Investors' Outlook: Licence for stimulus

Donald Trump’s trade policies have rattled US business and consumer sentiment. His confrontational approach to Europe, exemplified by his handling of the “Ukraine question”, has served as a wake-up call for European policymakers. In response, they’ve rolled out historic stimulus measures, capturing the attention of financial markets and prompting investors to flock to alternative equity regions in recent weeks.

From a macroeconomic perspective, conditions have worsened since February. The US growth outlook is deteriorating, weighed down by mounting uncertainty affecting both the industrial and consumer sectors. Despite this, recession fears may be overblown. The underlying fundamentals—like the strong US labor market and consumer, or healthy household balance sheets—remain solid, and many of the newly imposed tariffs are likely to be temporary.

Outside the US, several economies are benefiting from a new wave of monetary and fiscal stimulus—both implemented and pledged. Germany, once the fiscal scourge of Europe, has agreed to reform its constitutional debt brake, paving the way for a multibillion-euro spending spree. And China, the world’s second-largest economy, has also announced expansive stimulus plans going forward. Still, the longer trade uncertainty lasts, the more damage it risks inflicting—not just on the US, but on the global economy. While central banks’ wait-and-see stance is understandable to some extent, there’s a growing risk, particularly for the Fed, of falling behind the curve by reacting too late. The Multi Asset team shares the market’s expectation that the Fed will look past inflation fears and follow through on at least two rate cuts in 2025, especially as growth concerns tied to tariffs intensify.

A view to a ceasefire

After three years of conflict, the possibility of a ceasefire between Russia and Ukraine has increasingly come into focus following US President Donald Trump’s return to office. European equity markets have reacted positively, beginning to price in a more optimistic outlook. But what would a ceasefire mean for Europe? The Multi Asset Boutique explores the potential implications for the region’s economy and equities.

“I will prevent, and very easily, World War III […] I will have the disastrous war between Russia and Ukraine settled. And it will take me no longer than one day”. Throughout his presidential campaign, Trump repeatedly claimed he could end the war between Russia and Ukraine within 24 hours. However, he has since acknowledged that resolving the conflict may be more complex than initially suggested. While the timeline remains uncertain, the Multi Asset team believes that a ceasefire will eventually be reached.

To assess the potential economic impact, it is important to distinguish a ceasefire from a peace deal. A ceasefire is not a final resolution but rather an initial step that halts fighting, creating an opportunity for negotiations toward a peace deal. Current diplomatic efforts are mainly focused on achieving this first step.

A ceasefire would offer partial conflict resolution, but some uncertainty would remain. The most optimistic scenario would involve the signing of a comprehensive peace deal that ensures long-term stability, which would bring more significant economic benefits for Europe. However, such an agreement could take time to materialize.

What gives the Multi Asset team the confidence that a ceasefire could be reached in the coming months? Beyond war fatigue, all parties have their own motivations for restoring peace in the region. For the US, reducing military aid to Ukraine could ease some fiscal pressures and free up resources for other priorities. Politically, a ceasefire would allow Trump to position himself as a peacemaker, potentially boosting his domestic approval. Additionally, resuming commodity supplies—particularly energy—could help lower prices, a key objective for this administration.

In Europe, public support for aiding Ukraine has waned, with growing pressure to redirect military resources. While European governments remain strategically aligned with Ukraine, many view de-escalation as necessary to address internal political and economic challenges.

For Russia, the situation might be less straightforward. President Vladimir Putin’s recent approach suggests that Russia may try to prolong negotiations while attempting to secure additional territorial gains and concessions from the US and Ukraine. However, domestic factors also play a role. The war has become increasingly unpopular at home, and after an initial wartime economic boom, Russia is now grappling with high inflation and interest rates above 20 percent. A ceasefire could help conserve financial resources while allowing Putin to portray the outcome as a strategic victory.

