Volatility and divergence across commodity markets

November was a month marked by a combination of geopolitical tensions and weather-related concerns that drove volatility across commodity markets. Precious metals, led by silver, surged as dovish signals from the Federal Reserve and a tightening physical market fueled investor optimism. Conversely, oil and refined products faced significant pressure, as hopes for a ceasefire between Russia and Ukraine grew, which eased some of the geopolitical risk premiums. However, natural gas bucked the trend with an 11% rally, driven by fears of a colder-than-usual winter. The agricultural sector was more subdued, with soybeans benefiting from Chinese demand but facing headwinds from competition with South American crops. Looking ahead, the key question is which factor will dominate geopolitical risks or the looming winter season. How will these factors shape the outlook for energy and agricultural commodities?

Volatility grips the energy markets

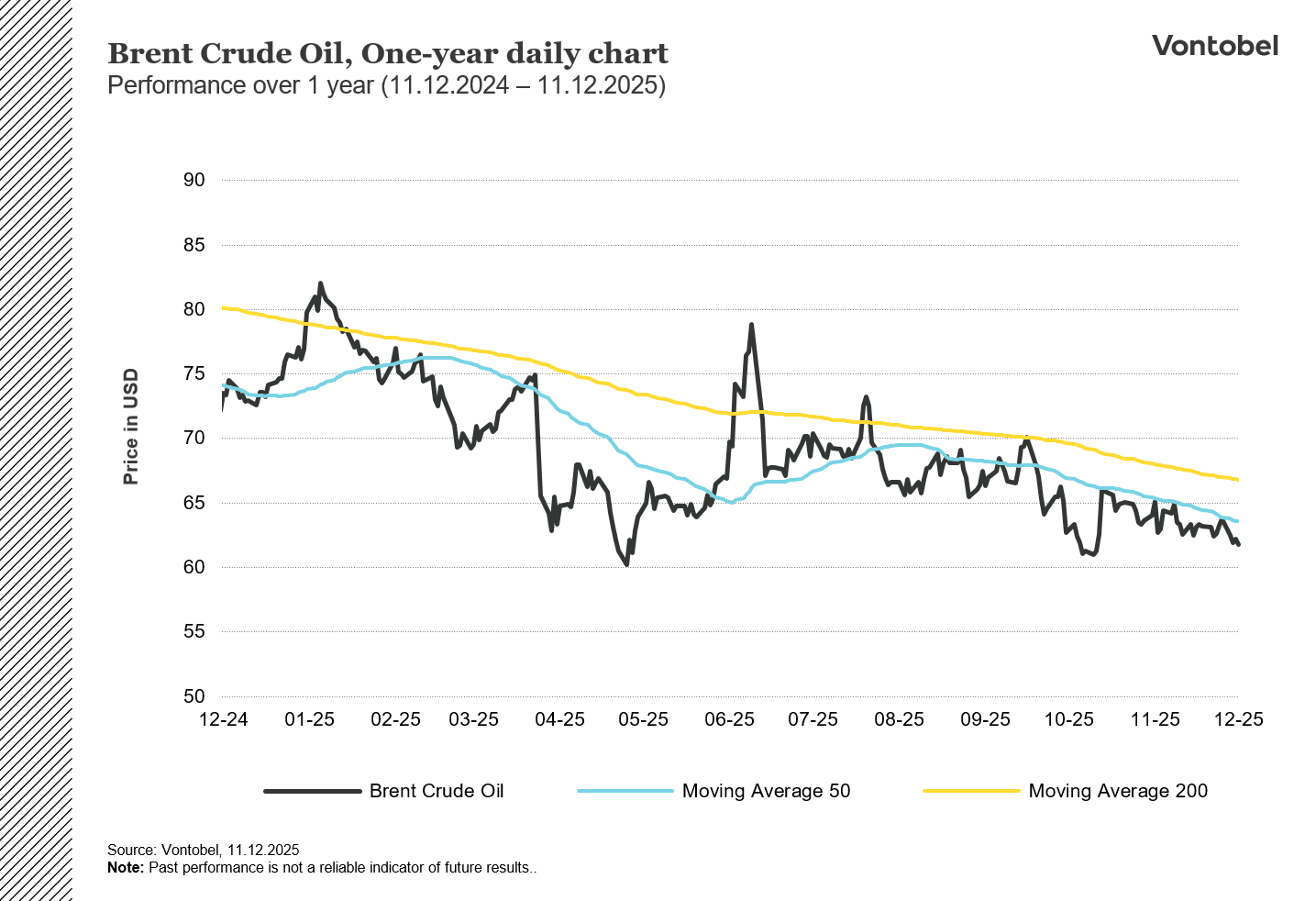

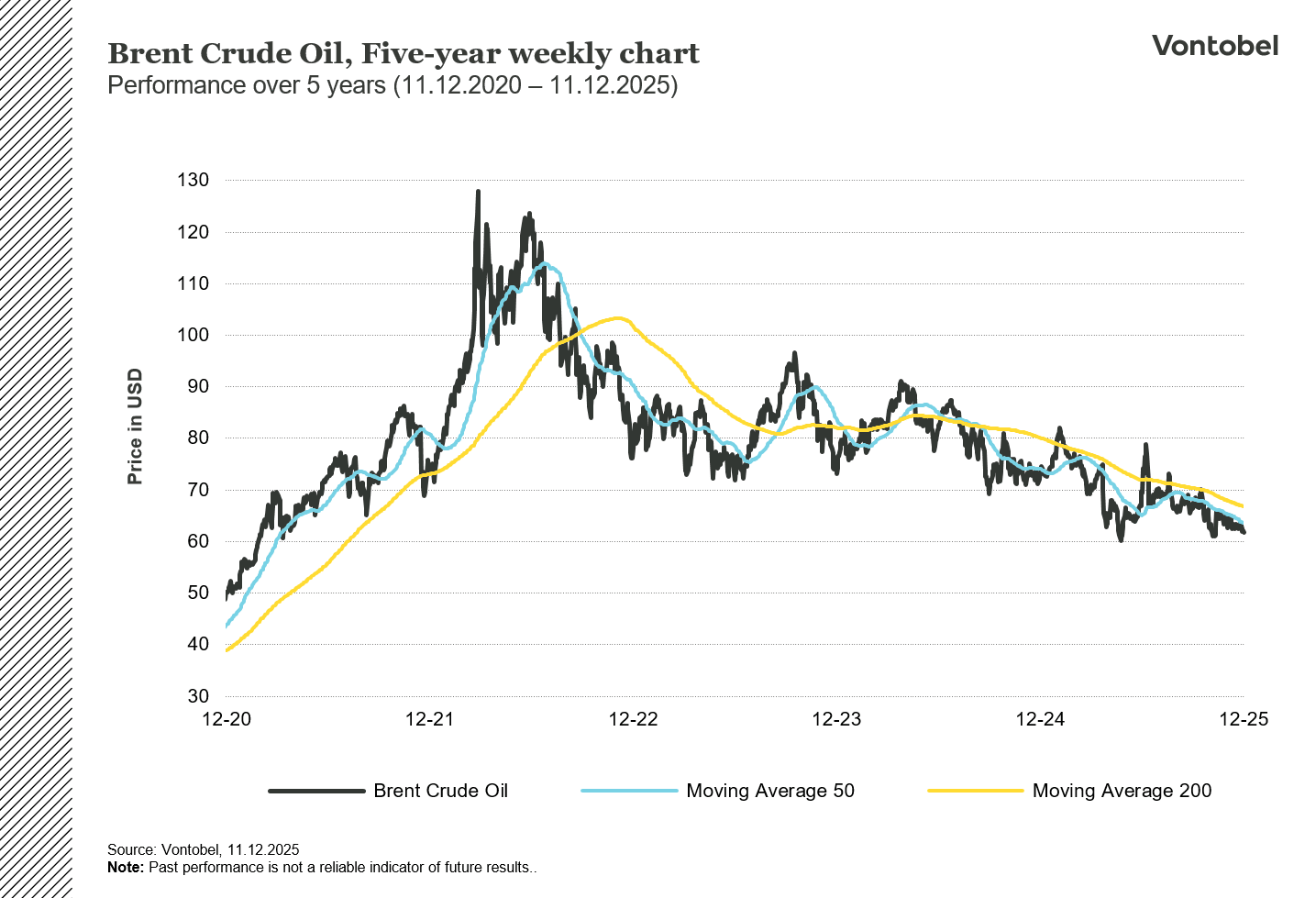

In November, oil markets showed a notable divergence, with refined oil products (such as diesel or gasoline) and crude oil moving independently in the first half of the month. Diesel led the market’s momentum, surging early in the month and pushing the Diesel-WTI crack spread to its highest level of the year. This strength in refining margins reflected tight diesel inventories, the upcoming European ban on fuel produced using Russian crude, and US sanctions on Rosneft and Lukoil at the end of October. Geopolitical factors added further volatility. Russian crude exports drew significant attention when India was reported to have significantly reduced its imports of Russian oil by around 650,000 barrels per day in November, down from over 1.5 million barrels per day in recent months. Meanwhile, continued Ukrainian attacks on Russian oil infrastructure underscored the fragility of supply flows. In the second half of November, Diesel came under severe pressure when hopes arose that a ceasefire between Russia and Ukraine could be established in the coming weeks causing sanctions against Russia as well as attacks on Russian oil infrastructure to fade. All oil commodities ended the month in negative territory between -25 and -4%.

