Reverse Convertibles: How they work

Reverse convertibles offer investors the opportunity to profit from sideways movements in the price of an underlying asset, usually a share. Similar to a bond, a reverse convertible features a coupon that is fixed at the time of issue and is generally paid out at the end of its term. The repayment of the nominal amount, on the other hand, depends on the performance of the underlying asset. A predetermined price level (strike price) is of decisive importance here. If the price is at or above the strike price at the end of the term, the investor will receive the nominal amount back. If the price is below the exercise price on the maturity date, the investor will be delivered units of the underlying with the settlement type “physical delivery”, the value of which will usually be less than the nominal amount. Alternatively, a cash settlement is also possible.

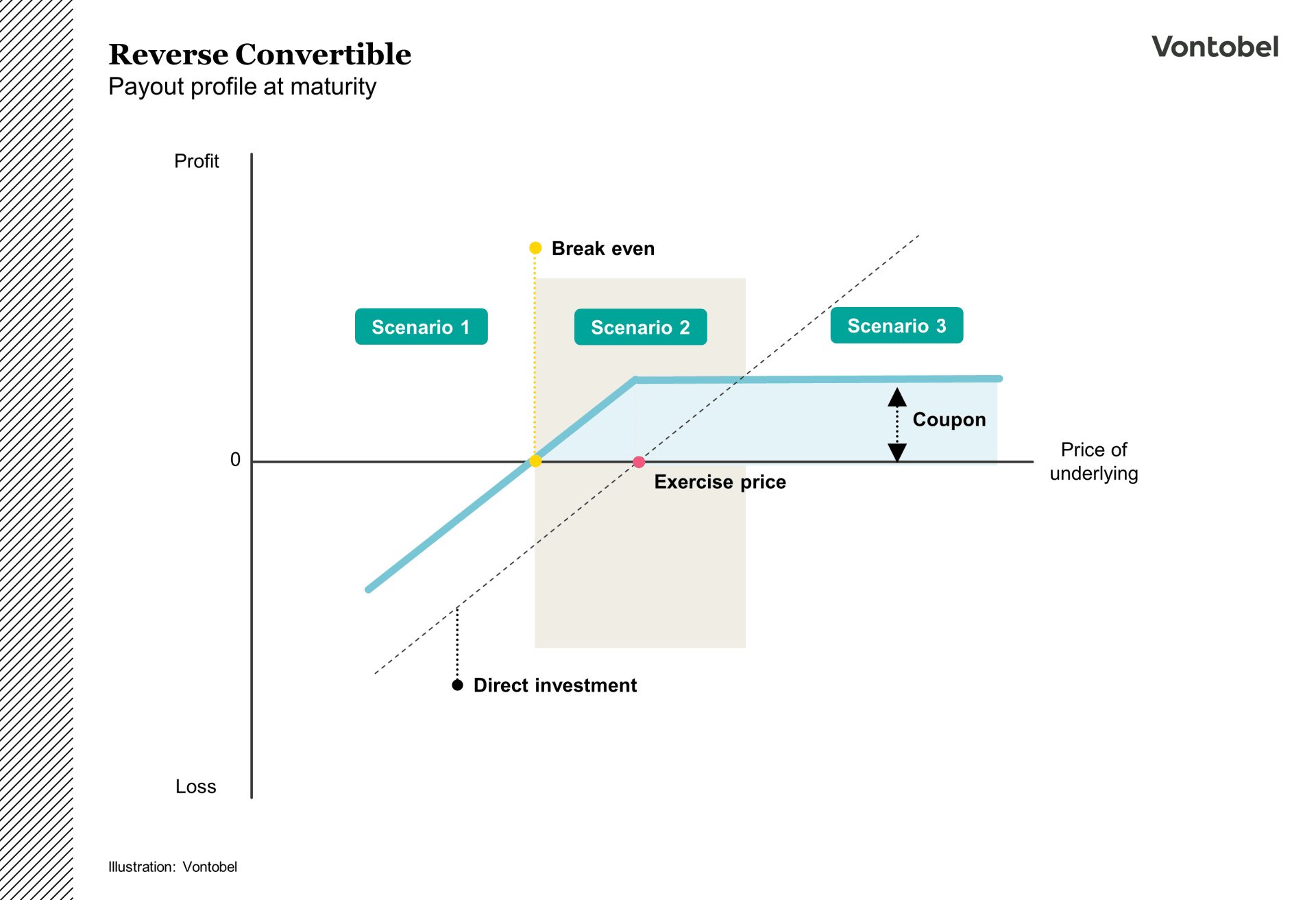

How Reverse Convertibles work

Reverse convertibles fall under the category of investment products and can be an interesting instrument for investors who expect sideways or slightly rising prices as a means of optimizing their returns in such market phases. A Reverse Convertible often offers an attractive coupon, which is usually paid out at the end of the term and whose attractiveness is accompanied by an increased risk. This risk is reflected in the fact that the repayment of the nominal amount depends on how the price of the underlying asset develops up to the end of the term. In this context, the exercise price set at the beginning of the product's term is decisive. If the price of the underlying is at or above the strike price at the end of the term, the investor receives the nominal amount. However, if the price of the underlying is below the strike price at the end of the term, the investor is either delivered units of the underlying or a cash settlement is paid. The investor therefore receives less than the nominal amount. However, the coupon is still paid out in this (negative) scenario, which can cushion possible “discounts on the nominal amount”. Nevertheless, losses may occur if prices fall more sharply.

Scenarios

To understand when it might be worthwhile for investors to buy a reverse convertible, it is useful to compare this product with a direct investment in the underlying asset. This comparison is also illustrated graphically in the figure below. Three scenarios are considered at the end of the term.

In scenario 1, the underlying loses a lot of value and the price is far below the strike price at the end of the term. An investment in both the reverse convertible and the underlying is associated with (significant) losses. Nevertheless, in this scenario the reverse convertible is superior to a direct investment, as the coupon is paid out independently of the redemption. The redemption amount of the reverse convertible - consisting of the delivered underlying and coupon - is therefore higher than the “residual value” of the direct investment (possible dividends not taken into account).

In scenario 2, the underlying moves either sideways or rises / falls slightly until maturity. This is where the reverse convertible really comes into its own compared to a direct investment in the underlying. This is because while the underlying asset provides the investor with hardly any price return (and possibly a dividend), the reverse convertible offers a coupon that can often be significantly higher. Even a slight fall in the share price below the strike price, combined with the delivery of the underlying security, can be compensated for by the coupon up to a certain point.