The Multi Asset team has identified five main economic channels through which a resolution to the conflict could impact Europe:

1. Energy—lower prices

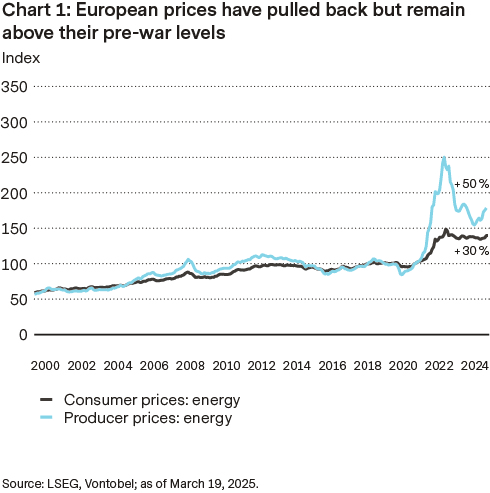

Lower energy prices are arguably the most important economic benefit that could result from a ceasefire. Following the invasion, energy prices in Europe spiked amid supply disruptions and rising geopolitical risk premium. While prices have since stabilized, they remain well above their pre-invasion average for both consumers and producers (see chart 1).

A decline in energy prices, potentially driven by the resumption of direct flows from Russia to Europe, would support consumer spending and economic growth. However, the extent of price reductions depends on supply dynamics, raising a key question: How much could direct flows from Russia resume, and how far could prices fall?

For Russian crude oil, exporters were already able to redirect tankers to refineries in Asian countries that did not recognize Western sanctions. As a result, the geopolitical risk premium tied to the Russia-Ukraine war had already faded from crude oil prices.

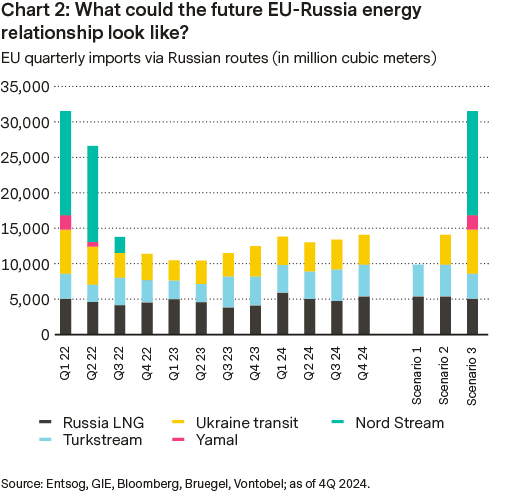

While the European Union sanctioned Russian crude oil, it shied away from imposing similar bans on Russian gas. Instead, Europe took significant steps to reduce its reliance on Russian gas. Of the five pipeline routes that once supplied Europe, only one remains operational today—via Turkey. To compensate, Europe resorted to buying liquefied natural gas (LNG) from suppliers such as the US, Norway, and Qatar. However, it also continued buying Russian LNG, at a much higher premium.

Although it may be tempting to price in a resumption of pipeline flows, it seems a politically and economically delicate dance. Some pipelines have been damaged, and most European leaders have expressed reluctance to depend on Russian pipeline gas again. Trump favors increased European purchases of US LNG, which could serve as leverage in future trade negotiations. From an economic standpoint, Russia may also prefer LNG over pipelines, as it offers higher earnings.

There are three potential scenarios for the future of Russian gas flows to Europe (see chart 2). In scenario 1, the status quo is maintained, with no changes to current gas flow levels. Scenario 2 involves a partial resumption, where pipeline flows through Ukraine return to 2024 levels. The most optimistic outcome would be scenario 3: a full resumption, in which gas flows via Ukraine are restored, and damaged infrastructure, such as Nord Stream 1 and the Yamal pipeline, is repaired.

Only Scenario 3 would likely exert enough downside pressure on European gas prices to bring them back to pre-war levels. But who would benefit most from these lower gas prices? Consumers, as well as cyclical sectors and countries, such as Germany or France, would see the greatest gains, while defensive markets like Switzerland and energy producers would benefit less. However, as things stand today, the Multi Asset team is skeptical whether European policymakers are willing to revert to a “pre-war world” anytime soon.

2. Reconstruction—investment in rebuilding Ukraine

After energy, the reconstruction of Ukraine is a major focus. Rebuilding war-torn areas will require significant investment, with estimates ranging from USD 155 billion to USD 486 billion over 10 years. The final cost will depend on how much territory Ukraine ultimately retains, as much of the destruction is in Russian-occupied regions. Additionally, many pre-war industries may never return to full operation.

As a result, most analysts estimate annual reconstruction spending to be closer to USD 10 billion to 20 billion, equivalent to just about 0.5 – 1 percent of the EU’s current annual construction spend. Another key consideration is whether any agreement guarantees free passage through Ukraine’s Black Sea ports, an essential trade route. Without unrestricted access, European investment could be deterred.

