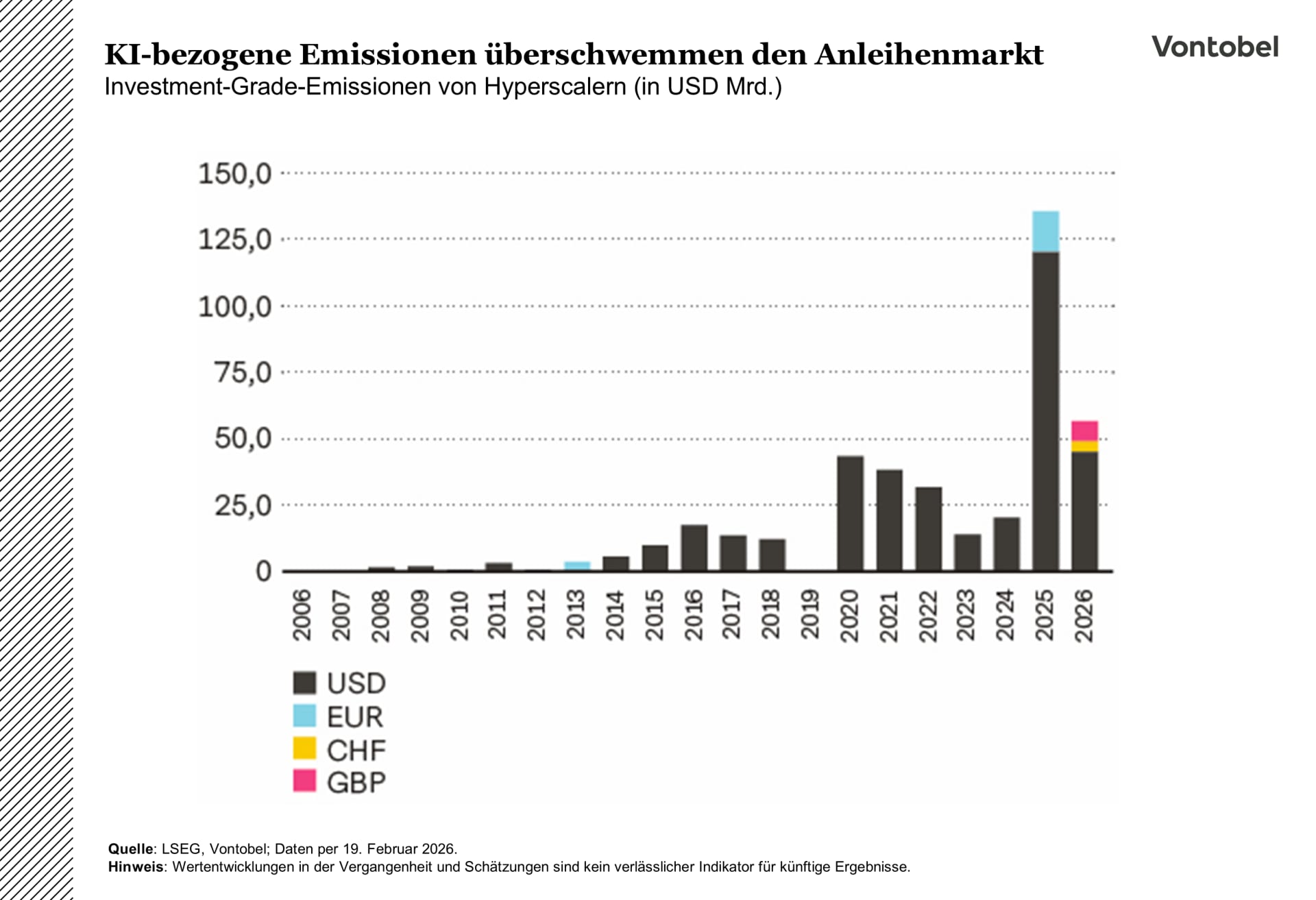

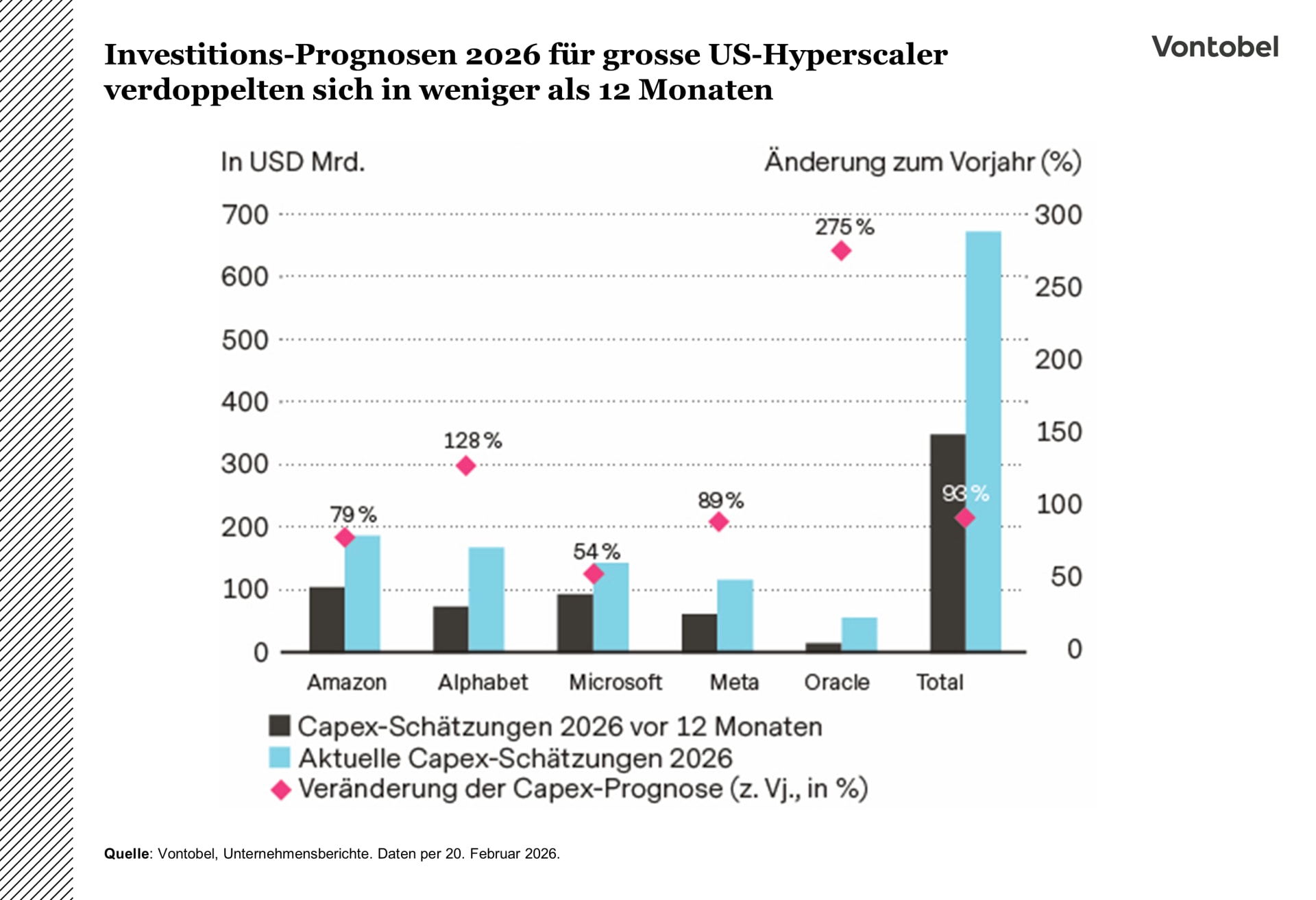

AI capex turns into a supply story for credit

Hyperscalers are already printing in size again this year. Demand is strong, but a heavier pipeline raises the odds that spreads will need to cheapen if sentiment or liquidity turns. AI capital expenditure (capex) is becoming the key supply question for credit: how much funding ends up in public markets, and how quickly. For US hyperscalers, 2025 already showed a surge: roughly USD 100 billion in plain-vanilla IG issuance, and more than USD 130 billion once you include joint venture and special purpose vehicle structures. 2026 is starting in the same gear, led by Oracle's USD 25 billion print and Alphabet's USD 31.5 billion-equivalent multi-currency deal, including a rare GBP 1 billion 100-year tranche.

AI-related debt issuance is poised to be heavy this year, mostly from hyperscalers. Even if demand stays healthy, more supply could nudge spreads wider, and the market may ask for higher concessions. Any widening should be modest in a stable macroeconomic context but could accelerate if risk sentiment or liquidity deteriorates.

An AI cold snap sweeps through markets

Investor sentiment toward AI soured in February, as earlier enthusiasm gave way to market anxiety over how disruptive the technology could become, escalating into an "AI scare trade."

Advancements from firms like Anthropic, particularly tools capable of carrying out independent legal, analytical, and operational tasks, triggered the sell-off. This was most pronounced in global software, where fears of obsolescence have driven the steepest non-recessionary correction the sector has seen in more than three decades. Investors worry that AI agents could automate customer relationship and workflow management as well as data analytics, eroding subscription revenues, pricing power, and earnings.

The pullback quickly extended beyond software. In financial services, wealth management firms, brokerages, insurance providers, private equity, and other data-heavy players came under pressure as markets contemplated AI's potential to threaten advisory roles, compliance checks, and risk modeling. Real estate services, including brokers and commercial platforms, also tumbled amid expectations that transactions could become automated. Even adjacent areas like logistics and trucking stocks declined on fears of AI-optimized routing and autonomous freight scaling.

