Not all that glitters is gold - what could be next for precious metals?

Precious metals were among the "driving forces" of the investment universe in 2025. As in the previous year 2024, the price of gold recorded a double-digit percentage increase, with the yellow precious metal rising by around 65% in 2025. Silver and platinum fared even better. Both precious metals have more than doubled in value since the beginning of the year. The bar is therefore set high for 2026. Can the precious metals continue their run in the new year or is the air slowly running out?

A year for the history books

In a year characterized by customs conflicts, geopolitical risks and falling interest rates, gold, silver and platinum increasingly moved into the spotlight and set new price records, while the broad commodities market, as measured by the S&P GSCI® (Goldman Sachs Commodity Index), was in a sideways trend in 2025. Against this backdrop, the question for 2026 is to what extent these supportive factors are already reflected in prices and whether the environment continues to offer scope for price gains. As prices rise, the susceptibility to corrections could increase if real interest rates or economic expectations develop unfavorably (World Gold Council, 08.12.2025). The outlook for precious metals in 2026 therefore requires a differentiated view of the individual metals and their drivers.

Silver has its finest hour

Silver outperformed gold in terms of performance in 2025. After jumping above $50 USD in the fall, the price set new records of over $60 USD per troy ounce in December (TradingView, 21.12.2025). The rally in silver is characterized by the precious metal's dual role: like gold, it acts as a monetary hedge, but is also increasingly being used in industry.

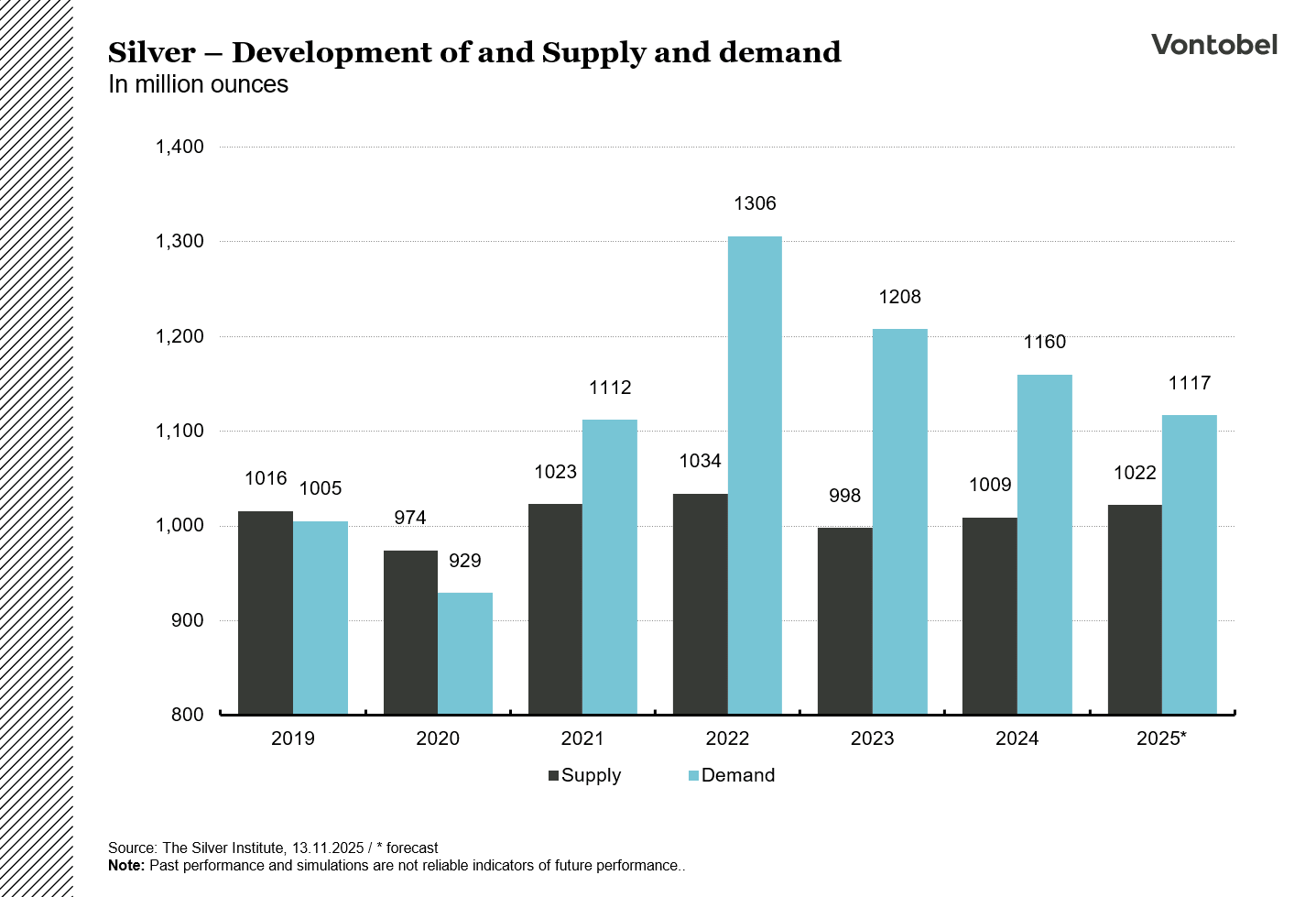

The silver market has been under pressure for some time. The Silver Institute expects a further structural deficit in 2025, the fifth year in a row, and points to robust industrial demand as a key driver. The Institute quantifies industrial demand alone at around 665 million ounces in 2025 with a total supply of 813 million ounces (Silver Institute, 13.11.2025).