3. Defense—shifts in European military spending

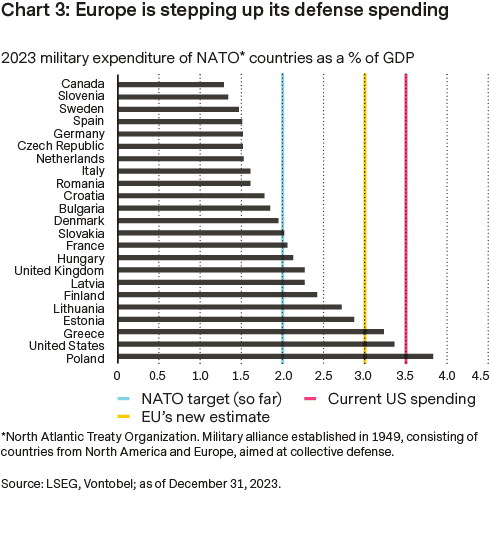

Another area drawing increasing attention is defense. The recent US disengagement from Europe’s military scene has prompted European leaders to ramp up their own defense spending. In early March, the EU proposed a plan to ease fiscal rules, unveiling a EUR 800 billion initiative to strengthen military capabilities. Shortly after, Germany announced a EUR 500 billion plan to expand infrastructure and military spending. Assuming a gradual implementation of these measures, European defense spending could rise toward 3 percent over the next two to three years (see chart 3). If this defense-related capital expenditure is geared toward domestic military production, it could provide a fiscal boost that acts as a tailwind for European economic growth, particularly for countries with lower fiscal deficits, such as Germany. Overall, the geopolitical shifts may mark the beginning of deeper European integration.

4. Confidence—improvement in sentiment

The outbreak of the war in early 2022 triggered a sharp decline in Eurozone consumer confidence, coinciding with heightened geopolitical uncertainty and rising inflationary pressures. While confidence and the Geopolitical Risk Index linked to Ukraine have since rebounded, they remain below pre-war levels, with elevated savings rates. This suggests that, should a ceasefire be reached, it may lead to a slight increase in confidence, potentially supporting consumer spending.

5. Migration trends—the return of Ukrainian refugees

As of January 2025, approximately 4.3 million Ukrainian refugees were registered under the EU’s temporary protection program, with the majority residing in Germany and Poland. Studies suggest that their presence has modestly increased the EU’s labor supply and potential economic output by 0.2 – 0.3 percent so far, while also contributing to higher public spending. If refugees return to Ukraine, this trend could reverse, though future migration patterns will likely depend on both the terms and perception of any peace agreement. In addition, many Ukrainians have now established new lives in their host countries. Survey data indicates that about 11 percent have already returned, and another 35 percent plan to do so if the war ends.

The potential impact on European equities

Turning to the potential implications for markets and European equities, a look at the correlation between various market segments and ceasefire probability reveals that the construction and materials sectors have demonstrated the strongest positive relationship. Furthermore, cyclical sectors such as airlines and financials also exhibit positive correlations, while defensive segments like healthcare and telecommunications tend to have negative correlation. While the defense sector is historically negatively correlated with rising ceasefire probabilities, it should continue to benefit from recent trends in military spending across Europe.

In terms of valuation, European Monetary Union (EMU) equities have risen sharply, now trading above their prewar price-to-earnings (P/E) ratios. However, on a relative basis compared to US equities, they still trade at a discount, though this valuation gap has narrowed significantly since the start of the year.

Analyzing year-to-date performance, not all of the market rallies can be attributed to improving fundamentals, such as rising EU and global Purchasing Managers’ Indices (PMIs) or a strong 4Q earnings season. A large portion of the gains appears to be driven by increased optimism about European growth, fueled by higher military spending, fiscal initiatives, and hopes for a ceasefire.

This suggests that much of the ceasefire-related optimism is already priced into European equities, particularly in sectors most closely correlated with the ceasefire probability. The expected impact of a potential peace deal on aggregate earnings remains relatively small—at least for 2025.