Related Products

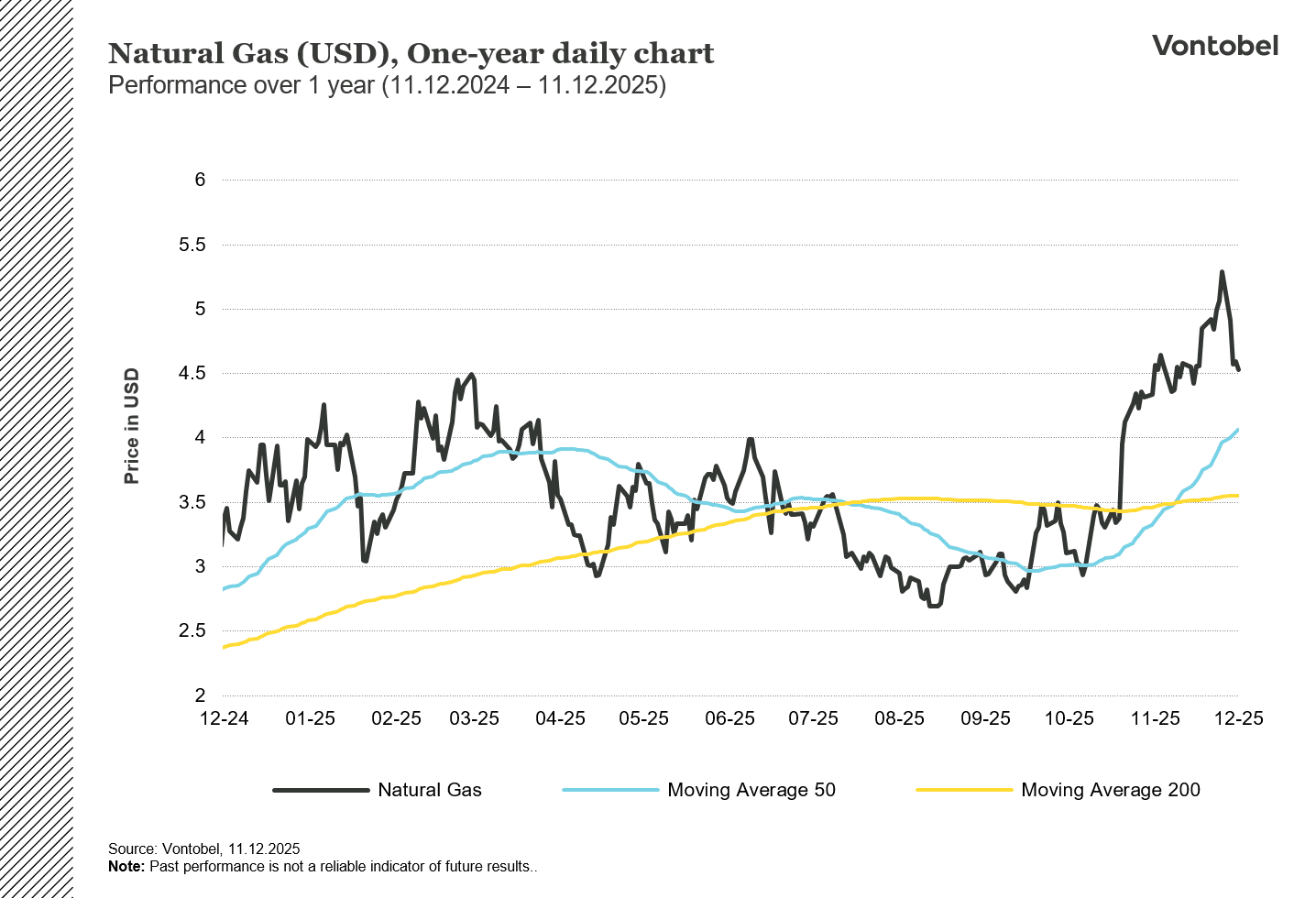

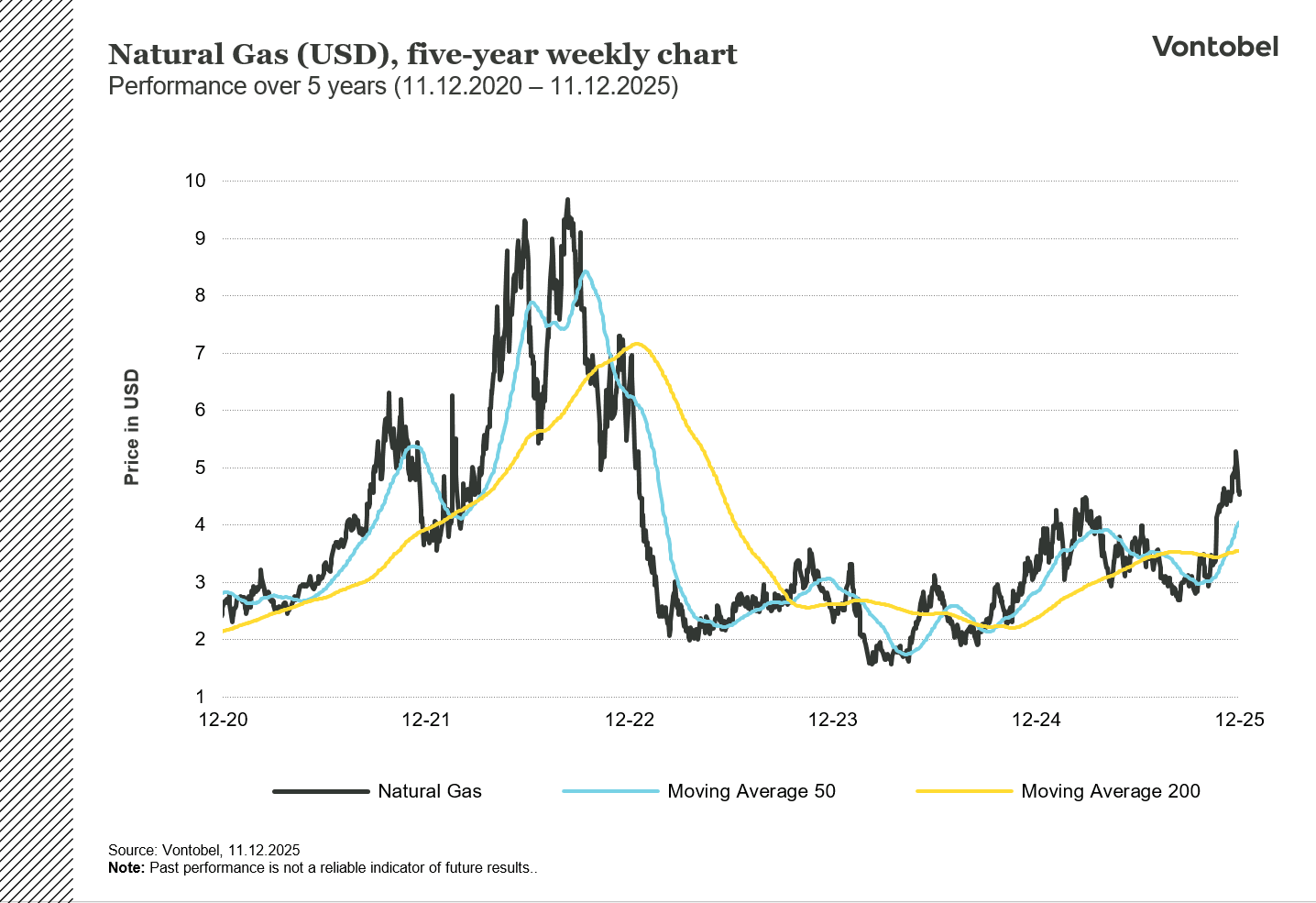

Natural gas prices surged in November (+11%) due to weather-related risks. Concerns about a stratospheric warming event, creating an imbalance in the polar vortex would allow for cold air from the arctic to flow into the Northern hemisphere in December. This is all but certain. However, the risk of a colder-than-normal winter weather in the US, pushed natural gas prices significantly higher.