The shortage in 2025 was not only reflected in the price, but also in the market structure. London silver stocks fell to their lowest level since the mid-2010s, according to LBMA (London Bullion Market Association) data, which encouraged short-term distortions in premiums and financing costs (Reuters, 07.03.2025). Another, albeit rather symbolic, factor was that the Saudi central bank invested in silver ETFs, according to disclosure documents. Although the volume was small at USD 40 million, it signaled that central banks may also be focusing on silver (NZZ, 30.08.2025).

The outlook for 2026 remains divided. If the expansion of solar, electricity and storage infrastructure continues, this should further support industrial demand for silver. The Silver Institute assumes that the market deficit will continue in 2026 (Silver Institute, 13.11.2025).

A noticeable slowdown in global growth or a reluctance to invest in the industry could in turn be reflected in demand. In addition, high price levels could accelerate substitution effects and efficiency increases. Profit-taking following the recent price rally could also put pressure on prices. Accordingly, the outlook for 2026 remains characterized by increased uncertainty, in which changes in direction are just as possible as a continuation of the current market structure.

Related Products

Platinum group metals also have an eventful year

Platinum and palladium were not quite able to stand out from the shadow of gold and silver in the media coverage in 2025, but delivered a convincing performance. After a prolonged sideways phase, both metals saw some movement in the market from May 2025. In China, platinum became more attractive as a cheaper jewelry alternative to gold, with demand picking up noticeably in the first half of the year (WPIC, 19.11.2025). At the same time, forward market signals for platinum indicated a physical shortage at times when the curve turned into "backwardation", in which forward contract prices are below the current spot price (WPIC, 19.11.2025). On the supply side, the market remains vulnerable, as a large proportion of primary platinum production comes from South Africa and production and refining risks regularly affect supply volumes (WPIC, 19.11.2025).

In contrast to platinum, palladium is much more closely linked to the automotive industry: It is mainly used in catalytic converters in gasoline engines and is therefore more sensitive to shifts in the drive mix. In 2025, the price of palladium rose in phases in parallel with the broad precious metal rally. As with other precious metals, the main drivers were macroeconomic factors such as high government deficits, above-target core inflation and simultaneously falling key interest rates, which supported demand for scarce tangible assets. Part of the rally could also be attributed to a catch-up movement. After platinum and palladium lagged significantly behind gold and silver in previous years, investors increasingly focused on the valuation difference in 2025 (CME, 04.11.2025).

An additional uncertainty factor for palladium arose at trade policy level in 2025. The South African producer Sibanye-Stillwater, together with the United Steelworkers union, filed anti-dumping and countervailing duty applications against Russian palladium imports with the US authorities. The background to this is the USA's heavy dependence on Russian material: in 2024, around 40% of US palladium imports came from Russia (WPIC, 2025). In the short term, rising inventories and trade diversions could cushion part of the supply gap. In the medium to long term, however, sustainable substitution of Russian supplies is considered challenging.

The automotive sector also remains important for platinum, where the metal, like palladium, is used in catalytic converters. While purely electric vehicles do not generate any direct demand for platinum, hybrid and plug-in hybrid drives tend to require higher platinum loadings in catalytic converters, as the combustion engine starts cold more often and has to meet stricter emission standards (Reuters, 09.09.2024). However, an unexpected slowdown in global vehicle production could affect both metals. This means that price dynamics will remain two-pronged in 2025: platinum is more dependent on the interplay between scarce supply, jewelry substitution and the economy, while palladium is increasingly dependent on demand for cars and political trade risks.