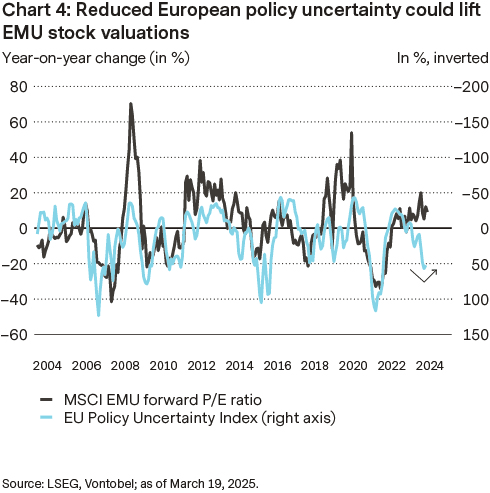

One potential driver for continued European equity outperformance could be a re-rating and improved sentiment, rather than significant earnings growth. As shown in chart 4, there is still room for improvement in economic policy uncertainty in Europe, which has historically supported higher valuations. However, uncertainties around US trade policy remain elevated and could also influence European asset prices.

The Multi Asset Boutique concludes that while a ceasefire could have a marginal positive impact on the European economy, only a comprehensive peace deal would create a solid foundation for investment. A lasting agreement would likely drive capital expenditures, reopen trade routes, normalize energy supplies, and effectively drive economic growth. The overall effect will largely depend on the specific terms of the deal. Second-round effects, such as improved sentiment and reduced uncertainty, could play a greater role in supporting European stock performance. Increased fiscal spending is expected to be an additional growth driver for Europe moving forward, while the developments in US tariffs also warrant close attention.

Skyfalling confidence

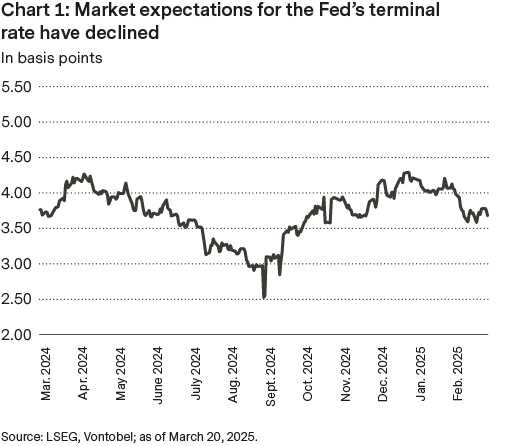

Tariffs are now the main driver of economic uncertainty, with record-high trade concerns weighing on business sentiment and consumer confidence. Unlike in 2017, tariffs have taken priority, while future policy changes remain unclear. Markets expect slowing growth and multiple Fed rate cuts, with the terminal rate projected just below 3.75 percent (see chart 1).

For now, tariffs remain the biggest wildcard. Key questions are: How broad will they be, and at what rates? The situation grows more complex by the day, compounding uncertainty in an already volatile economic landscape. The

Trade Policy Uncertainty Index, which tracks mentions in news, shows confusion has surged. Current levels exceed those during the first Trump administration. Overall economic uncertainty is running four times higher than the norm, while trade-related uncertainty is a staggering 25 times higher. Unfortunately, there’s little reason to expect clarity soon. The trade war looks set to escalate and drag on, further weakening business sentiment and consumer confidence. In this climate, companies may delay investments, and consumers could pull back on spending—adding another headwind to growth.

Beyond direct tariffs effects, the lingering uncertainty threatens to steer the US economy into choppy waters.

Compounding this, the Trump administration’s shifting tone signals higher tolerance for short-term economic disruption in pursuit of long-term policy goals. Unlike in 2017, when deregulation and tax cuts preceded tariffs, the current strategy flips the script: tariffs first, with future reforms uncertain.

Markets are reassessing the outlook amid unclear fiscal policy and slowing consumption. Over the next year, expectations reflect a bit more than two and a half rate cuts.

Despite rising equity-market volatility and policy uncertainty, investment-grade corporate bond spreads remain remarkably tight—near historic lows (see chart 2). This defies Merton’s theory that higher volatility should widen spreads. Under his structural credit risk framework, a corporate bond can be viewed as a government bond plus a short put option on the issuer’s assets. In theory, this means rising volatility should boost the value of that put option, reducing the bond’s price and widening spreads in line with higher default risk. During periods of market stress, falling equities and surging volatility typically pressure corporate bonds. Yet so far, spreads have barely budged.

US exceptionalism on pause

Markets are increasingly concerned about Donald Trump’s policies just 10 weeks in, with sentiment shifting rapidly. The April 2 tariff announcement exceeded expectations in both size and scope. While some effects were priced in since February, uncertainties around duration, retaliation, and economic impact persist.