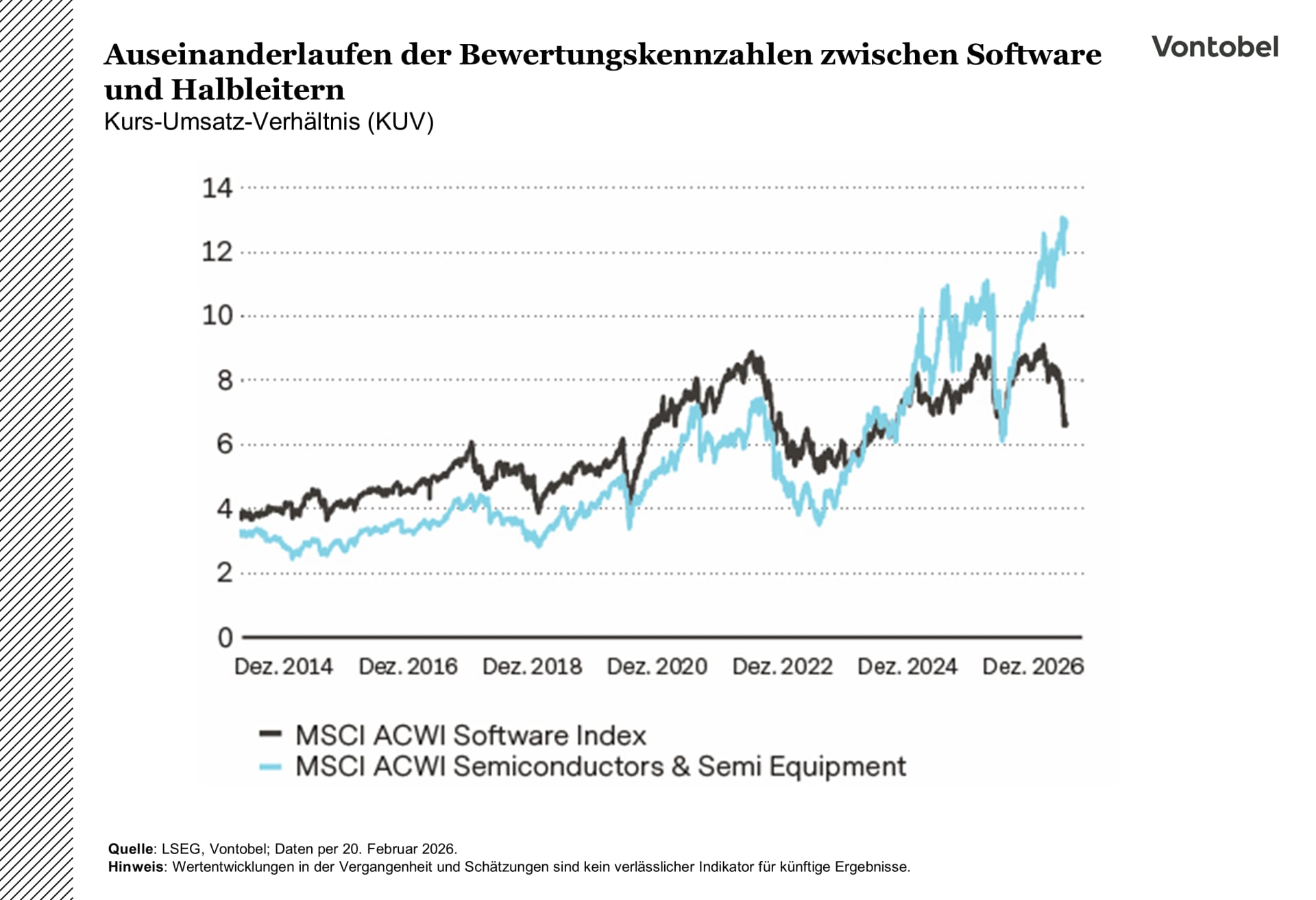

Within technology, the valuation and performance gap between software and semiconductor / AI infrastructure companies has widened. Semiconductor firms continue to benefit across the board from hyperscalers' capex boom. Their performance, market capitalizations, margins, and valuations have reached unprecedented levels, which is drawing closer scrutiny from investors.

While the sell-off may have appeared somewhat indiscriminate and sentiment-driven, the concerns around AI disruption aren't unfounded. It has the potential to cannibalize multiple industries, and given the speed of adoption, the impact could materialize quickly. Sectors built around knowledge work and structured processes face competition, especially where switching costs are low or competitive advantages are limited. However, the magnitude of the correction seems excessive to us, especially in parts of software, where valuations have compressed dramatically. Many of these companies have deeply entrenched processes or value chains that aren't easily fully replaced by AI.

The recent broadening market leadership seems justified and may expand further as the AI theme matures. The ongoing rotation toward defensive, cyclical, and value-oriented real-economy sectors could continue over the medium term. Volatility might also accompany sectors affected by speculation until new catalysts such as clearer evidence of monetization or earnings beats emerge.

From risk premium to reality

The geopolitical risk premium has transitioned from being a mere possibility to a present reality. In late 2025, the Multi Asset Boutique outlined three potential scenarios for the evolving situation in the Middle East.

We have now entered a phase of regional escalation. Iran has closed the Strait of Hormuz; in addition, energy infrastructure in the region has been damaged. Key OPEC members have already responded. The so-called Voluntary Eight (V8) announced a larger-than-expected increase of 206,000 barrels per day (bpd) in production quotas, compared with analysts' pre-meeting forecast of 137,000 bpd.

