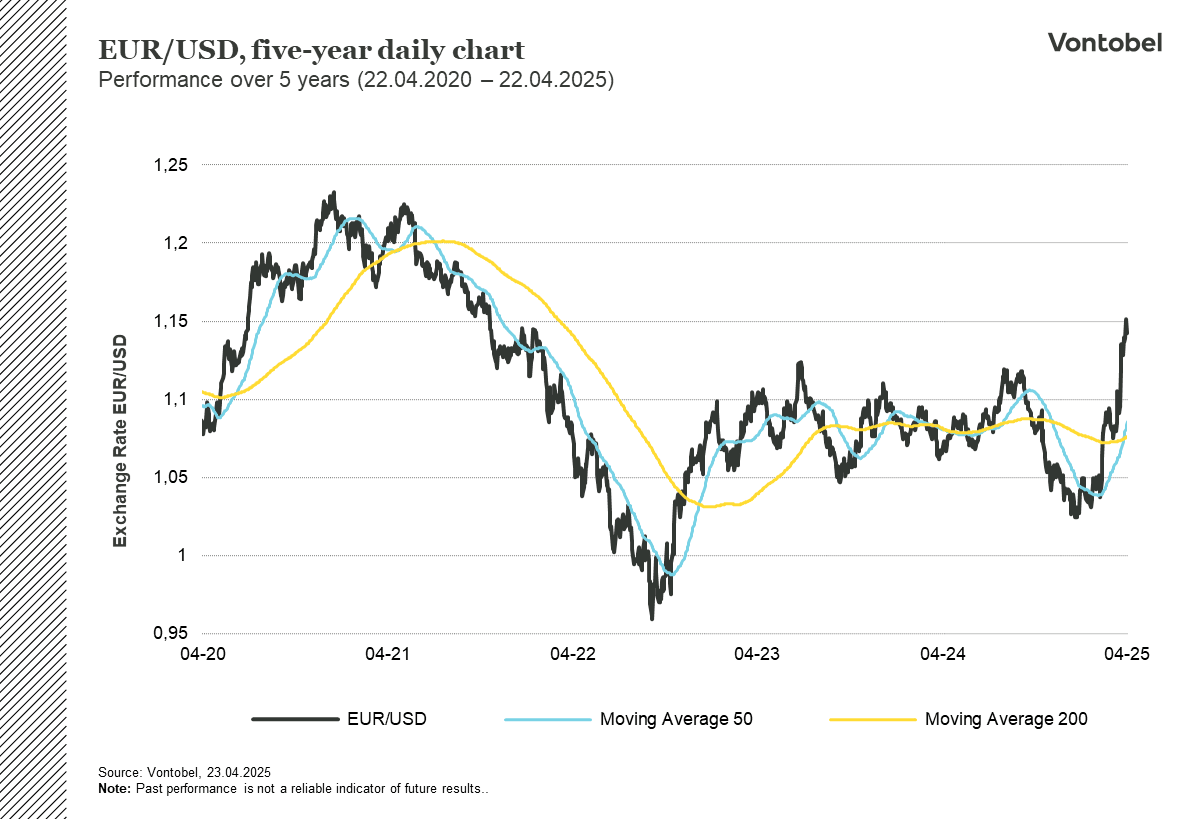

The unexpected rise of the Euro

Recently, the Euro has experienced a noticeable increase and, over the last month, has gained 5% against the USD. What makes this movement particularly interesting is the simultaneous increase in the interest rate spread between the US and the ECB. Normally, higher American interest rates lead to capital flows to dollar-denominated assets, which strengthens the dollar. However, this time the old relationship seems to be broken and no longer holds true, which points to a shift in investor sentiment.

A historical relationship is broken

Historically, German bonds and the Euro have moved in opposite directions. A strong Euro can usually be interpreted as economic optimism, which reduces the demand for secure investments like German bonds. However, currently, both the Euro and German bonds are rising, which is an unusual occurrence that can be interpreted as capital flight to the eurozone.

Since the traditional relationship between interest rates and German bonds is broken, it indicates a growing uncertainty among investors regarding American politics. Since 2022, the volatility in US Treasuries has remained high; yet, it has currently reached its highest level in over a year. Consequently, investors are increasingly questioning whether US Treasuries can still be considered the world’s ultimate safe-haven asset.

Stability over interest rate spreads

According to some interest rate experts, global investors are overlooking their exposure towards the US in favor of the eurozone, especially Germany, in search of stability, interest rate security, and a more politically predictable environment. Despite Germany’s bonds having had low or even negative interest rates in the past, they become an alternative since the government has promised to increase borrowing to finance new investments.

Simultaneously, the interest rate development seems to play a smaller role for the currency market than in the past. An interest rate spread of 2% in favor of the US would normally strengthen the USD; however, today we are experiencing the opposite. Importantly, this shows that today’s market cares less about interest rate spreads than political stability and predictability. Despite the change, it is unlikely that the USD will lose its role as the leading currency any time soon. The American bond market is still considerably larger and more liquid than Europe’s and dominates in world trade. Still, the change marks an important shift as institutional investors diversify into euro-denominated assets.

Related Products

The course remains uncertain

Ahead, the course remains largely in the hands of American politicians, who through their actions must address the growing concern in the market. If the volatility in the American bond market continues and trust in the American economy continues to deteriorate, the Euro stands to gain further. Ultimately, the unexpected strength in the Euro and the weakening of the dollar give insights into the occurring shift in capital flows — a development that could come to change the exchange market for several years to come.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.