March saw a widening performance gap between US equities and global markets amid three key drivers. First, after initial post-election optimism, markets are now focused on potential downsides of the Trump administration’s policies—particularly tariffs. Concerns include weaker consumer confidence, rising inflation (which may limit Fed rate cuts), and delayed corporate investments, all of which raise recession or stagflation risks. Worries intensified on April 2, as Trump’s proposals could raise the weighted average tariff on US imports from 2.5 percent at end-2024 to 24 percent—levels unseen since the 1920s.

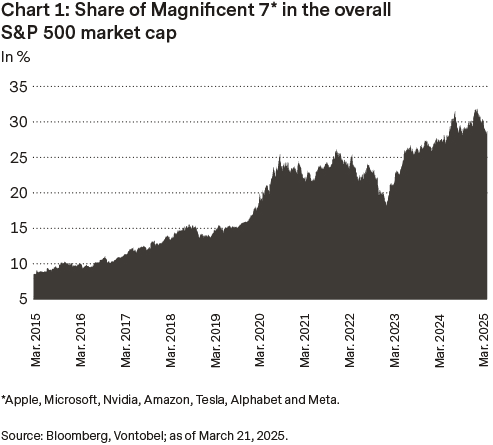

Second, the performance of stocks related to US technology and artificial intelligence (AI), major market drivers in recent years (see chart 1), has weakened.

Chinese AI breakthroughs have shaken confidence in US tech dominance, especially in monetizing massive investments and capital expenditures (see chart 2).

Combined with weaker earnings forecasts and high valuations, this has led to multiple compression. Third, Europe’s defense spending and China’s stimulus plans have fueled a regional rotation, benefiting European and Chinese equities.

Is US exceptionalism over? Probably not, but these uncertainties have put it on pause. 2025 earnings forecasts have barely moved since the November, leaving room for revisions as earnings season begins. Investor focus will be on tariff-driven margin pressure and pricing power. This could further weigh on valuations, which, even after March’s correction, remain above historical averages. A catalyst is needed to sustain them, and fundamentals must hold. US stocks remain fundamentally strong, and once trade uncertainty fades, momentum could return.

Dr. Demand

Last month, global manufacturing kept expanding, major economies announced stimulus measures, and the US dollar weakened. Throw in tariff-related supply concerns, and you have a promising backdrop for a cyclical asset class like commodities… right?

Well, performance was mixed. Crude oil fell another 5 percent as the Organization of the Petroleum Exporting Countries and its allies (OPEC+) announced it would gradually unwind some of its voluntary production cuts starting in April. The prospect of higher supply coincided with fears that demand may be weaker than expected this year, mostly due to the trade war and its negative impact on global growth.

Prices found some support after a US operation targeted Iran-aligned Houthi rebels, and again when a US export license for Venezuelan oil expired. But both effects were short-lived. With rising OPEC+ output and downside risks to the demand side, oil prices are likely to stay capped in the mid-60s to low 70s.

The main upside risk is Trump’s Iran strategy. Having managed to “bring down oil prices”, there is a risk that he returns to a more hawkish Iran policy, as in 2018. Still, a full-blown confrontation is rather unlikely, as it would clash with his goal of seeing oil prices at or below USD 50 per barrel.

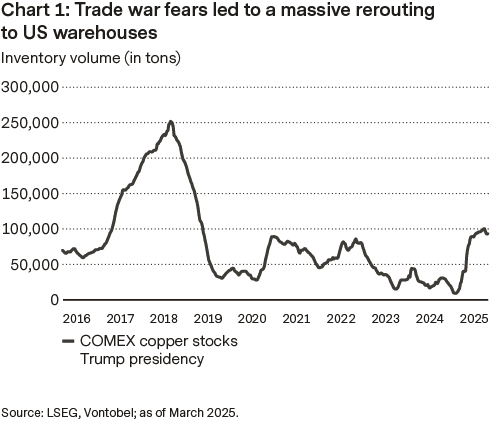

Industrial and precious metals did very well. The rally in industrial metals had more to do with tariffs —both imposed and threatened (e.g., steel, aluminum, copper)—than with strong consumer demand. This led to a disconnect in many markets as traders rushed to ship metals to US warehouses (see chart 1). Important consumer China announced new stimulus, though it mostly focused on boosting private consumption (not the housing market, which is key for metals demand). Europe’s planned stimulus (e.g., infrastructure, defense) could lead to higher metals demand, but its impact will likely only unfold over several years.