Related Products

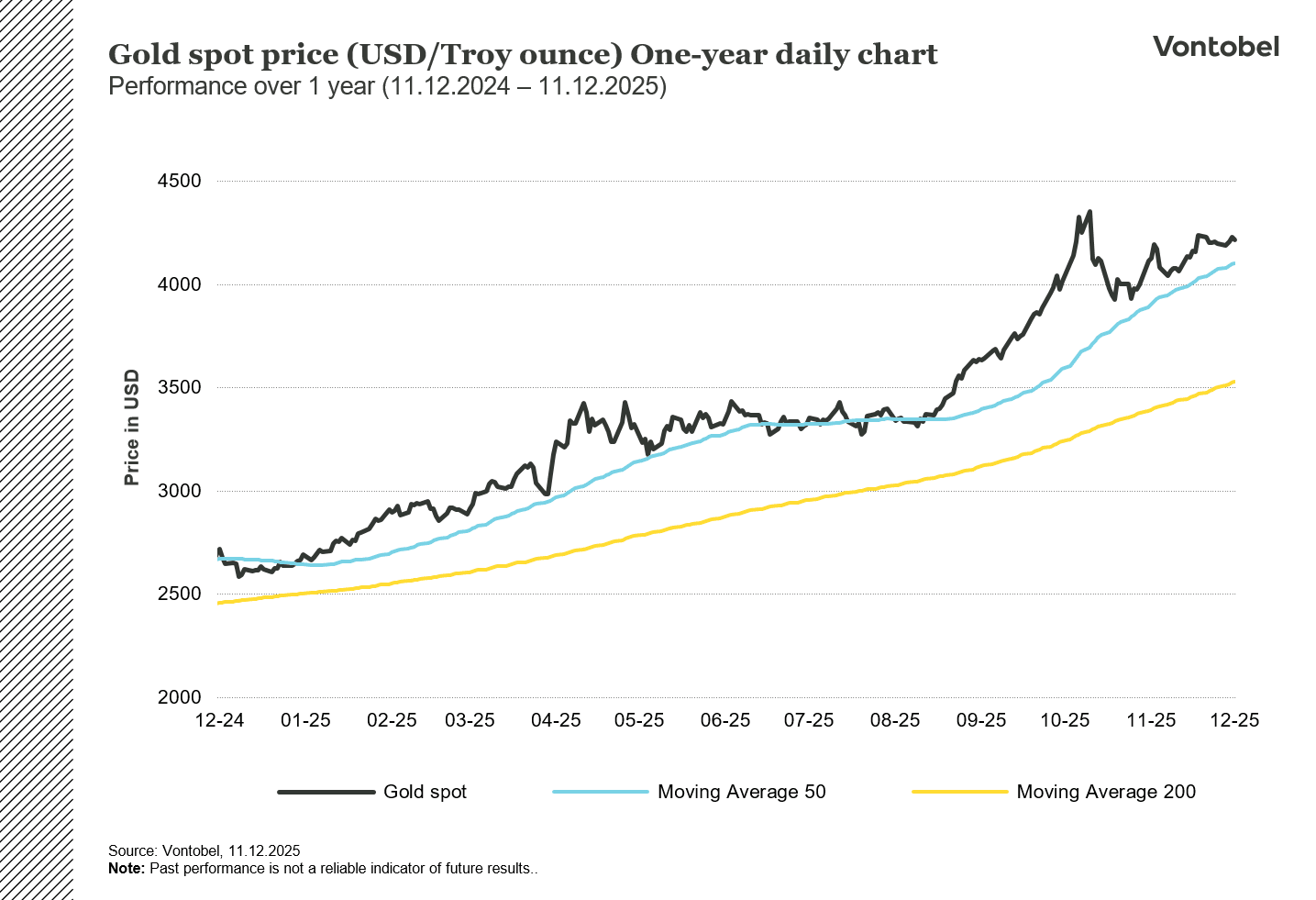

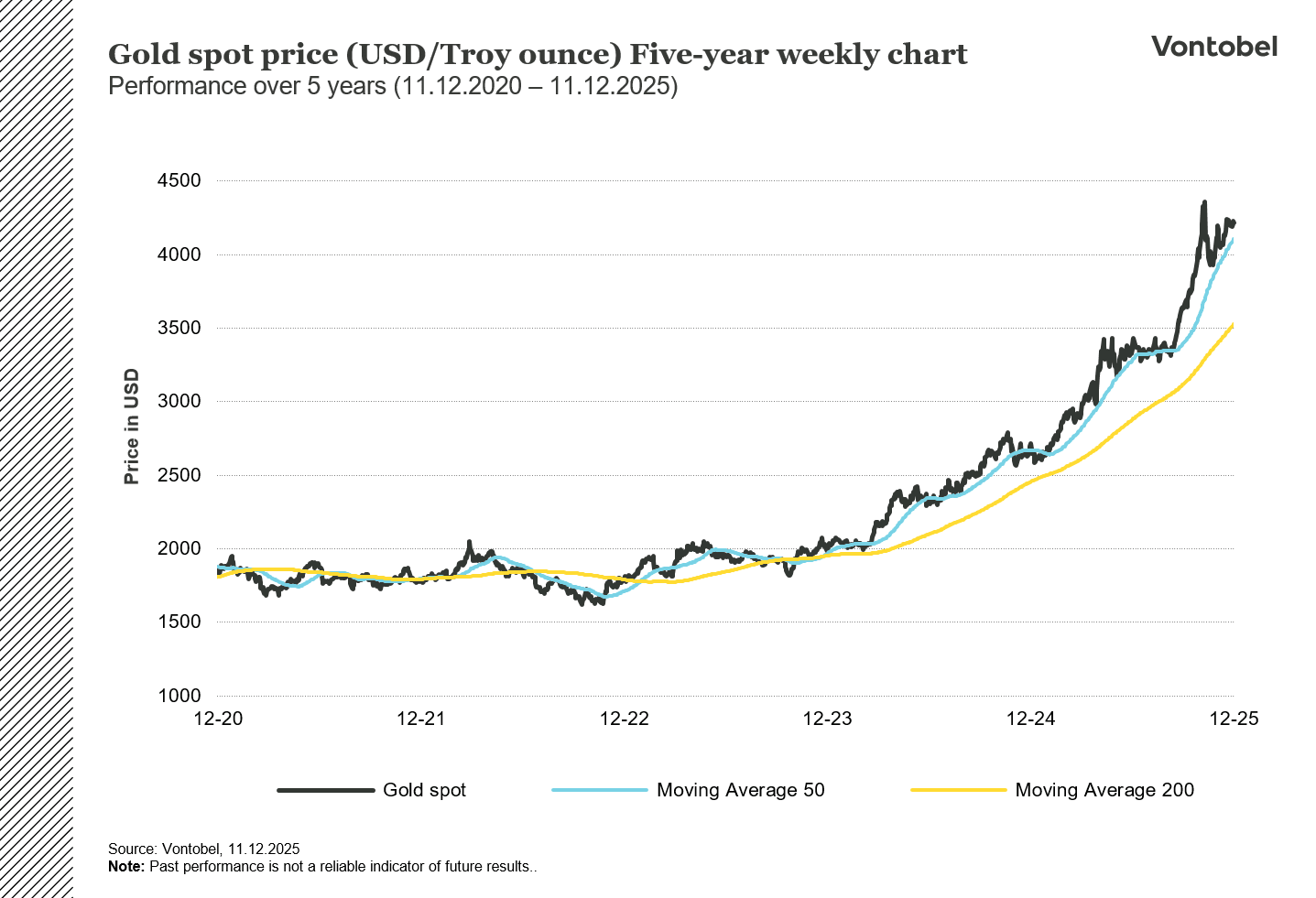

Divergence between precious and industrial metals

Precious metals experienced a consolidation phase during the first three weeks of November due to a lack of macroeconomic data, before seeing a month-end rebound spurred by dovish FED remarks. Silver was the top performer, closing the month up17.2%, followed by platinum (+7%), Gold (+5.6%) and palladium (+2.3%). Silver saw strong ETF inflows of nearly 2%, while COMEX inventories decreased for the second consecutive month, relaxing the tightness on the physical market and London lease rates eased. Short-term silver was pushed up by dovish macro news where the next FED rate cut shifted from 30% to almost certain. Longer-term silver finds support from a market deficit, and a weaker dollar. Similarly, platinum is supported by a deficit and physical backwardation, while palladium is pressured by oversupply. PGM’s remain sensitive to the outcome of the US Section 232 minerals review. On the gold side, despite central bank buying, ETF inflows remain muted despite central bank buying, leaving also gold vulnerable to macro swings as well.

Related Products

November was an uneventful month for industrial metals (+0.2%) with copper rising 2% while Nickel falling 3%. Notably, there is still an excess amount of copper flowing into the US due to fears of potential copper tariffs to be announced in mid-2026 and instated from 2027 on. This has caused US copper inventories to reach unprecedented levels, while Europe (LME) is experiencing a shortage, while the global inventory situation remains quite abundant.

Contrasting trends among the soft commodities