While the higher production quota may offer some relief, it will not take effect until April and is unlikely to offset the loss of oil supply if the Strait of Hormuz is closed for a prolonged period. Such a closure would place us in scenario 3 ("Protracted conflict"). A blockade or disruption of the Strait is the most critical tail risk to the global economy. Each day, roughly 20 million barrels (about one-fifth of global consumption) pass through this vital waterway.

Although the Iranian regime and its allies currently find themselves backed into a corner, they have the capacity to retaliate, potentially with drones. Iran-aligned groups, such as the Houthi rebels, have already shown they can inflict significant damage using low-cost drones. Another potential threat comes from sea mines, which could disrupt vital oil trade routes. Tankers are reluctant to enter the Strait of Hormuz due to fears of attacks and insurance considerations. This is already causing disruptions.

Regional and global players have certain levers at their disposal to help mitigate the impact. One option is rerouting crude oil via pipelines to alternative ports. The Saudi East-West Pipeline allows Saudi Arabia to pump oil from its eastern fields across the desert to the Red Sea port of Yanbu. The United Arab Emirates operates a pipeline which carries oil from inland fields to a port outside the Strait, and Iran has developed its own Goreh-Jask Pipeline. When combined, these could provide a total bypass capacity of some 7 to 8 million bpd. While significant, it still falls short of covering the roughly 20 million bpd that typically transit through the Strait.

Liquefied natural gas (LNG) is far more challenging, as it can't easily be rerouted by pipeline. Qatar, one of the world's largest LNG exporters, relies almost entirely on the Strait to transport its tankers. This highlights the Strait's importance as a global energy chokepoint, despite the development of alternative routes. In addition to OPEC output increases and pipeline flows, the US could also consider tapping into its Strategic Petroleum Reserve (SPR). But after repeated oil withdrawals during the Biden administration, the SPR currently holds just 415 million barrels.

Withering US dollar support and an overgrown Swiss franc

The US dollar has started 2026 much as it did in 2025, soft and without follow-through. With US rate support no longer improving and positioning lighter, the current setup appears closer to weak-dollar periods than a bull cycle.

The chart below puts the dollar's year-to-date path into context, and the message is clear: After last year's slide, there was no convincing rebound, the US dollar is still in negative territory. For contrast, look at the extremes. The yellow line (1981) is a textbook strong-dollar year. Volcker-era rates were pushed to very high levels to crush inflation, US real yields were miles above peers, and capital chased dollar assets. The red line (1985) shows the opposite. The US dollar had become overvalued, the trade deficit was blowing out, and the Plaza Accord delivered a coordinated push to weaken the currency.

Considering this history, 2026 so far, and 2025 especially, are much closer to the weak end of the distribution than to a true bull-dollar regime. The macroeconomic backdrop explains why. Rate differentials are no longer widening in the dollar's favor, and positioning is no longer structurally long US dollar, so an important pillar of support has faded.