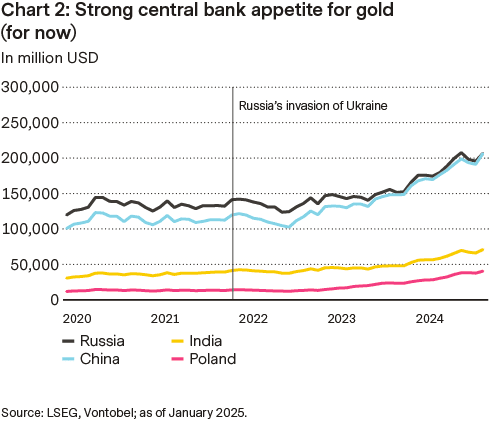

Gold was the standout. It broke through the psychologically important USD 3,000 per ounce level in mid-March, propelled by (geo)political and trade uncertainty as well as a weaker US dollar. While many of the Multi Asset Boutique’s assumptions (weaker dollar, real yields, and a Fed that may have to cut more than what is currently priced in) argue for further upside, it is crucial to get the “central bank question” right. It remains to be seen whether central banks will hold on to gold after they already went on a buying spree in 2024. For now, the latest available data suggests demand remains positive (see chart 2). Rising demand from exchange-traded funds could partially (but not fully) offset a slowdown from central banks.

The dollar is not enough

Forty years after the Plaza Accord, talk of a new “Mar-a-Lago Accord” to weaken the dollar has emerged, aimed at reviving US manufacturing and addressing fiscal woes. But critics warn it could disrupt global markets, erode trust in US Treasuries, and strain alliances. Might responsible fiscal reform be a safer alternative?

The 1985 Plaza Accord, forged at New York’s Plaza Hotel, marked a turning point in economic collaboration. Major economies agreed to weaken the dollar to boost US competitiveness. Now, whispers of a Mar-a-Lago Accord suggest a similar plan to depreciate the dollar in hopes of aiding US manufacturing.

Under the proposed plan, the US would push partners to weaken the dollar by selling US dollars and Treasuries, then shifting remaining holdings into long-duration bonds, possibly century bonds. In exchange, the US would lower tariffs, with the threat of reduced military support for noncompliance. This approach raises pressing questions. Can the US rebuild manufacturing without economic disruption? Will moving away from globalization fuel inflation via higher domestic costs? And would other nations, under pressure, reduce economic ties with the US, undermining the accord’s viability? Critics argue that a strong dollar can also bring benefits: it lowers borrowing costs and enhances international stature. Trade deficits, often viewed negatively, can actually help avoid economic overheating. A sustained dollar-weakening effort would require sweeping policy shifts. Ultimately, the proposed Mar-a-Lago Accord risks destabilizing the dollar and US Treasuries, suggesting that fiscal reform might be a wiser and more stable approach than pursuing aggressive trade policies.

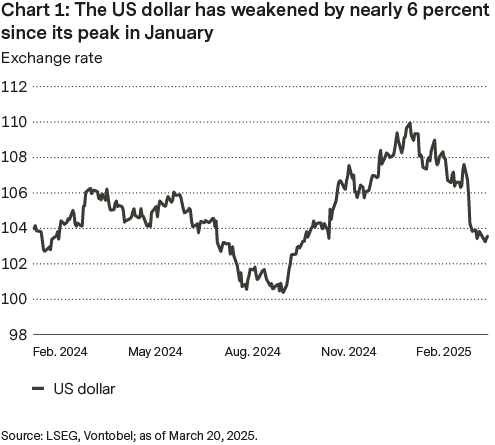

For some time, the euro-dollar pair lacked momentum. Conditions didn’t favor a stronger euro, and the currency drifted. But that’s changing. A slowdown in the US economy prompted a 6 percent appreciation in the euro from early-year lows (see chart 1).

Meanwhile, Europe is changing its fiscal policy to stimulate growth. These measures aim to give the euro a much-needed cyclical boost and strengthen its long-term appeal. Combined with softer US growth, this is reshaping the euro-dollar exchange outlook. Germany’s fiscal adjustments and a weakening US economy are pushing the euro upward and weakening the dollar (see chart 2), which benefits the Swiss franc. The Swiss National Bank now faces a nuanced environment: while a strong franc once helped curb inflation via cheaper imports, with inflation now stable, the SNB may reconsider its strategy.