Gold continues to advance

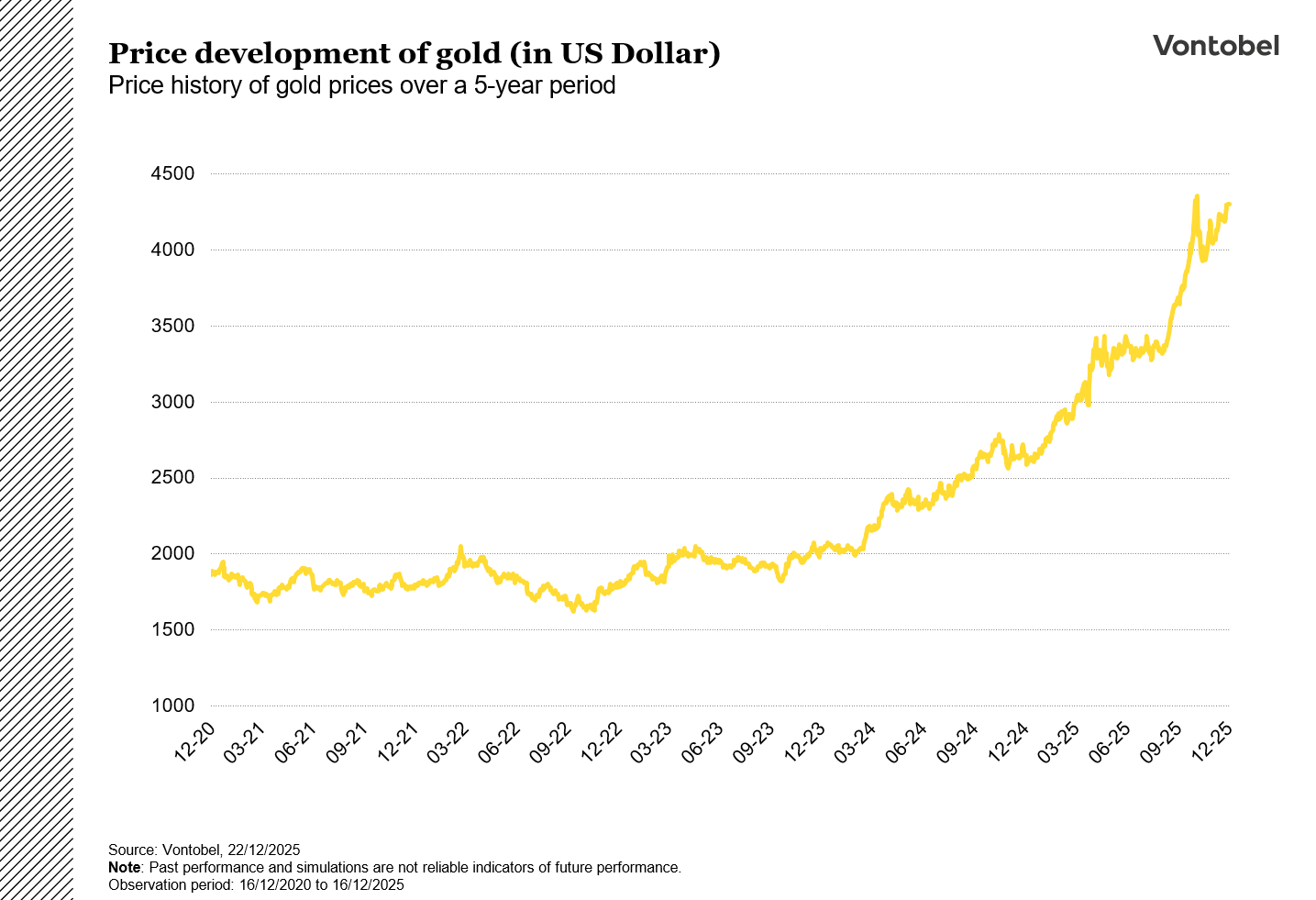

The development of the gold price in 2025 was driven by a combination of several developments. Falling real interest rates and the expectation of further interest rate cuts lowered the opportunity cost of the interest-free metal, while a weaker US dollar supported demand outside the US. The resilience of the demand side also became apparent in the second half of the year: After a correction, gold temporarily slipped below USD 4000 per troy ounce, but found support there and was last quoted around USD 4400 (TradingView, 22.12.2025).

The figures on physical demand underline the breadth of the movement. The World Gold Council reports global gold demand of 1,313 tons for the third quarter of 2025, the highest quarterly figure since the survey began, driven primarily by investments in bars, coins and ETFs (World Gold Council, 30.10.2025). According to the World Gold Council, ETF inflows alone amounted to 222 tons in the third quarter of 2025, while central banks bought 220 tons. Switzerland also stood out: demand for coins and bars rose to 18.1 tons in the first three quarters of 2025, up from 11.5 tons in the previous year (FuW, 31.10.2025).

Forecasts for 2026 range from moderate consolidation to a continuation of the bull market. According to Reuters, Deutsche Bank sees an average gold price of USD 4450 per ounce with a range of USD 3950 to 4950 per ounce (Reuters, 26.11.2025). In its base scenario, J.P. Morgan expects an increase towards USD 5000 per ounce by the end of 2026 and cites an average of around USD 5055 per ounce for the fourth quarter of 2026 (JPMorgan, 16.12.2025). The World Gold Council argues more cautiously: in an environment in which expectations are largely priced in, it only considers a range of around minus 5% to plus 5% to be plausible in the baseline scenario in 2026 (EuroNews, 09.12.2025). Decisive risk factors could be a change in interest rate and dollar expectations or a cooling of demand from central banks and institutional investors.

Related Products

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.