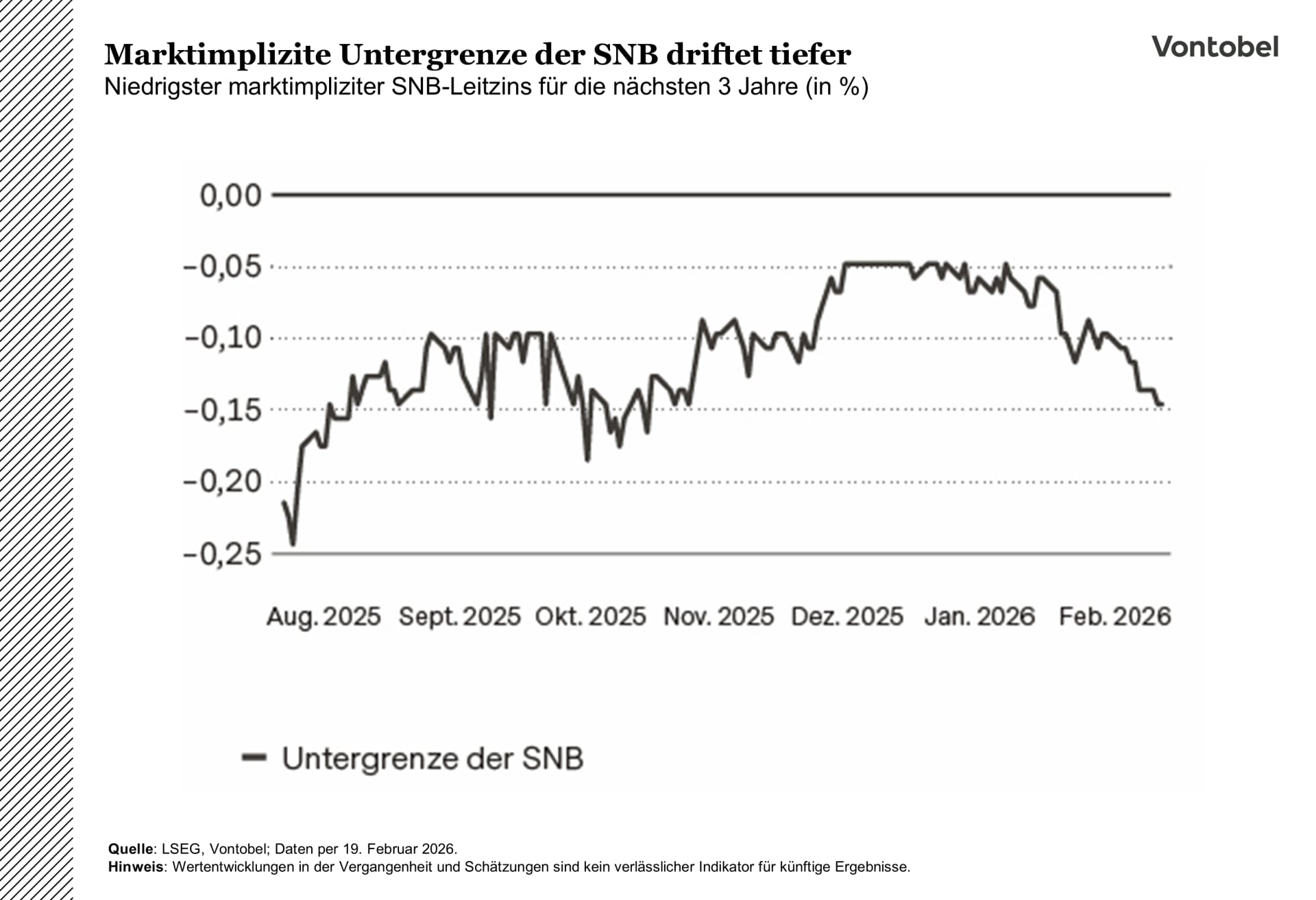

Elsewhere, the Swiss franc's strength is turning into a growth headwind and a policy constraint. With interest rates already at 0 percent and inflation near the bottom of its 0–2 percent range, the Swiss National Bank (SNB) is likely to hold steady and lean on foreign-exchange (FX) intervention, even as markets still price in a small chance of negative rates if the franc appreciates further. After gaining about 14 percent in 2025, the franc is up nearly another 3 percent this year, taking USD/CHF back toward levels last seen during the 2015 shock. That matters in an economy where exports exceed 70 percent of GDP. Big companies like Roche, Swatch, and Richemont are already flagging currency drag, with small and medium-sized enterprises feeling the impact even more.

The exchange rate also complicates policy. With rates at zero, resisting further franc strength would quickly put negative rates back on the table, an option policy makers have little appetite to revisit. Markets still assign some probability to that outcome, which shows how central the currency has become to the outlook. For now, the SNB looks set to hold, keep FX interventions as a backstop, and focus on rebuilding policy room. Any rate hike would likely come into view only later if inflation stays steady.