After rebounding in October (+6.5%) grains could not maintain their strong upside momentum and finished November up marginally higher with +0.4%. The main topic of discussion in the sector remains the trade agreement with China, which was announced at the end of October. However, the market had already priced in the hope of significant agricultural products shipments to China the previous month. This month, actual export announcements wanted to be seen by bulls. After some China soybean buying around the time of the trade agreement announcement, it took until mid-month for further purchases. Overall, it is estimated that China purchased ~2.5 to 3.0 million tons of US soybeans with delivery in December and January. After the Asian Summit, the US Administration announced the purchase of an additional 12 million tons of soybeans by the end of the year. China is well-equipped with beans from South America and US purchases until Brazilian soybeans come to the market in mid-January are pure goodwill purchases. The lack of buying from China also weighed on wheat, which fell 2.0% in November, as well as on soybean meal (-1.5%). Soybean oil, which lagged the rally last month, rose 2.0% in November, as US domestic soybean crush numbers exceeded expectations with 2 new crush facilities came online.

After two months of decline, soft commodities rebounded in November, rising + 2.6%. Sugar had its best month of 2025 and rose +5.4%. Sugar appears to have found a bottom, at least for the time being, after declining since mid-March of this year. Cocoa continued to trade lower (-12.4%) due to positive sentiment news in Western Africa, where favorable weather conditions are expected for the next crop. However, the inclusion of cocoa in the Bloomberg Commodity Index from 2026 on with a weight of 1.7%, starting in 2026 has not yet supported prices.

Livestocks (-3.7%) declined for the third consecutive month. Continued pressure from the US government on high beef prices weighs on live cattle (-4.9%) and feeder cattle (-3.7%). Fundamentally, the cattle market in the US is still tight, and some unusual cold weather in cattle areas at the end of November provided some relief to prices.

Outlook

For oil and refined products, a potential ceasefire between Russia and Ukraine remains a critical swing factor for oil and refined products. While it is not expected a meaningful progress in peace negotiations in the near term; however, the early-December talks in Moscow have lifted market expectations. Should a peace agreement been reached and sanctions on Russia be lifted or simply not get enforced, refined products would likely see a sharp sell-off, with crude oil also coming under pressure. Without geopolitical risk premiums, the underlying supply-demand balance is clearly bearish: Robust OPEC and substantial non-OPEC supply growth are expected to cause excessive inventory buildup through the first half of 2026.

For industrial metals, the key question is whether China’s export performance will weaken further after the soft October data. If China’s export engine continues to lose momentum, the sector may face short-term headwinds. That said, any downturn would likely only persist until the Chinese government ramps up its stimulus measures, which we expect to occur at some point in 2026. For grains, the fulfillment of the US/China trade agreement with soybean purchases will is critical to watch.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.