In scenario 3, the price of the underlying rises sharply over the term and is therefore significantly higher than the strike price at the end of the term. In this case, a direct investment in the underlying would have been more advantageous, as there is no upper limit to the profit potential. With a reverse convertible, on the other hand, in this optimistic scenario a return is only generated in the amount of the coupon and possibly a price gain. The participation in rising prices is therefore limited upwards.

Investors “buy” the advantages of the reverse convertible compared to a direct investment in the event of a sideways or moderate fall in the price of the underlying asset by forgoing participation in rising prices of the underlying asset above the strike price. At the same time, as with all structured products, investors bear the issuer's default risk.

Influencing factors

As the above section suggests, the pricing of a reverse convertible over the term is based on the value of the put option and the zero-coupon bond, among other things. Therefore, in addition to the price of the underlying asset, other price-forming factors of options, such as the implied volatility (expected fluctuation margin), the remaining term and - particularly with regard to the zero-coupon bond - the interest rate level, are also included in the price of the product. An increase in the underlying value leads to a higher price of the reverse convertible if the other variables do not change. The reason for this is that the greater distance from the strike price increases the probability of repayment of the nominal amount. The picture is different with an increase in implied volatility. Increased volatility increases the probability that the price of the underlying will end below the strike price due to the greater fluctuations and that the nominal amount will therefore not be repaid. This would therefore result in a lower price of the reverse convertible during the term. A decrease in the remaining term, on the other hand, has a “supporting” effect on the price of the reverse convertible, as the price of the underlying can generally deviate less from the exercise price within a shorter period of time. An increase in interest rates during the lifetime of the reverse convertible has a negative effect on the price of the reverse convertible, as the zero-coupon bond loses value. However, the redemption profile at the end of the term, which is shown graphically in the figure above, does not change due to temporary influencing factors such as volatility and interest rate levels.

Advantages and Risks

Advantages of reverse convertibles

- Comparatively high coupon rate above market level

- Yield optimization possible in sideways trending markets

- Manageable investment horizon (usually one to two years)

- Large selection of exercise prices enables individual risk management

- A barrier can protect against moderate price setbacks in the underlying asset

Risks of reverse convertibles

- Losses may arise if the underlying asset performs negatively

- In the worst case, a total loss of the capital invested is possible

- The profit is limited to the amount of the interest income

- Investors do not participate in possible dividends on the underlying asset

- Products are exposed to market influences during their term, such as the performance of the underlying asset, volatility and interest rate fluctuations

- Payout and repayment depend on the creditworthiness of the issuer (so-called issuer risk)